One late-night emergency can now cost more than your monthly rent. That’s not drama, that’s just how vet bills look in 2026. A quick ER visit, a few tests, maybe an overnight stay—and suddenly you’re staring at a $2,000–$5,000 estimate.

I think most millennial pet parents don’t have that sitting in a “my cat ate string” fund. That’s where cheap pet insurance comes in. Not as a luxury, but as basic financial first aid. In my opinion, the real question isn’t “Should I get pet insurance?” anymore. It’s “How do I find affordable pet insurance that actually pays out when my pet needs help?”

Why This Guide Exists (and Who It’s For)

This guide is for people who love their pets like family but still have to watch every dollar. If you’ve ever googled “best cheap pet insurance” or “low cost pet insurance” with a knot in your stomach, this is for you.

We’ll unpack how these plans really work, which companies offer genuine budget pet insurance, and how to choose coverage that fits your income and your anxiety level. By the end, I think you’ll know exactly what to buy, what to skip, and how to protect your pet in 2026 without wrecking your budget.

Table of Contents

- What “Cheap” Pet Insurance Actually Means (Without Getting Burned)

- Smart Trade-Offs for Budget Pet Insurance

- Quick-Start: Is Cheap Pet Insurance Even Right for You?

- How Pet Insurance Works in Plain English (So You Don’t Overpay)

- Expert Insights: What Our Research Shows About Cheap Pet Insurance in 2025–2026

- Best Cheap Pet Insurance Plans in 2026: Real Protection on a Budget

- How to Build a Budget-Friendly Policy That Still Covers the Big Stuff

- Real-World Scenarios: What Cheap Pet Insurance Actually Pays For

- Money-Saving Moves That Don’t Backfire

- How to Shop & Compare Cheap Pet Insurance in 20 Minutes

- Conclusion – A Safety Net That Fits Your Life (and Your Pet)

- Frequently Asked Questions (FAQs)

What “Cheap” Pet Insurance Actually Means (Without Getting Burned)

Cheap vs. “Too Cheap to Be Safe”

When people search for cheap pet insurance, they usually mean, “I need real help with big vet bills, but my budget is tight.” That’s very different, in my opinion, from “give me the absolute lowest price on the page.”

Good affordable pet insurance should do three things:

- Cover the big, scary stuff (emergencies, surgeries, serious illnesses).

- Make your share of the bill somewhat predictable.

- Fit into a monthly payment you can live with long-term.

If a policy doesn’t tick those boxes, I think it’s not “cheap” — it’s just risky.

Red Flags That Make Cheap Plans Dangerous

Here’s where low-cost pet insurance can quietly backfire. If a plan is dramatically cheaper than others, in my opinion, you should assume you’re trading away something important and find out what it is.

- Very low annual limits: $2,000–$3,000 a year total. One emergency can blow through that in a night.

- Tiny reimbursement: 50–60%, so you’re still paying most of every bill.

- Long waiting periods: Especially for knees, hips, or cancer. Problems show up before coverage kicks in.

- A wall of exclusions: Buried in the fine print.

Smart Trade-Offs for Budget Pet Insurance

The goal with budget pet insurance isn’t “pay as little as possible.” It’s “pay as little as possible without wrecking coverage.” Smart moves, I think, look like this:

- Raise your deductible a bit instead of slashing your annual limit.

- Drop from 90% to 70–80% reimbursement, but keep accident & illness.

- Skip wellness add-ons if cash is tight and focus on big-ticket risks.

That way, your plan stays cheap — but still shows up when things get serious.

Quick-Start: Is Cheap Pet Insurance Even Right for You?

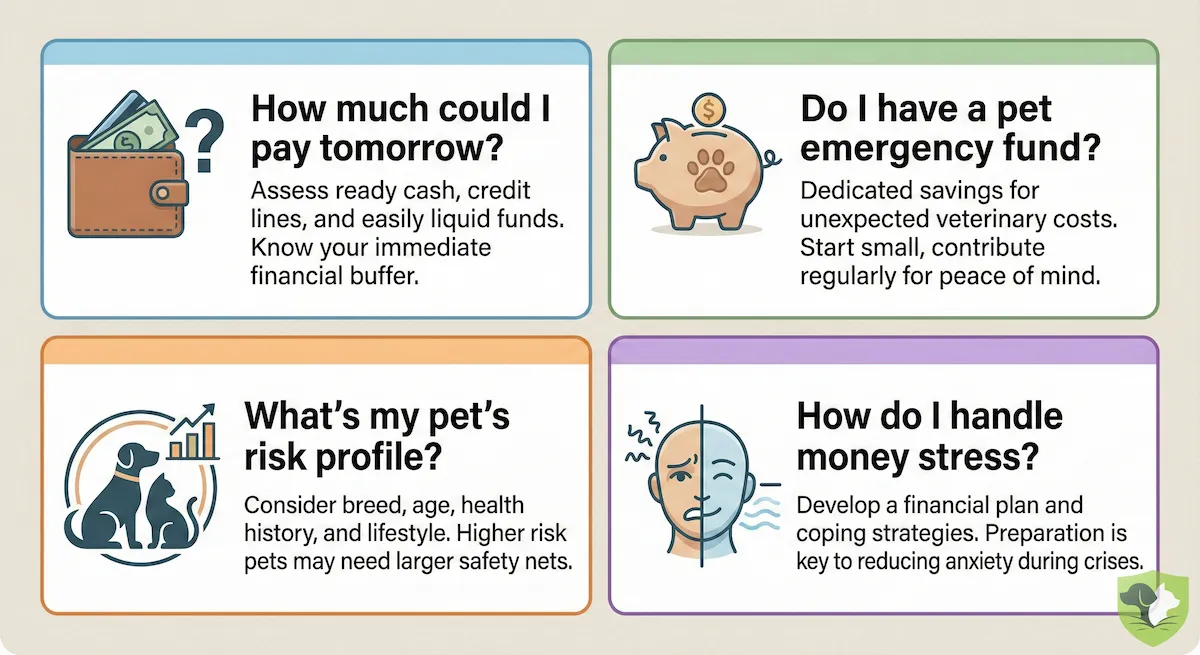

A 4-Question Self-Check

Before you dive into quotes, pause for 30 seconds and ask yourself:

- How much could I pay tomorrow if my pet needed emergency care? $300? $1,000? $3,000? Be honest.

- Do I already have a dedicated pet emergency fund? Or is everything mixed into one stressed-out savings account?

- What’s my pet’s risk profile? Young/healthy, or older, brachycephalic, large breed, or with known quirks?

- How do I handle money stress? I think this matters more than people admit. Does a surprise $2,000 bill keep you up at night?

If your answers are making you sweat a bit, cheap pet insurance is at least worth a serious look.

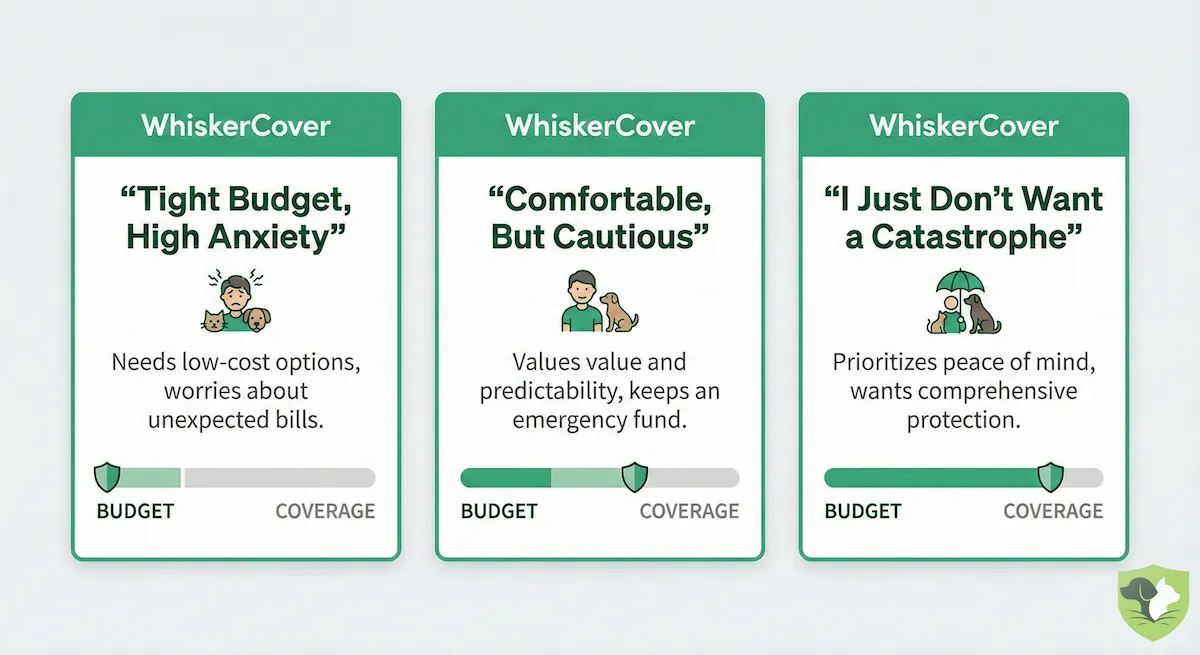

Three Common Buyer Profiles

In my opinion, most people fall into one of these:

- “Tight Budget, High Anxiety”: Little savings, big feelings. You need a budget pet insurance plan that covers big stuff, even if the deductible is higher.

- “Comfortable, But Cautious”: Some savings, but you’d rather not drain it on one accident. A balanced, affordable pet insurance plan with mid-range limits usually fits.

- “I Just Don’t Want a Catastrophe”: You can handle small stuff, but a $6,000 surgery would wreck you. A lean, low-cost pet insurance plan or accident-only policy can be a safety net.

When Cheap Pet Insurance Makes Sense (and When It Doesn’t)

If a surprise vet bill over $1,000 would seriously hurt you, I think cheap pet insurance is worth it. If you have a large, truly separate emergency fund and an older pet with multiple issues, self-insuring might make more sense—just go in with eyes open.

How Pet Insurance Works in Plain English (So You Don’t Overpay)

Types of Coverage

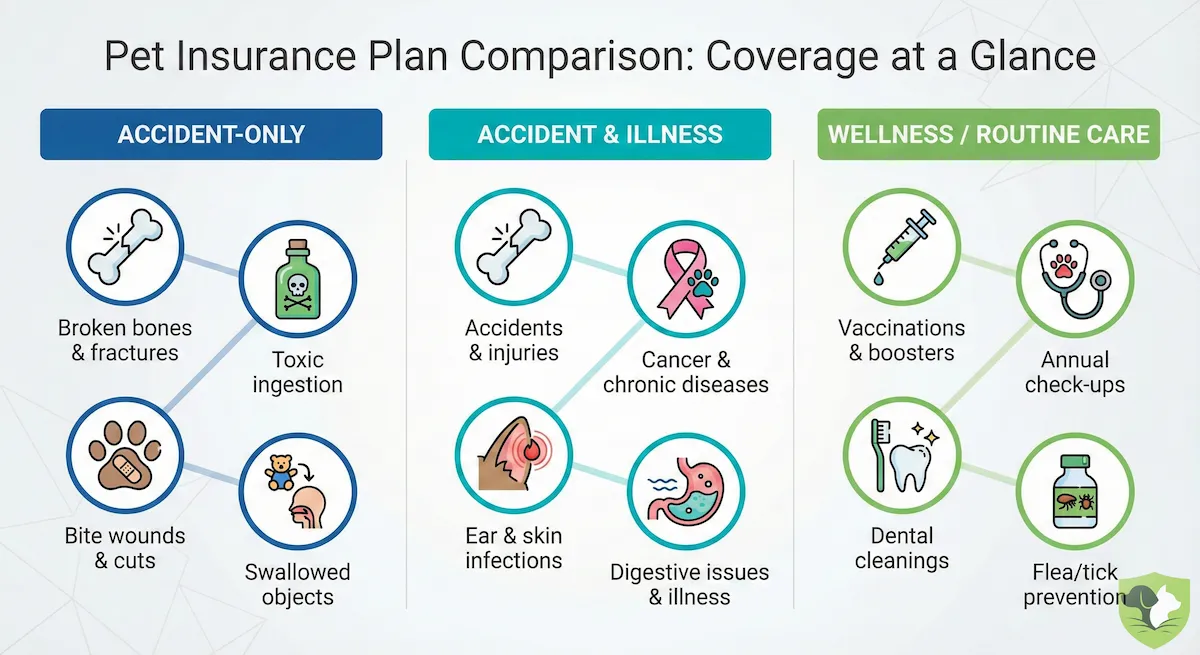

Most plans fall into three buckets:

- Accident-only: Covers things like car accidents, broken bones, and foreign body ingestion. Super low-cost pet insurance, but no illnesses.

- Accident & illness: Covers accidents and stuff like cancer, diabetes, allergies, and infections. This is, in my opinion, where the real value is for most pets.

- Wellness/routine care: Vaccines, checkups, flea meds. Often sold as an add-on. Sometimes useful, sometimes just fancy budgeting.

I think of it like this: accident-only = “bare-bones safety net,” accident & illness = “real protection,” wellness = “nice to have if priced right.”

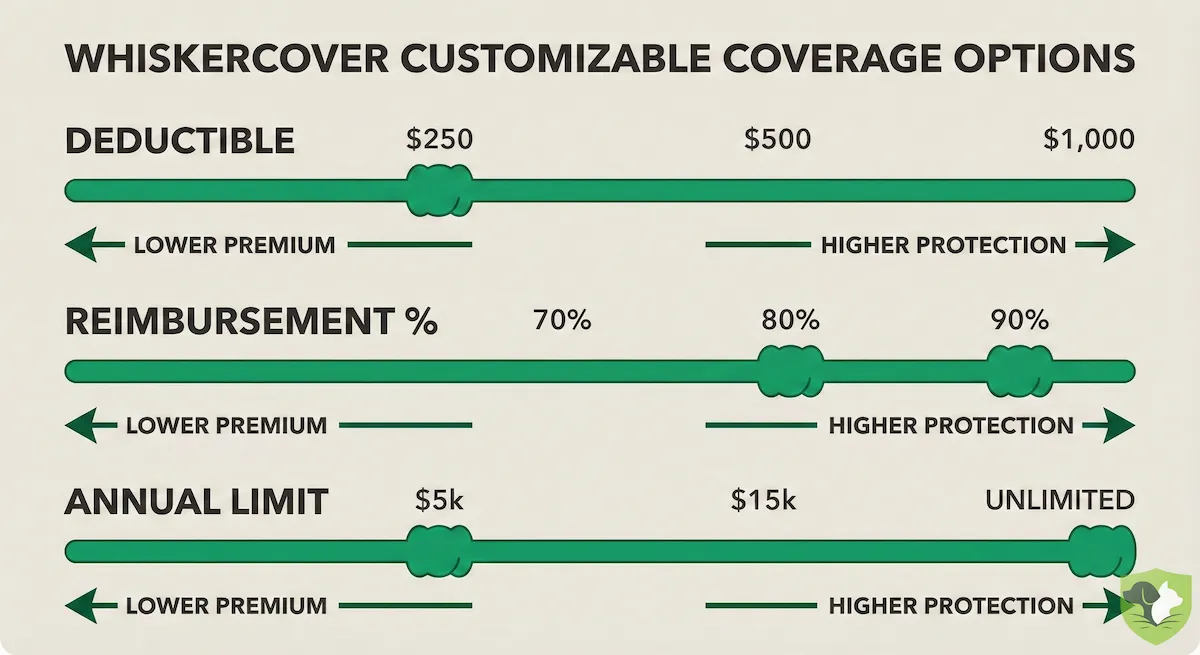

The Three Big Levers That Change Your Price

Every quote tool is basically asking you to set three sliders:

- Deductible: What you pay before insurance kicks in each year (e.g., $250, $500, $1,000). Higher deductible = lower monthly premium.

- Reimbursement %: How much the insurer pays after the deductible (70%, 80%, 90%). Lower % = cheaper, but you pay more on each claim.

- Annual limit: Max they’ll pay in a year ($5k, $10k, unlimited). Smaller limit = cheaper, but easier to hit the ceiling.

In my opinion, the sweet spot for cheap pet insurance is usually: decent annual limit (around common emergency costs), moderate deductible, 70–80% reimbursement.

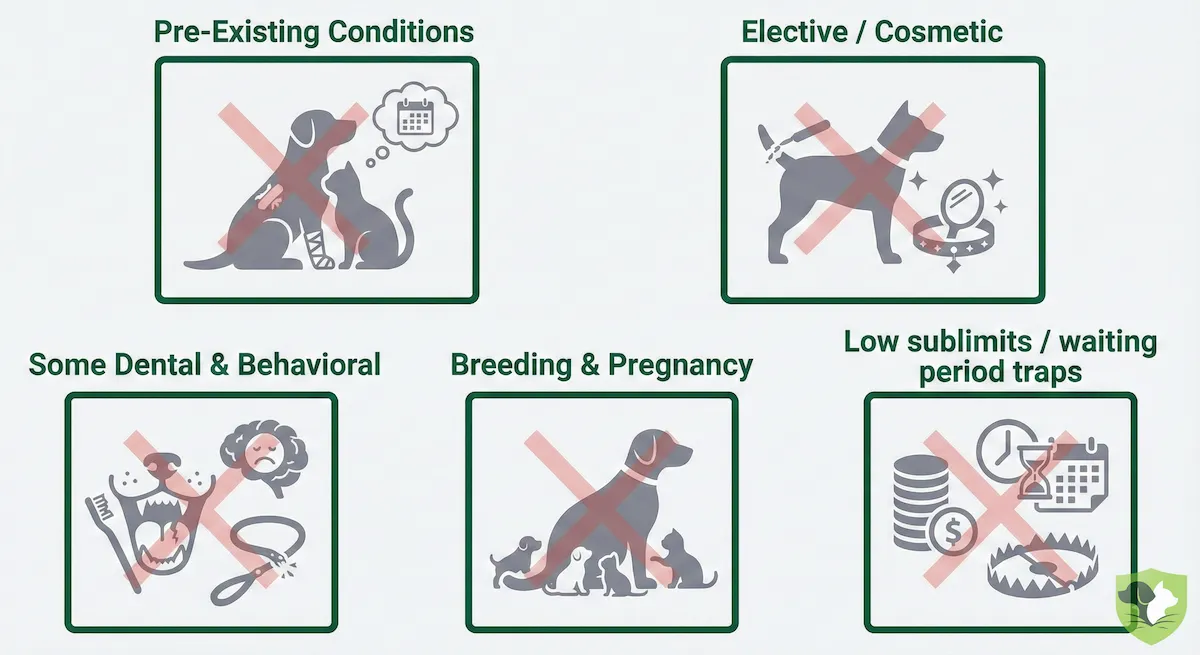

What’s Rarely Covered (and Why It Matters for Budget Shoppers)

Almost every policy excludes:

- Pre-existing conditions (anything that showed up before enrollment).

- Elective procedures (cosmetic, breeding-related).

- Some dental and behavioral issues, depending on the plan.

If a “budget pet insurance” policy looks suspiciously cheap, I’d double-check this section first. The exclusions page tells you more than the marketing page, in my opinion.

How Claims Actually Work in Real Life

The flow is simple: You go to the vet and pay the bill. You submit the invoice and medical notes in the app/portal. The insurer reviews and reimburses you to your bank account. Some providers can pay the vet directly, which I think is a game-changer if you don’t have big cash reserves. The claim process isn’t scary—what matters is how fast and how often they actually pay.

Expert Insights: What Our Research Shows About Cheap Pet Insurance in 2025–2026

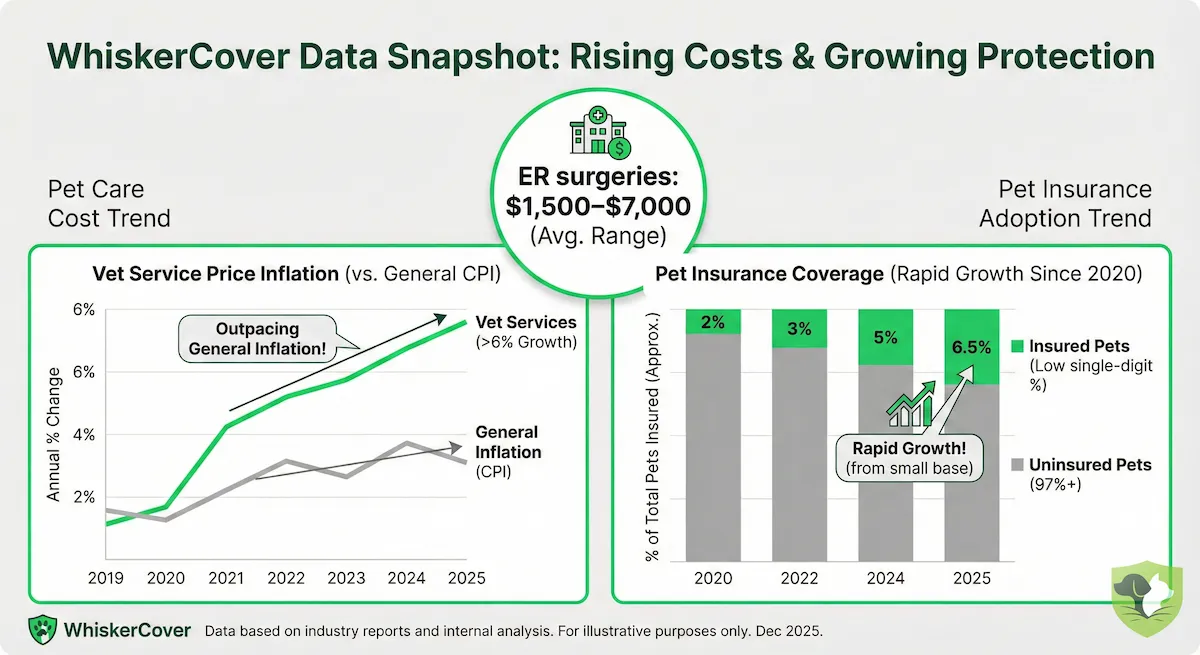

The Data on Rising Vet Costs and Inflation

Vet care isn’t just “a bit pricey” anymore. In our research, vet service prices jumped a little over 6% in a single year, growing faster than general inflation. Emergency surgeries regularly land in the $1,500–$7,000 range, and even a nasty tooth extraction can creep toward a few thousand dollars. In my opinion, that’s exactly the kind of environment where cheap pet insurance stops being optional and starts looking like basic risk management.

Insurance Uptake, Financial Stress, and Care Decisions

Here’s the wild part: only a small slice of U.S. pets are insured (roughly a low single-digit percent of cats and dogs), even though the number of insured pets has grown fast and the market has roughly doubled since 2020. That means most families are still one big vet bill away from a serious money problem. I think that’s why so many people end up googling affordable pet insurance only after they’ve already had a scare.

What Real Owners Say About Value

Owners who actually have coverage are pretty clear: more than nine out of ten say pet insurance is worth the cost. Even over half of people without a policy think it’s a good idea; they’re just worried about price. Insured pet parents also go to the vet more often and earlier, which means problems get caught sooner and treated cheaply. To me, that’s the quiet superpower of low-cost pet insurance.

How Millennials and Gen Z Are Shaping Budget Pet Insurance

Millennials and Gen Z are driving the shift. Pet ownership in those groups has jumped fast, and many are choosing pets before kids. They’re digital, cost-sensitive, and they expect app-based, budget pet insurance options that feel fair. That pressure is exactly what’s creating more and better cheap pet insurance plans for 2026.

Best Cheap Pet Insurance Plans in 2026: Real Protection on a Budget

The Best Cheap Pet Insurance Companies for 2026 (US)

How We Evaluated “Best Cheap Pet Insurance”

If I’m going to call something the best cheap pet insurance, I think it has to clear two hurdles at once: real coverage and a price normal people can actually pay every month. So we started with a broad list of major U.S. providers and newer budget-focused brands, then narrowed it down using the same realistic setup for each:

- Accident & illness coverage (not just accident-only teaser plans).

- Annual limit around $10,000 (or higher).

- 70–80% reimbursement.

- A mid-range deductible most people could handle.

From there, we compared what you’d actually feel as a pet parent: price at that baseline, coverage depth, waiting periods, claims experience, and discounts.

Across that testing, a few names kept showing up with strong, affordable pet insurance value:

- Lemonade: Often among the lowest prices for solid accident & illness coverage, app-first, great for younger pets.

- Pets Best: Very flexible deductibles and limits, strong accident-only option for ultra-tight budgets.

- Figo: Competitive pricing plus 24/7 vet chat, which I think is huge for avoiding unnecessary ER bills.

- Embrace: Not always the absolute cheapest, but their shrinking deductible can make long-term costs surprisingly low.

- MetLife: Good for multi-pet families looking for one budget pet insurance setup across several animals.

- ASPCA / Spot, Healthy Paws, ManyPets, Odie: Each has specific sweet spots (like unlimited coverage or very low starter prices) that make them worth a quote in 2026.

In my opinion, “cheap” only counts if the policy is still there for you at 2 a.m. when something really goes wrong—and that’s exactly what we screened for.

How to Build a Budget-Friendly Policy That Still Covers the Big Stuff

Step 1 – Decide Your “Pain Number”

Before touching any sliders, I think you need one number in your head: What’s the maximum you could pay out of pocket in a bad month? For some people, it’s $300. For others, it’s $1,000 or more. Be honest. This “pain number” is what should guide every decision you make about cheap pet insurance.

Step 2 – Tune Deductible, Reimbursement, and Limits

Now use that number to shape your affordable pet insurance settings:

- Deductible: Higher deductible = lower monthly cost. Just don’t set it higher than your pain number.

- Reimbursement %: 70–80% is a solid sweet spot, in my opinion. 90% is nice, but not always worth the extra premium if money’s tight.

- Annual Limit: Aim for at least around common emergency costs (often $5k–$10k). I think dropping limits too low is riskier than shaving a bit off reimbursement.

Step 3 – Keep the Essentials, Cut the Extras

Your priority for budget pet insurance is simple: Keep accidents + illnesses, realistic annual limit, decent reimbursement. Optional: wellness add-ons, fancy travel riders, niche extras. If you’re choosing between illness coverage and a wellness plan, I’d keep illness coverage every single time.

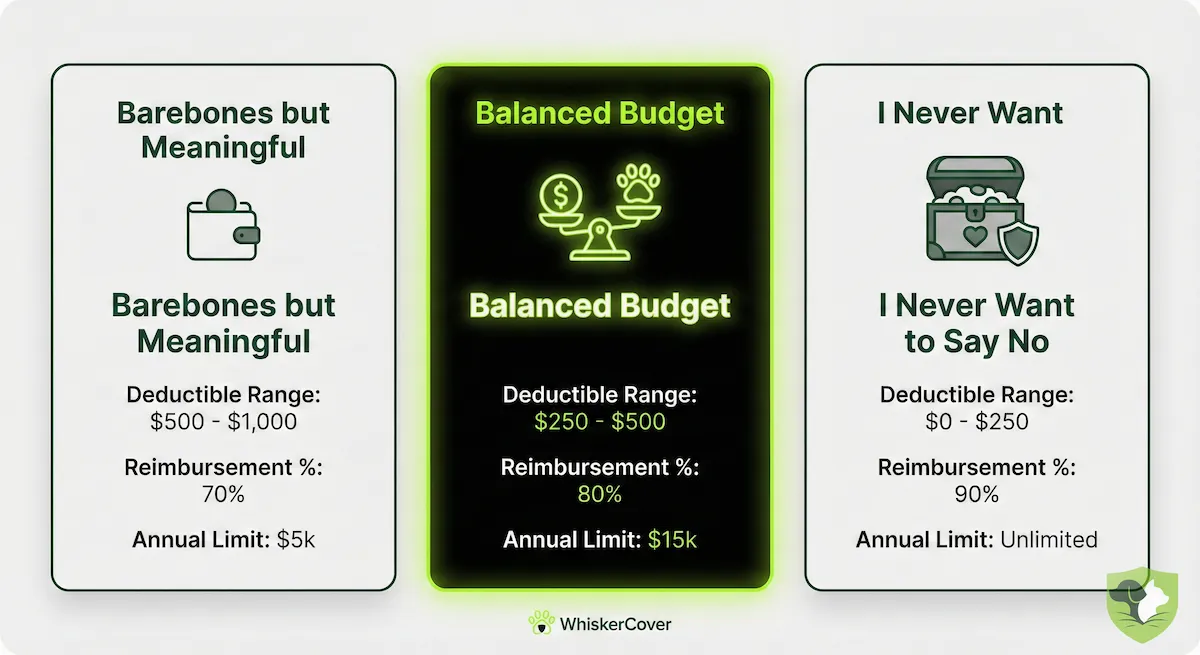

Sample “Baseline Setups” for Different Budgets

- Barebones but meaningful: Accident & illness, higher deductible, 70% reimbursement, mid-range limit.

- Balanced budget: Accident & illness, mid deductible, 80% reimbursement, higher limit.

- “I never want to say no”: Lower deductible, 80–90% reimbursement, high or unlimited limit.

Pick the one that feels closest to your reality, then tweak from there—I think that’s the easiest way to end up with low-cost pet insurance that actually works.

Real-World Scenarios: What Cheap Pet Insurance Actually Pays For

Emergency Surgery – The Classic “Oh No” Moment

Picture this: your dog eats a sock. The bill for imaging, surgery, and an overnight stay hits $4,000.

No insurance: you pay $4,000. Probably on a credit card.

Cheap pet insurance (70% reimbursement, $500 deductible): You pay about $1,700 total.

In my opinion, that’s the difference between “financial disaster” and “painful but manageable.”

Chronic Illness or Cancer

Now imagine your cat is diagnosed with cancer. Treatment over a year ends up at $8,000.

No insurance: you face each invoice alone and might have to say no to some options.

Affordable pet insurance: after your deductible, 70–80% of every chemo visit, scan, and med is reimbursed.

I think this is where cheap plans quietly shine: they spread a brutal year of expenses into something you can actually live with.

No Insurance vs Cheap vs Premium

Take any big event, and the pattern is similar: No insurance means you carry 100% of the risk. Low-cost pet insurance means you keep more risk, but the floor is higher. Premium plan means you pay more monthly for the lowest surprise. In my opinion, even a budget pet insurance plan can be the line between “we can’t afford this” and “let’s do the treatment.”

Money-Saving Moves That Don’t Backfire

Good Ways to Make Pet Insurance Cheaper

If you want cheap pet insurance without wrecking the coverage, start with the “safe” levers. In my opinion, these are almost always good moves:

- Multi-pet discounts if you’ve got a little zoo at home.

- Pay annually instead of monthly if you can swing it (many insurers knock a bit off).

- Bundle discounts when you pair pet insurance with renters or home insurance.

- Employer or shelter deals – lots of people forget to check these.

All of that lowers the price without gutting the policy.

Savings Tactics That Usually Hurt You Later

Some “savings” are really just time bombs, I think:

- Dropping your annual limit so low that one bad night blows it out.

- Cranking your deductible to a level you could never actually pay.

- Choosing accident-only when your real fear is cancer or chronic disease.

The Fine Print That Can Cost You Big

Hidden costs often live in the fine print of affordable pet insurance and low-cost pet insurance plans: Sublimits for hips, knees, or cancer; long waiting periods; tight rules on “bilateral conditions” (both knees, both eyes). With budget pet insurance, I’d always skim the exclusions page before I fall in love with the price.

How to Shop How to Shop & Compare Cheap Pet Insurance in 20 Minutes

Compare Cheap Pet Insurance in 20 Minutes

Prep in 5 Minutes

Grab a notepad (or Notes app) and jot down: Your pet’s age, breed, weight, and health quirks. Your monthly budget for cheap pet insurance. Your “pain number” for a surprise bill (how much you could pay tomorrow). In my opinion, this little prep makes everything else faster and less overwhelming.

Quote Sprint in 10 Minutes

Next, visit 3–5 insurers you’re considering (Lemonade, Pets Best, Figo, Embrace, MetLife, etc.) and run identical quotes:

- Same coverage type (accident & illness).

- Same deductible, reimbursement %, and annual limit.

That way, you’re really comparing affordable pet insurance prices, not different products. I think this is the single biggest mistake people make—they change sliders, then wonder why prices are all over the place.

Compare and Decide in 5 Minutes

Create a tiny comparison grid with columns for: Monthly price, Annual limit, Reimbursement %, Deductible, Big exclusions / waiting periods, and Notable perks. Now circle the 1–2 budget pet insurance options that fit your wallet and your risk comfort. In my opinion, if you can’t explain to yourself in one sentence why you chose a plan, keep comparing for another five minutes.

Conclusion – A Safety Net That Fits Your Life (and Your Pet)

What “Good Enough” Protection Looks Like

You don’t need a perfect policy. You need good enough protection that you’ll actually keep paying for it. In my opinion, that usually means: Accident & illness coverage, a deductible you can handle in a bad month, a limit that roughly matches real emergency costs, and 70–80% reimbursement. If your plan hits those points and still fits your budget? Congrats. You’ve basically found cheap pet insurance that works. It may not be fancy, but it’s a real safety net.

Your Next 20-Minute Action Plan

Here’s what I think you should do next:

- Decide your monthly budget and your “pain number” for emergencies.

- Shortlist 3–5 insurers (Lemonade, Pets Best, Figo, Embrace, MetLife, etc.).

- Run identical quotes and fill in a tiny comparison grid.

- Pick the affordable pet insurance option that you understand and can explain in one sentence.

That’s it. No endless scrolling. No analysis paralysis. Just one small step that future-you—and your pet—will probably be very glad you took.

Frequently Asked Questions (FAQs)

Is Cheap Pet Insurance Still Worth It with a High Deductible?

Yes, if the numbers make sense. A higher deductible can turn a solid plan into cheap pet insurance without gutting coverage. In my opinion, it’s worth it as long as the deductible is an amount you could realistically pay in a bad month.

Accident-Only vs Accident & Illness: What’s Better on a Budget?

Accident-only is the lowest-cost pet insurance, but it won’t help with cancer, allergies, diabetes, or most “real-life” vet issues. I think accident & illness, tuned to your budget, is the better long-term value for most pets.

Will My Premium Jump If I Use the Insurance?

Insurers can raise rates over time for everyone, not just you. Claims history might influence things a bit, but age, inflation, and vet costs matter more. Expect affordable pet insurance to creep up, not suddenly triple.

Can I Switch Insurers Later If I Find a Better, Cheaper Plan?

You can switch, but pre-existing conditions reset. That means anything diagnosed before the new policy likely won’t be covered. In my opinion, only switch budget pet insurance if the new plan is clearly better, even with those exclusions.

Cheap Pet Insurance vs Pet Emergency Fund – Which Wins?

Both help in different ways. Insurance protects you from big, early hits; a fund works best if you have time to build it. I think the sweet spot is a modest emergency fund plus cheap pet insurance for true disasters.

Is Cheap Pet Insurance for Older Pets Ever a Good Deal?

Sometimes. Premiums are higher and exclusions tougher, but a simple budget pet insurance plan can still soften one big emergency. Run quotes and compare them to what you’d actually be willing to spend out-of-pocket.

WhiskerCover is reader-supported. When you click on links to pet insurance partners on our site and purchase a policy, we may earn a commission at no extra cost to you. Learn more about how we make money.