A massive vet bill doesn’t feel like a “pet expense.” It feels like an emergency you didn’t agree to. One minute, your dog is zooming around the living room. Next, you’re in a clinic being quoted a number that looks more like a used car than a medical treatment.

In that moment, you’re not just scared for your dog. You’re scared of your bank balance, too. That’s the brutal truth most dog parents discover the hard way: love doesn’t protect you from invoices.

Modern vet care can do incredible things, but it’s built on scans, specialists, and surgeries that add up fast. If you don’t have a plan, you’re forced into ugly choices—delay treatment, cut corners, or take on debt and hope nothing else goes wrong this year.

Dog insurance is simply a way to stop money from having the loudest voice in that room. You pay a predictable monthly amount so that when something big happens, you’re not starting from zero.

This guide will walk you through how dog insurance works, what it really costs, and how to choose coverage that lets you say “yes” to care when your dog needs you most.

Table of Contents

- Dog Insurance Basics: What Is It, Really?

- How Dog Insurance Works From Sign-Up to Payout

- Coverage in Real Life, Not Legalese

- Dog Insurance Cost – From Ballpark Numbers to Exact Quotes

- Is Dog Insurance Worth It? A Simple Decision Framework

- How to Choose the Best Dog Insurance for Your Dog

- Side-by-Side Example: Same Dog, Three Policies

- Dog Insurance by Life Stage

- Why Breed Matters So Much in Dog Health Insurance

- Expert Insights: What the Data Says in 2026

- Wrapping It All Up: Peace of Mind for You and Your Dog

- Frequently Asked Questions (FAQs)

Dog Insurance Basics: What Is It, Really?

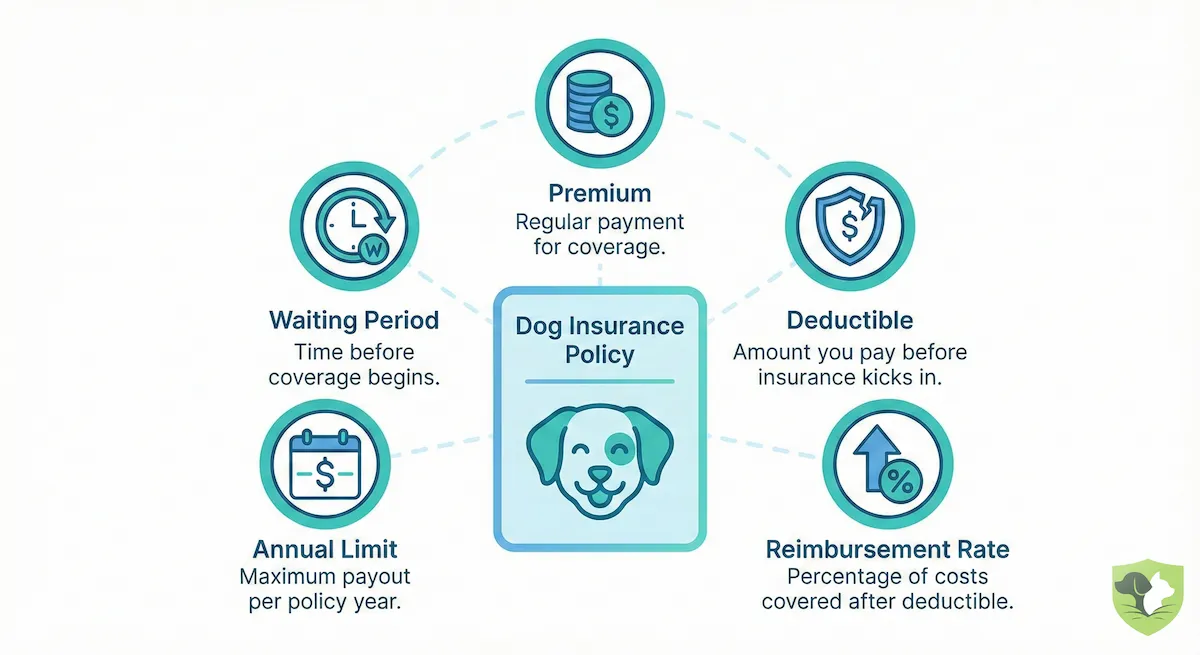

Dog insurance (or pet insurance for dogs) is a simple idea: you pay a monthly fee so part of your vet bills is paid back when your dog gets sick or hurt. It’s not a savings account, and it’s not a discount card. It’s a contract that says, “If these things happen, we’ll cover this share of the bill.”

Here’s how it usually works. You take your dog to any licensed vet. You pay the invoice. Then you submit a claim to your insurer through an app or website. After they review the visit and check it against the policy rules, they send money back to you.

A few key terms you’ll see everywhere:

- Premium: What you pay each month to keep coverage active.

- Deductible: How much you pay before insurance starts helping.

- Reimbursement rate: The percentage of the covered bill the insurer pays back.

- Annual limit: The maximum the policy will pay in a year.

- Waiting period: Time after you buy before new problems are covered.

Understand these five ideas, and most dog insurance fine print already starts to make sense.

How Dog Insurance Works From Sign-Up to Payout

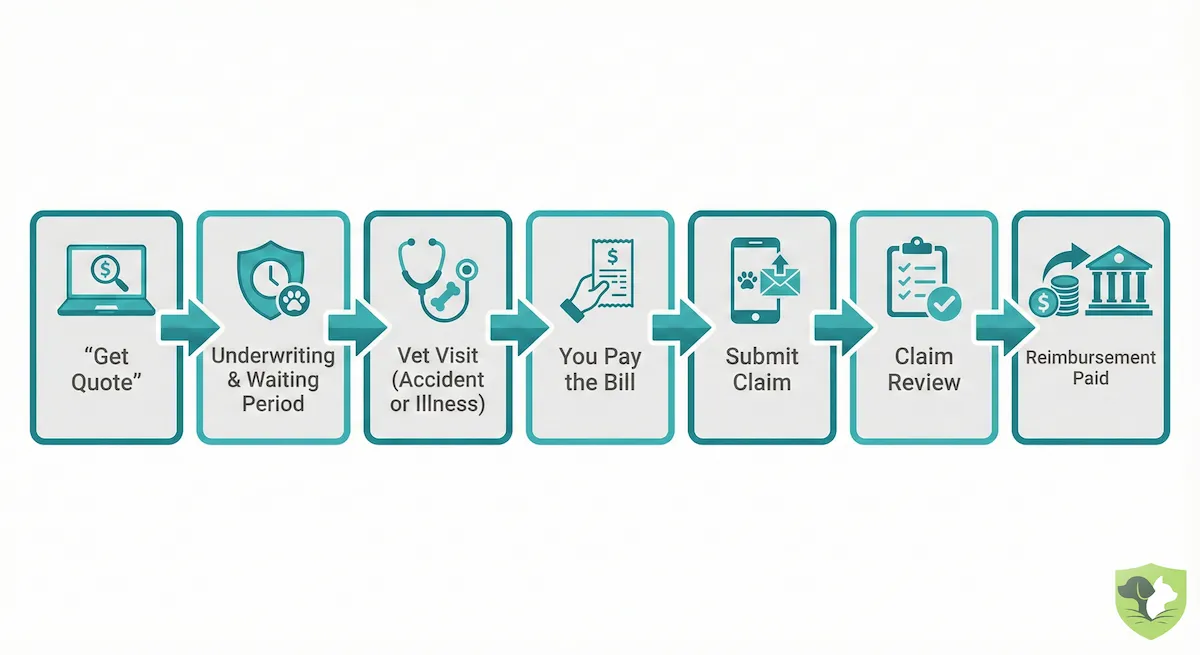

If you wanted to sketch the process, it's really just: Vet visit → Pay bill → Submit claim → Insurer reviews → Reimbursement hits your account.

1. Before Your Dog Ever Gets Sick or Hurt

The journey starts before anything is wrong. You go online, plug in your dog’s age, breed, weight, and your ZIP code, and answer a few health questions. In my opinion, this is the most important moment, because what you say here shapes everything that happens later.

The insurer uses that info to “underwrite” your policy. In plain language, they look at your dog’s risk profile and decide what they’ll cover, how much it will cost, and what counts as a pre-existing condition.

Anything your dog has already shown signs of – even if it’s not fully diagnosed – can be listed as pre-existing and excluded going forward. That’s why I think insuring dogs earlier, before problems pile up in the medical record, usually works out better.

Once you buy the policy, a waiting period kicks in. During this time, new issues generally aren’t covered yet. It can feel annoying, but it’s there to stop people from buying insurance on the way to the ER.

2. When Something Happens (Accident or Illness)

Fast-forward. Your dog eats a sock, tears a ligament, or wakes up with scary symptoms. You choose any licensed vet or emergency clinic, go in, and approve the tests and treatment your dog needs. At checkout, you pay the full bill yourself. That “pay first, claim later” setup is how most pet insurance for dogs works.

3. Filing a Claim

After the visit, you submit a claim through an app or website. You upload the itemized invoice, any medical notes the clinic provides, and answer a few basic questions. Some companies offer pre-approval or direct pay for big procedures, but in day-to-day life, it’s usually you → claim → reimbursement.

4. Getting Reimbursed

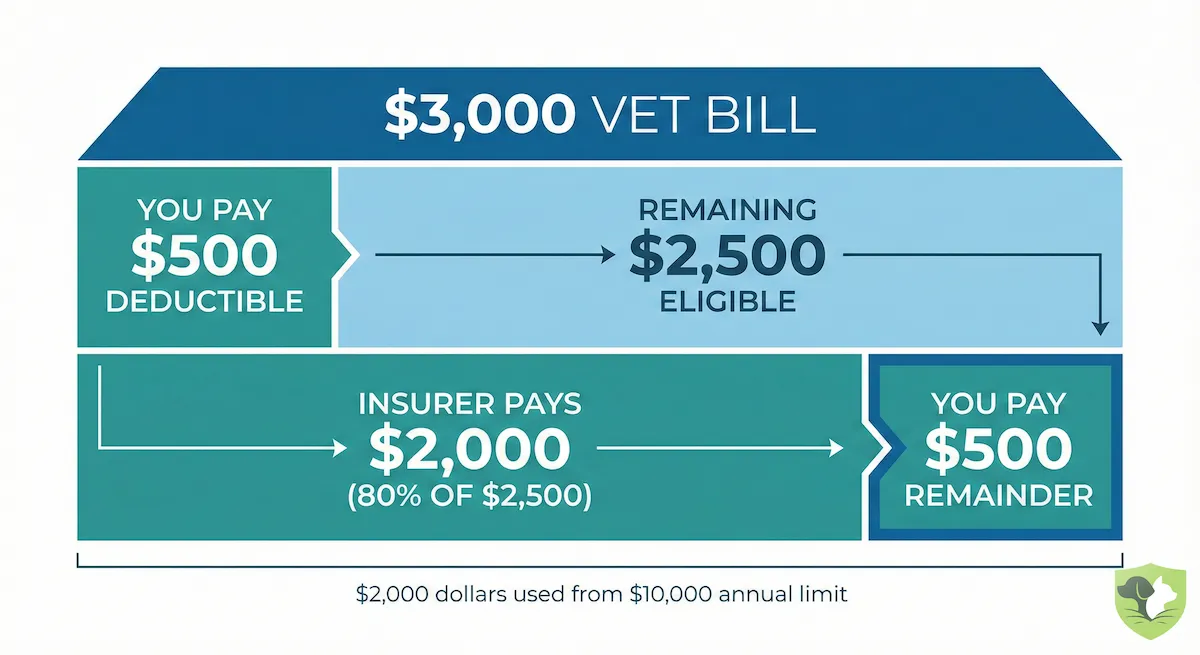

Once the insurer reviews your claim, they do the math based on your policy. Let’s say you had a $3,000 surgery, a $500 annual deductible, 80% reimbursement, and a $10,000 annual limit.

- First, you cover your $500 deductible.

- That leaves $2,500 of eligible costs.

- At 80% reimbursement, the insurer pays $2,000.

You've paid $1,000 total ($500 deductible + $500 remaining bill), and your policy has used up $2,000 of its yearly limit.

Coverage in Real Life, Not Legalese

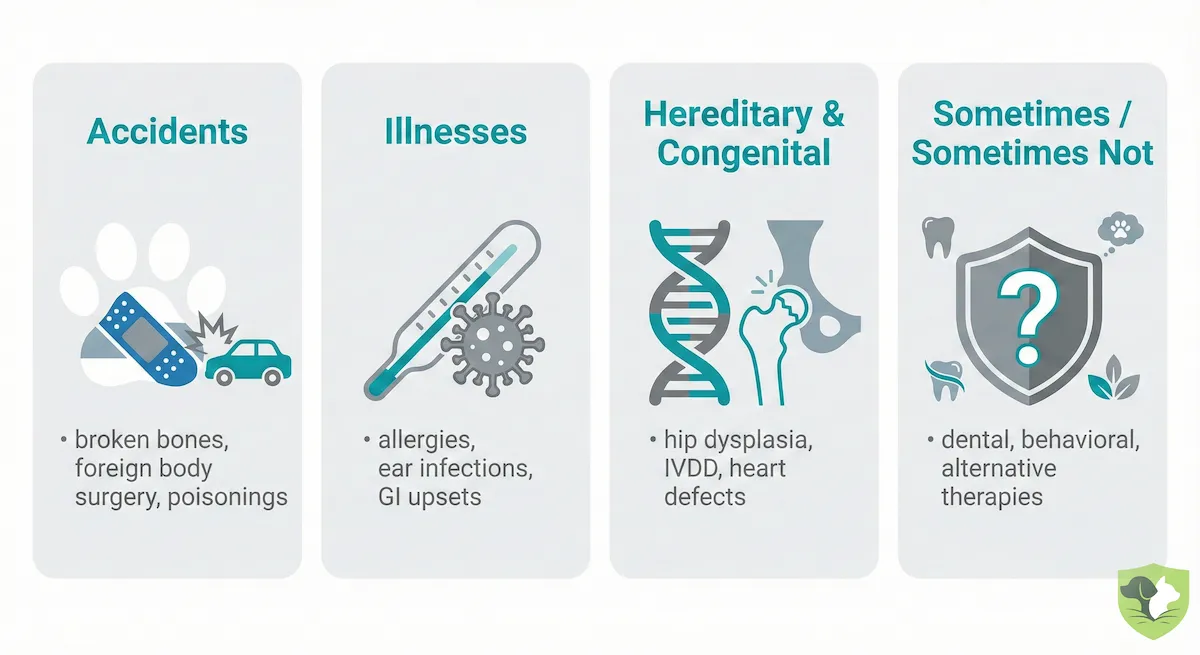

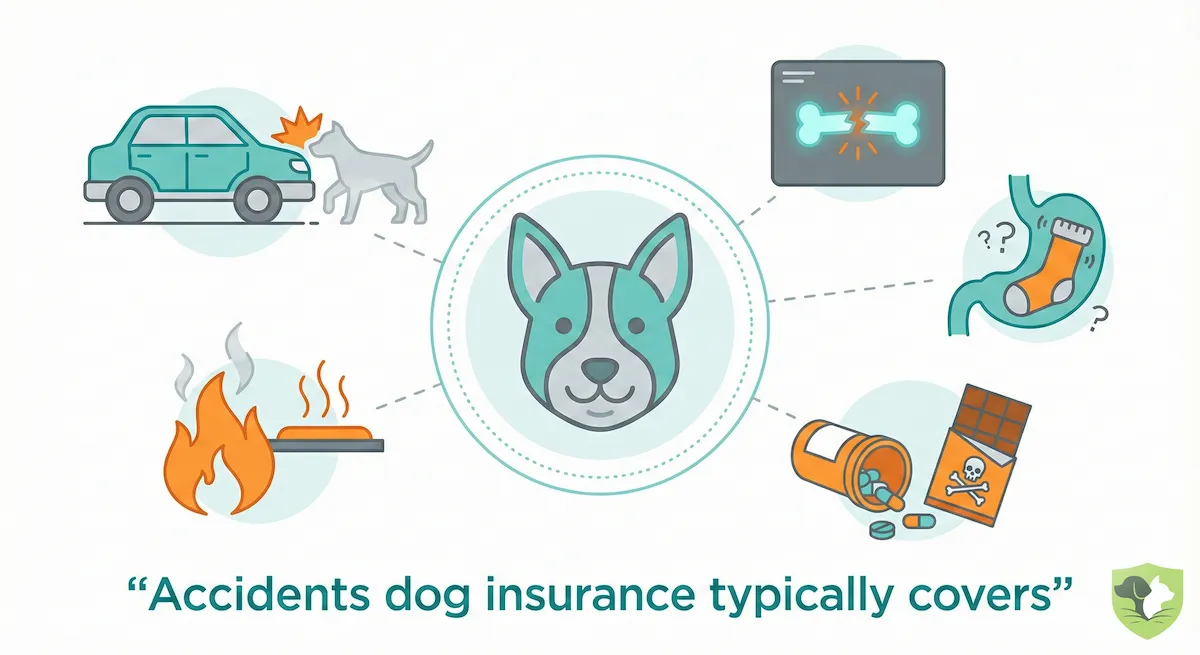

When you strip away the policy-speak, most dog insurance is built around a few big buckets: accidents, illnesses, inherited problems, and then a grey zone of “it depends.”

Accidents

This is the easy part. If your dog is hit by a car, breaks a leg on the stairs, swallows a toy, or licks up something toxic, accident cover is usually what kicks in. It typically helps with the whole chain: exam, X-rays or scans, surgery, meds, and even an overnight stay if needed.

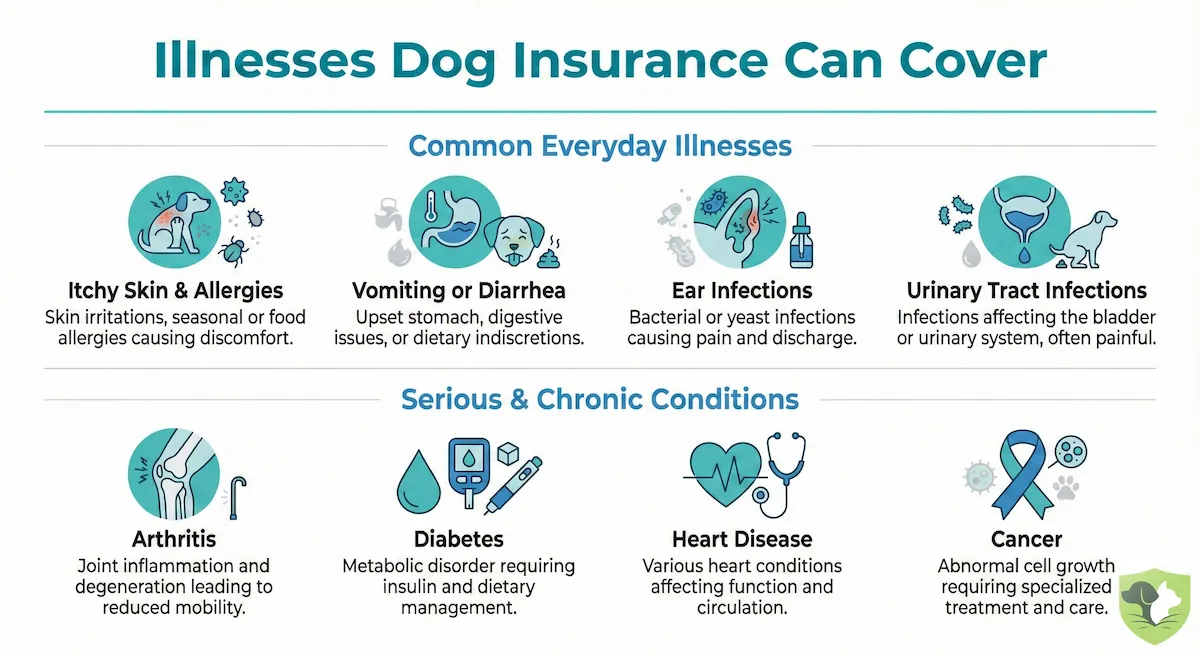

Illnesses

Most real-world claims come from sickness rather than dramatic mishaps. Skin allergies, gut troubles, ear infections and urinary issues show up again and again in insurer data, along with bigger diagnoses like arthritis, diabetes, heart disease and cancer.

In my opinion, this is where good pet insurance for dogs quietly earns its keep, because these conditions often come back year after year.

Hereditary and Congenital Issues

Things like hip dysplasia, IVDD (spine problems), certain heart defects or breed-linked cancers are often treatable but expensive. Many modern dog health insurance plans will cover them if your dog had no signs or diagnosis before the policy started, and any waiting period has passed. Others limit or exclude them, especially for high-risk breeds, so the fine print here really matters.

Sometimes Covered, Sometimes Not

Dental is a perfect example. Treatment for broken teeth or serious dental disease is often included under accident/illness cover, but routine cleanings are usually only reimbursed if you add a separate wellness plan.

Behavioural issues (like anxiety-related chewing) and alternative therapies (acupuncture, hydrotherapy, laser) may be fully covered, partly covered, or excluded depending on the insurer.

Common Exclusions

Most policies will not pay for:

- Pre-existing conditions

- Elective or cosmetic procedures

- Breeding, pregnancy, whelping

- Boarding, grooming, routine food, vitamins and many supplements (unless specifically prescribed and allowed)

Later in this guide, I’ll lay all of this out in a simple “Covered / Sometimes / Not Covered” table with one real-world example in each row so you can see, at a glance, where your dog’s situation fits.

Dog Insurance Cost – From Ballpark Numbers to Exact Quotes

Let’s talk money. When people ask, “How much does dog insurance cost?” the honest answer is: it depends, but there are solid ballparks.

Recent industry data puts the average monthly premium for dog health insurance somewhere in the $50–$65 range for a standard accident-and-illness policy. Cheaper accident-only plans can dip into the $20s, while rich “everything covered” policies for certain breeds can easily push past $100 a month.

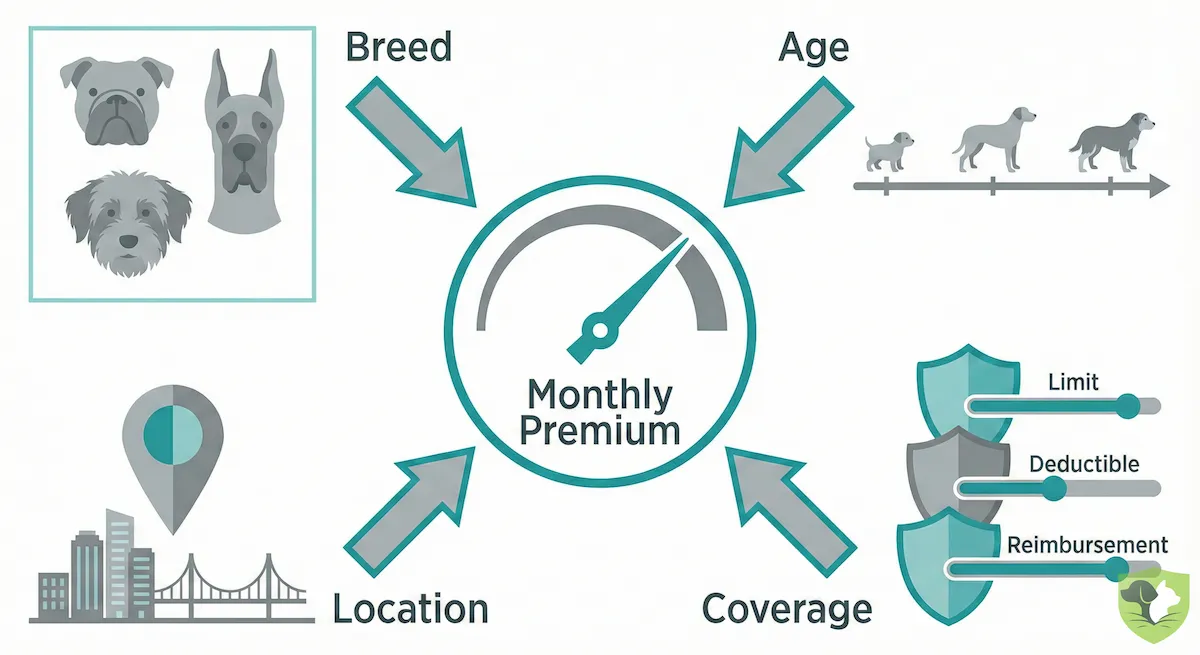

Why the spread? Insurers price pet insurance for dogs based on risk:

- Breed: High-risk breeds (big, very active, or flat-faced dogs) cost more than small, mixed breeds.

- Age: Puppies are usually cheaper; premiums rise as your dog gets older.

- Location: Big-city vet clinics with higher fees push premiums up.

- Coverage: Higher annual limits, lower deductibles and higher reimbursement rates all raise the price.

There’s also the inflation problem. Vet care costs have climbed far faster than general prices in the last decade. In many places, the cost of veterinary services has grown roughly two to three times faster than overall inflation, and some countries have seen treatment prices jump around 60% in eight years. Surgeries that used to be a few thousand dollars now routinely land in the $3,000–$7,000 range or more, especially for orthopedic repairs or foreign-object removals. Dog insurance costs have followed that curve because those are the claims insurers are paying.

To make this more concrete, here are three rough scenarios for a mid-cost U.S. city:

- 2-year-old mixed-breed, $5,000 annual limit, 80% reimbursement, $250 deductible: roughly $35–$45 per month.

- 4-year-old Golden Retriever on the same plan: often $60–$80 per month.

- 9-year-old newly insured senior dog: $90+ per month, with more exclusions and fewer plan options.

The goal isn’t to find the absolute cheapest number, but to choose a dog insurance cost that fits your budget and still meaningfully protects you from a big vet bill.

Is Dog Insurance Worth It? A Simple Decision Framework

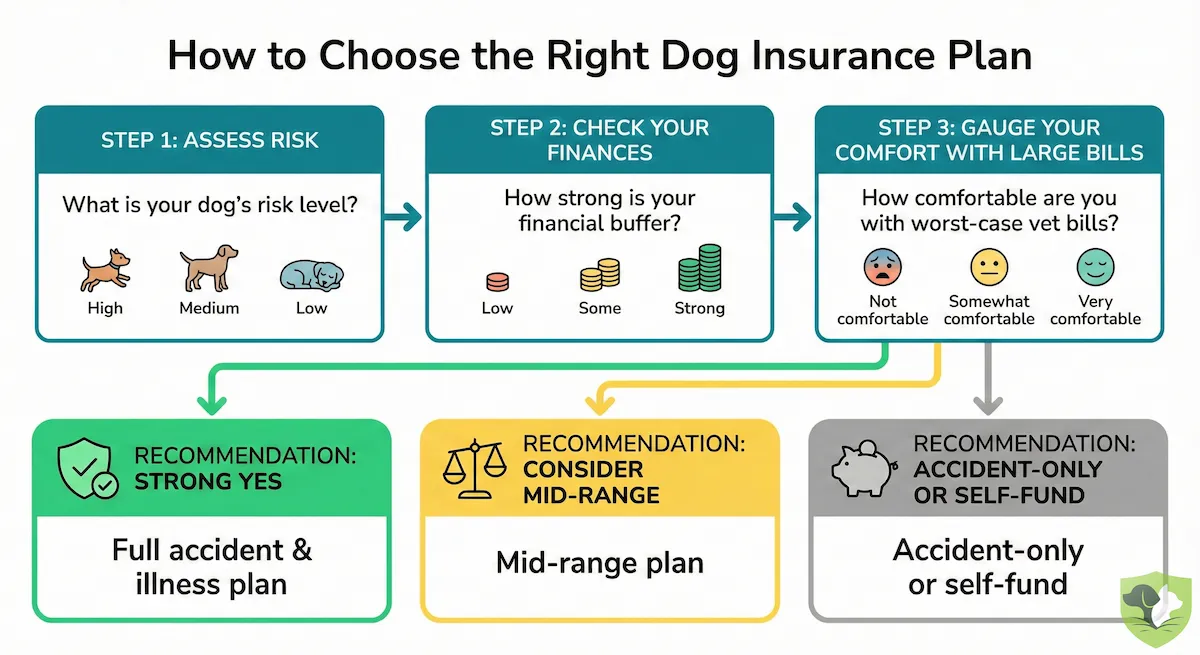

“Is dog insurance really worth it?” is the question everyone asks, and annoyingly, the answer is “it depends.” But it doesn’t have to be a guess. You can walk through a few simple checks and get to a clear yes/no for your own dog.

First, look at your dog’s risk. Some dogs are walking claim machines: big breeds with joint issues, flat-faced dogs with breathing problems, or super-active “I ate another sock” types. Industry data shows the average claim for pets sits in the mid-hundreds of dollars, with multiple claims per policy each year, and serious conditions like orthopedic surgery or cancer easily jumping into the thousands (and in rare cases, much higher).

Second, look at your financial buffer. Could you comfortably handle a $1,000–$5,000 vet bill tomorrow without taking on debt or delaying care? Many owners say they would struggle with even a mid-range unexpected bill, and a big share already end up borrowing or cutting back on treatment because of money. If that sounds like you, paying a predictable dog insurance cost each month can be a lot kinder on your nerves.

Third, be honest about your tolerance for worst-case scenarios. Could you live with saying no to a recommended surgery or advanced treatment because the cash just isn’t there? For some people, that’s unthinkable; for others, strict budget reality wins. Rising vet bills and even pet abandonment linked to costs show how real this pressure has become.

As a quick gut check:

- High-risk dog + low savings → dog insurance is usually a strong yes.

- Medium-risk dog + some savings → consider a higher deductible, mid-range plan.

- Low-risk dog + solid emergency fund → maybe a slim accident-only plan or self-funding is enough.

How to Choose the Best Dog Insurance for Your Dog

Choosing the best dog insurance isn’t about finding a magic brand. It’s about matching a policy to your dog and your bank account. Here’s a simple way to do it.

Step 1: Set your non-negotiables

Look for a dog health insurance plan that:

- Covers accidents and illnesses, not accidents only.

- Includes hereditary and chronic conditions (not just “one year” of treatment).

- Lets you use any licensed vet or emergency clinic.

- Has clear waiting periods and exclusions you can actually understand.

Step 2: Adjust the dials

You control three levers that drive dog insurance cost:

- Deductible: higher deductible, lower monthly premium (and vice versa).

- Reimbursement %: usually 70%, 80% or 90%; higher means you get more back but pay more each month.

- Annual limit: the most the policy will pay in a year; $5k is bare-bones, $10k+ is safer for big emergencies.

Step 3: Ask these questions before you buy

- Are exam fees covered?

- How are bilateral issues (both knees, both eyes) handled?

- What exactly is covered for dental illness?

- How long do claims usually take to be paid?

- How much can premiums rise as my dog ages?

Use those answers to compare 3–4 pet insurance for dogs quotes side by side and circle the one that feels both affordable and genuinely protective.

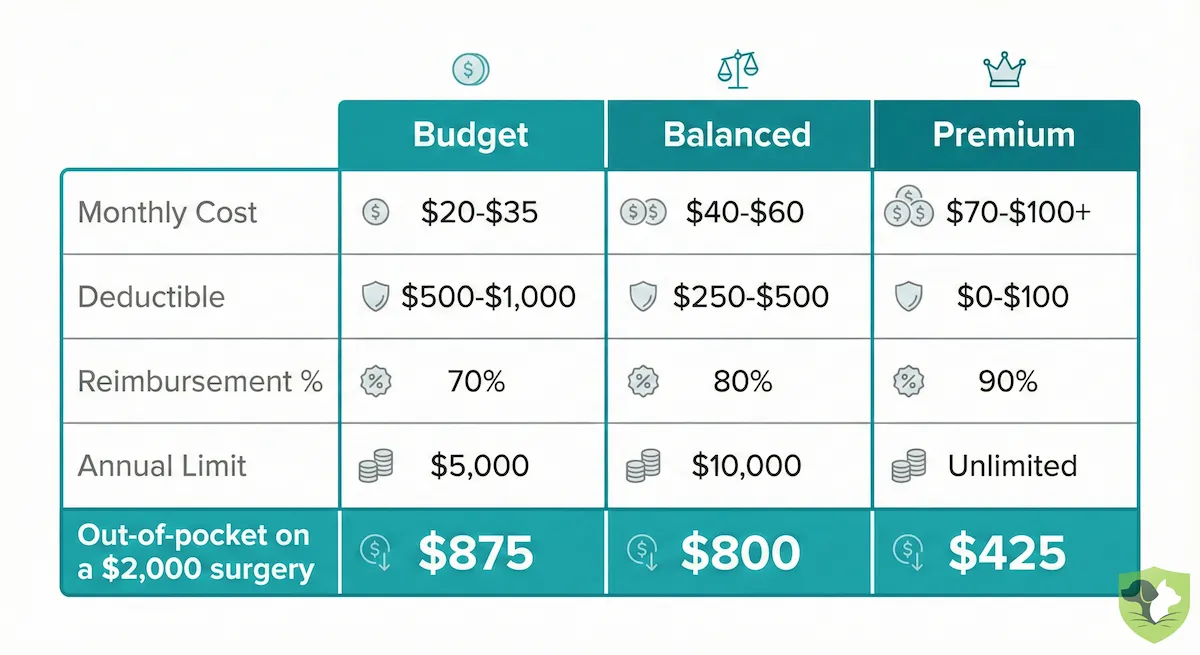

Side-by-Side Example: Same Dog, Three Policies

Let’s make this real. Same dog: 3-year-old, 40 lb mixed-breed, spayed female, mid-cost city.

| Plan Type | Monthly Cost | Deductible | Reimbursement | Annual Limit |

|---|---|---|---|---|

| Budget | $35 | $750 | 70% | $5,000 |

| Balanced | $50 | $500 | 80% | $10,000 |

| Premium | $75 | $250 | 90% | $20,000 / Unlimited |

Now picture a $2,000 emergency surgery. Out-of-pocket on a $2,000 bill:

| Plan Type | Bill | Deductible | Remaining | You Pay % | Insurer Pays | Your Cost |

|---|---|---|---|---|---|---|

| Budget | $2,000 | $750 | $1,250 | 30% ($375) | $875 | $1,125 |

| Balanced | $2,000 | $500 | $1,500 | 20% ($300) | $1,200 | $800 |

| Premium | $2,000 | $250 | $1,750 | 10% ($175) | $1,575 | $425 |

Same dog, same surgery, three very different totals. This is the number that really matters. The goal is to find the balance between the monthly premium and that final "Your Cost" number.

Dog Insurance by Life Stage

A good dog insurance plan should age with your dog. What makes sense for a wild puppy isn’t always right for a grey-muzzled senior.

Puppies

With puppies, I think the big focus is accidents and early illnesses. They chew, swallow, fall, and bounce off everything. Starting coverage early means fewer “pre-existing condition” exclusions later, because most issues haven’t shown up yet. It also helps if something serious is picked up in that first year, like congenital heart problems or joint issues.

Adult Dogs

For healthy adult dogs, the goal is balance. You’re protecting against surprise injuries and the first wave of chronic issues (allergies, joint pain, tummy troubles) without overpaying. This is often the sweet spot to lock in a solid accident-and-illness plan, then fine-tune the deductible and annual limit so the premium fits your budget.

Senior Dogs

With seniors, the challenge is choice. Many insurers either charge much higher premiums, add more exclusions, or stop accepting new enrollments above a certain age. Existing policies can be lifesavers here because ongoing conditions are usually still covered as long as you keep the plan active. Dropping or switching late in life can mean losing protection right when your dog is most likely to need expensive care.

Why Breed Matters So Much in Dog Health Insurance

Whether we like it or not, insurers judge your dog by their genes. Some breeds are simply more expensive to treat, and that shows up directly in the premium.

Flat-faced breeds like French Bulldogs, Pugs and Bulldogs sit at the top of many “most expensive to insure” lists. They’re magnets for breathing problems, eye issues and skin folds that get infected easily, so insurers expect more frequent, higher bills.

Big, deep-chested breeds – think Great Danes, German Shepherds, Rottweilers and similar – have their own set of red flags: hip and elbow dysplasia, cruciate ligament tears, heart disease and bloat (a life-threatening stomach twist). Those conditions often need surgery or long-term medication, which makes coverage pricier too.

On the other hand, mixed-breed dogs are often cheaper to insure because they’re statistically less likely to inherit specific genetic disorders, even though they still get the “big three” claim types: skin problems, tummy troubles and ear infections.

In the finished article, this is a great place for a simple chart: high-risk breeds in one column, their most common issues in the next, and a note on what you’d want your policy to cover for each.

Expert Insights: What the Data Says in 2026

When you zoom out from individual stories and look at the numbers, a few things jump out.

- Claims are not rare events: One recent analysis found the typical policy generates just over three claims a year, with the average claim in the U.S. sitting in the mid-hundreds of dollars. That’s not just “one big crisis” — it’s a steady drip of real costs.

- Skin and allergy issues quietly dominate the charts: Large insurers report that allergic skin disease has been the top dog claim for more than a decade, accounting for around a fifth of all dog claims in some datasets and hundreds of thousands of invoices a year. It’s not glamorous, but it’s expensive.

- Emergencies are where people panic: An ER exam alone averages around $100 in 2025, and the total bill for an emergency visit can easily run from a few hundred to several thousand dollars once tests and treatment are added.

- The market is exploding because costs are: The global pet insurance market has climbed into the high-teens billions of dollars and is projected to keep growing fast, driven largely by rising vet prices and more owners trying not to be caught off guard.

Put bluntly: the data shows that vet bills are frequent, rising, and concentrated in a few pricey problem areas — exactly where solid dog insurance earns its keep.

Wrapping It All Up: Peace of Mind for You and Your Dog

When you strip everything back, dog insurance is really about buying choices, not paperwork. It’s the choice to say “yes” to treatment without doing mental gymnastics in the waiting room.

It’s knowing that if your dog has a bad day, it doesn’t have to become the day your savings disappear. You don’t need a perfect policy. You just need one that fits your dog, your risk tolerance, and your budget.

Take ten minutes, compare a few plans, and pick a starting point. Future you — and the dog snoring on your couch — will be seriously grateful.

Frequently Asked Questions (FAQs)

What’s the best age to get dog insurance?

As early as possible. Insuring a puppy or young dog means fewer pre-existing conditions, broader coverage options, and usually lower dog insurance costs over time.

Can I get pet insurance for dogs after my dog is already sick?

You can buy a policy, but that specific illness (and related issues) will usually be excluded as a pre-existing condition. Insurance is for future problems.

Does dog insurance cover dental work?

Most plans cover dental accidents and serious dental illness, but not routine cleanings unless you add a wellness option. Always check the dental section of the policy.

Can I use any vet?

Most dog health insurance plans let you use any licensed vet, emergency clinic, or specialist. You pay the bill, then claim it back.

What’s the difference between dog insurance and a wellness plan?

Dog insurance handles big, unexpected costs (accidents, illnesses). Wellness plans help with predictable routine care like vaccines and checkups.

Can I change my deductible later?

Many insurers let you change your deductible or annual limit at renewal, but not mid-policy year. Changes can affect both coverage and price.

WhiskerCover is reader-supported. When you click on links to pet insurance partners on our site and purchase a policy, we may earn a commission at no extra cost to you. Learn more about how we make money.