It is the question every pet parent fears. It’s 2:00 AM, and the emergency vet hands you a tablet. The estimate for your dog’s surgery isn't $500—it is a staggering $10,000 or more.

Then comes the devastating pause: "How do you want to proceed?"

In 2026, this is the reality. We have moved past the days of "wait and see" medicine. Today, the "standard of care" involves MRIs, chemotherapy, and complex orthopedic reconstruction.

While general inflation has stabilized, veterinary service costs continue to rise, driven by advanced technology and corporate consolidation. For millennials, insurance often feels like just another subscription. But viewing it as a simple Return on Investment is a math error.

If your pet stays healthy, you will lose money on premiums—and that is the best-case scenario.

The core thesis is simple: Pet insurance in 2026 is not an investment strategy; it is a critical financial instrument. It converts a potential $20,000 household liability into a predictable monthly cost, ensuring you never have to choose between your bank balance and your best friend’s life.

Table of Contents

- The New Math of Vet Care: Why Costs Are Soaring

- The Financial Breakdown: Premiums vs. Payouts

- Is Dog Insurance Worth It?

- Is Cat Insurance Worth It? (The Indoor Cat Fallacy)

- Pros and Cons of Pet Insurance (The Unfiltered Truth)

- The "Gotchas": 4 Clauses That Kill Value

- Expert Insights: The 2026 Market Landscape

- Strategic Advice: How to Play the Game in 2026

- Conclusion: The Final Verdict

- Frequently Asked Questions (FAQs)

The New Math of Vet Care: Why Costs Are Soaring

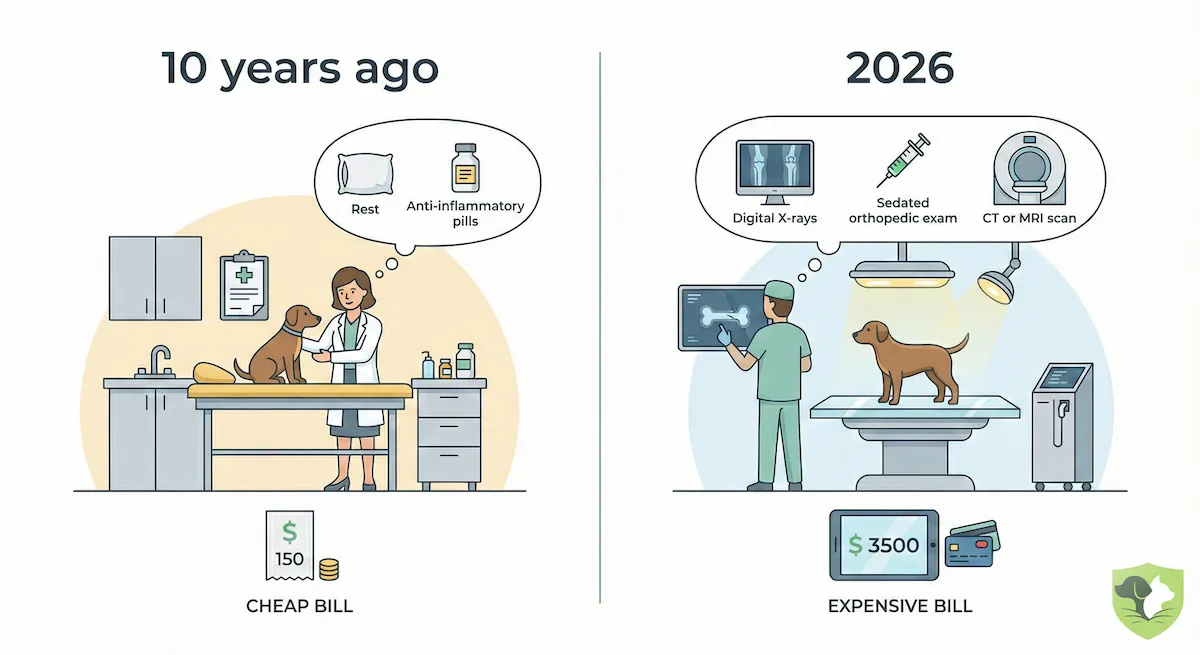

You aren't imagining it—the bill really is higher. If you owned a dog ten years ago, a limp was treated with rest and maybe some anti-inflammatories. Today, that same limp triggers a recommendation for digital X-rays, a sedated orthopedic exam, and possibly a referral for a CT scan.

This isn't price gouging; it is a fundamental structural shift in veterinary medicine. We have entered the era of the "Medicalization of Pets". In 2026, the veterinary sector has decoupled from the general economy. While the Consumer Price Index (CPI) has stabilized, veterinary services in key metropolitan markets are seeing inflation rates between 5.7% and 11% annually.

Here are the three factors driving your vet bill into the stratosphere:

1. The New "Gold Standard" of Care

The days of "wait and see" medicine are effectively over. Advances in human healthcare have migrated to veterinary hospitals, creating a new baseline for what is considered responsible ownership.

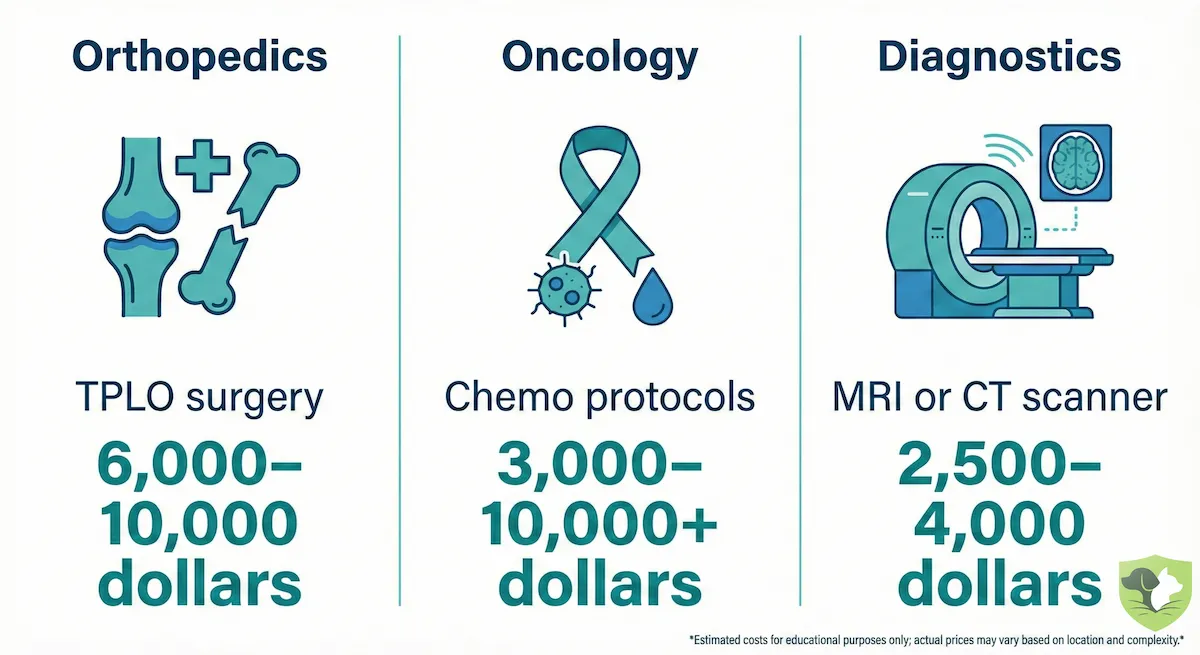

- Orthopedics: The standard treatment for a torn ACL (CCL) in dogs is now the TPLO surgery. In 2026, this costs between $6,000 and $10,000 per knee.

- Oncology: Cancer is no longer an automatic death sentence. Chemotherapy protocols (like CHOP for lymphoma) are routine but expensive, costing $3,000 to over $10,000 depending on the regimen.

- Diagnostics: MRIs and CT scans are now standard diagnostic tools for seizures or spinal issues, adding $2,500 to $4,000 to a bill before treatment even begins.

2. The Corporate Takeover

The era of the independent "James Herriot" style vet is ending. Large corporate groups and Private Equity firms (like Mars or NVA) have consolidated the industry.

- Standardized Pricing: Corporate ownership often standardizes pricing at a higher baseline to maximize revenue.

- Diagnostic Density: These groups prioritize "diagnostic density"—running blood panels and imaging earlier in a workup. This improves care but significantly increases the Average Transaction Value (ATV) of a simple visit.

3. The Labor Crunch

There is a massive shortage of veterinary professionals. To attract talent, clinics have had to raise wages significantly. Since labor is the largest expense for a clinic, these costs are passed directly to you.

The Bottom Line: You are paying for a level of medical sophistication that didn't exist a generation ago. The "sticker shock" you feel is the cost of access to MRI machines, board-certified surgeons, and life-saving cancer drugs.

The Financial Breakdown: Premiums vs. Payouts

To determine true pet insurance value, we have to move beyond feelings and look at the ledger. The math of insurance is a trade: you trade a known, fixed cost (premium) to avoid an unknown, potentially catastrophic cost (claim).

Here is what that trade looks like in 2026.

The Cost of Coverage

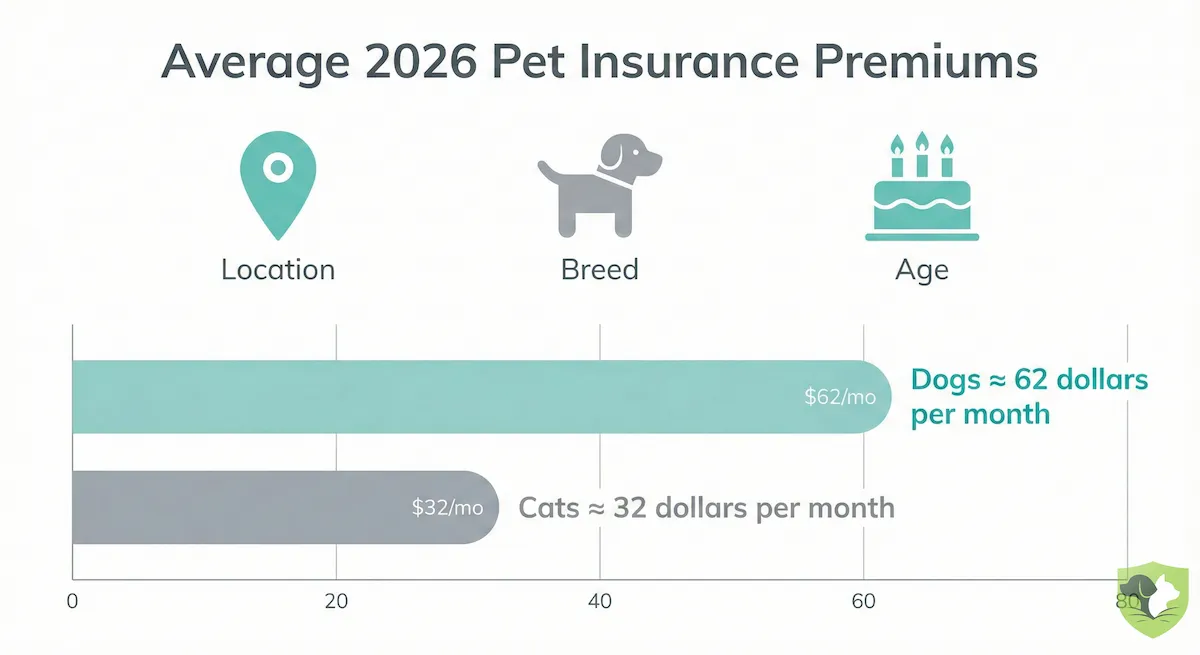

In 2025-2026, the average monthly premium for a comprehensive accident and illness policy is approximately $62 for dogs and $32 for cats. However, "average" is a dangerous metric. Your actual rate depends heavily on three variables:

- Location: Veterinary overhead in New York or Los Angeles can drive premiums nearly double those in rural areas.

- Breed: A French Bulldog, prone to spinal and respiratory issues, can cost $88–$97 per month to insure, while a mixed breed might cost $32–$50.

- The "Loyalty Penalty" (Birthday Pricing): This is the factor most owners miss. Premiums are not fixed; they rise as your pet ages. Data indicates that insuring a dog at age 7 can cost 81% more than insuring the same dog at age 2.

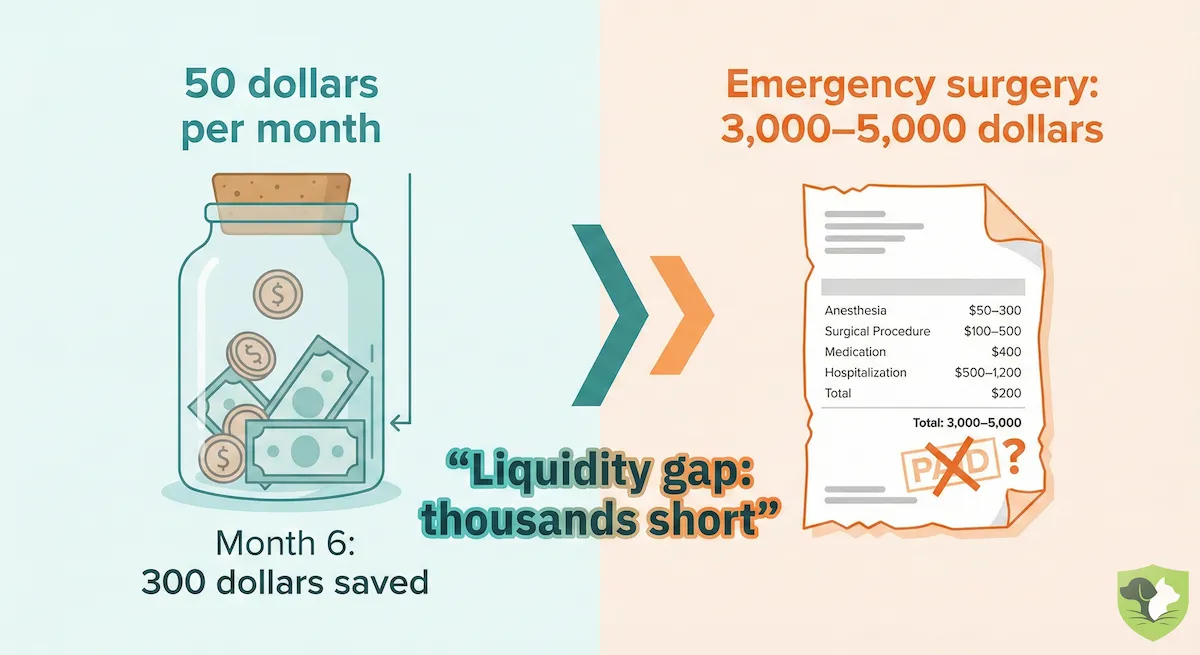

The "Self-Insurance" Myth

A common argument against insurance is the "Savings Account Strategy." The logic seems sound: Why pay an insurer $50 a month? I’ll just put that $50 into a High-Yield Savings Account.

Here is why that math often fails in the real world: Liquidity Speed.

| Scenario | Timeline | Amount Saved | Vet Bill | Result |

|---|---|---|---|---|

| Savings Account | Month 6 | $300 | $5,000 (Surgery) | -$4,700 Shortfall |

| Insurance | Month 6 | $300 (Premiums) | $5,000 (Surgery) | Full Coverage* |

To "self-insure" effectively, you need to have $5,000 to $10,000 available on Day 1, not accumulated over five years. Insurance provides that immediate liquidity.

The Break-Even Analysis

Does insurance ever pay for itself? Statistically, if your pet is lucky and healthy, you will "lose" money. But it only takes one major event to flip the equation.

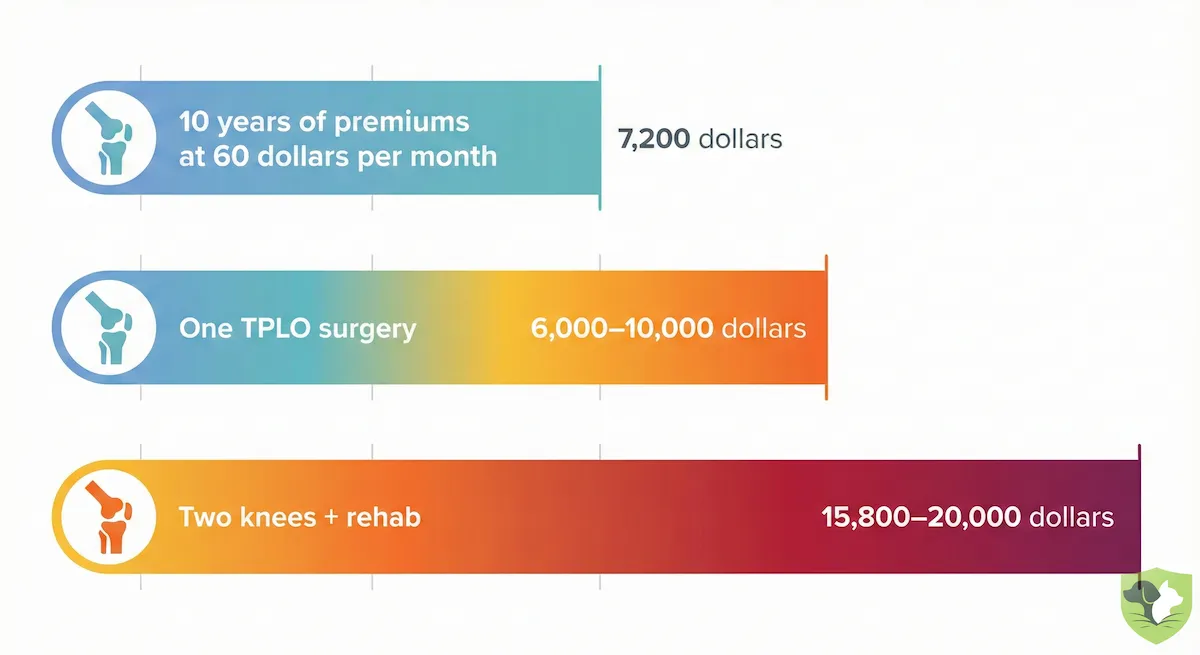

Consider the TPLO (knee) surgery for a dog, a standard procedure in 2026:

- Total Cost: $6,000 to $10,000 per knee.

- Lifetime Premiums: If you pay $60/month for 10 years, your total spend is $7,200.

In this scenario, a single surgery on one knee covers a decade of premiums. If your dog tears both knees (a common "bilateral" occurrence), the insurance policy could save you over $12,000 net. That is where the financial value lies—not in the small stuff, but in the catastrophic.

Is Dog Insurance Worth It?

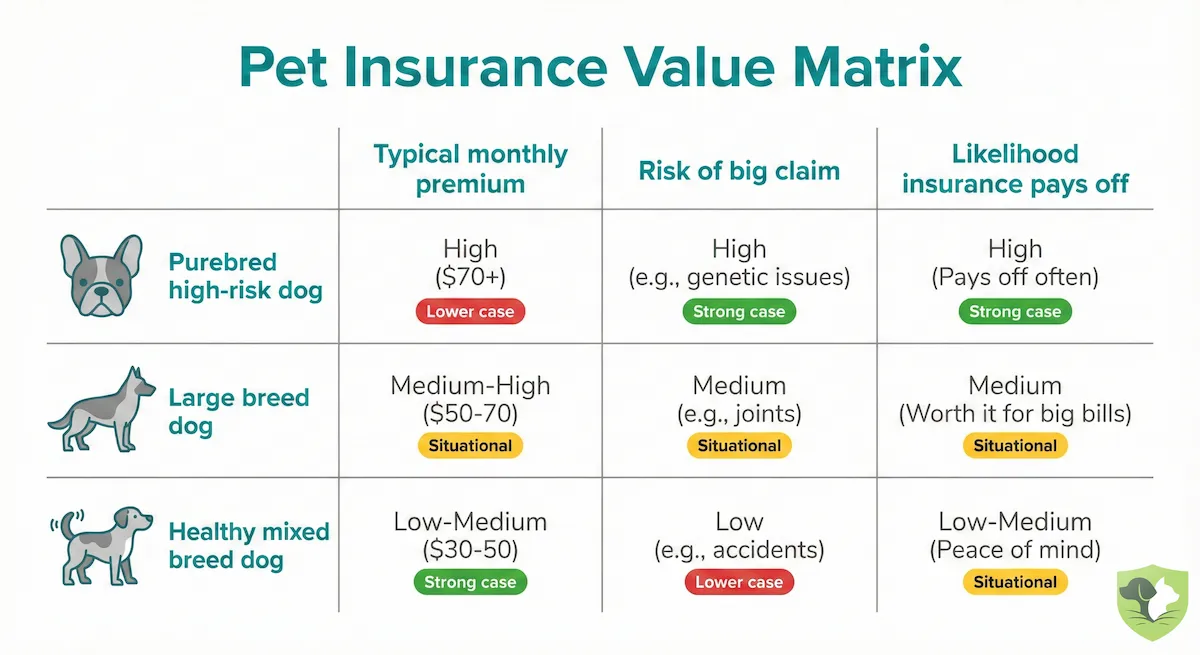

If you own a dog in 2026, the answer to is dog insurance worth it almost always comes down to two factors: genetics and lifestyle.

Dogs are statistically more expensive to treat than cats, with premiums averaging double the cost. But this average hides the real story. To understand if insurance makes sense for you, you need to look at your dog not as a pet, but as an actuarial risk profile.

The "Genetic Time Bomb" (Purebreds)

If you own a purebred, you are often paying a "breed tax". Insurers use vast datasets to predict exactly what health issues your dog will likely face, and they price premiums accordingly.

- The French Bulldog: One of the most expensive breeds to insure, with premiums averaging $88 to $97 per month. Why? They are a "genetic time bomb" for Brachycephalic Obstructive Airway Syndrome (BOAS), spinal issues (IVDD), and chronic dermatitis.

- Large Breeds (Rottweilers, Bernese Mountain Dogs): These breeds are prone to osteosarcoma (bone cancer) and hip dysplasia. The break-even point for these dogs is reached incredibly fast; a single cancer treatment protocol involving chemotherapy can run $5,000 to over $10,000.

For these breeds, insurance isn't a gamble; it’s a prepayment for a statistically probable event.

The Mixed Breed Argument

Owners of mixed breeds often argue, "My dog is a healthy mutt; I don't need coverage." It is true that mixed breeds generally command lower premiums, often in the $30–$50 range, because their genetic diversity protects them from some hereditary crises.

However, mixed genetics do not protect against accidents. The primary risk for a healthy, active mixed breed is Foreign Body Ingestion—veterinary speak for swallowing a sock, a corn cob, or a toy.

- The Cost: Emergency surgery to remove a blockage (gastrotomy) typically costs $3,000 to $5,000.

- The Math: You would need to save $50 a month for 8 years to cover a single "sock incident."

Insurance covers it immediately.

Case Study: The $20,000 Knee

To understand the true financial risk of dog ownership, look no further than the Cranial Cruciate Ligament (CCL)—the dog equivalent of an ACL. It is the most common orthopedic injury in dogs. In 2026, the standard treatment is the Tibial Plateau Leveling Osteotomy (TPLO).

Here is the brutal math for a large breed dog:

- Surgery Cost: $6,000 to $10,000 per knee.

- Rehabilitation: Post-op hydrotherapy and laser therapy adds roughly $1,500 per leg.

- The Bilateral Trap: If a dog tears one CCL, there is a high probability they will tear the other.

For a bilateral rupture, you are looking at a potential $15,800 to $20,000 household expense. If you have a $5,000 annual limit on your policy, you are still on the hook for $15,000. This is why for large dogs, unlimited annual coverage is not a luxury upgrade—it is a mathematical necessity.

Is Cat Insurance Worth It? (The Indoor Cat Fallacy)

If you ask a cat parent is cat insurance worth it, the hesitation is almost always the same: "He’s an indoor cat. He just sleeps on the sofa. What could possibly happen?"

This is the Indoor Cat Fallacy. We assume risk is tied to the outdoors—cars, fights, and falls. But for cats, specifically males, the most expensive dangers are biological, not environmental.

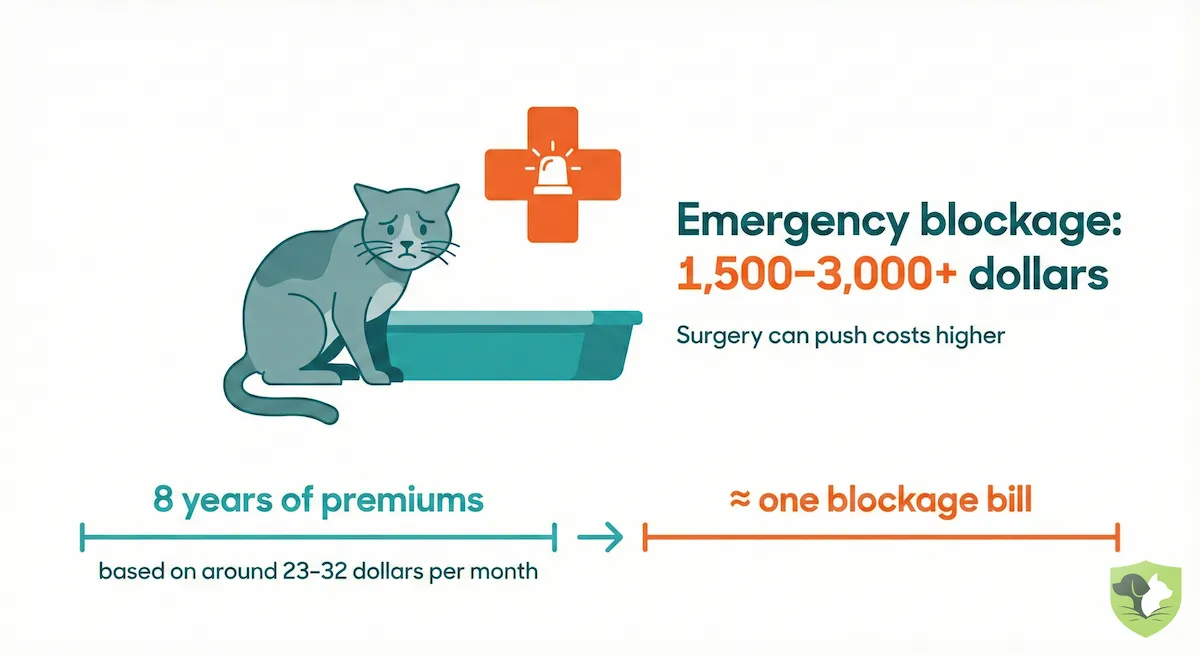

The $3,000 Litter Box Problem

The single biggest argument for insuring a male cat is the "Blocked Tom" scenario (urinary obstruction). It is a life-threatening emergency where the urethra becomes blocked. It happens suddenly, often to young, healthy indoor cats.

- The Cost: Emergency catheterization and hospitalization typically cost $1,500 to $3,000. If surgery (Perineal Urethrostomy) is required, the bill climbs higher.

- The Math: With average cat insurance premiums hovering around $23 to $32 per month, a single urinary blockage pays for nearly 8 years of premiums.

The "Slow Burn" of Chronic Illness

While dogs often suffer from acute orthopedic injuries (like the knee surgeries mentioned above), cats are masters of chronic illness. Kidney disease, diabetes, and hyperthyroidism are rampant in the feline population.

Treating a diabetic cat involves insulin, needles, and frequent blood panels for the rest of their life. This isn't a one-time $5,000 hit; it is a recurring $100 to $200 monthly drain on your budget for years.

Insurance policies like Trupanion, which use a "per-condition" deductible, are particularly mathematically favorable here: you pay the deductible once for diabetes, and the insurer covers 90% of the insulin forever.

The "Felix" Factor: A Market Shift

The industry has finally recognized that cats are not just "small dogs." In 2025, we saw the rise of cat-specific insurance brands like Felix (owned by Independence Pet Holdings). These plans are tailored to the indoor lifestyle. They often cover behavioral issues common in indoor cats and even include "Final Respects" coverage (cremation/burial) as a standard feature, rather than an expensive add-on.

The Verdict: Because cat premiums are significantly lower than dog premiums, the threshold to "break even" is much lower. You don't need a catastrophic car accident to justify the cost; one bad weekend with a urinary issue makes the policy worth it.

Pros and Cons of Pet Insurance (The Unfiltered Truth)

Searching for "pros and cons of pet insurance" usually yields generic lists about "peace of mind." But in 2026, the distinctions are much sharper. Insurance is a sophisticated financial product, and like any financial product, it has structural flaws you need to accept before buying. Here is the unfiltered reality of what you are signing up for.

The Pros: Why It Save Lives

- Liquidity is the Real Product: The primary benefit isn't "saving money"; it is liquidity. Most American households cannot access $5,000 in cash on a Tuesday night without raiding a 401(k) or maxing out high-interest credit cards. Insurance provides the liquidity to say "yes" to life-saving treatment instantly.

- Access to "Human-Grade" Medicine: Without insurance, a referral to a board-certified neurologist for an MRI ($3,000+) is often a non-starter. With insurance, it becomes a standard diagnostic step. It allows you to make medical decisions based on prognosis, not your bank balance.

- The Rise of "Direct Pay": Historically, you had to pay the vet first and wait for a check. Innovations from carriers like Trupanion (and to a lesser extent Pets Best) now allow the insurer to pay the veterinarian directly at checkout. This solves the cash-flow gap, meaning you only pay your deductible, not the full $5,000 bill.

The Cons: The "Fine Print" Frustrations

- The Reimbursement Lag (The "Float"): For 95% of providers (like Lemonade, Spot, and Fetch), the model is still Indemnity Insurance. You must pay the vet bill in full upfront. If you don't have $5,000 available on a credit card to "float" the cost while you wait 10-30 days for reimbursement, the insurance policy is useless in an emergency.

- Premium Volatility (The "Loyalty Penalty"): This is the biggest complaint in 2026. Premiums are not fixed. As your pet ages, rates rise aggressively—sometimes by 20% to 30% in a single year. Data shows that insuring a dog at age 7 can cost 81% more than insuring the same dog at age 2. You are effectively "locked in" because switching providers would reset your pre-existing conditions.

- It Does Not Cover Everything: Unlike human health insurance, pet insurance generally excludes routine maintenance. Unless you buy expensive riders, you are still paying for annual exams, vaccines, and teeth cleaning out of pocket.

The Verdict: The "Pro" is that it prevents financial ruin. The "Con" is that it requires you to tolerate rising monthly costs and navigate a complex reimbursement system.

The "Gotchas": 4 Clauses That Kill Value

If you skim the brochure and skip the fine print, you are gambling, not insuring. The difference between a payout and a denial letter often hides in four specific clauses. In 2026, understanding these "gotchas" is the difference between a life-saver and a waste of money.

1. The Pre-Existing Condition Trap (Notes Matter)

This is the #1 reason claims are denied. A "pre-existing condition" isn't just a diagnosed disease; it is any clinical sign noted in your pet’s medical record before the policy starts. If your vet noted "minor itching" two years ago, a new insurer could deny a claim for chronic allergies today, labeling it pre-existing.

The 2026 Shift (Curable vs. Incurable): Not all pre-existing conditions are a life sentence anymore. Top-tier providers like ASPCA, Spot, and Embrace now distinguish between "Curable" and "Incurable" conditions.

- Curable: If your dog had an ear infection but has been symptom-free for 180 days, coverage can be reinstated.

- Incurable: Conditions like diabetes or hip dysplasia are banned for life if they appeared before coverage.

2. The Bilateral Exclusion (The Knee Trap)

For large dogs, this is the silent killer of value. "Bilateral" means "both sides." Insurers assume that if a condition affects one side of the body (like a knee or hip), the other side is a ticking time bomb.

The Trap: If your dog tears the cruciate ligament (ACL) in their left knee before you have insurance, the insurer will permanently exclude the right knee from coverage.

The Waiting Period: Orthopedic issues often come with a strict 6-month waiting period—much longer than the standard 14 days for illness. If your dog limps in month 4, you aren't covered. Note that newer providers like Spot and Pumpkin have disrupted this by reducing the orthopedic wait to 14 days.

3. The Dental Gap

Dental disease is one of the most common issues in pets, but coverage is notoriously spotty. You must distinguish between Dental Accidents and Dental Illness.

- Accidents: Almost all plans cover a tooth broken on a bone.

- Illness: Periodontal disease (gum disease) requires expensive extractions, often costing $1,000 to $3,000. Many budget plans exclude this entirely. Others, like Fetch and Pets Best, cover it, but often only if you can prove you’ve had annual dental exams.

4. The Wellness Plan "Scam"

Insurers love to upsell "Wellness" or "Preventative" riders that cover vaccines and check-ups. Do the math before you buy.

The Reality: These are usually "dollar-swapping" arrangements. You pay $25/month ($300/year) to get $300 worth of reimbursement for shots.

The Caps: Often, these plans cap payouts per item (e.g., only $15 for a fecal test that actually costs $45).

Verdict: Unless you are terrible at budgeting, skip the wellness rider. Put that $25 in a jar instead. Use insurance for the big, unpredictable stuff, not the routine bills you can plan for.

Expert Insights: The 2026 Market Landscape

You can read a dozen "Top 10" lists, but they often miss the tectonic shifts happening behind the scenes. As industry insiders, we track the regulatory filings and corporate mergers that actually determine your premium. Here is the "inside baseball" on the pet insurance market in 2026.

The "Big Three" Market Updates

-

The California Transparency Shock (SB 1217): California’s Senate Bill 1217 has effectively become the national standard for transparency. In 2026, insurers can no longer hide behind vague jargon when raising your rates.

- The Change: Insurers must now explicitly disclose whether a rate hike is due to your pet’s specific age ("Birthday Pricing") or a general change in veterinary costs in your zip code.

- The Win: They are strictly prohibited from marketing "Wellness Programs" (discount plans) as insurance, ending the confusion that led many owners to think their vaccines were covered by their accident policy.

-

The "Illusion of Choice" (Consolidation): If you are comparing Spot, ASPCA Pet Health Insurance, Pets Best, and Figo, you might think you are shopping around. You aren’t.

- The Reality: All of these brands are now effectively under the umbrella of Independence Pet Holdings (IPH).

- Why It Matters: While the frontend apps and customer service teams differ, the underlying risk capital often flows to the same place. Don't stress about finding a "different" underwriter among these four; focus on which policy features (like waiting periods) fit your specific needs.

-

The 4% Penetration Stat: Despite the hype, pet insurance remains a niche product. As of late 2024, approximately 7.03 million pets were insured in North America.

- The Stat: That sounds like a lot, but it represents only 3.9% of U.S. pets.

- The Takeaway: The market is still young. This low adoption rate is partly why premiums are volatile; the risk pool isn't yet large enough to stabilize costs completely against the skyrocketing price of veterinary care.

Strategic Advice: How to Play the Game in 2026

Your strategy must match your pet's life stage. One size does not fit all.

1. The "Puppy Strategy" (The Clean Slate)

The Goal: Lock in coverage before a "paper trail" exists.

The Tactic: Enroll your puppy at 8 weeks old, before their first major vet visit if possible.

Why: If you wait until 6 months and your puppy has a single vet note about "itchy skin," you could be barred from allergy coverage for life. Getting in early guarantees a "clean slate" with no pre-existing exclusions.

2. The "Rescue Strategy" (The Curable Loophole)

The Goal: Insure a dog with a history without getting denied.

The Tactic: Prioritize carriers like ASPCA or Spot that distinguish between "curable" and "incurable" conditions.

Why: A rescue dog often comes with baggage (e.g., a past ear infection). "Curable" clauses allow these conditions to be covered again after a symptom-free period (usually 180 days), whereas other insurers would ban them permanently.

3. The "Big Dog" Strategy

The Goal: Avoid the orthopedic cap.

The Tactic: Never buy a policy with a $5,000 or $10,000 limit for a Lab, Golden, or Rottweiler.

Why: A bilateral knee injury (TPLO) costs $15,000+. You statistically need an Unlimited annual payout to be safe.

Conclusion: The Final Verdict

So, is pet insurance worth it in 2026? If you look at it strictly as an investment, the answer is likely no. If your pet lives a long, healthy life and only visits the vet for annual shots, you will "lose" thousands of dollars in premiums over the years. And that is the best-case scenario.

Because the alternative—"winning" at pet insurance—means your best friend has suffered a catastrophic illness or injury. You don't want to "win" this bet. You want to pay for a safety net you hope to never use.

In the 2026 economy, where a single knee surgery can cost $10,000, pet insurance is no longer a way to save money on the vet bills you expect. It is the only viable mechanism to pay for the vet bills you cannot afford. It buys you the freedom to look a veterinarian in the eye and say, "Do whatever it takes," without hesitating over the cost.

Your Next Move: Before you click "buy" on a policy, take this one actionable step: Audit your pet's medical records. Request the full history from your vet. Read it yourself. If there is a note about "itchy skin" from three years ago, know that your new insurer will likely flag that as a pre-existing condition. Understanding your pet’s specific "risk profile" on paper is the best defense against a denied claim later.

Ultimately, pet insurance is about being the hero your pet already thinks you are. When the worst happens, you won't be worrying about your bank account. You’ll just be holding their paw, waiting for them to wake up.

Frequently Asked Questions (FAQs)

Is pet insurance actually worth it in 2026?

If you have a healthy pet, you will likely lose money on premiums—and that is the best-case scenario. Pet insurance is not an investment; it is a hedge against catastrophe. It becomes "worth it" the moment you face a $5,000 to $10,000 emergency bill. For 1 in 3 pets that experience an emergency annually, it is a financial lifesaver.

How much does pet insurance cost on average?

In 2025-2026, the average monthly premium is approximately $62 for dogs and $32 for cats for standard accident and illness coverage. However, this varies wildly by breed and location; a French Bulldog in a major city can cost nearly $100/month, while a mixed-breed cat might cost $23.

Does pet insurance cover pre-existing conditions?

Generally, no. Any illness or injury noted in your pet’s medical records before your policy starts is excluded. However, in 2026, the best policies distinguish between "incurable" (e.g., diabetes) and "curable" conditions (e.g., ear infections). Curable conditions can often be covered again after a symptom-free period of 180 days.

Why shouldn't I just put $50 a month into a savings account?

Because you need liquidity speed, not just accumulation. If you save $50/month, you will only have $600 after a year. If your dog needs a $5,000 surgery in Month 6, your savings account will fail you. Insurance provides access to the full coverage limit immediately after waiting periods are met.

Is pet insurance worth it for senior dogs (8+ years old)?

It is difficult to justify financially. Premiums for senior dogs often exceed $133 per month, and any conditions they developed earlier in life (arthritis, heart issues) will be excluded as pre-existing. Unless you enroll them while they are young, the value proposition drops significantly as they age.

Does pet insurance cover routine vet visits and shots?

Not by default. Standard policies cover accidents and illnesses only. You can buy "Wellness" add-ons to cover vaccines and exams, but the math rarely works out in your favor. These plans often act as "dollar swapping" where you pay $300 a year to get capped reimbursements that roughly equal what you paid in.

Does pet insurance cover dental work?

It depends on the "type" of dental issue. Almost all plans cover dental accidents (e.g., a tooth broken chewing a bone). However, dental illness (periodontal disease/extractions) is frequently excluded or capped unless you have a premium plan from providers like Fetch or Pets Best, and often requires proof of annual cleanings.

What is the "Bilateral Exclusion"?

This is a clause that affects orthopedic coverage. If your pet injures one side of their body (like a torn ACL in the left knee) before coverage starts, the insurer may permanently exclude coverage for the right knee as well, assuming the issue is genetic. This is a major risk for large breeds like Labradors and Rottweilers.

Do I have to pay the vet upfront?

Usually, yes. Most pet insurance works on a reimbursement model: you pay the bill, file a claim, and get paid back in 1–2 weeks. However, Trupanion and Pets Best offer "Direct Pay" options that can pay the veterinarian directly at checkout, meaning you only pay your deductible and copay.

Why did my premium go up if I didn't file a claim?

This is known as the "Loyalty Penalty" or "Birthday Pricing." Premiums are adjusted based on your pet's age and local veterinary inflation, not just your personal claim history. As your pet gets older, the statistical risk of illness rises, and premiums can increase by 20% or more annually to reflect that risk.

WhiskerCover is reader-supported. When you click on links to pet insurance partners on our site and purchase a policy, we may earn a commission at no extra cost to you. Learn more about how we make money.