If you've visited a veterinary clinic recently, you've likely noticed the sticker shock. Veterinary medicine has advanced rapidly—treatments like MRIs and chemotherapy are now standard, which has driven costs higher. Common surgeries like a TPLO (knee repair) now range from $6,000 to $10,000. For this reason, pet insurance has shifted from a luxury to a financial necessity for millions of families.

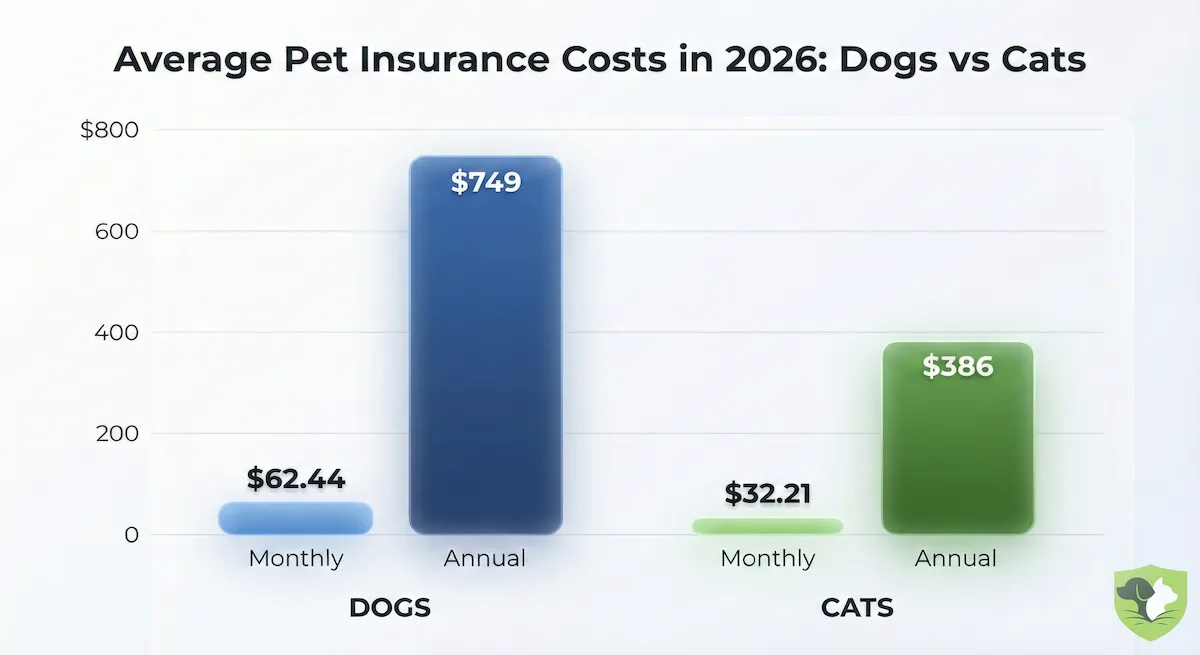

So, what's the damage? According to market data, the national average monthly premium for standard accident and illness coverage is $62.44 for dogs and $32.21 for cats.

However, relying on a national average is a bit like checking the average temperature of the entire United States—it doesn't tell you if you need a coat. A mixed-breed puppy in Ohio might be insured for $28 a month, while a French Bulldog in New York City could easily cost over $130. Your actual premium isn't random; it is a calculated figure based on the "Risk Triangle" of location, breed, and age. Understanding these levers is the only way to predict what you will actually pay.

Table of Contents

- The 2026 National Averages: Establishing a Baseline

- The 4 Factors That Swing Your Premium

- Scenario Analysis: Real World Quotes for 2026

- Expert Insights: The "Hidden" Costs Nobody Talks About

- Top Provider Price Comparison (2026 Landscape)

- Is Pet Insurance Worth the Cost? (ROI Analysis)

- Conclusion

- Frequently Asked Questions (FAQs)

The 2026 National Averages: Establishing a Baseline

Before we dive into the specific factors that can spike or lower your rate, we need to look at the "sticker price." In 2026, the market has stabilized around two distinct price points, depending on whether you have a canine or a feline companion.

Understanding these baseline costs is crucial before we explore the 'four factors' that influence your insurance premium. These factors—geography, breed risk, age, and coverage specifics—paint a comprehensive picture of what to expect financially when choosing pet insurance. Some policies may cost less, but these averages are for standard Accident & Illness coverage—the plan that actually covers cancer, diabetes, and difficult-to-diagnose stomach problems.

Average Dog Insurance Cost

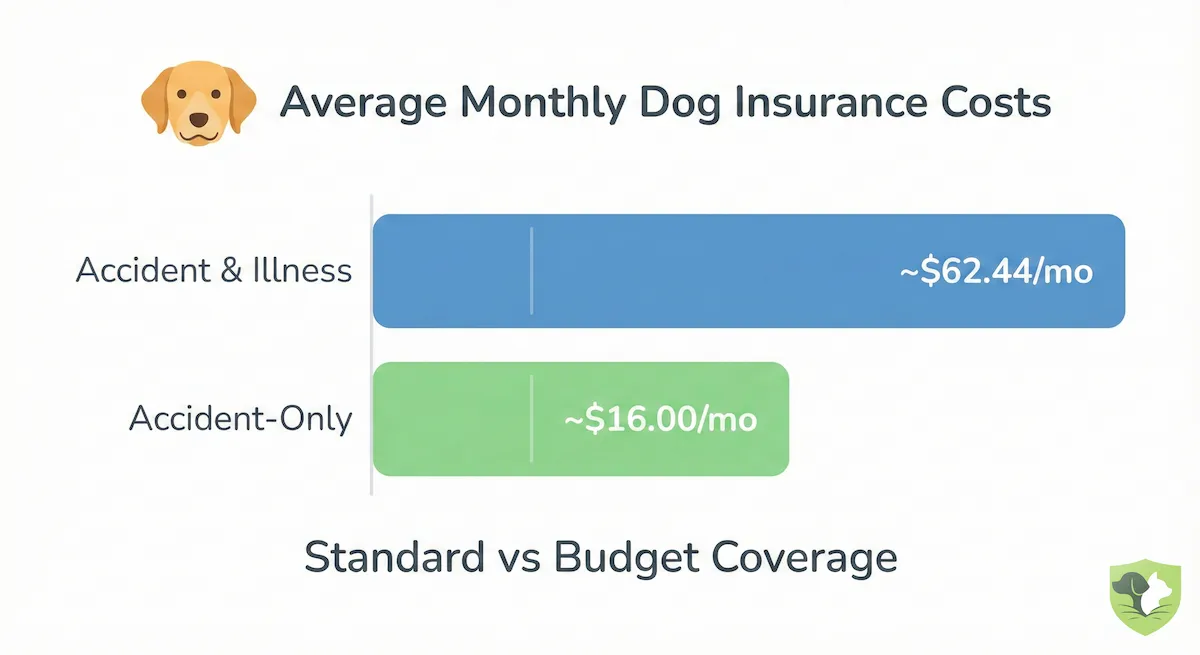

If you are insuring a dog in 2026, expect to pay significantly more than your cat-owning friends. The national average for a comprehensive accident and illness plan is approximately $62.44 per month. On an annualized basis, that's roughly $749 to protect your pup.

However, if you strip away the illness coverage and opt for a bare-bones plan, the price drops dramatically.

2026 Monthly Benchmarks (Dogs):

- Accident & Illness (Standard): ~$62.44/mo

- Accident-Only (Budget): ~$16.00/mo

Why are dogs so expensive? Actuarial data show that dogs have a much higher risk profile than cats. They are simply more prone to accidental injuries—like swallowing socks or tearing ligaments at the dog park—and they suffer from a broader spectrum of expensive hereditary conditions that require surgery.

Average Cat Insurance Cost

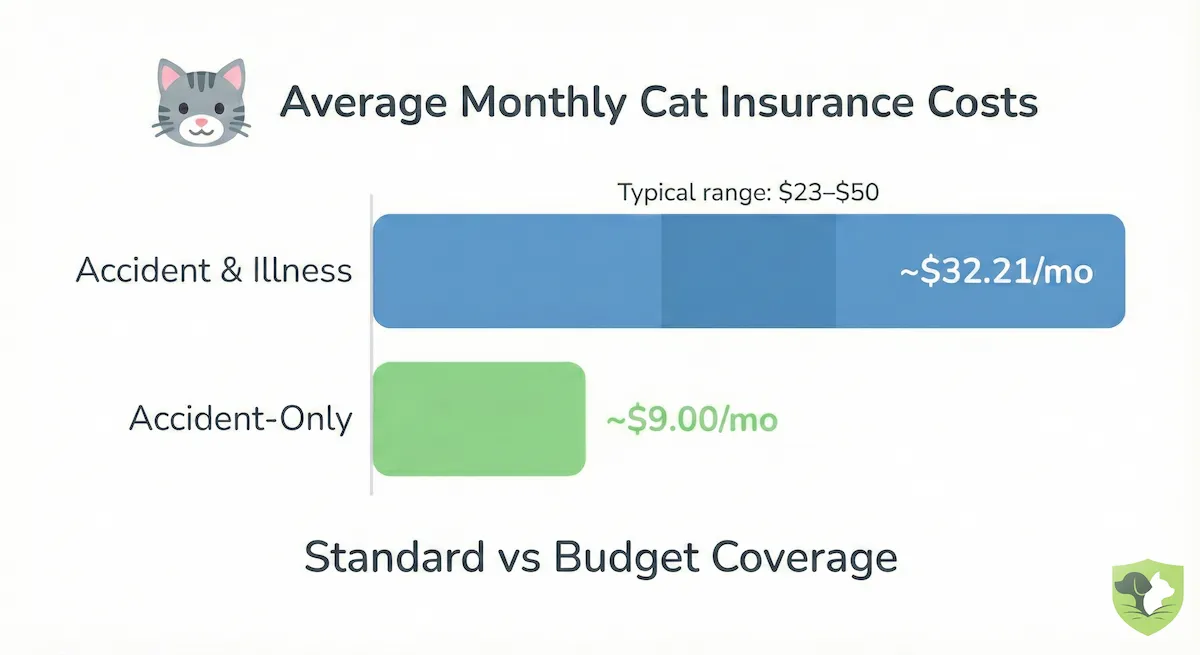

Cats are generally the bargain of the insurance world. The average monthly premium for a standard feline policy is $32.21, roughly half the cost of a dog policy. For a full year of coverage, you are looking at an investment of about $386.

2026 Monthly Benchmarks (Cats):

- Accident & Illness (Standard): ~$32.21/mo

- Accident-Only (Budget): ~$9.00/mo

The "Stability" Factor: Cat pricing tends to be more stable than dog pricing. While dog premiums can swing wildly by breed (a French Bulldog costs nearly triple what a mixed breed costs), cat premiums stay in a tighter range, typically between $23 and $50 per month. However, don't let this low entry price fool you; as we will discuss in the next section, premiums for senior cats can still climb aggressively as kidney issues and hyperthyroidism become common risks.

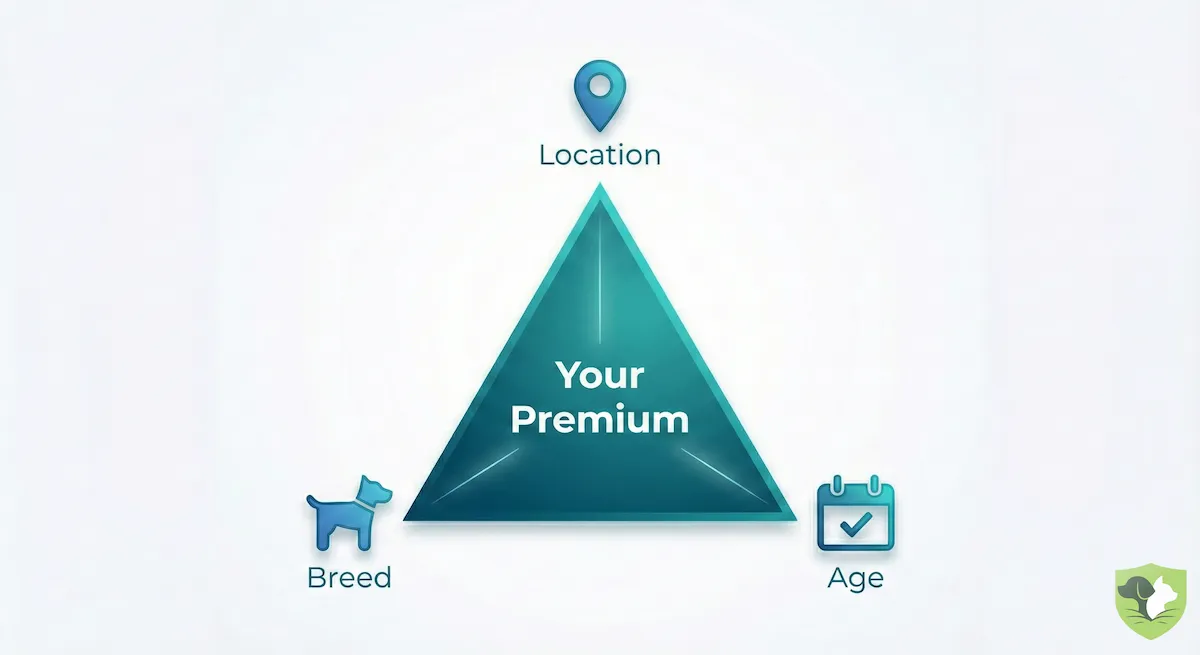

The 4 Factors That Swing Your Premium

While national averages give you a ballpark figure, your actual quote will be determined by four specific levers. Think of this as the "Risk Triangle"—insurers calculate your premium based on where you live, who your pet is genetically, and how old they are.

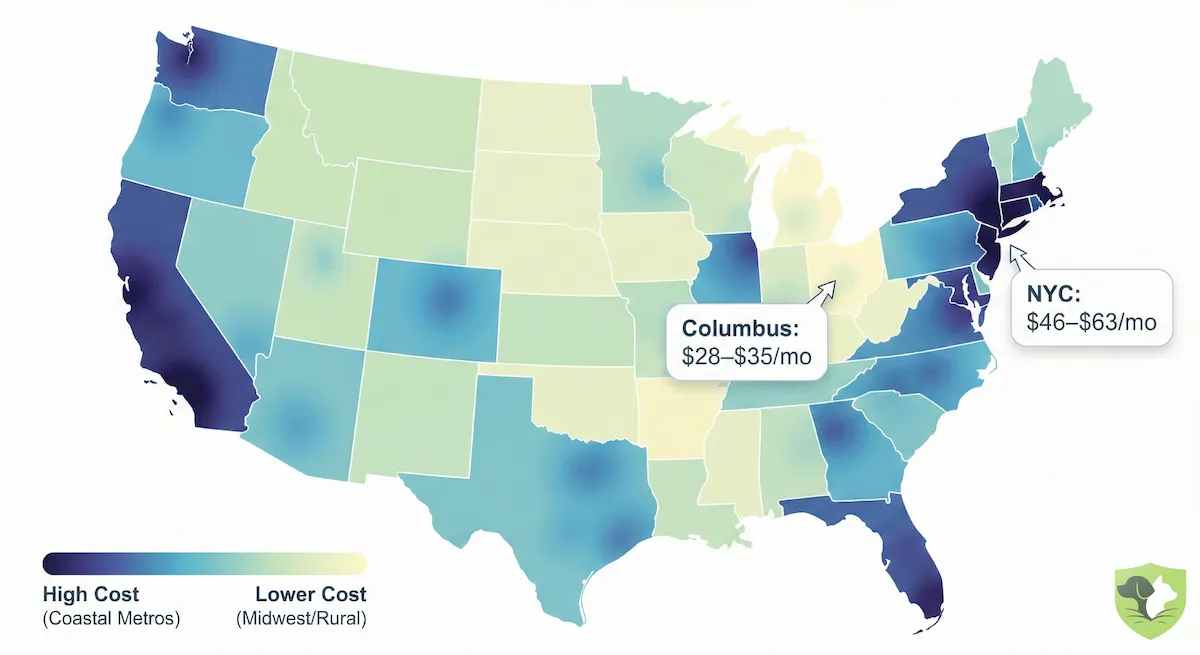

1. Geography: The "Coastal Premium"

Real estate isn't the only thing more expensive on the coasts. Insurance carriers divide the country into "rating territories," often down to the zip code level. If you live in an area where veterinarians pay high rent and high wages, those costs are passed on to you in the form of higher premiums.

In 2026, this "coastal premium" is stark. A policy in New York City or Los Angeles can cost nearly twice as much as the same policy in the Midwest. For example, insuring a dog in New York City might cost upwards of $63 per month, whereas the exact same dog in Columbus, Ohio, would cost around $28 to $35.

| Location | Cost Level | Monthly Range |

|---|---|---|

| New York, NY | High Cost | $46 - $63 |

| Los Angeles, CA | High Cost | $42 - $46 |

| Boston, MA | High Cost | $38 - $53 |

| Columbus, OH | Low Cost | $28 - $35 |

| Grand Rapids, MI | Low Cost | $27 - $34 |

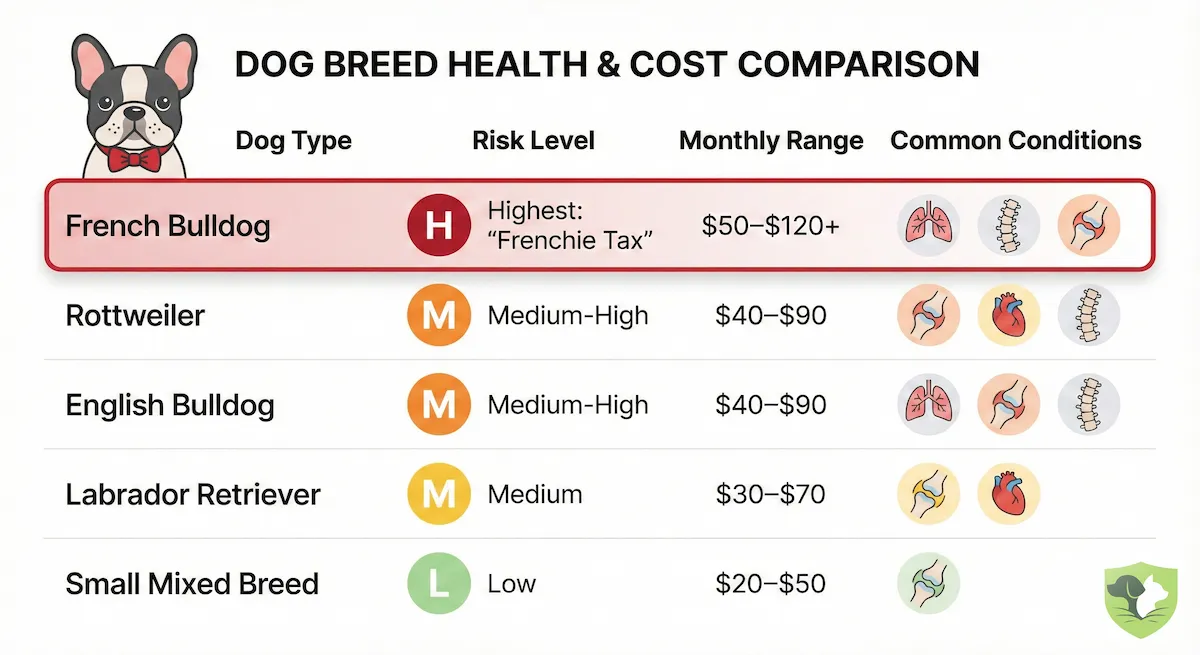

2. Breed Risk: The "Frenchie Tax"

Your pet’s DNA is a major financial variable. Insurers have decades of data linking specific breeds to expensive medical conditions, and they price that risk into your monthly bill. The clearest example in 2026 is the French Bulldog.

Because this breed is highly prone to Brachycephalic Obstructive Airway Syndrome (BOAS) and spinal issues requiring MRIs, they command the highest premiums in the market—often ranging from $92 to $113 per month.

Conversely, a mixed-breed dog, benefiting from "hybrid vigor" and fewer hereditary risks, costs significantly less, averaging around $30 per month.

| Breed | Risk Level | Avg Cost | Key Medical Drivers |

|---|---|---|---|

| French Bulldog | High Risk | $92 - $113 | Airway Syndrome (BOAS), IVDD |

| Rottweiler | High Risk | ~$83 | Bone Cancer, ACL Tears |

| English Bulldog | High Risk | ~$78 | Cardiac & Respiratory Issues |

| Labrador Retriever | Medium Risk | $53 - $62 | Joint Issues, Foreign Object Ingestion |

| Mixed Breed (Small) | Low Risk | ~$30 | Lower Hereditary Risk |

3. The Age Curve: Understanding the "Senior Cliff"

Pricing does not rise in a straight line as your pet ages; it follows a steep curve. For the first few years of your pet’s life, the costs ascend gently, like strolling up a gradual incline.

However, data shows a sharp "Senior Cliff" between the ages of 5 and 7, where premiums suddenly escalate, demanding you to climb a steep face of expenses. By the time a dog reaches age 7, premiums effectively jump 81% compared to age 2. This reflects the biological reality that cancer, arthritis, and heart disease—the most expensive conditions to treat—strike in the latter half of a pet's life. By age 10, owners of large breeds often face premiums exceeding $100 per month.

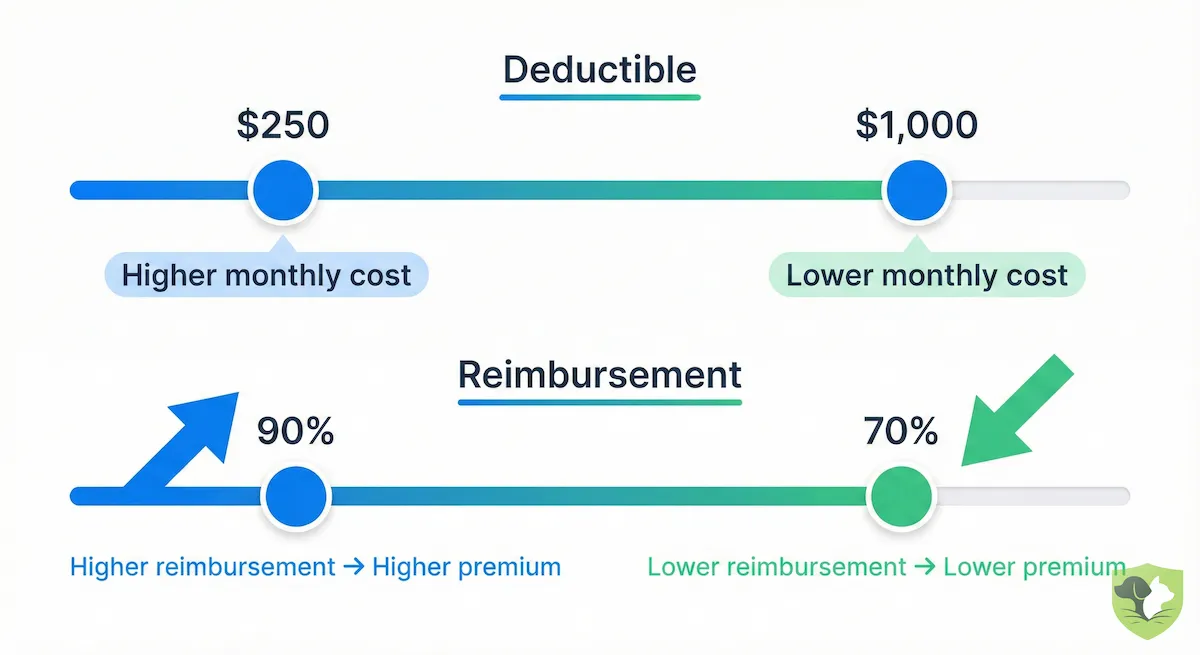

4. Coverage Levers: Deductibles & Reimbursements

Finally, you have control over the price through your policy structure. The most powerful tool you have is the deductible.

Most standard plans come with a $250 deductible. However, by raising that deductible to $500 or $1,000, you can slash your monthly premium significantly—often by $20/month or more. This strategy shifts the cost of small visits (like ear infections) to you, while keeping the insurance focused on catastrophic bills like surgery.

Similarly, adjusting your reimbursement rate from 90% down to 70% lowers the insurer's liability and reduces your monthly cost, a common tactic for owners of older pets trying to keep premiums affordable.

Scenario Analysis: Real World Quotes for 2026

National averages are useful, but they don't pay your bills. To understand what you will actually pay, we need to look at how the "Risk Triangle" (Location, Breed, Age) plays out in the real world. Below are three distinct scenarios based on 2025 market data. These show how identical insurance products can have vastly different price tags—and values—depending on who (and where) you are.

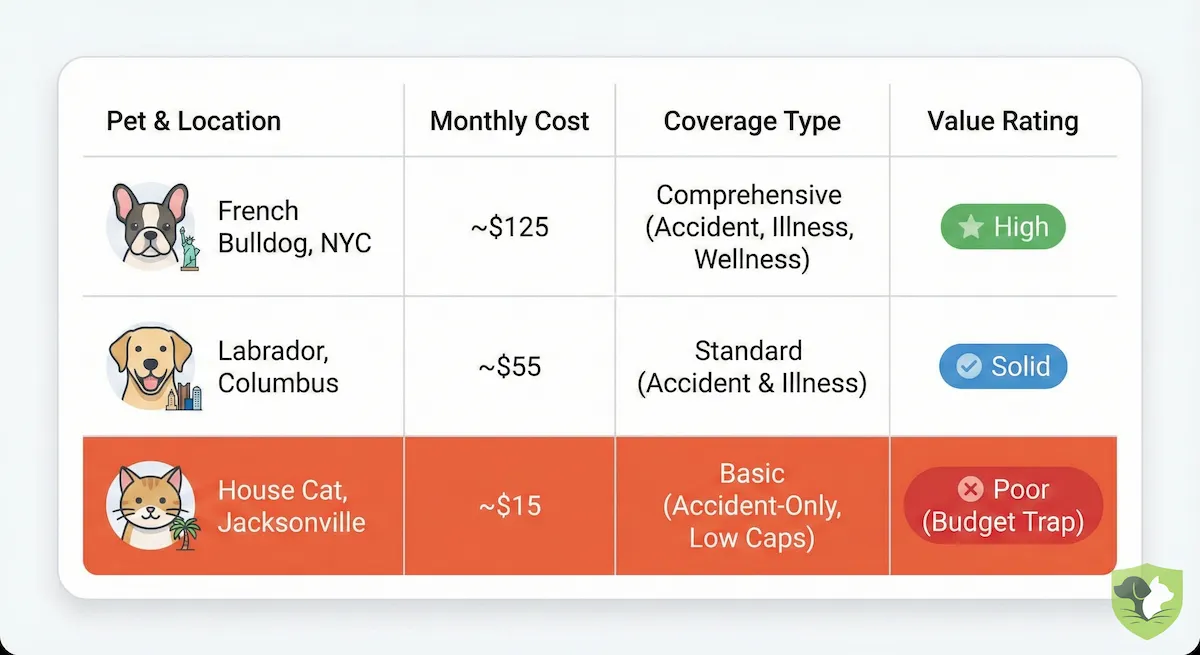

Scenario A: The "Urban Professional" (High Risk, High Cost)

The Profile: A 6-month-old French Bulldog living in New York City.

The Plan: Unlimited Coverage, $250 Deductible, 90% Reimbursement.

Monthly Cost: ~$130 – $150.

The Logic: This is an expensive policy, costing over $1,600 a year. Why buy it? Because French Bulldogs are what veterinarians call "genetic time bombs."

The Math: If this dog needs BOAS (airway) surgery ($4,500) and an MRI for spinal issues ($3,000) by age two, the total claim is $7,500. The insurance pays out ~$6,525. The owner saves nearly $5,000 net of premiums. In this case, the high monthly cost is a necessary hedge against a near-certain high-cost medical future.

Scenario B: The "Suburban Family" (Moderate Risk, Balanced Cost)

The Profile: A 3-year-old Labrador Retriever living in Columbus, Ohio.

The Plan: $5,000 Annual Limit, $500 Deductible, 80% Reimbursement.

Monthly Cost: ~$40.

The Logic: This owner chose a higher deductible ($500) and a capped limit to keep the monthly bill low. Labs are prone to "silly accidents," like eating socks.

The Math: If the dog requires surgery to remove a foreign object ($2,500), the insurance pays $1,600. That single payout covers more than 3 years of premiums. This is the "sweet spot" for most pet owners—protection against accidents without breaking the monthly budget.

Scenario C: The "Budget" Trap (Low Cost, High Risk)

The Profile: A 4-year-old Domestic Shorthair Cat in Jacksonville, Florida.

The Plan: Accident-Only Coverage.

Monthly Cost: ~$9.50.

The Logic: The owner wants the cheapest possible option.

The Math: The cat suffers a urinary blockage, a common illness that costs $1,500 to treat. Because the policy is "Accident-Only," the claim is denied. The Lesson: The low premium provided a false sense of security. For just $15–$20 more per month, a full Accident & Illness policy would have covered the claim.

| Profile | Location | Cost | Verdict | |

|---|---|---|---|---|

| French Bulldog (Puppy) | New York, NY | $130 - $150 | Unlimited / 90% | High. Essential due to severe genetic risks. |

| Labrador (Adult) | Columbus, OH | ~$40 | $5k Limit / $500 Ded | Solid. Covers common accidents reasonably. |

| House Cat | Jacksonville, FL | ~$9.50 | Accident-Only | Poor. Leaves you exposed to common illnesses. |

Expert Insights: The "Hidden" Costs Nobody Talks About

While the monthly premium draws attention, the real cost of pet insurance is often hidden in fine print. As an industry insider, I see daily claim denials—not for unpaid bills, but because owners misunderstand three key aspects of the 2026 market.

1. The "Bilateral Exclusion" Trap

This is the single most common reason for high-value claim denials, particularly for large dogs. A "bilateral" condition is one that can affect paired body parts, such as the knees (cruciate ligaments) or the hips.

The Trap: Most insurers have a clause stating that if a condition appears on one side of the body before your policy starts, the other side is permanently excluded.

Example: You adopt a Labrador who had a "minor limp" in his left leg noted in vet records three years ago. You buy insurance today. Next year, he tears the ACL in his right leg. The Outcome: The claim is denied. The insurer views the left-leg limp as evidence of a pre-existing genetic weakness, voiding coverage for both legs.

Who is strict vs. lenient?

- Strict: Healthy Paws and Nationwide generally enforce strict bilateral exclusions. If one side is compromised, the other is often uninsurable.

- Lenient: AKC Pet Insurance is a rare exception. They offer coverage for pre-existing conditions (including bilateral ones) after 365 days of continuous coverage, effectively a "time served" model.

2. Veterinary Inflation is Structural, Not Temporary

If your quote feels high, it’s because the underlying cost of care has fundamentally shifted. Veterinary inflation is outpacing the broader economy, running between 7.8% and 11% in major metros. This isn't just price gouging; it's a "Standard of Care" evolution.

- The Old Days: A limping dog might get crate rest and pain meds.

- 2026 Standard: That same dog gets an MRI ($3,000+) and TPLO surgery ($6,000–$10,000).

The Reality: Insurers are pricing your premium based on the assumption that you will want this "Gold Standard" care.

3. The "Decoupling" of Wellness Plans

In 2026, you will notice that "Wellness" (routine care) plans are sold more distinctly from insurance. This is largely driven by regulations like California’s SB 1217, which legally separates "risk" products (insurance) from "discount" products (wellness) to prevent misleading marketing.

The Math Check: For most pet owners, wellness plans are a zero-sum game.

- Typical Cost: ~$25/month ($300/year).

- Typical Max Benefit: ~$250–$400/year for specific items (vaccines, flea meds).

Verdict: Unless you are 100% sure you will max out every benefit (which is rare), you are often better off putting that $25 into a savings account. Treat insurance as protection against the $10,000 accident, not the $50 vaccine.

Top Provider Price Comparison (2026 Landscape)

Finding the "best" price isn't just about sorting by the lowest monthly number. It’s about finding the right financial fit for your specific risk tolerance. In 2026, the market has bifurcated: some companies race to the bottom on price by stripping out coverage, while others charge a premium for "medical-grade" protection. Here is how the top players stack up beyond the brochure.

Best for Budget & Tech-Savvy: Lemonade & Figo

If your priority is a low monthly payment and you are comfortable using an app for everything, these "insurtech" disruptors are hard to beat.

- Lemonade:

- The Price Tag: Often the lowest entry point in the market, with base plans for cats starting around $10 and dogs around $15.

- The Trade-Off: The coverage is "unbundled." A base policy might not cover vet exam fees, physical therapy, or dental illness unless you pay extra to "toggle on" those specific add-ons.

- Why it wins: Their AI claims bot, "AI Jim," holds the record for paying claims in seconds.

- Figo:

- The Price Tag: Competitive pricing for young pets, often under $31/month for dogs.

- The "Powerup": Figo offers one of the shortest waiting periods in the industry—just 1 day for accidents—meaning your coverage kicks in almost immediately.

Best for Medical Safety Net: Trupanion

Trupanion doesn't compete on price; they compete on value. They operate more like human health insurance than property insurance.

- The Price Tag: Expect to pay a premium—often $100+ per month for larger breeds in cities.

- The Value Proposition:

- Direct Pay: They can pay your vet directly at checkout, so you aren't floating $5,000 on a credit card while waiting for a check.

- Lifetime Per-Condition Deductible: You pay the deductible once per condition for the life of the pet. If your dog develops diabetes, you pay the deductible once, and Trupanion covers 90% of the insulin forever.

- Unlimited Caps: They will never cap your payouts, making this the mathematical choice for "catastrophic" risks like cancer.

Best for Older Pets: Spot & Pets Best

Most insurers slam the door on new enrollments once a pet hits age 14. These two providers keep it open.

- The Price Tag: Premiums for seniors will be high (often $150+), but the key is eligibility.

- The Senior Advantage:

- No Upper Age Limit: Both Spot and Pets Best (and ASPCA) have no upper age limit for new enrollments.

- Mobility Focus: Pets Best is known for covering wheelchairs and prosthetic devices, which are critical for aging dogs with mobility issues.

- Orthopedic Speed: Spot has a 14-day waiting period for knee injuries (CCL), whereas most competitors make you wait 6 months. This is huge for senior dogs prone to ligament tears.

| Provider | Best For... | Avg. Cost Tier | Unique Feature |

|---|---|---|---|

| Lemonade | Puppies/Kittens | $ (Low) | Super fast AI claims & modular pricing |

| Figo | Tech-Savvy Owners | $$ (Mid) | 1-Day Accident Waiting Period |

| Trupanion | High-Risk Breeds | $$$ (High) | Vet Direct Pay & Lifetime Deductibles |

| Spot | Seniors & Rescues | $$ (Mid) | No age limit & 14-day knee wait period |

Is Pet Insurance Worth the Cost? (ROI Analysis)

The biggest mistake pet owners make is trying to "beat the house." If you are buying insurance hoping to get back exactly what you paid in premiums, you are doing the math wrong. Insurance isn't an investment product; it is a hedge against bankruptcy.

The "Savings Account" Fallacy

A common argument is, "I’ll just put $50 a month into a savings account." In 2026, the math rarely supports this strategy for catastrophic events.

- The Scenario: You save $50/month for your Golden Retriever.

- The Reality: By year two, you have saved $1,200.

- The Crisis: Your dog tears his ACL (a common injury for the breed). The TPLO surgery costs $6,000 to $10,000.

- The Result: You are short by thousands of dollars.

To self-insure against a standard $10,000 cancer protocol, you would need to save $50 a month for 16 years before you could afford the treatment.

When to Skip It

There are specific times when insurance is not worth the cost.

- Geriatric Enrollment: If you try to insure a 12-year-old dog with pre-existing diabetes, you will pay a massive premium (often $150+) for a policy that excludes the diabetes. In this case, a dedicated savings account is a better option.

- Zero-Risk Tolerance: If you know you would never pursue chemotherapy or complex surgery for your pet due to personal beliefs, high-limit insurance is unnecessary. A budget "Accident-Only" plan is a better fit.

The "Peace of Mind" Dividend

Ultimately, the ROI of pet insurance is measured in hard decisions avoided. In the industry, we call it "Economic Euthanasia"—the heartbreaking moment when a pet owner has to put a treatable animal to sleep simply because they cannot write a check for $5,000. Insurance ensures that medical decisions are based on prognosis, not your bank balance.

Conclusion

The era of cheap, flat-rate pet insurance is over. In 2026, the market has matured into a sophisticated financial ecosystem where prices are precisely calibrated to the "Risk Triangle" of location, breed, and age. While the national average of $62 for dogs and $32 for cats gives you a starting point, your reality will differ.

You might pay $20 for a barn cat in Ohio or $150 for a French Bulldog in Manhattan. But with veterinary costs for standard surgeries now rivaling human healthcare—frequently exceeding $10,000—the question is no longer "is insurance too expensive," but "can I afford to be uninsured?".

Frequently Asked Questions (FAQs)

Why did my pet insurance premium go up 30% this year?

Insurers adjust rates based on your pet's age (moving into a higher-risk age bracket) and "veterinary inflation," which is currently running between 7% and 11%.

Is "Accident-Only" insurance worth it?

Yes, if you are on a tight budget. For ~$16/month, it won't cover cancer, but it will cover the $3,000 bill if your dog breaks a leg or swallows a toy. It is a catastrophic safety net.

Does insurance cover spaying/neutering?

Generally, no. Spaying and neutering are considered "wellness" or elective procedures. While you can buy a "Wellness Rider" to cover it, the extra monthly cost usually equals what you would pay out-of-pocket anyway.

How do I choose between providers if my pet has a pre-existing condition?

The right choice depends entirely on whether the condition is "curable" or "incurable."

- For Curable Conditions (e.g., ear infections, UTIs, kennel cough): Look for providers like ASPCA, Spot, and Pumpkin. These insurers distinguish between temporary and chronic issues. If your pet has been symptom-free and treatment-free for 180 days, they will often "reset" the condition and cover it moving forward.

- For Incurable Conditions (e.g., diabetes, allergies, arthritis): Most insurers will exclude these for life. The notable exception is AKC Pet Insurance, which offers a unique "time served" model—covering pre-existing conditions after you have had continuous coverage for 365 days.

What specific illnesses or treatments are most commonly excluded from standard policies?

Beyond the universal exclusion of pre-existing conditions, be aware of these three common coverage gaps:

- Exam Fees: Many budget plans (like Healthy Paws or Lemonade’s base plan) cover the treatment but not the $75–$150 exam fee charged just to walk into the room.

- Bilateral Conditions: If your dog injured his left knee before coverage, many policies (like Nationwide or Healthy Paws) will automatically exclude the right knee, assuming it is a genetic inevitability.

- Dental Illness: While dental accidents (broken teeth) are usually covered, dental illness (periodontal disease/gingivitis) is often excluded or capped unless you have a specific rider or a premium plan like Fetch.

How quickly do most insurers reimburse claims, and what documentation is typically required?

Speed varies wildly by provider type.

- The Speed: "Insurtech" companies like Lemonade use AI bots to settle simple claims in seconds or days. Traditional carriers often take 15 to 30 days to mail a physical check. For the fastest relief, Trupanion skips reimbursement entirely and pays the vet directly at checkout.

- The Paperwork: To get paid, you typically need to submit the itemized invoice and proof of payment. Crucially, for your first claim, most insurers will demand a comprehensive medical history (often the previous 12–24 months of SOAP notes) to prove the issue wasn't pre-existing. Missing a page here is the #1 reason for denials.

Can I adjust my deductible or reimbursement rate after enrolling, or am I locked in?

You are generally not locked in, but the direction of the change matters.

- Lowering Coverage (Cheaper): You can almost always raise your deductible (e.g., from $250 to $500) or lower your reimbursement (e.g., 90% to 70%) at any time or during renewal to save money on premiums.

- Raising Coverage (Better): If you want to lower your deductible or increase your limits, insurers will often treat this as a "new" application. This means they may re-evaluate your pet, and any conditions that developed since you first enrolled could effectively become "pre-existing" for that new, higher level of coverage.

WhiskerCover is reader-supported. When you click on links to pet insurance partners on our site and purchase a policy, we may earn a commission at no extra cost to you. Learn more about how we make money.