If you’re searching for pet insurance for pre-existing conditions, it probably means your dog or cat has already spent some time at the vet. Maybe it’s allergies, a previous UTI, or a diagnosis that still weighs on you—we’ve all been there.

Many guides seem to avoid this reality, but it matters. This article is here to help. You deserve straightforward, compassionate answers about what’s really insurable in 2026, what likely isn’t, and how you can avoid frustration and wasted money when shopping for coverage for a pet you worry about.

We’ll walk through:

- When pet insurance that covers pre-existing conditions is realistically possible (and when it isn’t).

- How “curable pre-existing conditions” work in real life, not just in marketing copy.

- Which companies are, honestly, the best pet insurance for pre-existing issues—and what they still exclude.

- Practical alternatives if every insurer keeps saying no.

My goal is simple: by the end, you’ll know exactly what you can protect, what you can’t, and the smartest next step for your very real, not-perfectly-healthy pet in 2026.

Table of Contents

- What “Pre-Existing Conditions” Really Means in Pet Insurance

- Is Pet Insurance Worth It If Your Pet Already Has a Condition?

- Types of Pre-Existing Conditions & How Insurers Treat Them

- Best Pet Insurance for Pre-Existing Conditions in 2026 (Shortlist)

- Deep Dives: How Each Top Insurer Handles Pre-Existing Conditions

- How to Read Pre-Existing-Condition Fine Print (Without a Law Degree)

- Real-World Scenarios: What Actually Gets Paid (and What Doesn't)

- Expert Insights: What the Data (and Real Pet Parents) Say

- Step-by-Step: How to Choose the Best Pet Insurance for Your Pet's Pre-Existing Condition

- When Insurance Isn’t an Option: Alternatives for Pets With Serious Pre-Existing Conditions

- Frequently Asked Questions (FAQs)

What “Pre-Existing Conditions” Really Means in Pet Insurance

If you feel like every site describes pet insurance pre-existing conditions differently, you’re not alone. The industry could do much better at making this clear for regular pet parents.

The Simple Definition (Without the Legalese)

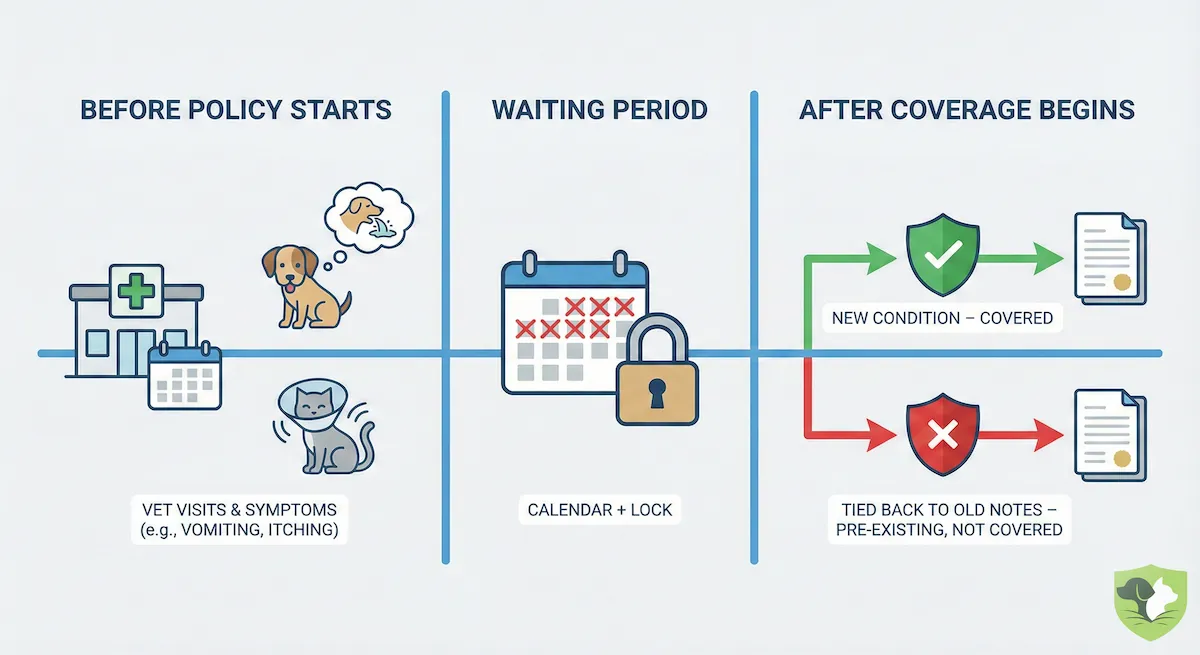

A pre-existing condition is any illness, injury, or symptom your pet had before your policy started or during the waiting period.

It doesn't have to be fully diagnosed. If your vet mentioned "possible allergies" or your dog had repeated vomiting noted in the record, insurers can treat that as pre-existing later. I think the key question is: "Could an adjuster reasonably tie this new claim back to something that showed up before coverage started?" If yes, they'll usually call it pre-existing.

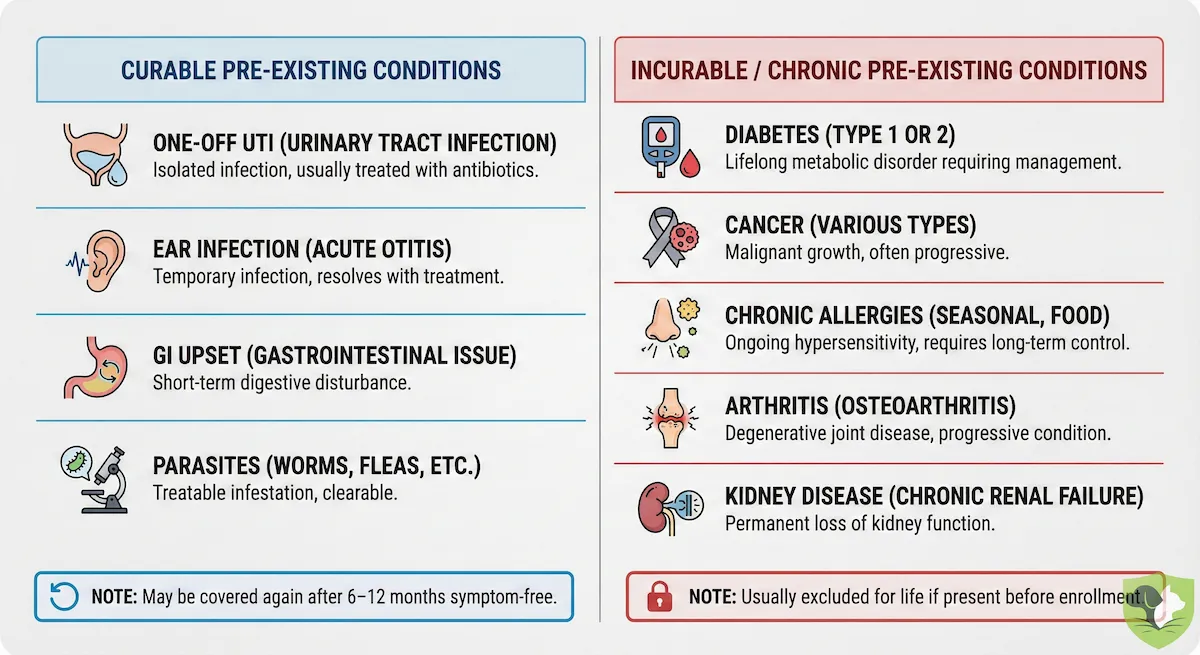

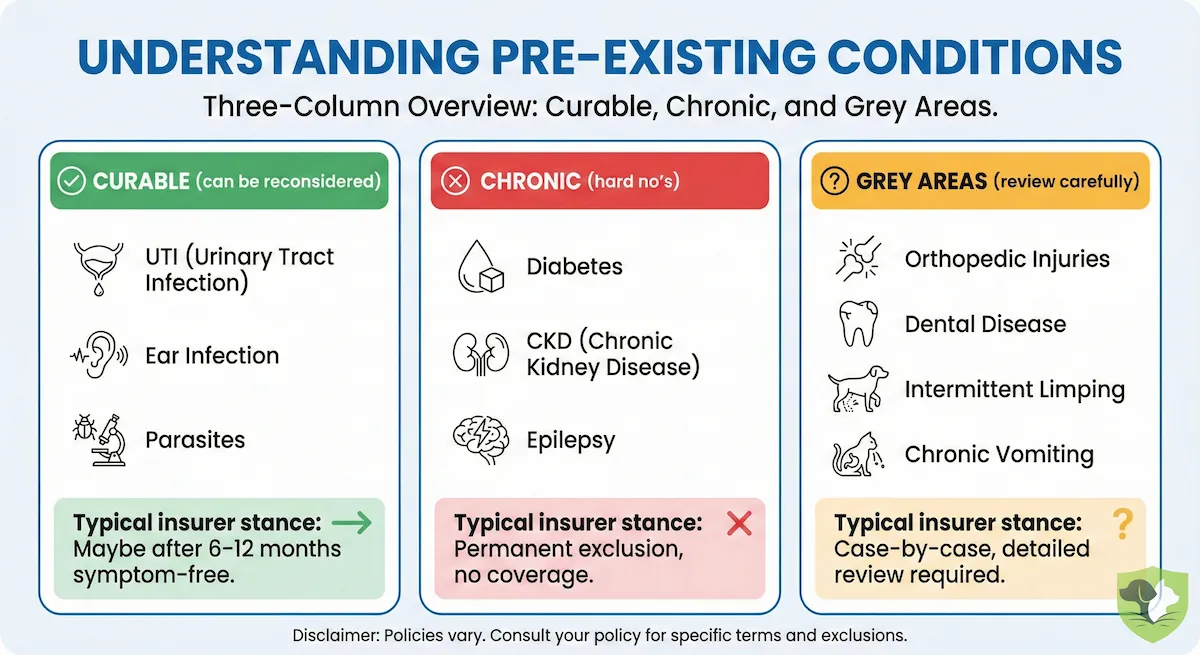

Curable vs Incurable Pre-Existing Conditions

Not all pre-existing issues are treated the same.

- Curable pre-existing conditions: things like a one-off UTI, an ear infection, a simple GI upset, or parasites. If your pet is symptom-free for a set time (often 6–12 months), some companies will cover it again.

- Incurable or chronic conditions: diabetes, cancer, chronic allergies, arthritis, and kidney disease. Once these exist before enrollment, they're almost always excluded for life.

In my opinion, understanding this curable vs incurable split is more important than memorizing any brand's marketing pitch.

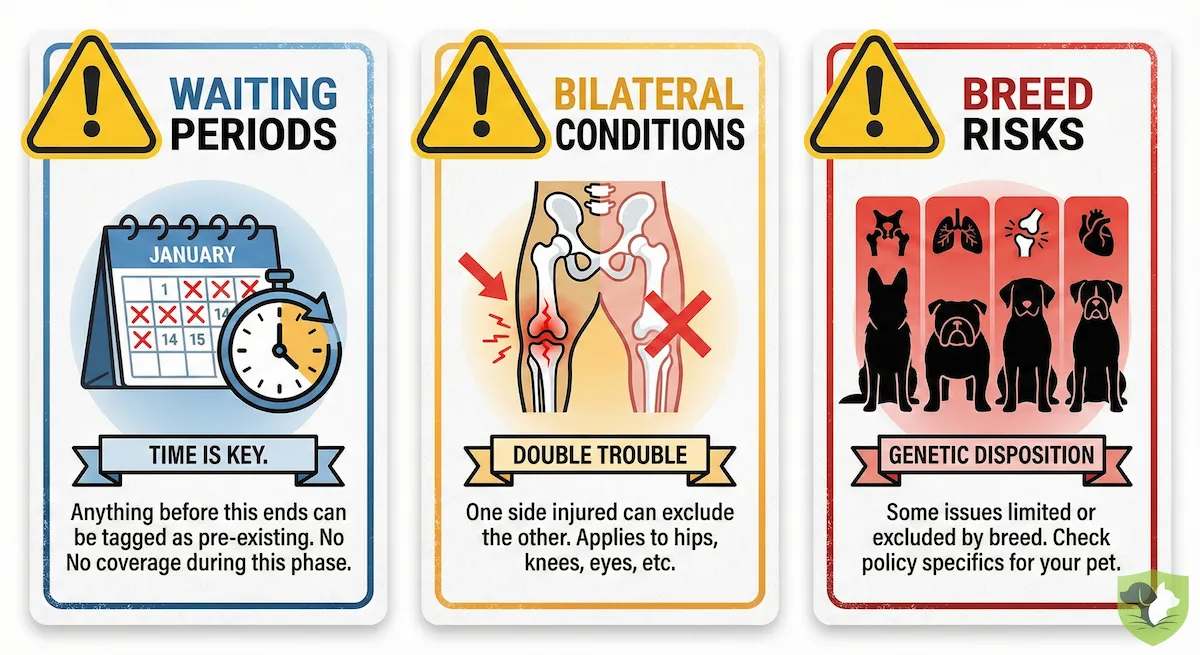

Hidden Traps: Waiting Periods, Bilateral Issues, and Breed Risks

This is where pet insurance exclusions quietly multiply:

- Waiting periods: Anything that pops up before they end can be tagged as pre-existing.

- Bilateral conditions: One torn ACL can exclude the other knee.

- Breed-related issues: Some high-risk conditions (like hip dysplasia in large breeds) may be limited or excluded.

I think of this section as the fine print that decides whether your future claim gets paid—or denied.

Is Pet Insurance Worth It If Your Pet Already Has a Condition?

This is the big question no one really answers. If your pet already has a diagnosis on their record, is pet insurance for pre-existing conditions even worth the money anymore? In my opinion, the answer is: sometimes yes, sometimes absolutely not. The trick is knowing which camp you’re in.

When It Still Makes Sense (Even With Exclusions)

Insurance can still be smart if:

- Your pet has one main issue, but is otherwise young or middle-aged.

- The condition is curable (such as a past UTI, ear infection, or GI bug).

- You can find pet insurance that covers pre-existing conditions once your pet is symptom-free for 6–12 months.

I think of it this way: you’re not buying coverage for the old problem. You’re buying protection for the next crisis you can’t see yet—car accidents, new cancers, surprise surgeries.

When It Probably Doesn’t Pencil Out

It may not be worth it if:

- Your pet is a senior with multiple chronic issues already.

- The main problem is clearly incurable (diabetes, CKD, chronic allergies, long-term arthritis).

- Most quotes feel like high premiums for very low annual limits.

In that scenario, in my opinion, you’re often better off putting that money into a dedicated vet savings fund instead of chasing the best pet insurance for pre-existing conditions that doesn’t really exist for your case.

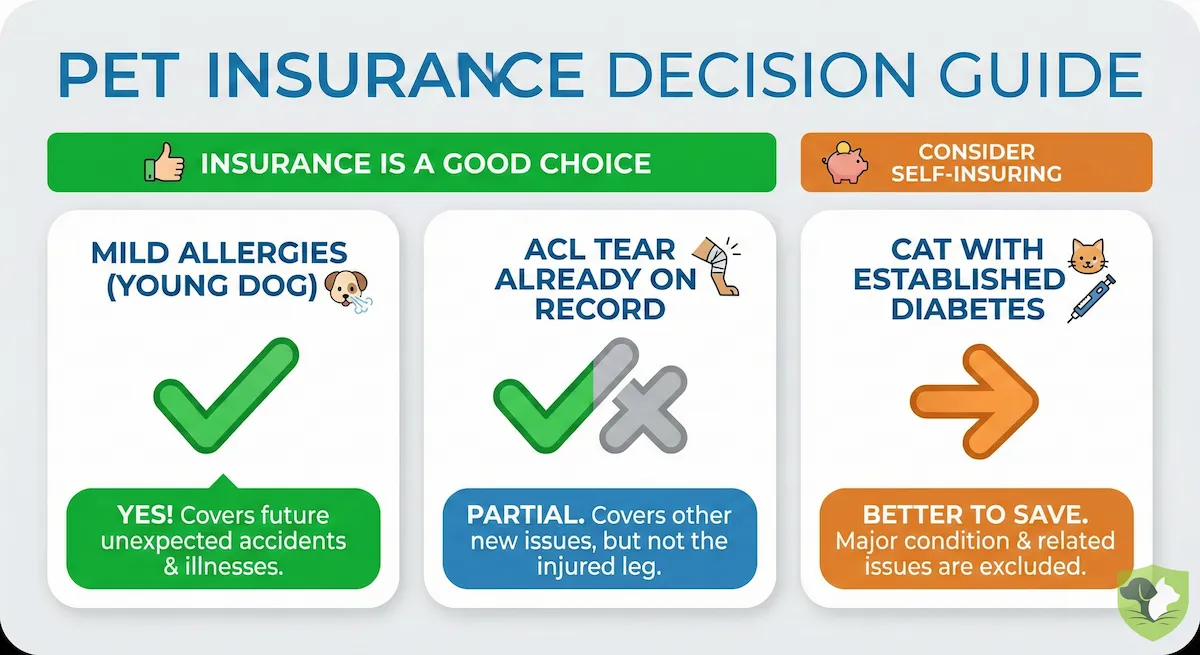

Quick Decision Matrix: Allergies vs ACL Tear vs Diabetes

| Scenario | Verdict |

|---|---|

| Young dog with mild allergies | Yes. Insurance can still make sense for future issues. |

| Dog with an ACL tear on record | Maybe. Coverage for that leg is gone, but other accidents/illnesses may still be worth insuring. |

| Cat with established diabetes | No. Focus on savings, discount plans, and honest talks with your vet. |

I think the goal is to buy insurance where it can still actually do something for you.

Types of Pre-Existing Conditions Types of Pre-Existing Conditions & How Insurers Treat Them

How Insurers Treat Them

Not all pre-existing issues are treated equally. In my opinion, this is where most confusion (and disappointment) comes from.

Curable Pre-Existing Conditions (And Typical Waiting Rules)

These are short-term problems your pet can fully recover from: a one-off UTI, an ear infection, a simple GI upset, parasites, and a minor skin infection. Many of the best pet insurance plans for pre-existing conditions will reconsider these after a “clean” period—often 6–12 months with no symptoms, no meds, no vet notes. I think of these as “probation conditions”: if your pet behaves and stays symptom-free long enough, some companies will treat them like new again.

Incurable or Chronic Conditions (The Hard No’s)

These include diabetes, cancer, chronic allergies, arthritis, kidney disease, and epilepsy. Once these exist before enrollment, they’re generally permanent exclusions. In my opinion, no policy built for profit can afford to take on an already-known, lifelong high-cost condition.

Grey Areas: Orthopedic, Dental, and “Maybe” Conditions

Orthopedic issues, cruciate tears, hip dysplasia, dental disease, and vague symptoms (“intermittent limping,” “chronic vomiting”) live in the grey zone. I think of these as “review carefully” flags—they’re where insurers love to argue something was pre-existing all along.

Best Pet Insurance for Pre-Existing Conditions in 2026 (Shortlist)

Let’s talk names. When people search for pet insurance with pre-existing conditions, they’re usually not asking for theory. They want, “OK, which companies should I actually look at now?” In my opinion, this is where most comparison sites get vague or overly polite. Here’s the blunt version.

At-a-Glance Comparison Table

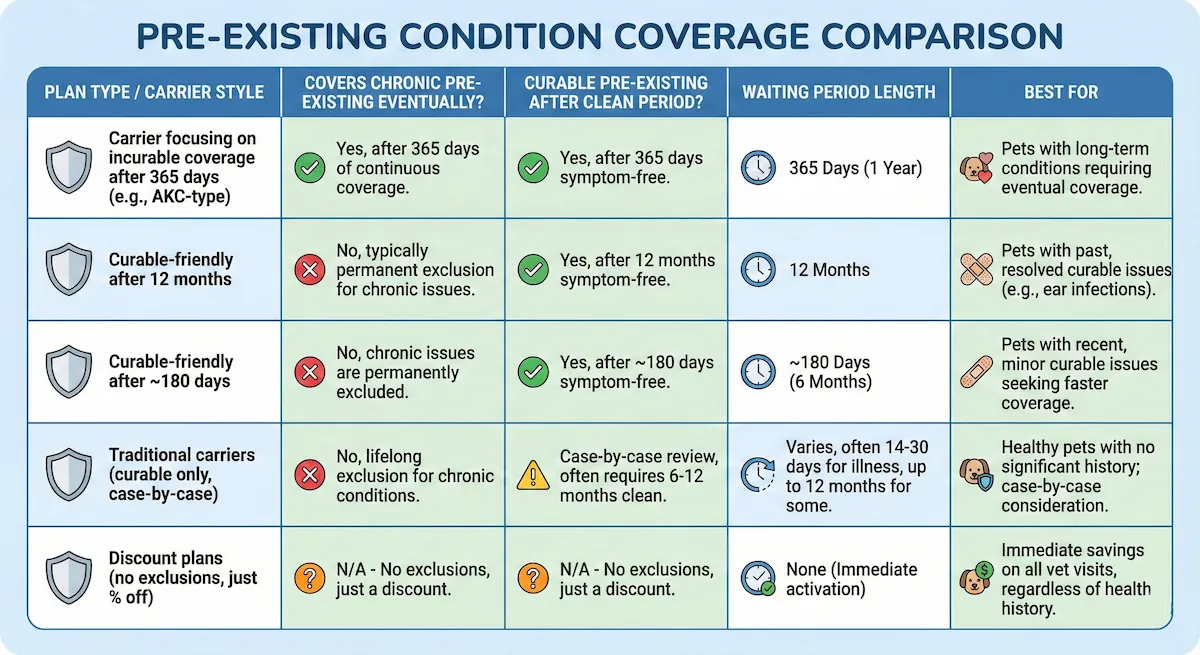

| Company | Policy on Pre-Existing Conditions | Best For |

|---|---|---|

| AKC Pet Insurance | Will consider both curable and some chronic pre-existing conditions after 365 days of continuous coverage (with big caveats). | Dogs with serious history when you’re willing to play the long game. |

| Embrace | One of the few that clearly distinguishes curable vs incurable; some curable pre-existing conditions may be covered again after 12 months symptom- and treatment-free. | Owners willing to wait for a "clean slate" on minor issues. |

| Spot & ASPCA | Similar posture: may cover curable pre-existing conditions again after roughly 180 symptom-free days (knees/ligaments usually excluded). | Rescue pets with minor, resolved medical histories. |

| Pumpkin | Like many, excludes pre-existing up front, but may reconsider some curable issues after a symptom-free period (around 180 days). | Cats and younger pets (high reimbursement rates). |

| Nationwide / Pets Best | Typically no coverage for chronic pre-existing, but may be flexible on curable one-offs after 6–12 months. | Existing customers or specific needs (mobility). |

| Pet Assure | Not insurance. No exclusions, no deductibles; they just ignore pre-existing conditions and give a flat discount. | Pets that have been denied by everyone else. |

I think of this list as your “shortlist to investigate,” not a final answer. The fine print still matters a lot.

Best for Dogs With Pre-Existing Conditions

For dogs, AKC is the standout if you’re specifically hunting for pet insurance that covers pre-existing conditions (including some chronic ones) after a long wait. It’s not magic, but it’s unique. For mostly healthy dogs with one or two past issues, I’d personally start quotes with Embrace, Spot, ASPCA, or Pumpkin, and then compare prices and waiting rules side by side.

Best for Cats With Pre-Existing Conditions

Cats often have UTIs, GI flare-ups, or early kidney flags on their record. In my opinion, Pumpkin, Embrace, ASPCA, and Spot are the main brands worth checking first for curable pre-existing conditions, then comparing how they treat kidney, urinary, and dental illness risk.

Best “Non-Insurance” Option for Pets Nobody Will Cover

If every quote is “no, no, no,” I think it’s time to reframe. A discount plan like Pet Assure, plus a dedicated savings account, can be more honest and less stressful than paying for a policy that will never touch your pet’s real issues.

Deep Dives: How Each Top Insurer Handles Pre-Existing Conditions

Here’s where we get specific. In my opinion, this is the part most “best of” lists rush through, even though it’s what actually decides if your claim gets paid.

AKC Pet Insurance – The Rare Option for Incurable Pre-Existing Conditions

AKC is the closest thing you’ll find to pet insurance that covers pre-existing conditions in a meaningful way. After 365 days of continuous coverage, AKC can start covering both curable and incurable pre-existing conditions—yes, even chronic allergies, heart disease, epilepsy, cancer, etc. Your pet doesn’t have to be symptom-free during that year, which is wild compared with everyone else. The catch? Annual payout caps (often around $10,000) and the usual pet insurance exclusions on things like routine care. In my opinion, AKC is the go-to if your pet already has serious diagnoses and you’re willing to play the long game.

Pumpkin – Strong for Curable Pre-Existing Issues (Especially Cats)

Pumpkin treats pre-existing conditions like most mainstream insurers: chronic issues stay excluded, but curable pre-existing conditions (like a one-off infection or GI bug) can be covered again after about 180 days symptom- and treatment-free. I think Pumpkin is especially attractive for cats and younger pets: no age cap, solid 80–90% reimbursements, and relatively straightforward waiting periods.

Embrace – Curable Pre-Existing Coverage After 12 Months

Embrace is one of the few carriers that clearly spells out a 12-month clean period: if a curable condition hasn’t shown symptoms or needed treatment for a full year, they may cover it again. Chronic stuff still stays excluded, but in my opinion, Embrace is strong for owners willing to think long-term about minor past issues.

Spot, ASPCA, Hartville – The 180-Day Symptom-Free Crowd

These three behave similarly: most pre-existing conditions are excluded, but if an issue was fully resolved and your pet stays symptom-free for 180 days, they may treat a recurrence as new and cover it. Knees/ligaments are usually the big exception—once a cruciate problem exists, it’s out for good. I think of them as “curable-friendly but orthopedic-grumpy.”

Nationwide / Pets Best / ManyPets – Case-by-Case and Curable Only

Nationwide (and some similar brands) will not touch active chronic conditions, but they may reconsider a cured issue after about six months with no symptoms—if you proactively ask and provide records. In my opinion, these are fine if you’re already there as a customer, but I wouldn’t choose them specifically for pre-existing coverage.

Pet Assure – Discount Plan That Ignores Pre-Existing Conditions Completely

Pet Assure isn’t insurance; it’s a veterinary discount plan. That’s why it happily includes pets of any age and health status—no underwriting, no pre-existing questions, just a flat discount on covered services. I think of Pet Assure as the honest option when every insurer has said “no”: it won’t pay your bills, but it also doesn’t punish your pet for having a medical history.

How to Read Pre-Existing-Condition Fine Print (Without a Law Degree)

This is where, in my opinion, people either protect themselves… or get burned. The wording around pet insurance pre-existing conditions and pet insurance exclusions is where everything actually happens.

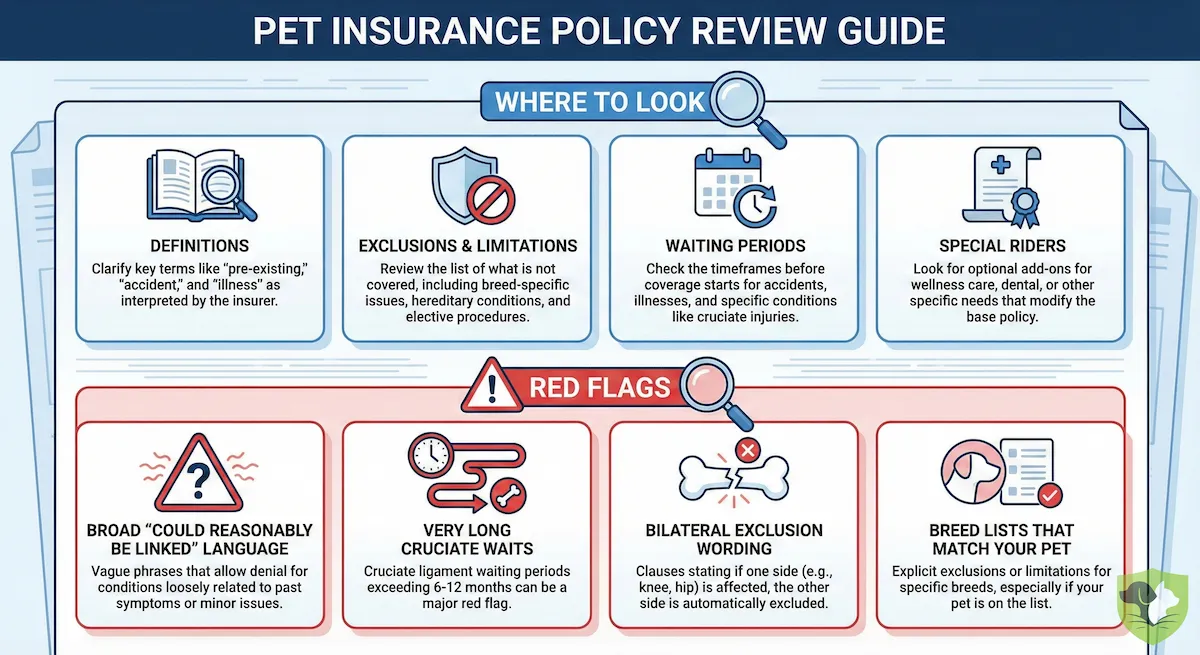

Where to Look in a Sample Policy

When you download a sample policy (you always should), I think you start with four sections:

- Definitions – how they define “pre-existing condition,” “symptoms,” and “onset.”

- Exclusions & Limitations – the master list of “we will not cover…”

- Waiting Periods – different waits for accidents, illnesses, and orthopedic issues.

- Special Riders/Endorsements – orthopedic riders, hip dysplasia clauses, breed-specific notes.

If a company makes these sections hard to find, that’s already a red flag in my book.

Red Flags That Should Make You Pause

In my opinion, you should slow down or walk away if you see:

- Super broad language like "any condition that could reasonably be linked…"

- Very long illness or cruciate waiting periods (6–12 months).

- Bilateral language that lets them exclude the "other side" forever.

- Breed lists that basically target your exact dog or cat.

These are the little sentences that later become big denials.

Questions to Ask Before You Click “Buy”

I think you should email or chat with support and ask, in writing:

- How do you treat curable pre-existing conditions after X months symptom-free?

- Do you ever re-evaluate exclusions? Under what rules and timeline?

- How do you handle vague notes like “intermittent limping” in records?

If they can’t answer clearly, that tells you a lot.

Real-World Scenarios: What Actually Gets Paid (and What Doesn't)

This is the part I wish every pet insurance pre-existing conditions page started with: real timelines, real outcomes. In my opinion, this is how you actually understand "Does pet insurance cover pre-existing conditions or not?"

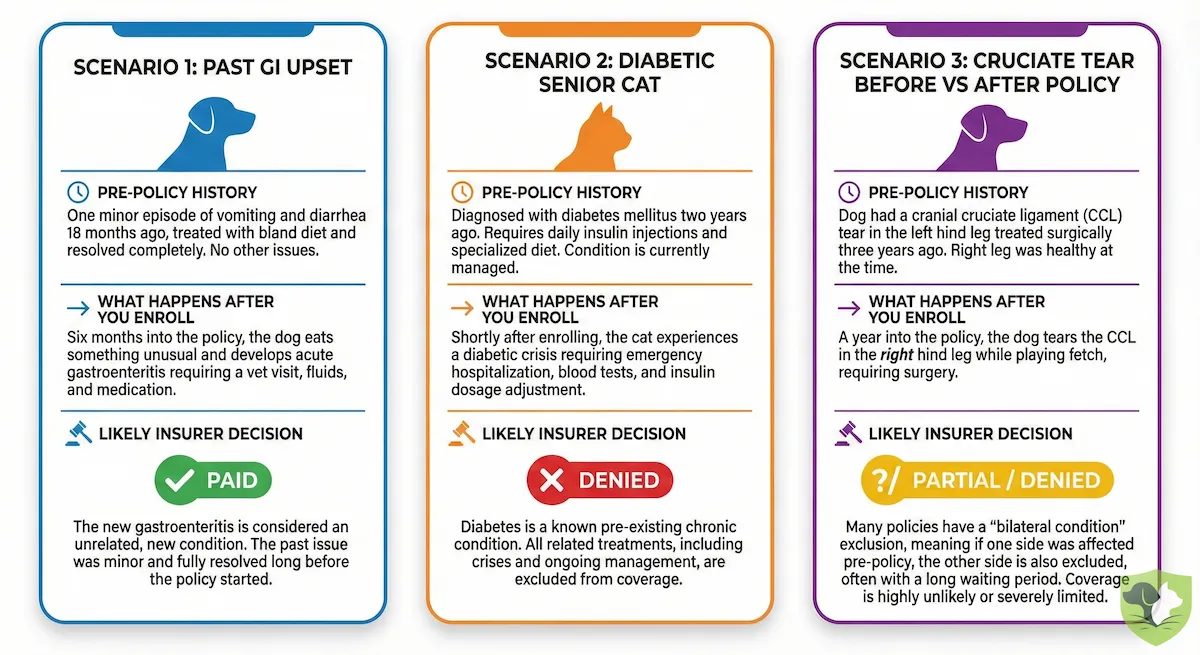

Scenario 1 – Dog With a Past GI Upset and a New Claim

Your dog had one bad vomiting episode 10 months before you bought insurance. Vet note: “suspected dietary indiscretion, resolved.” You enroll, pass the illness waiting period, and a year later, there’s a new, unrelated GI crisis. If the first episode is treated as a curable pre-existing condition and your dog has been symptom-free ever since, many “curable-friendly” insurers will pay this new claim. I think this is a case where insurance really can work for you.

Scenario 2 – Senior Cat With Diabetes and a New Infection

Your older cat is diagnosed with diabetes before enrollment. That diabetes care is excluded forever. Six months into the policy, the cat gets a urinary infection not clearly tied to diabetes. Most plans will still cover the UTI treatment, but not the insulin, monitoring, or diabetic complications. In my opinion, this is a “partial win” scenario—insurance helps at the edges, not with the main battle.

Scenario 3 – Cruciate Tear Before vs After Policy

If your dog tore an ACL before coverage, anything related to the knees is usually excluded. Tear it after the waiting period? That surgery is typically covered—unless there was limping noted before. I think knee cases are where the fine print bites the hardest.

Expert Insights: What the Data (and Real Pet Parents) Say

When you zoom out from individual stories, pet insurance pre-existing conditions look very different from the marketing.

How Common Pet Insurance Really Is (And Why That Matters)

Only a slice of US pets are insured, but the number keeps climbing every year. In my opinion, that matters because insurers are tightening how they define pre-existing conditions as claims volume grows. The earlier you get in, the better your pet’s record looks.

Vet Bills vs What People Think Pet Insurance Costs

Most people wildly underestimate emergency vet bills and overestimate premiums. I think that’s why so many wait until after a diagnosis. By then, “pet insurance that covers pre-existing conditions” is mostly off the table, and you’re stuck with exclusions.

The #1 Regret Theme From Reddit & Forums

Reading owner stories, one pattern screams: “I wish I’d bought before this happened.” Not “I wish I’d found a cheaper plan,” but “I waited until it was already pre-existing.”

What Vets and Industry Guides Recommend for Pre-Existing Conditions

Vets I’ve seen quoted are surprisingly aligned: insure early, don’t expect cures for chronic pre-existing issues, and use insurance to protect against the next big thing, not the one already on the chart. In my opinion, that mindset shift changes everything.

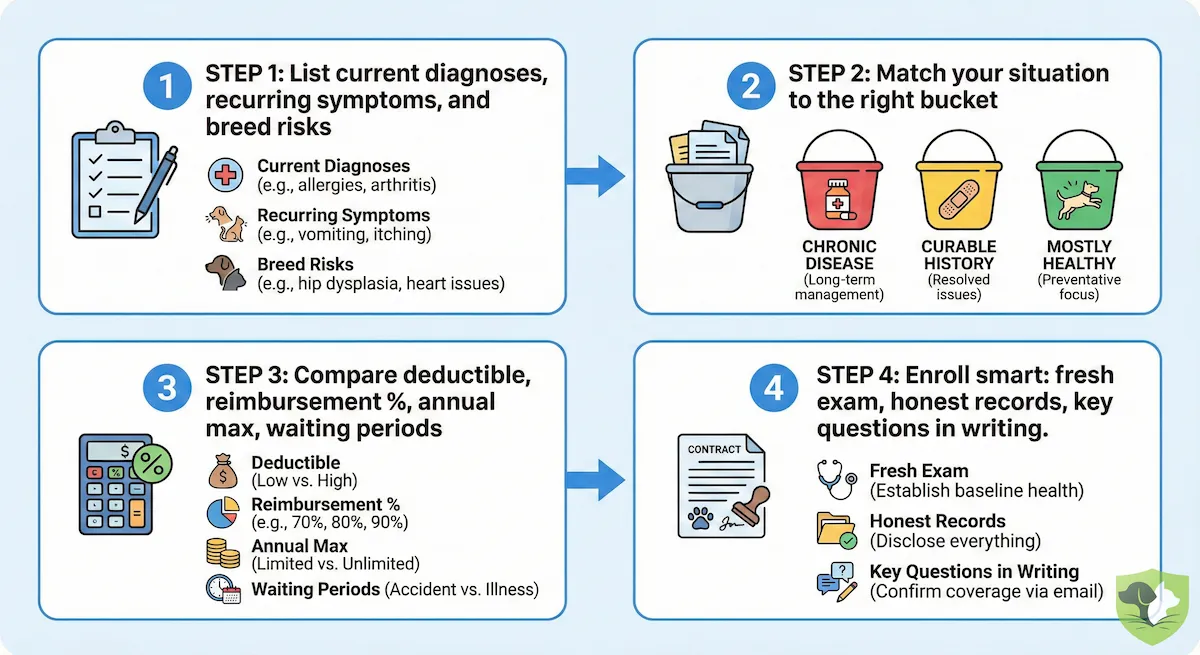

Step-by-Step: How to Choose the Best Pet Insurance for Your Pet's Pre-Existing Condition

If you feel overwhelmed comparing plans, you're not alone. In my opinion, choosing the best pet insurance for pre-existing issues gets way easier if you follow a simple framework.

Step 1 – List Your Pet’s Current and Likely Future Issues

Grab a notepad. Write down:

- Existing diagnoses

- Recurring symptoms (“ear infections 2–3 times a year”)

- Breed risks (hips, heart, breathing, cancers)

I think this is your reality-check list. Insurers will see all of this anyway.

Step 2 – Match Your Situation to the Right “Bucket”

Roughly:

- Chronic pre-existing disease already on record → AKC / discount plan / savings.

- One or two curable pre-existing conditions in the past → Embrace, Pumpkin, Spot, ASPCA.

- Young and mostly healthy → broader choice; focus on price and extras.

Step 3 – Compare Real Numbers, Not Logos

For each quote, compare:

- Deductible

- Reimbursement %

- Annual max

- Waiting periods and pet insurance exclusions

In my opinion, this “mini spreadsheet” tells you more than any award badge.

Step 4 – Enroll the Smart Way

Get a fresh exam, keep records, and be fully honest on applications. If something matters a lot, I think you should email the insurer and ask for the answer in writing before you buy.

When Insurance Isn’t an Option: Alternatives for Pets With Serious Pre-Existing Conditions

Sometimes, after you’ve checked every quote, the answer to pet insurance pre-existing conditions is still basically “no.” In my opinion, that doesn’t mean you’re out of options—it just means the strategy has to change.

Veterinary Discount Plans and Employer Benefits

If traditional insurance won’t touch your pet’s history, I think discount plans are the next thing to look at. Programs like vet discount cards or Pet Assure don’t exclude pre-existing conditions at all—they simply knock a flat percentage off covered services at participating vets. Also, check your HR portal. More employers now offer pet benefits: small insurance stipends, negotiated discounts, or tele-vet access. It’s not a magic fix, but stacked together, it can noticeably lower your bills.

Building a DIY “Pet Health Fund”

If you were ready to spend $60–$100/month on premiums that don’t really help, consider redirecting that into a separate savings account. In my opinion, an automatic transfer into a “pet fund” is the most honest way to self-insure a pet with serious pre-existing issues. No exclusions, no denials—just money you control.

Talking With Your Vet About Realistic, Compassionate Plans

I think one of the most underrated tools is an honest money talk with your vet. Tell them your pet’s conditions and your budget. Ask about:

- Generic vs brand-name drugs

- Staging tests over time instead of all at once

- Payment plans or lower-cost clinics for specific procedures

In my opinion, a good vet would rather help you build a realistic, compassionate plan than watch you avoid care out of fear.

Frequently Asked Questions (FAQs)

Does pet insurance ever cover pre-existing conditions?

Sometimes. In my opinion, you should assume active chronic conditions are excluded, but some companies will cover curable pre-existing conditions (and AKC may reconsider some chronic ones later).

What counts as curable vs incurable in practice?

Curable: one-off issues that fully resolve (UTI, ear infection, GI bug).

Incurable: long-term diseases like diabetes, CKD, epilepsy, and chronic allergies.

I think the key test is: can it truly go away?

Do I have to send my pet’s full medical history?

Yes, eventually. Insurers will ask your vets for records when you claim. In my opinion, it’s better to assume they’ll see everything and be honest from day one.

Can switching companies wipe my pet’s record clean?

No. Your pet’s body doesn’t reset when you change logos. New insurers will still treat anything in the old records as pre-existing.

How long does my pet need to be symptom-free before a condition is covered again?

Often, 6–12 months for curable issues, if at all. Each company is different, so I think you should ask for their rule in writing.

Is accident-only insurance worth it if my pet has a chronic illness?

Sometimes, yes. It won’t touch the chronic disease, but it can still save you from broken legs, car accidents, or swallowed toys.

Can I insure multiple pets when one has a pre-existing condition?

Absolutely. One pet’s pre-existing condition doesn’t “infect” the others. I think multi-pet discounts can still make sense in that case.

WhiskerCover is reader-supported. When you click on links to pet insurance partners on our site and purchase a policy, we may earn a commission at no extra cost to you. Learn more about how we make money.