You don’t really care about pet insurance. You care about not having to choose between your savings and your pet’s life at 2 a.m. at the emergency vet.

Most people only learn what pet insurance covers after they’re staring at a $3,000+ estimate. They assume, “It’s insurance, so it’ll cover most of this,” and then run headfirst into exclusions, waiting periods, and pre-existing condition rules.

If your dog or cat is family, you deserve straight answers. This guide breaks down what’s covered, what’s not, how pet insurance pre-existing conditions work, and how to avoid the most painful surprises.

Table of Contents

- Quick Answer – What Pet Insurance Usually Covers (and Doesn’t)

- How Pet Insurance Coverage Works (Without the Jargon)

- What Pet Insurance Covers: The Medical Stuff That Actually Matters

- What Pet Insurance Doesn’t Cover: The Fine Print That Bites

- Pet Insurance Pre-Existing Conditions, Curable vs Incurable, and Bilateral Rules

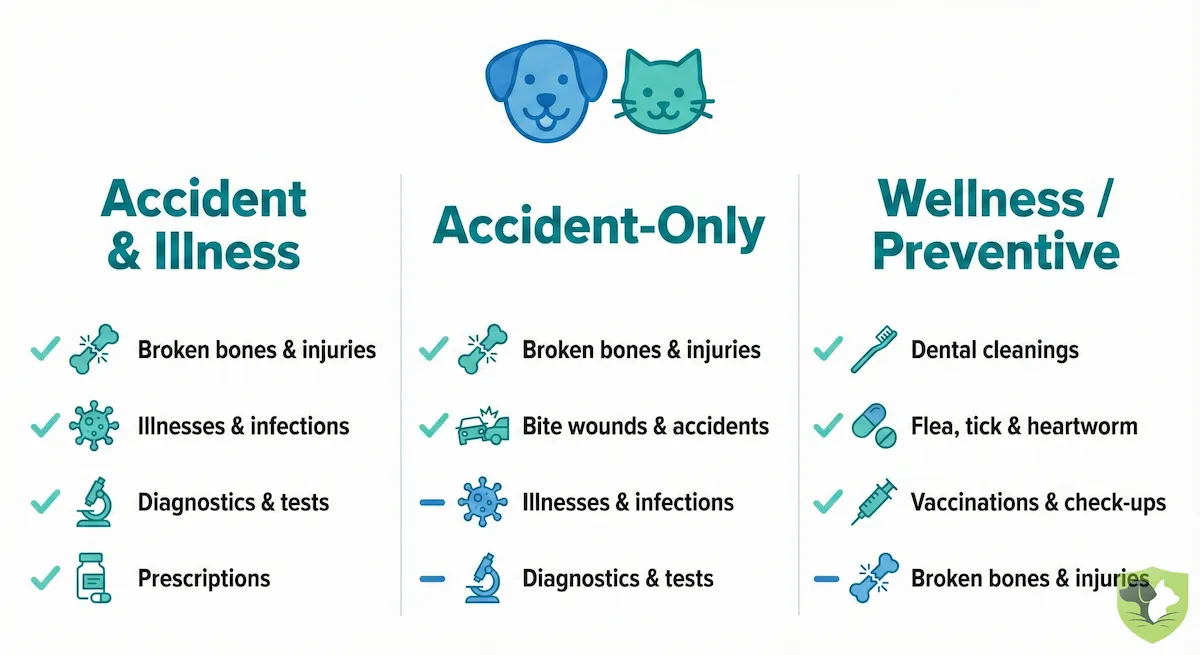

- Accident-Only vs Accident & Illness vs Wellness: Picking the Right Mix

- Expert Insights: How Policies Are Structured (and Where People Get Burned)

- Scenario Snapshots – How Coverage Plays Out in Real Life

- Key Takeaways – What Pet Insurance Covers (and Doesn’t)

- Final Thought

- Frequently Asked Questions (FAQs)

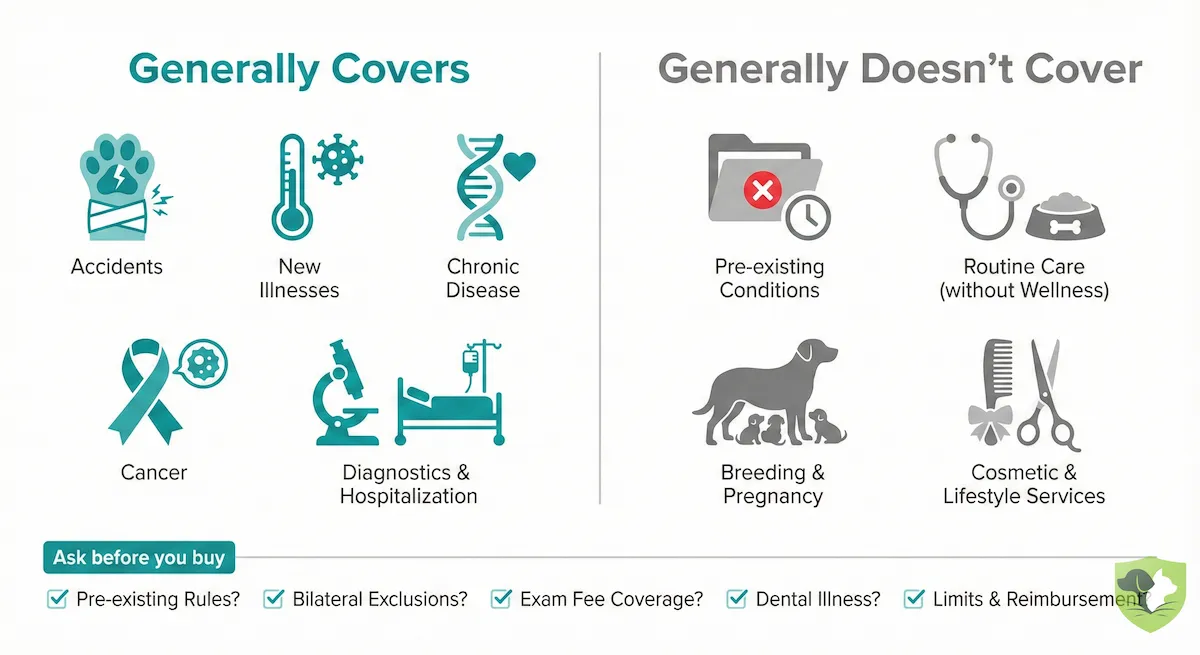

Quick Answer – What Pet Insurance Usually Covers (and Doesn’t)

What Pet Insurance Typically Covers

NAPHIA groups pet insurance products into accident-only, accident & illness, insurance with embedded wellness, and endorsements. Most accident & illness plans focus on the big, unexpected stuff:

- Accidents: Broken bones, swallowed toys or foreign objects, bite wounds, cuts, burns, and poison or toxin ingestion.

- Illnesses: Ear and eye infections, vomiting, diarrhea, pancreatitis, skin allergies and hot spots, urinary tract infections, diabetes, kidney disease, heart disease, cancer, and other serious diseases.

- Diagnostics & Treatment: Bloodwork, urinalysis, X-rays, ultrasound, advanced imaging (MRI/CT), surgery, hospitalization, prescription meds, and follow-up visits for covered conditions.

Covered diagnostic tests can include bloodwork, urinalysis, X-rays, ultrasound, MRI/CT, and lab work. Coverage can vary based on the insurer, state, policy type, add-ons, waiting periods, and whether the condition is eligible.

In simple terms: sudden accidents + new illnesses + the testing and treatment around them, as long as the condition is eligible under the policy and past any waiting period.

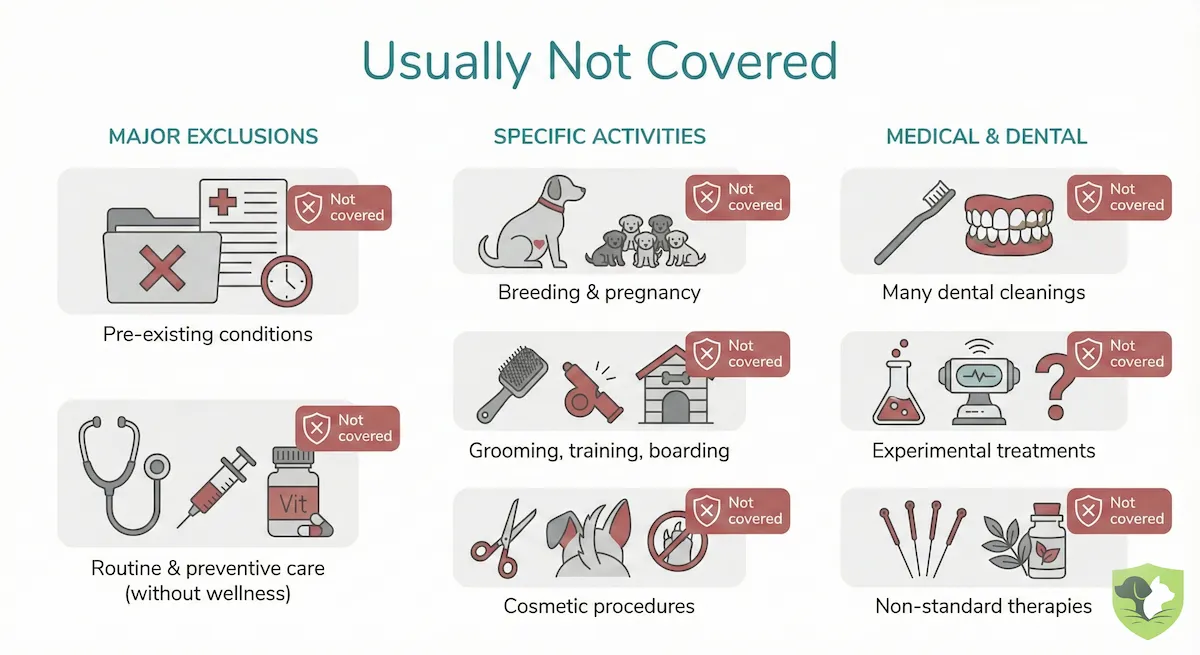

What Pet Insurance Usually Doesn’t Cover

Most plans do not cover:

- Pre-existing conditions (anything with advice, treatment, or signs and symptoms before coverage starts or during a waiting period).

- Routine and preventive care (wellness exams, vaccines, flea/tick meds) unless you add wellness or preventive coverage.

- Breeding, pregnancy, and whelping, unless a specific policy or add-on says otherwise.

- Cosmetic or elective procedures (ear cropping, declawing, tail docking).

- Grooming, boarding, training, pet-sitting.

- Routine dental cleanings and some dental diseases, depending on the plan.

- Experimental or non-standard treatments.

- Many admin line items and some end-of-life costs.

We’ll unpack these in more detail, but this is the snapshot.

How Pet Insurance Coverage Works (Without the Jargon)

Before worrying about brands and quotes, it helps to know what kind of product you’re actually buying. Pet insurance is usually reimbursement-based: you pay the vet, submit a claim, and the insurer pays you back for eligible expenses.

Some insurers offer direct-pay options at participating hospitals, but you should not assume that is available unless the provider and vet confirm it.

The Three Main Types of Pet Insurance

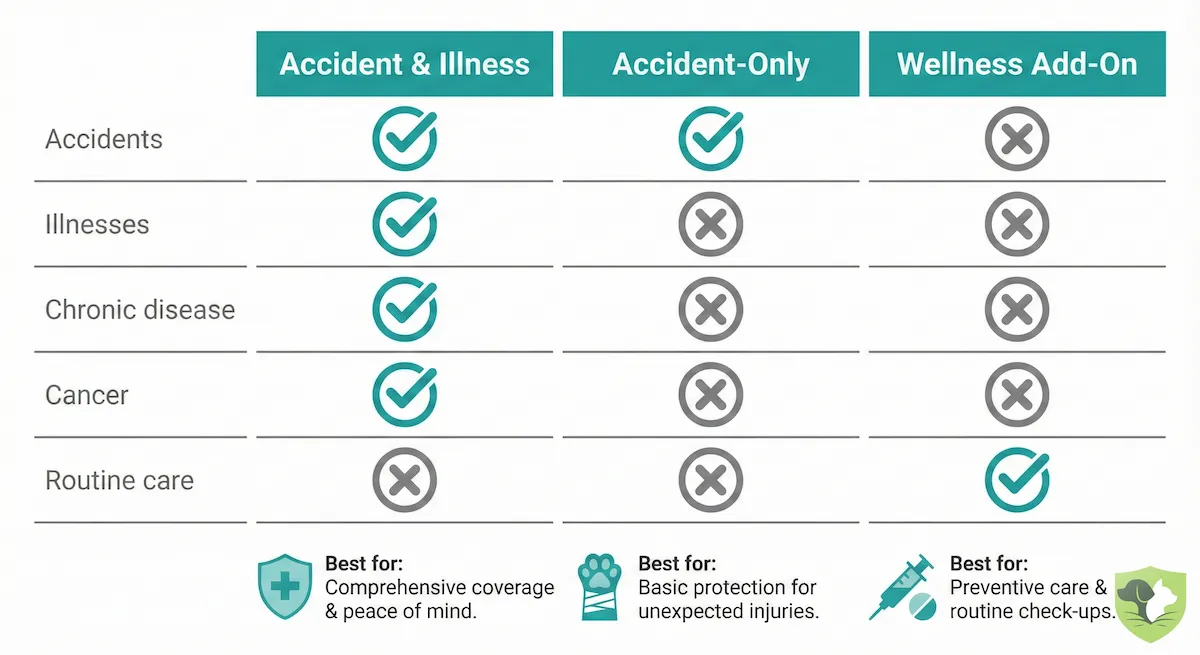

1. Accident & Illness (Most Common)

This is what most people mean when they say “pet insurance.” It usually covers:

- Accidents (injuries, swallowed objects, toxins)

- Illnesses (infections, chronic disease, cancer)

- Diagnostics and treatments (tests, surgery, meds, hospital stays)

If you want protection from both ER disasters and serious illnesses, this is the lane. NAPHIA defines accident & illness coverage as accident benefits plus illnesses such as cancer, infections, and digestive problems.

2. Accident-Only

Cheaper, but much narrower. Generally covers broken bones, wounds, trauma, swallowed objects, ligament tears, and poisoning.

It does not cover infections, allergies, arthritis, diabetes, kidney disease, cancer, or any illness at all. Useful for some senior pets or very tight budgets, but very limited.

3. Wellness / Preventive Plans

Wellness programs are usually separate subscription or reimbursement programs for routine care, not a replacement for medical insurance. They often help pay for annual wellness exams, vaccines, flea/tick/heartworm prevention, basic screening tests, and sometimes spay/neuter, microchipping, or routine dental cleaning.

Wellness is a budgeting tool. Accident & illness is risk protection.

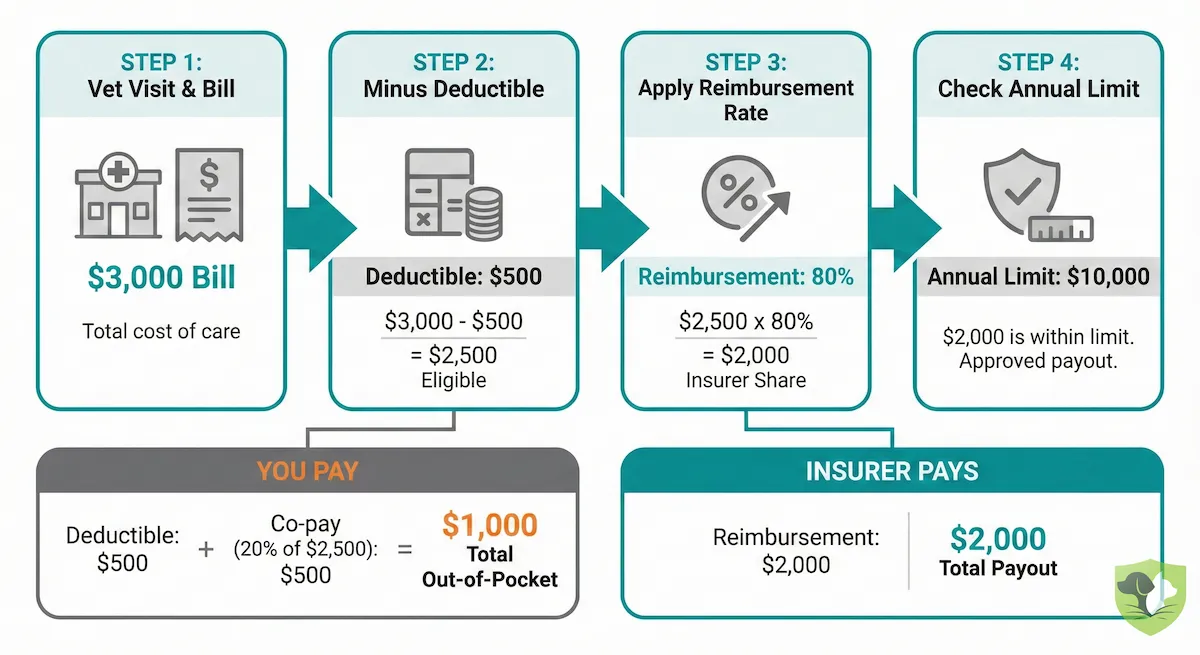

How Reimbursement Works

With most pet insurance, you go to the vet and pay the bill, then submit a claim through the insurer’s app or website. The insurer reimburses you based on your plan.

Three numbers decide how much you really get back:

- Deductible: The amount you pay before insurance starts paying. Often annual (e.g., $250, $500) or per-condition.

- Reimbursement rate: The percentage the insurer covers after the deductible. Common options: 70%, 80%, 90%.

- Annual (or lifetime) limit: The most the insurer will pay in a policy year (or over your pet’s lifetime). e.g., $5,000, $10,000, or unlimited.

Get those three settings right, and the policy will behave closer to the way you expect when a big bill hits. Then check what the reimbursement is based on:

- Actual vet bill: Reimbursement is based on the eligible charges on your invoice.

- Benefit schedule: The policy pays up to a set amount for each covered condition or service.

- Usual-and-customary fees: The insurer caps payment at what it considers typical for that care in your area.

The NAIC Model Act requires insurers using those formulas to disclose how claim payments are determined.

What Pet Insurance Covers: The Medical Stuff That Actually Matters

Now let’s get specific about what pet insurance covers when your dog or cat needs real help. For cat-specific coverage questions, our pet insurance for cats guide goes deeper on feline risks and pricing.

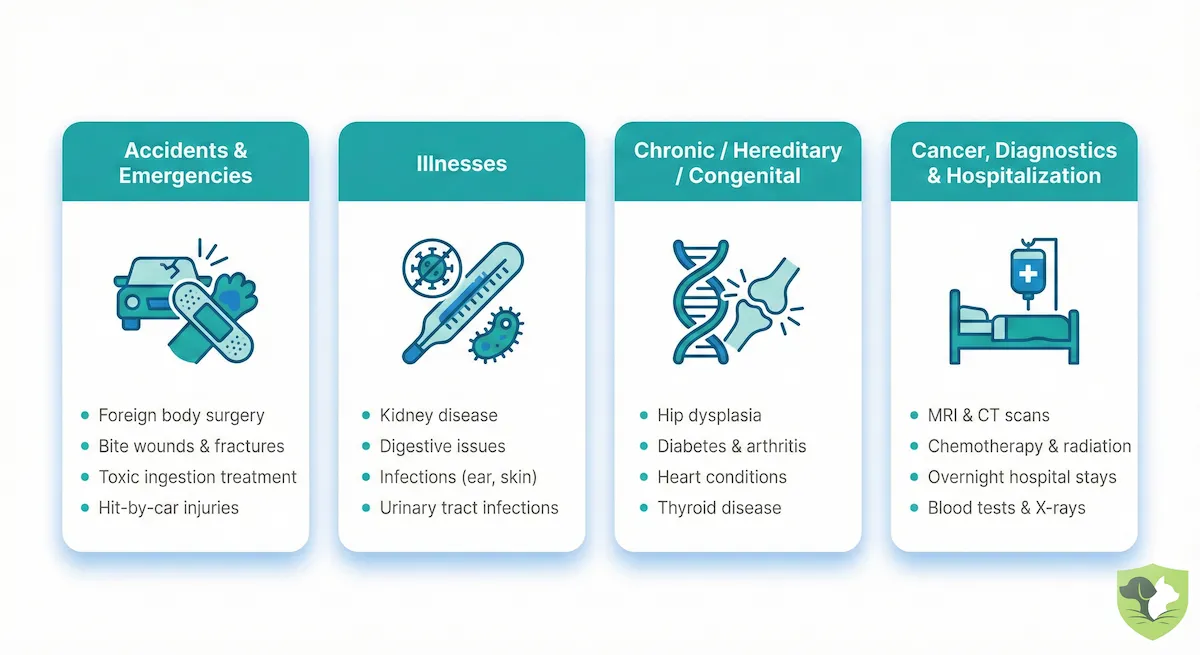

Accidents and Emergencies

This is where pet insurance often saves people from draining savings or maxing out cards.

Common covered accidents: Hit by a car, broken or fractured bones, bite wounds and deep cuts, foreign body ingestion (toys, socks, bones, string), poison or toxin ingestion (chocolate, meds, toxic plants), and burns or other serious trauma.

Typical covered costs around those: ER exam and emergency fees when included, X-rays, ultrasound, and other imaging, surgery and anesthesia, hospitalization and IV fluids, pain meds and follow-up care.

If it’s sudden, accidental, and serious, it often fits accident coverage, subject to the policy’s waiting period, exclusions, and eligible-expense rules.

Illnesses: From “Off” to “Oh No”

Illness is where costs quietly keep coming. Most accident & illness plans cover:

- Ear and eye infections

- GI issues: vomiting, diarrhea, pancreatitis

- Skin allergies and hot spots

- Respiratory infections

- Urinary tract and bladder problems

As pets age, this often expands into kidney and liver disease, heart disease, thyroid issues, seizure disorders, autoimmune disease, and cancer.

If the problem wasn’t there before you bought the policy and you’re past waiting periods, it’s usually part of your pet insurance coverage.

Chronic, Hereditary, and Congenital Conditions

For many breeds, this section is the big one. Accident & illness plans may cover:

- Chronic issues: allergies, arthritis, diabetes

- Hereditary conditions: hip dysplasia, heart disease, luxating patellas

- Congenital issues: problems present from birth but diagnosed later

Note: Catches to watch: Symptoms can’t appear before you bought the plan (otherwise, they’re pre-existing). Hereditary and congenital coverage varies: some plans include it, some sell it as an add-on, and some apply age or enrollment rules. If you have a Frenchie, Golden, German Shepherd, doodle, or other high-risk breed, read this part of the policy twice.

Cancer Treatment

Cancer is one of the biggest financial shocks in pet care. Most accident & illness policies cover eligible diagnostics (bloodwork, imaging, biopsies), tumor removal surgery, chemotherapy, and sometimes radiation or advanced therapies when the cancer is not pre-existing.

Cancer treatment can easily reach thousands per year. A decent reimbursement rate and a solid annual limit (or unlimited) matter a lot here.

Diagnostics and Hospitalization

The “just to find out what’s going on” portion of the bill adds up fast.

Typically covered diagnostics: Blood and urine tests, X-rays and abdominal ultrasound, CT, MRI (depending on plan), cytology, aspirates, and biopsies.

Typically covered hospital care: Day hospitalization and overnight stays, IV fluids and medications, oxygen cages, intensive monitoring, and ICU care.

If the condition itself is covered, the testing and hospital care around it usually are too.

Behavioral and Mental Health (Sometimes)

Some plans now acknowledge that behavior is a health issue too. You may see coverage for veterinary behaviorist visits, behavior-related medications (e.g., anti-anxiety), and treatment for diagnosed issues like separation anxiety or compulsive licking.

But: Basic obedience or puppy classes are not covered. Some companies exclude behavior entirely or limit it to higher-tier plans.

Alternative and Rehab Therapies

If your vet prescribes them for a covered condition, some plans include physical rehab, hydrotherapy, acupuncture, laser therapy, and chiropractic care.

These may be included, covered only up to a certain amount, excluded from budget versions of a plan, or available as an optional add-on. Look for a section labeled “rehab,” “complementary,” or “alternative therapies.”

Dental: Accidents vs Disease

Dental is its own headache in pet insurance. Many plans are more generous with dental accidents, like broken teeth from trauma, jaw fractures, and emergency extractions after an accident.

Where things get restrictive is dental disease. Routine cleanings are usually preventive/wellness care. Dental illness may be covered, capped, excluded, or tied to dental-care requirements. Complex dental surgery can be limited or excluded. If you have a small dog or a cat prone to dental trouble, this part of the policy is non-negotiable.

What Pet Insurance Doesn’t Cover: The Fine Print That Bites

Now the other side of the coin: what pet insurance doesn’t cover. This is where unpleasant surprises live.

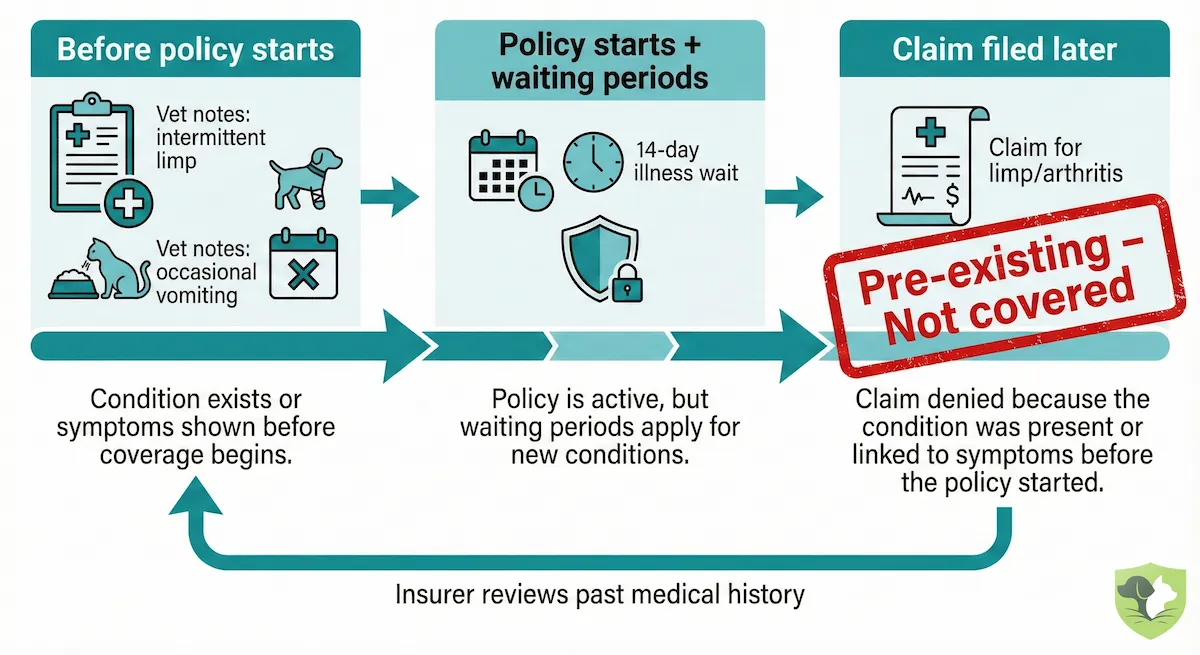

Pre-Existing Conditions

This is the big one. The NAIC Model Act defines a pre-existing condition around prior veterinary advice, previous treatment, or verifiable signs or symptoms before the policy effective date or during a waiting period.

That could include:

- Intermittent limping noted six months ago.

- “Occasional vomiting” visits.

- “Mild heart murmur, monitoring” in the chart.

- Long-standing allergies or chronic ear infections.

Insurers dig through medical records. If they can connect today’s problem to past notes, they may call it pre-existing and deny related claims.

Most pet insurance does not cover pre-existing conditions, although some insurers may re-cover eligible curable conditions after a clean period. AKC also advertises limited pre-existing-condition coverage after 365 days of continuous coverage where available. Enrolling early is your best defense.

Routine and Preventive Care (Without Wellness)

Standard accident & illness policies usually do not cover routine care such as:

- Annual wellness check-ups.

- Vaccines and routine screening labs.

- Flea, tick, and heartworm prevention.

- Fecal tests, nail trims, and anal gland expressions.

- Microchips, unless the policy or add-on clearly includes them.

To get help with this, you either add a wellness plan or budget and pay for routine care yourself. If a plan doesn’t clearly list routine care as covered, assume it’s not.

Pregnancy, Breeding, and Elective Procedures

Most base pet insurance isn’t designed for breeding programs. Commonly excluded items include fertility testing, artificial insemination, routine pregnancy monitoring, whelping, planned C-sections, and elective breeding costs.

Some specialized add-ons may cover certain breeding complications, so breeders need policy-specific language, not generic pet insurance marketing.

Also excluded in most policies: ear cropping, tail docking, declawing, and cosmetic dewclaw removal. If it’s for looks or convenience rather than medical necessity, don’t expect coverage.

Grooming, Training, and Lifestyle Services

Insurers cover medical problems, not lifestyle services. That usually means no coverage for grooming, baths, haircuts, de-shedding, daycare, boarding, dog walking, pet taxis, basic training, or obedience classes.

If it feels like a “Rover, trainer, or groomer” service, it’s generally on you.

Dental Cleanings and Dental Disease

Dental is one of the most misunderstood areas. Most plans don’t cover routine cleanings unless wellness or preventive care is added.

Dental disease coverage varies by insurer. Some accident & illness plans cover eligible dental illness, sometimes with caps or requirements; others exclude much of it. Dental accidents are more likely to be covered than years of neglected teeth.

Experimental, Holistic, and “Nice-to-Have” Treatments

You’ll often see exclusions around anything considered experimental, investigational, or not standard of care. That might include clinical trial treatments, certain alternative therapies, or general wellness supplements not tied to a diagnosis.

Holistic care, like acupuncture or chiropractic treatment, might be covered. But it usually has to be prescribed by a vet, tied to a covered condition, and clearly listed in the policy.

Hidden or Overlooked Exclusions

Small, easy-to-miss exclusions:

- Exam fees and admin charges: Some plans cover diagnostics and treatment, but not exam or waste-disposal fees.

- Prescription foods: Often excluded, or only covered short-term with caps.

- End-of-life costs: Euthanasia may be covered. Cremation, burial, and memorial items are often excluded, minimally covered, or available only through an add-on.

- Bilateral conditions: If one knee, hip, or eye was affected pre-enrollment, the other side can be excluded too.

Individually, these are small. Together, they define the true edges of your coverage.

Pet Insurance Pre-Existing Conditions, Curable vs Incurable, and Bilateral Rules

Let’s zoom in on the thing that causes the most frustration: pre-existing conditions.

How Insurers Decide Something Is “Pre-Existing”

They don’t just look at today. They look back through your pet’s records. A condition is usually called pre-existing if symptoms showed up before your policy started, or symptoms showed up during waiting periods.

Even without a formal diagnosis, repeated patterns count. That “intermittent limp” or “keeps vomiting, likely dietary” can be enough to link later joint surgery or GI disease back to the past. If it’s in your pet’s record before coverage, it can be used to deny future related claims.

Curable vs Incurable Pre-Existing Conditions

Many insurers categorize issues as curable or incurable.

Curable: These can be resolved and stay gone (e.g., one-time ear infection, single UTI, mild respiratory infection, short GI upset that doesn’t recur). Some plans will exclude them at first, then cover them again after a symptom-free period. ASPCA uses a 180-day cured, symptom-free, treatment-free rule for some conditions, while Embrace says temporary conditions may be re-evaluated after 12 consecutive symptom-free and treatment-free months.

Incurable: These tend to stick around or recur (e.g., allergies, arthritis, diabetes, kidney or liver disease, chronic GI disease like IBD, heart disease, epilepsy, cancer). If these start before your policy, they’re typically excluded unless the policy has a specific pre-existing-condition exception.

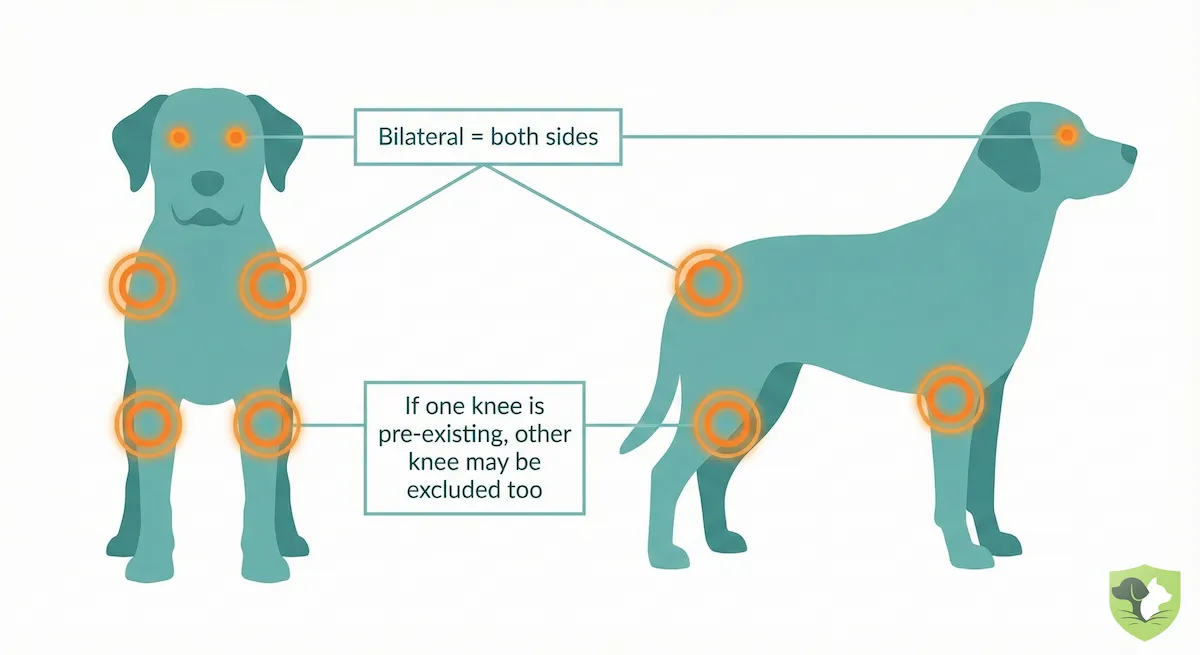

Bilateral Exclusions: When One Side Affects the Other

“Bilateral” = both sides of the body (left/right knees, hips, eyes, ears).

Many policies say: If a condition is pre-existing on one side, the same condition on the other side is also excluded.

Example: Left cruciate ligament ruptures pre-enrollment → noted as pre-existing. Right cruciate ruptures after enrollment. Policy treats cruciate disease as bilateral, so both knees are excluded. Same idea with hips, patellas, and some eye diseases. This matters a lot for breeds prone to orthopedic issues.

Switching Insurers and Losing Coverage

Switching can feel smart financially, but medically, it can be a reset.

When you move to a new insurer: Past issues can become pre-existing under the new policy unless the new insurer explicitly offers applicable pre-existing, cured-condition, or transfer coverage. Chronic problems that were covered under your old policy may be excluded under the new one. So even if a new company is cheaper or has a nicer app, switching can be a downgrade if your pet has an existing medical history.

Often, the best move is: Get a solid plan while your pet is healthy. Stick with it as long as it continues to treat your pet fairly.

Accident-Only vs Accident & Illness vs Wellness: Picking the Right Mix

You’ve seen what each type does. Let’s boil it down.

- Accident & illness is usually the best fit if your pet is young or middle-aged, your breed has known genetic risks, or you want help with both emergencies and serious diseases.

- Accident-only might make sense if your pet is older and can’t qualify for illness coverage, or your budget is tight, but you still want help with injuries.

- Wellness plans are worth considering if you like predictable monthly costs, you already plan to keep up with exams and vaccines, and you understand wellness is budgeting, not risk transfer.

Order of operations: Buy the strongest medical (accident & illness) coverage you can comfortably afford. Decide whether accident-only is an acceptable compromise if you truly can’t. Add wellness if it fits how you like to manage routine costs.

Expert Insights: How Policies Are Structured (and Where People Get Burned)

How Most U.S. Pet Parents Actually Use Insurance

In practice: Accident & illness is the dominant product. Accident-only is used by a smaller group, and wellness is usually an add-on or embedded feature, not the main event.

A common setup for many shoppers: accident & illness policy, optional wellness add-on, and a high enough annual limit to cover at least one major surgery or cancer case.

What Pricing Tells You About Real Risk

Look at average premiums, and you’ll see: Accident-only is cheap because it is narrower. Accident & illness is more expensive because chronic diseases, cancer, and specialty care can cost thousands over the years. NAPHIA’s 2024 U.S. averages show accident-only premiums far below accident & illness premiums for both dogs and cats.

Insurers price for reality: Over a pet’s life, illness can be far more expensive than a single broken leg. If you’re most worried about cancer, kidney disease, or diabetes, an accident-only policy won’t help you.

Waiting Periods and Orthopedic Rules

Waiting periods are where “I thought it was covered” turns into “they denied everything.”

Typical pattern:

Accidents: short wait, sometimes same-day or a few days, depending on insurer and state.

Illnesses: longer wait, often around 14 days but sometimes longer.

Orthopedic issues: sometimes 6–12 months or a special cruciate/ligament wait, especially for knees and hips.

Some companies offer an orthopedic exam/waiver path to shorten that—but only if you follow their process exactly and your pet passes. For large breeds or active dogs, enrolling early and understanding these rules is huge.

The Most Common “I Didn’t Know” Moments

From a pattern perspective, pet parents are most often surprised by: Conditions labeled pre-existing because of old notes, Dental coverage not being provided as expected, Exam fees not being reimbursed, and Bilateral exclusions excluding both knees or both hips.

If you focus your questions on those four areas, you’ll be ahead of most people buying pet insurance.

Scenario Snapshots – How Coverage Plays Out in Real Life

Scenario 1: Puppy Swallows a Toy

The Situation: An 8-month-old Lab mix swallows a rubber toy. This requires ER visits, imaging, surgery, and two nights in the hospital.

- Example Total Bill: $4,000. Actual intestinal blockage surgery can range from roughly $2,000 to more than $10,000 depending on complexity, emergency/specialty setting, and location.

- With Insurance: (Assuming $250 deductible, 80% reimbursement, $10k annual limit, and all charges are eligible). $4,000 - $250 = $3,750. Insurer pays 80% of $3,750 = $3,000. You pay $1,000.

- Without Insurance: You pay $4,000.

Verdict: Same emergency. Very different financial impact.

Scenario 2: Cat Develops Diabetes

The Situation: A 7-year-old indoor cat is diagnosed with diabetes. Initial workup and regulation can cost a few hundred dollars or climb into the thousands if hospitalization, diabetic ketoacidosis, or other complications are involved. Ongoing care usually includes insulin, syringes, glucose monitoring, vet visits, lab work, and sometimes prescription food.

- Accident & Illness Plan (Enrolled Young): ($250 deductible, 80% reimbursement, all charges eligible). Year one example: $2,000 costs → you pay ~$600 total. Future year example: $1,200 costs → you pay ~$240 per year after the deductible has already been met for that policy year; if it has not, you pay the deductible first.

- Accident-Only Plan: Diabetes is an illness, so it is not covered.

- Enrolled After Symptoms: Treated as pre-existing, so it is often not covered.

Verdict: Same disease. Timing and plan type decide everything.

Key Takeaways – What Pet Insurance Covers (and Doesn’t)

What Pet Insurance Generally Covers

Most accident & illness plans cover: Accidents (injuries, swallowed objects, toxins), Illnesses (from simple infections to major chronic diseases and cancer), and Diagnostics and treatments (tests, surgery, hospital care, meds, follow-up).

In plain language: When something unexpected and medical happens, this is where pet insurance is meant to show up, subject to exclusions, waiting periods, deductibles, reimbursement rates, and limits.

What Pet Insurance Generally Doesn’t Cover

Most plans don’t cover: Pre-existing conditions, Routine wellness care (unless you add wellness), Breeding/pregnancy/elective procedures unless specifically added, Lifestyle services like grooming/daycare/training, Routine dental cleanings and some dental diseases, Experimental or non-standard treatments, and Some prescription diets, supplements, and end-of-life costs.

How to Use This When You Shop

When you’re comparing plans, ask:

- Exactly what does pet insurance cover in this plan?

- How do you define and handle pre-existing conditions?

- Do you have bilateral or orthopedic exclusions?

- Are exam fees and dental illness covered?

- What are my deductible, reimbursement rate, and annual limit—and what does that look like on a $3,000 bill?

If the answers feel fuzzy, keep asking—or pick a different company.

Final Thought

Pet insurance won’t make vet care free. But the right policy can make sure that when your dog or cat really needs help, money isn’t the main reason you say “no.”

Understand what pet insurance covers, respect what it doesn’t, and choose a plan that matches your pet’s real risks and your budget—not just the cheapest number on a comparison table.

Frequently Asked Questions (FAQs)

What does pet insurance typically cover?

Most accident & illness plans cover sudden accidents (broken bones, swallowed objects), new illnesses (infections, cancer, diabetes), and the diagnostics and treatments required for them, as long as the condition is eligible and not pre-existing.

Does pet insurance cover routine care?

Standard accident & illness policies usually do not cover wellness exams, vaccines, or flea prevention unless you purchase a specific wellness or preventive-care add-on.

What is a pre-existing condition?

A pre-existing condition is generally anything with prior advice, treatment, or signs and symptoms before your policy started or during the waiting period—even if no formal diagnosis was made yet.

Does pet insurance cover dental?

It depends on the plan. Routine cleanings are usually wellness or preventive care. Dental accidents and some dental diseases may be covered, but coverage can vary based on the policy, dental requirements, waiting periods, and limits.

What are bilateral exclusions?

This rule states that if a condition (like a knee injury) existed on one side of the body before coverage, the insurer may exclude coverage for the same condition on the other side.

WhiskerCover is reader-supported. When you click on links to pet insurance partners on our site and purchase a policy, we may earn a commission at no extra cost to you. Learn more about how we make money.

Sources

- NAIC Pet Insurance Overview

- NAIC Pet Insurance Model Act

- NAIC Regulator’s Guide to Pet Insurance

- NAPHIA Industry Data

- NAPHIA About This Data

- NAPHIA Average Premiums

- ASPCA Pet Health Insurance Coverage

- ASPCA Pet Health Insurance Pre-Existing Conditions

- Pets Best Coverage

- Pets Best FAQ

- Embrace Pre-Existing Conditions

- Embrace Waiting Periods

- Embrace Coverage

- AKC Pet Insurance Pre-Existing Conditions

- AKC Pet Insurance Coverage FAQ

- CareCredit Emergency Vet Cost Guide

- PetMD Dog Intestinal Blockage Surgery

- PetMD Diabetes in Cats

- Spot Cost of Cat Diabetes

- PetMD Chemotherapy for Dogs

- PetMD Radiation Therapy for Dogs

You may be interested...

More published guides that build on this topic.