Your cat is family—not just a pet or a budget line. But when a $2,000 emergency veterinary bill lands in front of you, your priority is saving them, not worrying about expenses. That’s the moment coverage becomes very real.

In simple terms, pet insurance for cats is a way to make sure money isn’t the reason you say no to treatment. You pay a predictable monthly fee, the insurer helps cover big, unexpected vet bills, and you get to focus on your cat instead of your credit card limit.

In this guide, we’ll break down how the policy works, what it really covers, what it doesn’t, and how cat premiums compare to the average cost of pet insurance in the U.S. right now. We’ll also talk about finding affordable coverage that still actually helps when things go wrong.

Table of Contents

- Why Cat Insurance Matters More Than Ever

- What Is Pet Insurance for Cats, in Plain English

- How Cat Insurance Actually Works (Step-by-Step)

- What Cat Insurance Covers (With Real-World Scenarios)

- What Cat Insurance Doesn’t Cover (The Fine Print to Check)

- Cat Insurance Cost: What You’ll Actually Pay Each Month

- Is Cat Insurance Worth It? An Honest Look

- How to Choose the Best Cat Insurance Policy

- How We Choose the Best Cat Insurance Providers

- Expert Insights: What the Data (and Vets) Say

- Real-World Stories: When Cat Insurance Changed Everything

- How to Get Started in the Next 15 Minutes

- Frequently Asked Questions (FAQs)

Why Cat Insurance Matters More Than Ever

The New Reality of Vet Bills

Vet bills are not what they used to be. A "quick checkup" can turn into bloodwork, imaging, and maybe an overnight stay. An emergency visit for a blocked urinary tract or poisoning can jump from a few hundred dollars to a few thousand fast.

That is the new reality of rising vet costs for cats: modern medicine is powerful, but it is not cheap. Gallup and PetSmart Charities found that 52% of U.S. pet owners skipped or declined veterinary care in the past year, and cost was the leading barrier among those who skipped or declined care.

When the number on the estimate gets big enough, a horrible phrase shows up in the exam room: "economic euthanasia." In plain English, it means the treatment exists, but the money does not. A policy does not fix every access-to-care problem, but it can reduce the chance that cost is the first reason you say "no."

Millennial Pet Parents and the Money Gap

Millennial and Gen Z pet parents feel this especially hard. Your cat is not lawn decor; they are your roommate, your emotional support, your "kid." You are already juggling rent, student loans, and a shaky emergency fund. Federal Reserve data shows that 63% of U.S. adults could cover a $400 emergency expense using cash or its equivalent in 2025, which means a meaningful minority could not.

So when you ask, "Is cat insurance necessary?" what you are really asking is: "If something big happens, could I actually afford to do what my heart wants?" For many people, the honest answer is "not without help."

Why Cats Get Overlooked (But Shouldn’t)

Cats quietly slip through the cracks. We insure dogs more often, even though cats develop their own expensive issues: urinary blockages, kidney disease, asthma, cancer, and dental disease. Cornell Feline Health Center notes that kidney failure, hyperthyroidism, diabetes, inflammatory bowel disease, cancer, arthritis, and dental disease all become more common concerns as cats age. Indoor-only does not mean "invincible." It just means the risks look different.

That is why coverage is important right now. It is not about being paranoid. It is about admitting that modern vet care is powerful, pricey, and worth planning for before you are standing in a clinic, staring at an estimate, trying to do math through tears.

What Is Pet Insurance for Cats, in Plain English

Simple Definition

Pet insurance for cats works like health insurance for your cat’s vet bills, but with an important legal difference: the NAIC describes pet insurance as coverage with exclusions, deductibles, payment limits, and reimbursement methods, and notes that it is generally regulated as property/casualty insurance. You pay a monthly premium. When your cat gets sick or injured, the insurer reimburses part of the eligible vet bill for covered problems.

Key Terms Without the Jargon

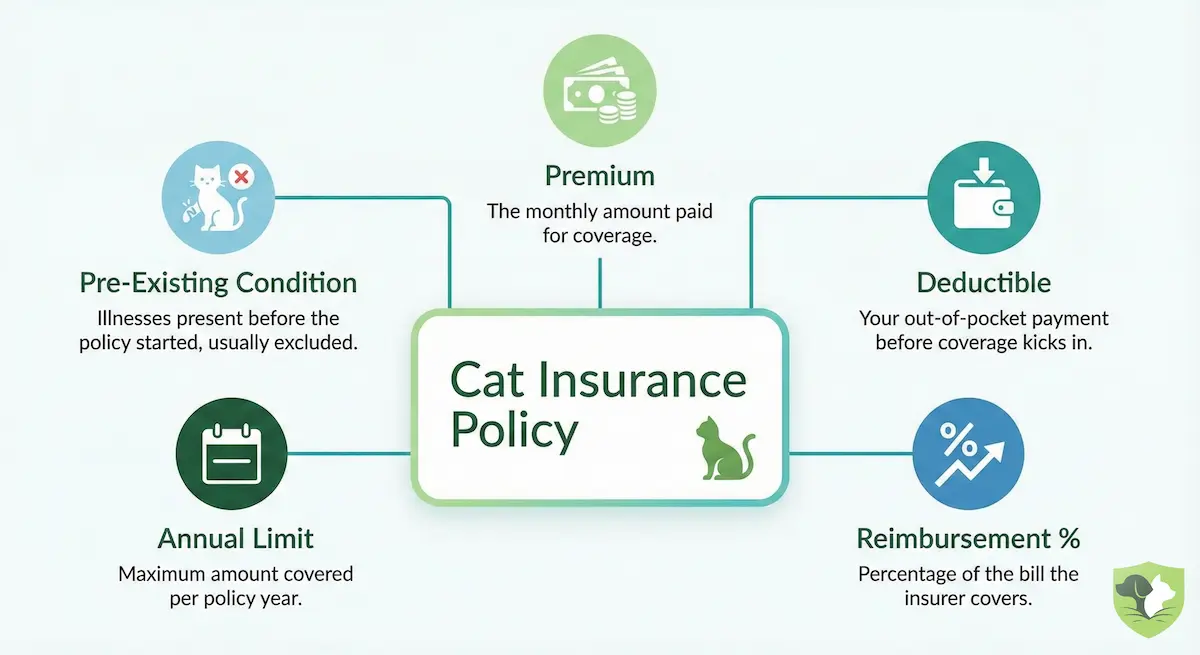

- Premium: What you pay every month or year to keep coverage active.

- Deductible: The amount you pay out of pocket before insurance starts reimbursing (for example, the first $250 each year).

- Reimbursement Rate: The percentage the insurer covers after the deductible (often 70%, 80%, or 90%).

- Annual Limit: The maximum they will pay in a year (for example, $5,000, $10,000, or unlimited).

- Pre-Existing Condition: Under the NAIC Pet Insurance Model Act, this can include a condition where a veterinarian provided advice, the pet received treatment, or verifiable signs or symptoms existed before the policy effective date or during a waiting period.

Insurance vs Emergency Savings

Could you just save money instead? Maybe. But a major cat emergency can land in the thousands, and Gallup found that about two-thirds of pet owners said they could pay $1,000 or less for lifesaving treatment. Think of a policy as backup: you keep some savings, and the insurer steps in when a covered problem gets really expensive.

How Cat Insurance Actually Works (Step-by-Step)

Step 1 – You Pick a Plan and Customize It

You choose the basics: accident-and-illness or accident-only, your deductible, reimbursement rate, and annual limit. The NAIC groups pet insurance products into accident-only, accident-and-illness, and wellness coverages. Lower deductibles and higher reimbursement rates usually mean a higher monthly premium, but less pain when a big covered bill hits.

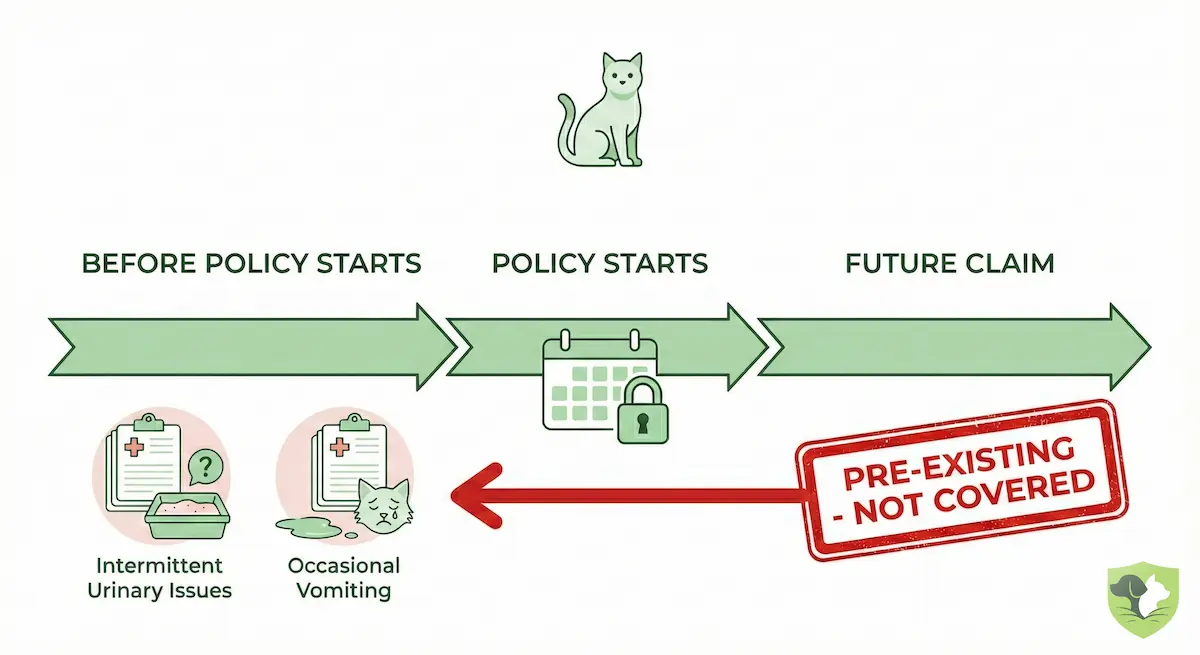

Step 2 – Waiting Periods and Pre-Existing Conditions

After you enroll, there is usually a window where some problems are not covered yet. Anything your cat showed signs of, received treatment for, or had vet advice about before the policy or during the waiting period may become a pre-existing condition. The NAIC Model Act sets standardized definitions and, where adopted, limits some waiting periods; actual rules still depend on state law and the policy.

Step 3 – Visit a Licensed Vet

Many plans let you use any licensed vet, ER clinic, or specialist, but always check the policy. The NAIC’s Regulator’s Guide says most pet insurance plans use a reimbursement model, meaning you usually pay the veterinarian first and then get reimbursed by the insurer.

Step 4 – You Pay the Vet, Then File a Claim

You pay the invoice at the clinic, then submit an itemized bill and, sometimes, medical records through the insurer’s app or portal. Direct-pay options exist at some insurers and participating clinics, but reimbursement is still the default model in most policies.

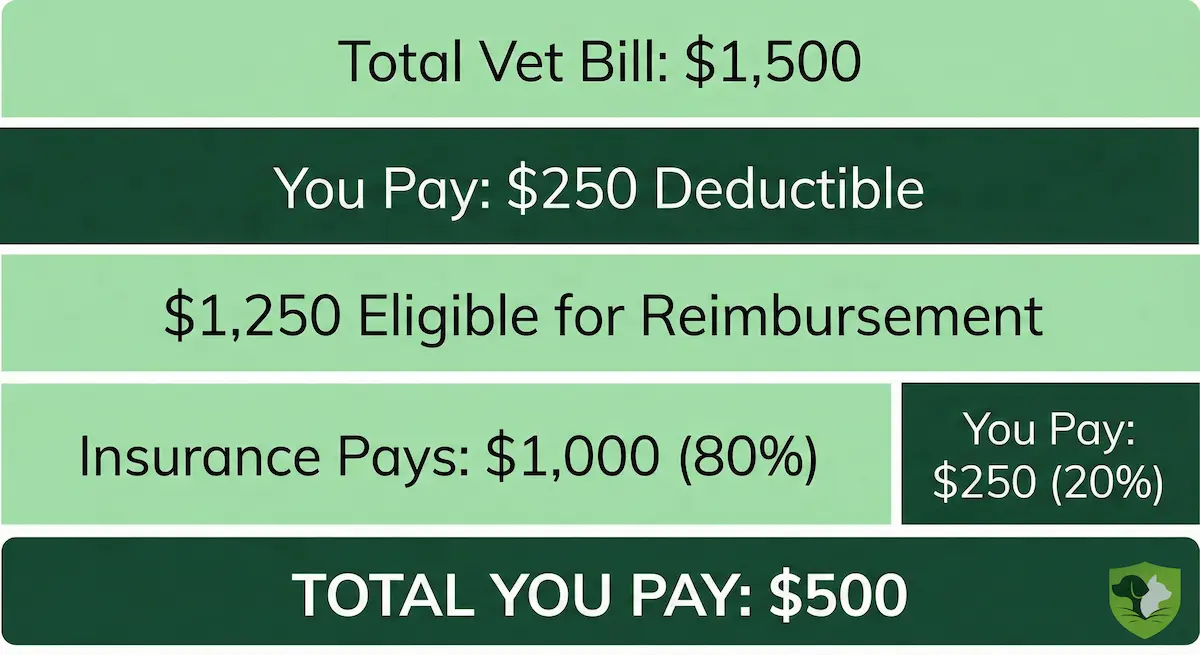

Step 5 – Reimbursement Example

$1,500 bill, $250 deductible, 80% reimbursement:

- You pay the first $250 deductible, then 20% of the remaining $1,250.

- Insurance pays $1,000. You pay $500 total.

This example assumes the whole bill is eligible, the annual limit is not exhausted, and the policy does not apply a benefit schedule or usual-and-customary fee cap.

How Cat Insurance Differs from Your Own Health Insurance

Most policies do not work like an HMO or PPO. You usually pay the vet first and file for reimbursement. In that sense, it feels closer to car insurance than human health insurance, even though NAIC notes that pet insurance has some health-insurance-like features, including waiting periods, age limits, exclusions, deductibles, and coinsurance.

What Cat Insurance Covers (With Real-World Scenarios)

Accident & Illness Policies (The Default Choice)

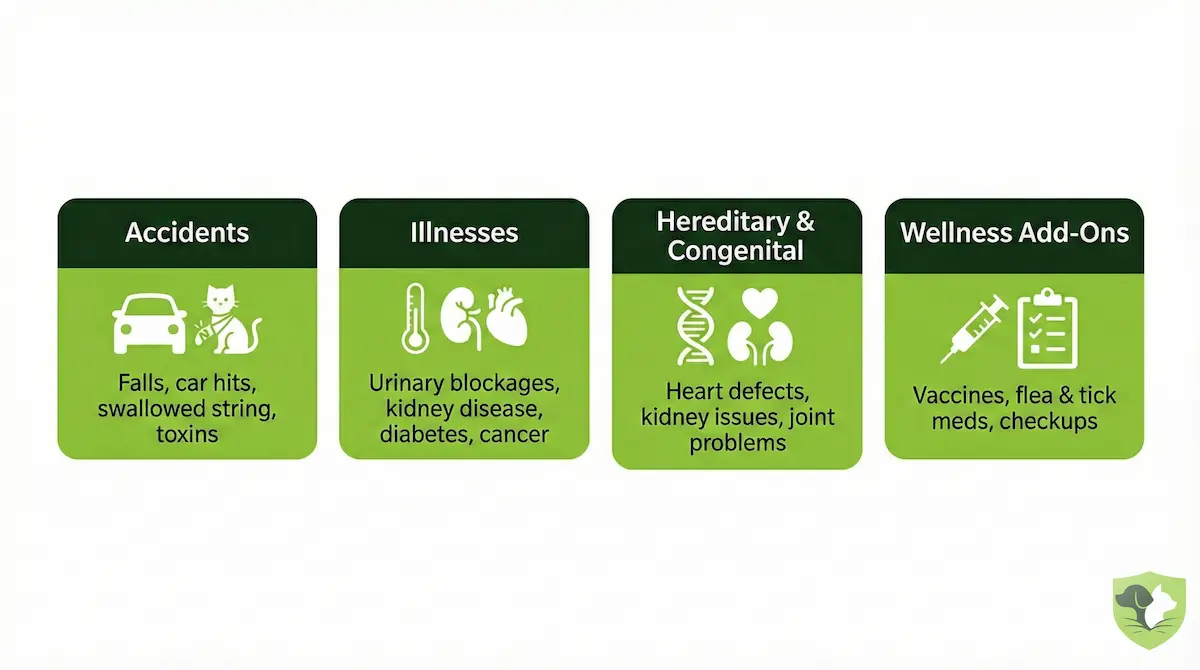

Most comprehensive plans are "accident and illness." This is the core of pet insurance for cats. They typically cover:

- Accidents: car hits, falls, broken bones, swallowed string or hair bands, toxic plants like lilies, and household poisonings.

- Illnesses: urinary blockages, bladder stones, kidney disease, diabetes, asthma, chronic vomiting or diarrhea, hyperthyroidism, and cancers like lymphoma.

Depending on the policy, eligible care may include exams, bloodwork, X-rays, ultrasound, hospital stays, surgery, medications, and referrals to specialists. The policy matters: NAIC notes that pet insurance coverage levels, exclusions, deductibles, and payment limits vary by company.

Hereditary and Congenital Conditions

Many accident-and-illness policies cover genetic and birth-related disorders if there were no signs before you enrolled. PetMD notes that many companies cover congenital and hereditary conditions when no signs or diagnosis existed before coverage starts, but some policies exclude them or require special riders. Think of hypertrophic cardiomyopathy in certain breeds, polycystic kidney disease, or certain vision and joint problems. Always check this section carefully; it is where surprise exclusions can hide.

Accident-Only Policies (When "Cheap" Isn’t Always Better)

An accident-only plan is the budget version. It can help if your cat is hit by a car, breaks a leg, or eats something dangerous. But it will not cover illnesses at all: no help with kidney disease, urinary crises, diabetes, asthma, or cancer. It is better than nothing, but it leaves out many of the expensive problems cats develop as they age.

Optional Wellness Add-Ons

Wellness add-ons are separate from core accident-and-illness coverage. The NAIC Model Act defines a wellness program as a subscription or reimbursement-based program separate from insurance unless state insurance law treats the benefit as insurance. These add-ons can help budget for routine care such as exams, vaccines, flea and tick medication, and sometimes spay/neuter or dental cleaning. They do not replace real medical coverage for emergencies and serious diseases.

What Cat Insurance Doesn’t Cover (The Fine Print to Check)

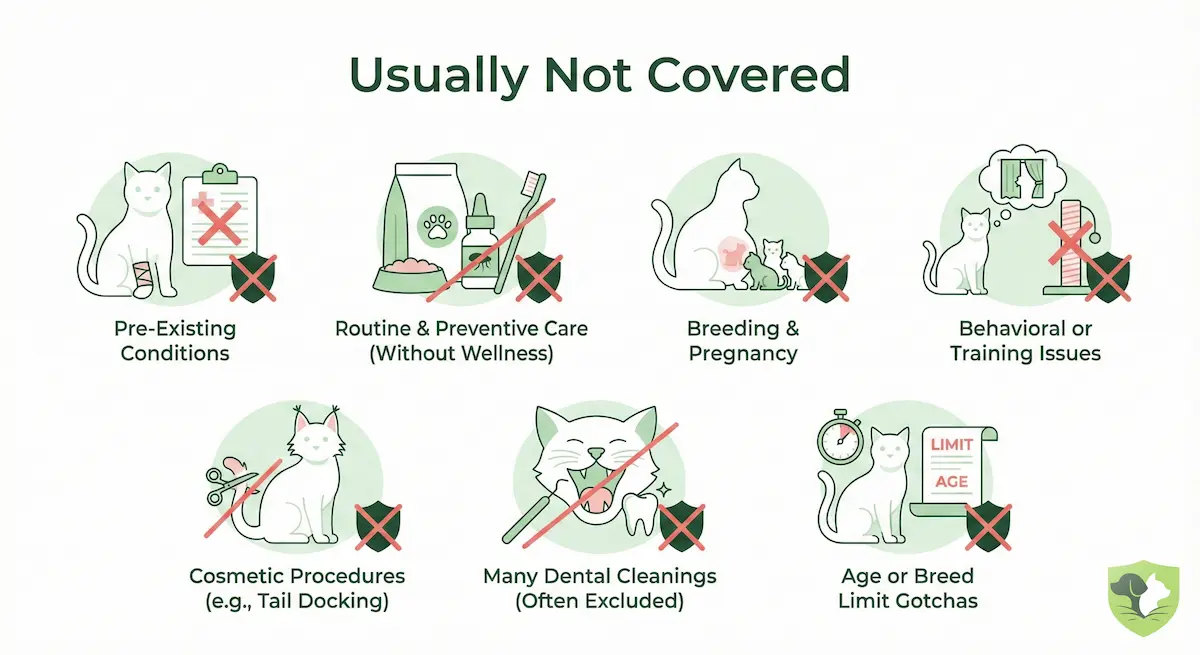

Pre-Existing Conditions

This is the big one in policy exclusions. Under the NAIC Model Act, a pre-existing condition can be tied to prior veterinary advice, previous treatment, or verifiable signs or symptoms directly related to the claim. Chronic issues like kidney disease, diabetes, or recurring urinary problems are usually excluded once they are labeled pre-existing. Some insurers may cover curable issues again, such as a one-off respiratory infection, after a symptom-free and treatment-free period, but that depends on the policy. Moral of the story: do not wait until your cat is already sick to think about insurance.

Routine and Preventive Care

If you are wondering what coverage does not include, start with routine care. The NAIC Regulator’s Guide lists common exclusions such as preventive treatment, wellness care, vaccinations, flea prevention, spaying or castration, and dental care. These services can sometimes be added through a wellness plan, but they are separate from core accident-and-illness coverage.

Dental, Behavioral, and "Grey Area" Exclusions

Dental is tricky. Cornell Feline Health Center says 50% to 90% of cats older than four have some form of dental disease, but many insurance plans only cover dental injury or certain dental illnesses, not routine cleanings or mild tartar. Behavioral issues, training, and anxiety medication can be excluded or tightly limited. Alternative care, such as acupuncture, hydrotherapy, or laser therapy, may require special add-ons.

Age Limits and Breed-Specific Gotchas

Some insurers will not newly enroll older cats, and many charge higher rates as cats age. Certain purebreds can have special terms or higher premiums because of known genetic risks. NAIC warns consumers that pet insurance prices may increase substantially as the animal gets older. Always read the exclusions and rating-factor disclosures slowly; that is where future arguments live.

Cat Insurance Cost: What You’ll Actually Pay Each Month

Average Cat Insurance Cost in the U.S.

So, how much is cat insurance really? The best current benchmark is NAPHIA’s 2025 State of the Industry data: the average U.S. accident-and-illness premium for cats was $386.47 per year, or $32.21 per month, in 2024. NAPHIA’s report highlights put the average accident-only cat premium at $110.03 per year, or about $9.17 per month. Wellness add-ons sit on top of that.

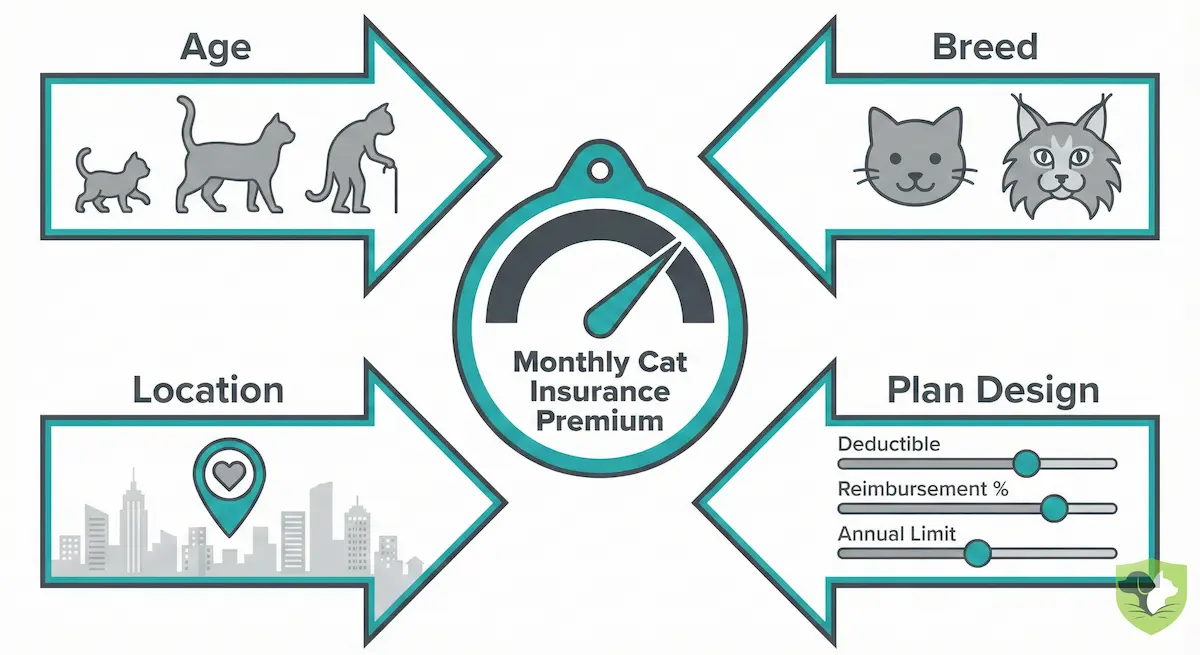

What Drives Your Premium Up or Down

Your monthly premium is not random. It is driven by:

- Age: kittens are cheaper; prices often rise as your cat gets older.

- Breed: purebreds with known issues may cost more than mixed-breed or domestic shorthair cats.

- Location: big, pricey cities can mean higher vet bills and higher premiums.

- Plan design: lower deductible, higher reimbursement percentage, and higher annual limits all raise your monthly price.

The NAIC Model Act requires disclosure if a pet insurer reduces coverage or increases premiums based on claim history, pet age, or geographic location, where the model has been adopted into state law.

Example Quote Scenarios

Very rough idea of the monthly price:

- 2-year-old indoor domestic shorthair, mid-cost city:

- $500 deductible, 70% reimbursement, $5k limit -> on the lower end.

- $250 deductible, 80% reimbursement, $10k limit -> closer to the market average or above it.

- 9-year-old purebred in a high-cost city: Expect noticeably higher premiums for the same coverage.

How Premiums Change Over Time

Premiums usually rise over the years. Your cat ages, vet care gets more expensive, and insurers adjust prices. You can hunt for a cheaper policy by raising your deductible or lowering your reimbursement percentage, but do not gut the coverage. The goal is not the cheapest policy on paper. It is a price you can keep paying that still actually helps when things go really wrong.

Is Cat Insurance Worth It? An Honest Look

The Upsides (Why Many Owners Swear by It)

So, is cat insurance worth it? For many people, yes. It can turn a potential $2,000-$5,000 crisis into a more manageable hit. MetLife’s emergency vet cost guide lists common cat emergency services such as hospitalization, wound treatment, emergency surgery, and oxygen therapy in ranges that can reach thousands of dollars. Coverage gives you a way to say "do the scan, run the tests" without panicking over every line on the estimate.

The Downsides (What People Complain About)

The flip side: you might pay premiums for years and rarely claim. You still usually have to pay the vet first and wait for reimbursement. Exclusions and pre-existing conditions can sting. That is where the "is pet insurance worth it for cats or a waste of money?" frustration usually comes from.

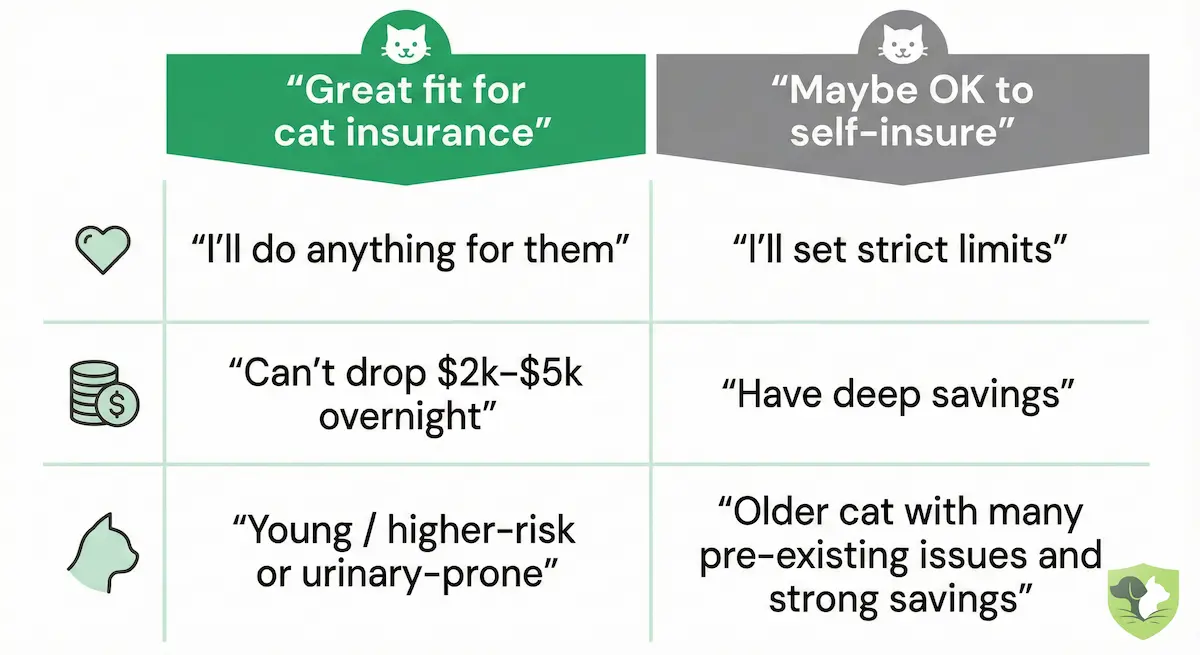

When Cat Insurance Makes the Most Sense

- It is most powerful when your cat is young, healthy, and has years of future risk ahead.

- It is also a strong fit if you are emotionally "I’ll do anything for them," but financially cannot drop several thousand dollars overnight.

- Purebreds or breeds prone to kidney, heart, or urinary issues are prime candidates, especially when hereditary coverage is included.

When Self-Insuring Might Be Reasonable

If you have deep savings and a high risk tolerance, self-insuring can work. Just be honest: will you really keep a few thousand dollars untouched, waiting for your cat’s worst day?

How to Choose the Best Cat Insurance Policy

Step 1 – Decide Your Monthly Budget and Risk Level

Before you compare brands, pick a number. How much can you spend each month without stress? Then ask: if my cat needed a $3,000 surgery tomorrow, how much could I actually afford?

Step 2 – List Your Must-Have Coverage

"Best" means "best for your cat." Do you need chronic illness covered for life? Hereditary issues? Emergency and specialty care? Write your must-haves down.

Step 3 – Compare Plan Structures

Look at deductible, reimbursement percentage, and annual limit side by side. Higher coverage and lower deductibles usually mean higher monthly cost, but less pain at claim time. Avoid rock-bottom limits that will not touch a real emergency.

Step 4 – Check the Company’s Reputation

Read reviews about claim speed, denial patterns, and premium hikes. The best pet insurance for cats pays fairly and clearly, not just cheaply.

Step 5 – Use a Short Checklist Before You Enroll

Before you click "buy," confirm:

- Accident and illness covered?

- Hereditary and chronic issues covered, or excluded?

- Sick exam fees included, excluded, or add-on?

- Is the annual limit high enough for a real emergency?

- Deductible realistic?

If you can say "yes" with a calm gut, you have likely found your best policy match.

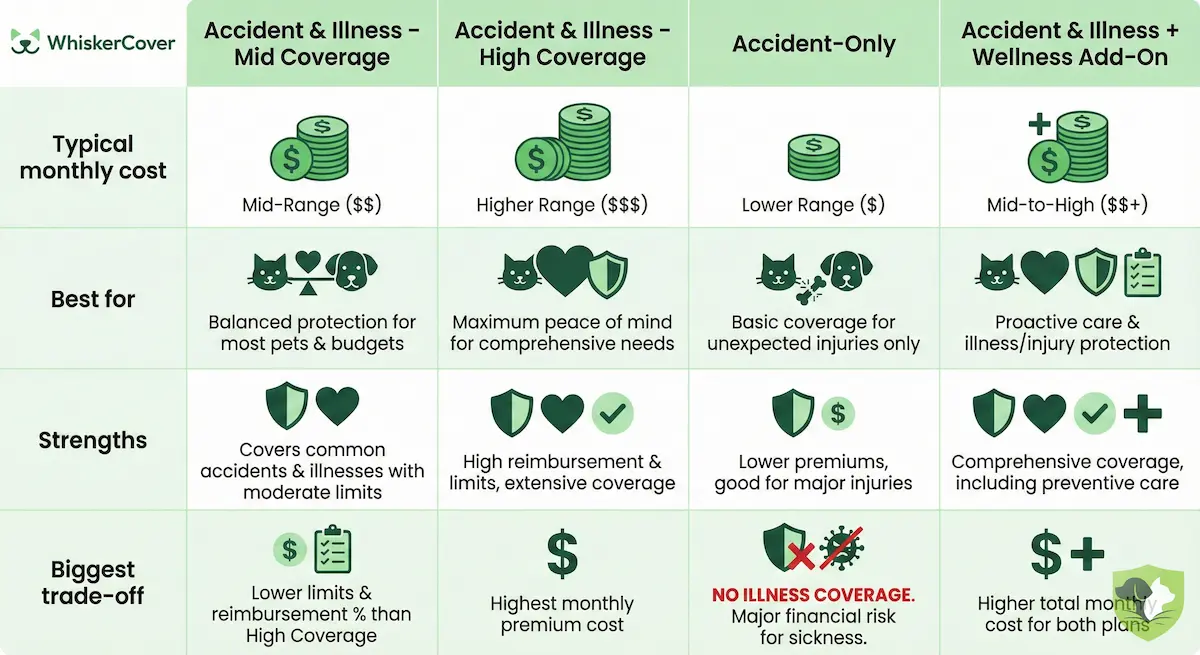

Comparing Cat Insurance Options at a Glance

Here is a simple way to think about different coverage setups. Costs are rough, but the trade-offs are real:

| Plan Type | Est. Cost* | Best For | Pros & Cons |

|---|---|---|---|

| Accident & Illness (Mid) | $25-$35 | Most cat parents | Strong overall protection. Good value, though not the cheapest option. |

| Accident & Illness (High) | $40-$60+ | Worriers / high-risk breeds | Higher limits and lower out-of-pocket costs, but a higher monthly bill. |

| Accident-Only | $9-$20 | Very tight budgets | Low premium, covers major trauma. No illness cover for kidney disease, cancer, urinary issues, or diabetes. |

| A&I + Wellness Add-on | $40-$70+ | Predictable costs | Helps with routine care plus big unexpected bills. Can be overkill if you skip checkups or do not use the capped benefits. |

*For a young adult cat in a typical U.S. city. NAPHIA’s 2024 U.S. average for accident-and-illness cat coverage was $32.21/month.

How We Choose the Best Cat Insurance Providers

When we talk about the best policy, we’re not chasing the lowest price. We look at:

- Depth of accident-and-illness coverage (including hereditary issues)

- Annual limits and how they handle chronic conditions over time

- Exclusions and waiting periods in the fine print

- Claim speed, approval rates, and customer reviews

- Long-term price behavior, not teaser rates

The "best" pet insurance for cats is the one that still pays out fairly when your cat has a bad year, not just the one that looks cheap on a quote screen.

Expert Insights: What the Data (and Vets) Say

The Adoption Gap – Most Cats Are Still Uninsured

For all the talk about coverage, very few cats actually have it. The latest NAPHIA data shows that U.S. pet insurance penetration reached 5.46% for dogs and 2.04% for cats at year-end 2024. Among insured U.S. pets, dogs represented 75.6% and cats 23.5%.

The gap is still huge, but cats are catching up faster in percentage terms: NAPHIA reported U.S. insured cats grew 23.5% year over year in 2024, compared with 9.8% growth for insured dogs.

The Reality of Emergency Care

Insurer claim data shows the average emergency vet bill for a cat is about $900: Pumpkin reports an average emergency care cost of $919 for cats based on claims filed between February 2022 and February 2025. Just the basics of an ER visit can add up fast: MetLife lists cat hospitalization for 3-5 days at $1,500-$3,000 and emergency surgery at $1,500-$3,000.

On top of emergencies, common lifetime problems quietly add to costs. Cornell reports that 50% to 90% of cats older than four have some form of dental disease. Cornell also estimates feline asthma affects about 1% of domestic cats in the U.S., and severe asthma attacks can become emergencies.

The $1,500 Decision Point

Here is the uncomfortable part: many households are not built for a four-figure vet bill. Federal Reserve data shows 63% of adults could cover a $400 emergency with cash or its equivalent in 2025. For pet-specific care, Gallup found that 66% of pet owners said they could pay $1,000 or less for lifesaving treatment. When a cat’s estimate crosses $1,500-$2,000, many owners start hesitating or delaying care because the math breaks. This is the line a policy is designed to move.

How Vets See Cat Insurance

Industry research should be read with that bias in mind, but it consistently points in the same direction: insured pets may come in sooner and receive a fuller range of care because cost is not blocking every decision. NAPHIA tells veterinary teams that insured patients are more likely to come in sooner and receive the full range of care they need. Telehealth tools can help with triage, but they do not pay the invoice; the policy does.

Real-World Stories: When Cat Insurance Changed Everything

The examples below are composites based on common insurance scenarios for cats, not individual verified customer case studies.

The $10,000 Hospital Stay That Didn’t Break a Family

Luna stopped eating and hid under the bed. By the time her owner rushed her in, she needed intensive care, a feeding tube, and several days in the hospital. The bill crossed $10,000 fast. If Luna had an eligible policy with 80% reimbursement, her family would still feel the hit, but they would not have to choose between total self-pay and another goodbye.

"I Wish I’d Gotten It Earlier" – The Pre-Existing Condition Trap

Milo had his first urinary blockage at three. His owner paid out of pocket, then finally shopped for coverage. Plans could flag urinary issues as pre-existing because the symptoms and treatment happened before coverage started. Future related blockages might be excluded under a new policy. The regret is brutal: one big bill before insurance can mean no coverage for the same expensive problem later.

Catching Problems Early Because "It’s Covered"

Tuna started peeing outside the box once. With no policy, many people would "wait and see." Her owner did not hesitate. A full workup found early crystals and inflammation. With treatment, Tuna avoided a rush-to-ER blockage and a possible surgery. That is one of those quiet insurance claim examples you rarely see in ads, but it is where the value can hide.

How to Get Started in the Next 15 Minutes

A Simple Action Plan

Here is how to get covered without overthinking it:

- Pick a budget. Decide what you can spend each month without stress. NAPHIA’s latest U.S. average for accident-and-illness cat coverage is about $32/month, but your quote can be lower or higher.

- Write down the basics. Your cat’s age, breed, health history, and whether they are indoor-only or go outside.

- Get 3-4 quotes. Visit a few insurer sites or comparison tools. Use the same settings (deductible, reimbursement percentage, annual limit) so you can compare apples to apples.

- Check the fine print. Look specifically at pre-existing conditions, dental, hereditary conditions, sick exam fees, age limits, and whether premiums can change based on age or location.

- Choose the plan that feels realistic long-term. A slightly higher deductible you can afford every year beats "perfect" coverage you will cancel in 12 months.

Final Reassurance

There is no single "perfect" policy or "best" setup for everyone. There is just the option that lets you sleep at night. Whether you buy a policy today or start a dedicated "cat emergency" savings fund, the goal is the same: never having to choose between your bank account and your cat’s life when it really counts.

Frequently Asked Questions (FAQs)

Is cat insurance worth it for an indoor-only cat?

Usually, yes. Indoor cats skip many outdoor trauma risks, but not urinary blockages, diabetes, cancer, kidney disease, asthma, or dental disease.

When should I get cat insurance?

The earlier the better. The best time is when your cat is young and healthy, before symptoms or vet notes become pre-existing-condition issues.

Can I get cat insurance for an older cat?

Often yes, but with higher premiums and more exclusions. Some insurers cap new enrollments at a certain age, while others advertise no upper enrollment age, so check this first.

Does cat insurance cover dental?

Sometimes. Many plans cover dental injury and some dental illness, but routine cleanings, mild tartar, and pre-existing dental disease are often excluded or limited.

Will cat insurance cover pre-existing conditions?

Usually no. Most policies exclude conditions tied to symptoms, treatment, or vet advice before coverage starts or during waiting periods. Some insurers make exceptions for curable conditions after a symptom-free and treatment-free period, but the rule is policy-specific.

How long does reimbursement usually take, and what documentation is typically required?

Many straightforward pet insurance claims are processed in roughly 5-15 business days, but timing varies by insurer and the first claim can take longer because medical records are reviewed. You will usually need an itemized vet invoice and may need medical notes or full records.

Is there such a thing as cheap cat insurance that’s still good?

Yes, if you tweak the levers carefully. Choose a higher deductible and a realistic reimbursement rate, but keep accident-and-illness coverage and a decent annual limit if you want protection against illness as well as trauma.

What about multi-cat households?

Most insurers rate each cat separately, and many offer a small multi-pet discount. Some insurers also offer family or shared-limit structures. You can mix coverage levels as long as each cat’s age, breed, and health history are accurate.

Can I switch policies or providers if my needs change, and what happens to coverage for existing conditions?

You can switch providers or tweak your coverage, but diagnosed conditions or prior symptoms can become pre-existing conditions under a new policy. That means the new insurer may not cover those problems, so weigh savings against losing coverage for ongoing or chronic issues.

WhiskerCover is reader-supported. When you click on links to pet insurance partners on our site and purchase a policy, we may earn a commission at no extra cost to you. Learn more about how we make money.

Sources

- NAIC Pet Insurance Overview

- NAIC Pet Insurance Model Act

- NAIC Regulator’s Guide to Pet Insurance

- NAPHIA 2025 State of the Industry Report

- NAPHIA Total Pets Insured

- NAPHIA 2025 Report Highlights PDF

- NAPHIA Veterinary Resources

- Gallup / PetSmart Charities State of Pet Care Study

- Federal Reserve $400 Emergency Expense Data

- Pumpkin Emergency Vet Cost Data

- MetLife Emergency Vet Cost Guide

- Cornell Feline Health Center: Senior Cat Health

- Cornell Feline Health Center: Feline Dental Disease

- Cornell Feline Health Center: Feline Asthma

- PetMD Urinary Blockage in Cats

- PetMD Pre-Existing Conditions Guide

- Embrace Pet Insurance Claims

- MetLife Pet Insurance Claims