If you've visited a veterinary clinic recently, you've likely noticed the sticker shock. Veterinary medicine has advanced rapidly, and referral-level diagnostics are no longer rare edge cases. PetMD says a dog MRI typically ranges from $2,300 to $5,000 or more, and dog TPLO knee surgery can reach $10,000, depending on hospital, region, and case complexity. That is why pet insurance has moved from a niche product to a serious budget question for many families.

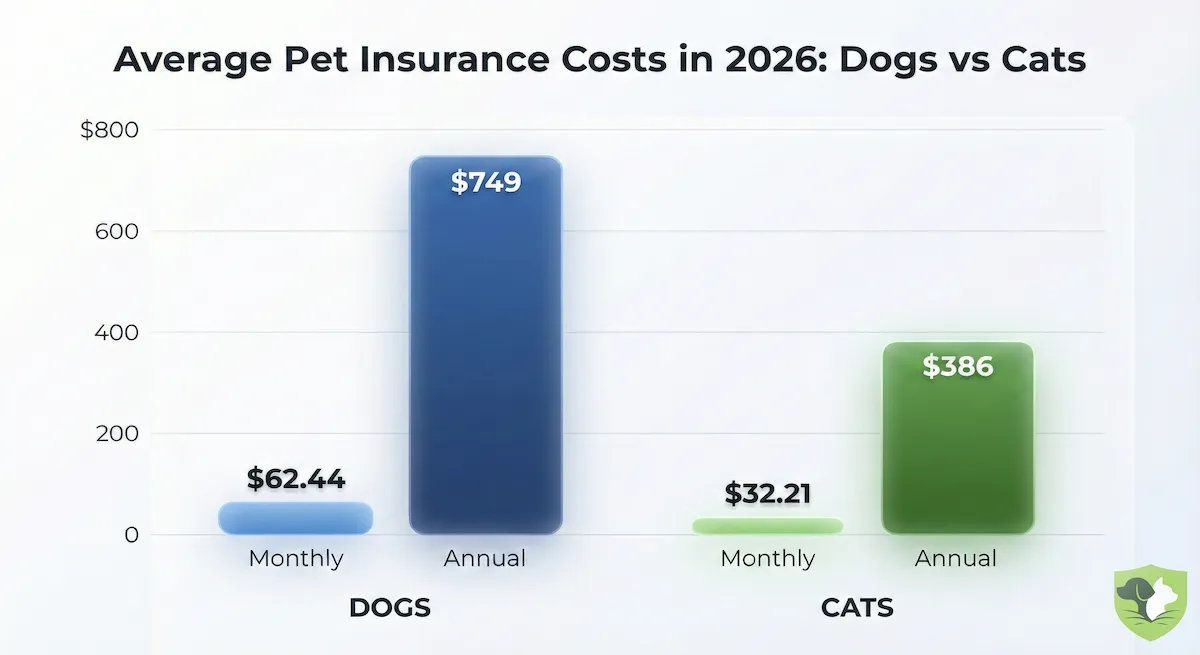

So, what's the damage? For accident-and-illness coverage, the average cost of pet insurance is about $62.44/month for dogs and $32.21/month for cats. The best current public benchmark is the North American Pet Health Insurance Association (NAPHIA) 2025 State of the Industry data, which uses 2024 U.S. policies. NAPHIA reported average accident-and-illness premiums of $749.29 per year for dogs and $386.47 per year for cats.

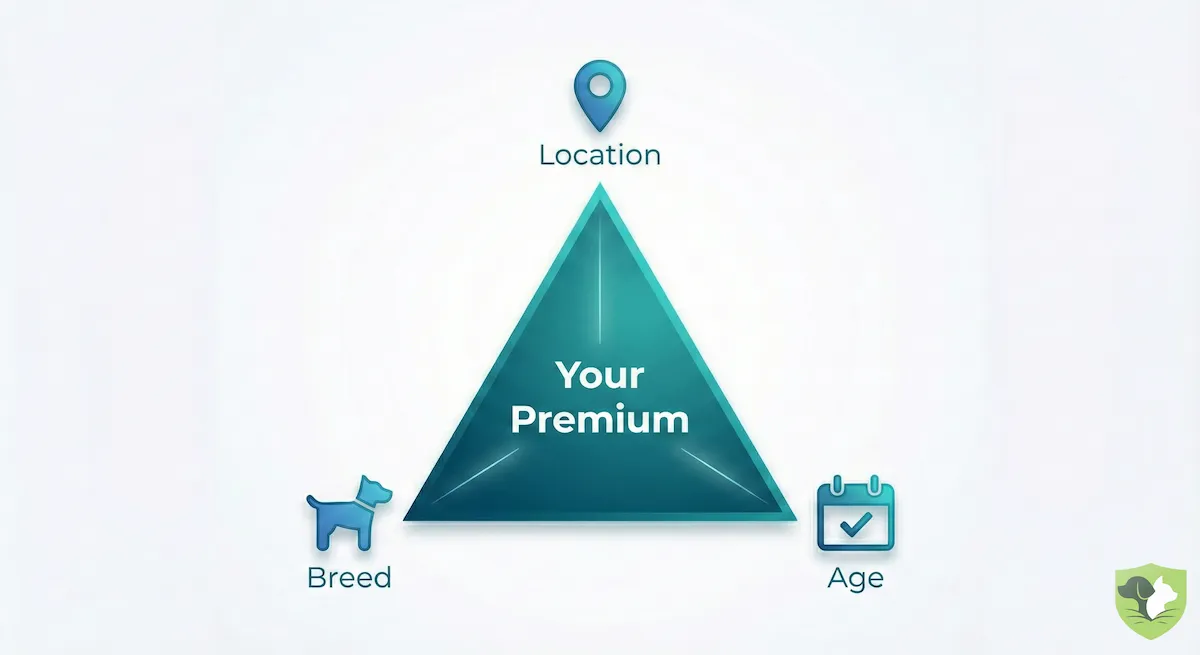

However, relying on a national average is a bit like checking the average temperature of the entire United States: it doesn't tell you if you need a coat. A small mixed-breed dog in a lower-cost ZIP code can price near the low end of national quote samples, while a high-risk breed in an expensive metro can move well above $100 per month under richer coverage. Your premium is not random; it is mainly shaped by four levers: location, breed/species, age, and coverage design.

Table of Contents

- The 2026 National Averages: Establishing a Baseline

- The 4 Factors That Swing Your Premium

- Scenario Analysis: Real World Quotes for 2026

- Expert Insights: The "Hidden" Costs Nobody Talks About

- Top Provider Price Comparison (2026 Landscape)

- Is Pet Insurance Worth the Cost? (ROI Analysis)

- Conclusion

- Frequently Asked Questions (FAQs)

The 2026 National Averages: Establishing a Baseline

Before we dive into the factors that can raise or lower your rate, we need a baseline. The most useful public benchmark for a 2026 buyer is still NAPHIA's 2025 report, because it summarizes the U.S. market at year-end 2024 and is compiled from industry-wide data.

These figures are for standard Accident & Illness coverage, not wellness-only budgeting plans. NAPHIA defines accident-and-illness products as accident benefits plus illnesses such as cancer, infections, and digestive problems. Some policies may cost less because they use accident-only coverage, lower limits, higher deductibles, or fewer included benefits.

Average Dog Insurance Cost

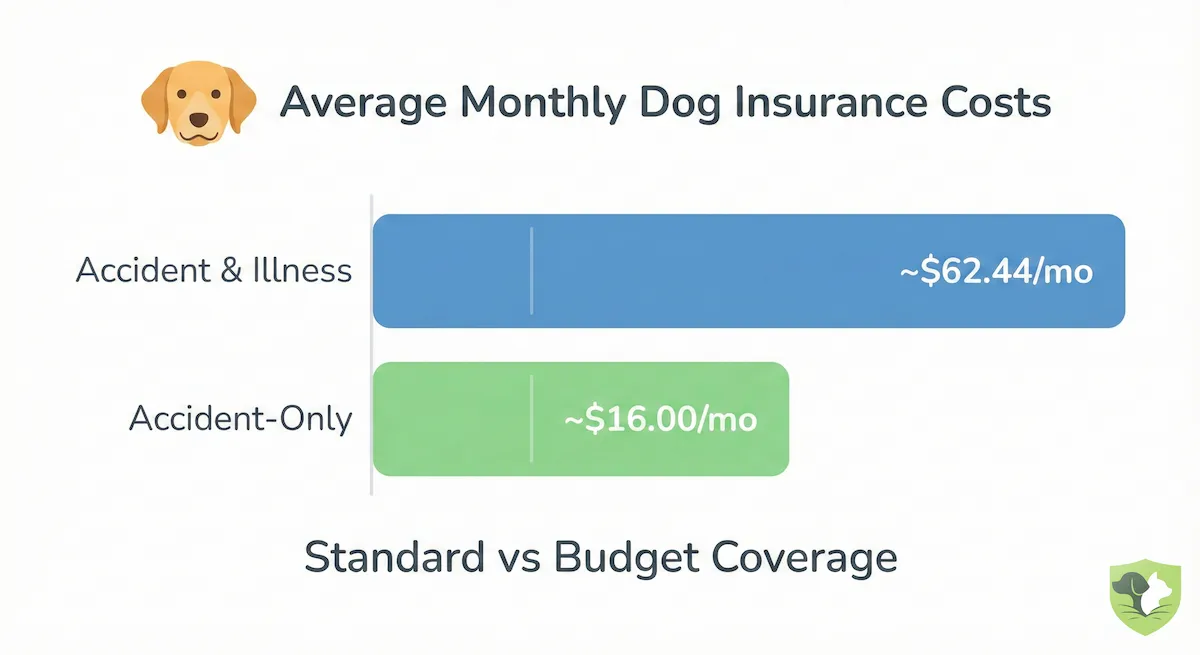

If you are insuring a dog in 2026, expect to pay significantly more than most cat owners — our dog insurance guide breaks down how much dog insurance costs by breed and life stage. NAPHIA's latest U.S. accident-and-illness benchmark is $749.29 per year for dogs, or about $62.44 per month.

However, if you strip away illness coverage and choose an accident-only policy, the national average drops sharply.

Latest Monthly Benchmarks (Dogs):

- Accident & Illness (Standard): ~$62.44/mo

- Accident-Only (Budget): ~$16.11/mo, based on NAPHIA's $193.29 average annual dog accident-only premium

Why are dogs more expensive? The premium gap reflects expected claim cost, not just pet size. Dogs include many higher-risk breed and activity profiles, and MoneyGeek's 2026 model found large swings by breed, age, location, and coverage design. In practice, orthopedic injuries, swallowed objects, cancer, and breed-linked conditions all feed into the pricing math.

Average Cat Insurance Cost

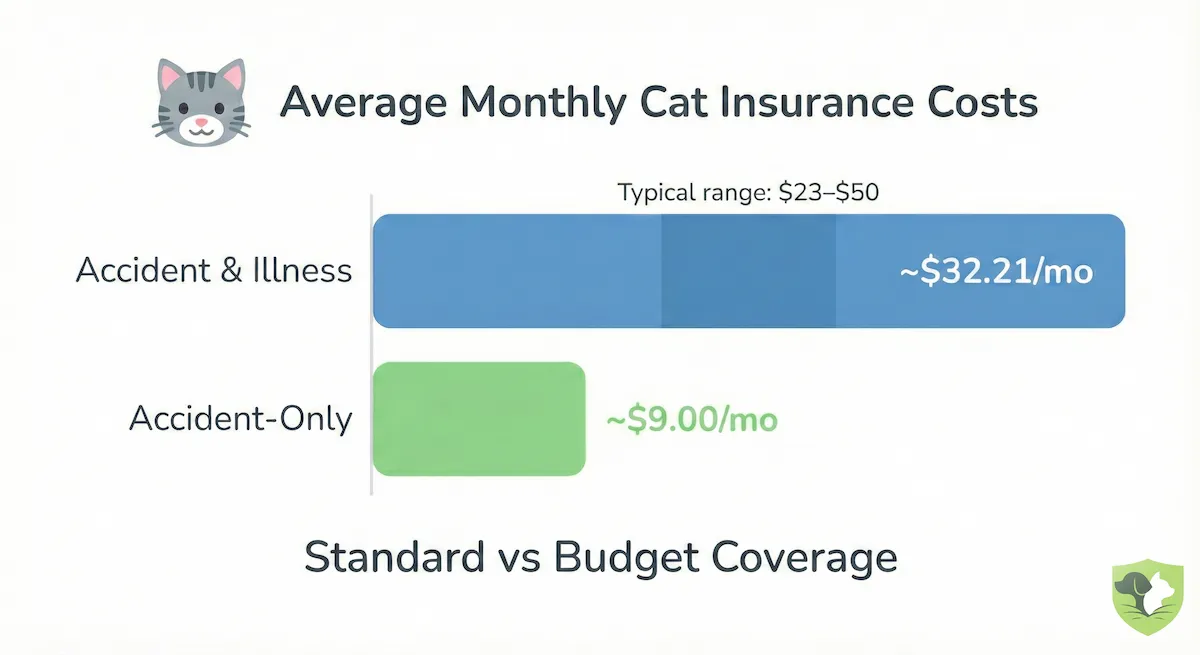

Cats are generally cheaper to insure; our cat insurance guide breaks down how much cat insurance costs and the cat-specific coverage tradeoffs. As a benchmark, NAPHIA's latest U.S. accident-and-illness average is $386.47 per year for cats (about $32.21/month), while accident-only coverage averages about $9.17/month ($110.03/year). Cat premiums vary less than dog premiums, though senior cats cost more as chronic conditions like kidney disease and hyperthyroidism become more relevant.

The 4 Factors That Swing Your Premium

National averages give you a ballpark figure; your quote is built from levers that insurers can rate. The NAIC says pet insurance premiums vary by factors such as species, breed, age, location, and coverage choices. For shopping purposes, think in four buckets: where you live, who your pet is genetically, how old they are, and how much risk you ask the insurer to take.

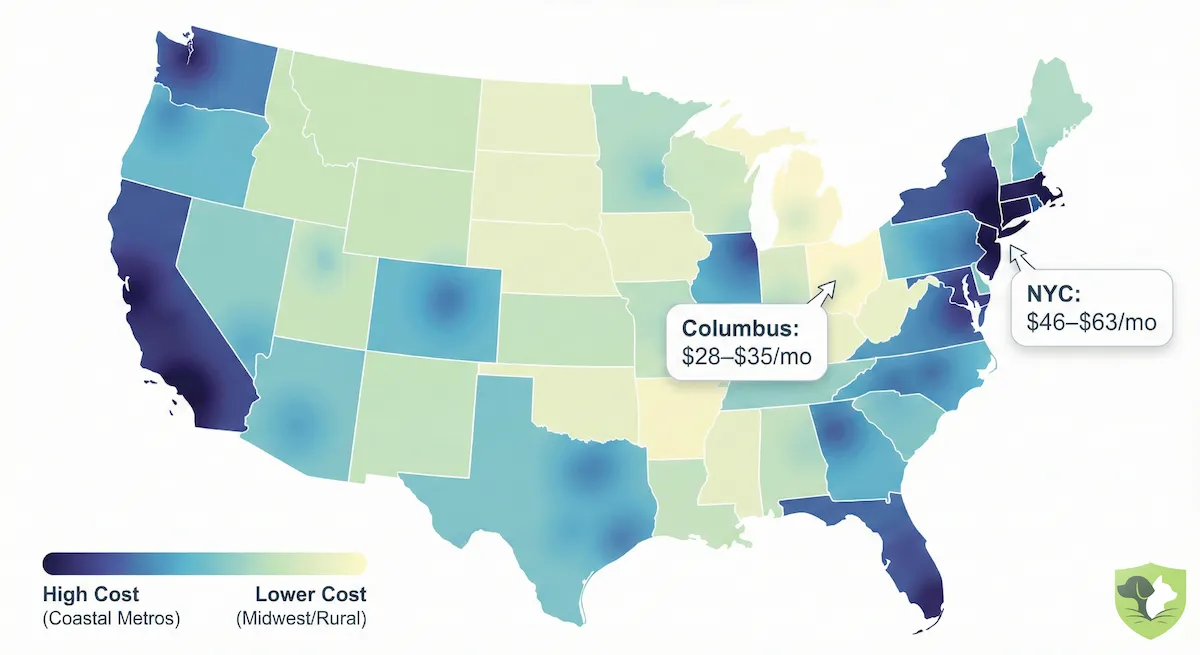

1. Geography: The Local Vet-Cost Effect

Real estate is not the only thing that costs more in expensive markets. Pet insurers price against local veterinary costs and rating territories. Higher practice overhead, emergency-hospital density, specialist availability, wages, and local cost of living can all flow into claim costs and then premiums.

The spread is material. MoneyGeek's 2026 analysis found a 90% gap between the lowest- and highest-cost state or D.C. markets under its standardized profile. That is a cleaner fact than claiming one city is always twice another: the exact quote still depends on your ZIP code, pet profile, and plan settings.

| Location Signal | Why It Matters | What to Check |

|---|---|---|

| High-cost metro or specialty-care market | Higher local vet costs and emergency/specialty infrastructure can raise expected claims. | Compare at least three quotes using the same deductible, reimbursement rate, and annual limit. |

| Lower-cost state or smaller market | Lower local operating costs may reduce premiums for the same pet and plan design. | Do not assume cheap premium equals equal coverage; compare exclusions and limits. |

| Moving ZIP codes | Many policies can rerate based on your new address. | Ask the insurer how a move affects renewal pricing before you relocate. |

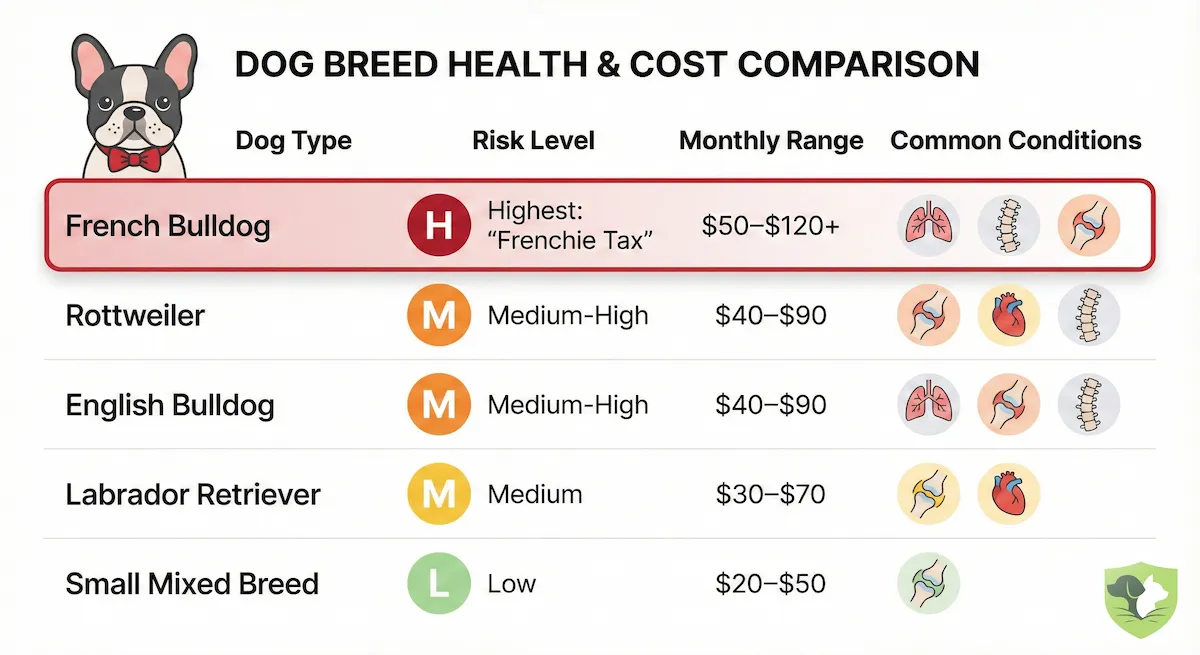

2. Breed Risk: The "Frenchie Tax"

Your pet's DNA is a major financial variable. Insurers use breed-level claims and veterinary-risk data to price the probability of expensive conditions. French Bulldogs are a useful example because they are flat-faced, popular, and often expensive to insure.

Cornell lists French Bulldogs among the breeds most frequently affected by BOAS, and advanced diagnostics such as MRI can run into the thousands when spinal or neurologic problems need workup. That does not mean every Frenchie will have a major claim, but it explains why many quote models place the breed among the higher-cost dogs.

Forbes Advisor's dog-breed pricing table gives a helpful standardized comparison for age-3 dogs with a $250 deductible and 80% reimbursement:

| Breed | $5,000 Annual Coverage | Unlimited Annual Coverage | Risk Context |

|---|---|---|---|

| French Bulldog | $85 | $112 | BOAS, spinal/IVDD exposure |

| Rottweiler | $88 | $107 | Orthopedic and cancer exposure |

| Bulldog | $78 | $101 | Respiratory, skin, orthopedic exposure |

| Labrador Retriever | $56 | $76 | Orthopedic and foreign-body exposure |

| Small Mixed Breed | $32 | $53 | Lower modeled breed cost, but accidents still happen |

3. The Age Curve: Understanding the Senior Cliff

Pricing does not rise in a neat straight line as your pet ages. Younger adult pets often price near the low point; older pets tend to cost more because illness and injury become more likely and more complex.

Forbes Advisor's age table shows dog coverage with a $5,000 annual limit rising from $41/month at age 3 to $74/month at age 7, an increase of about 80% under that sample. Unlimited coverage rose from $64/month at age 3 to $114/month at age 7. By age 9, Forbes also notes that one age-rating dataset more than doubled the base age factor.

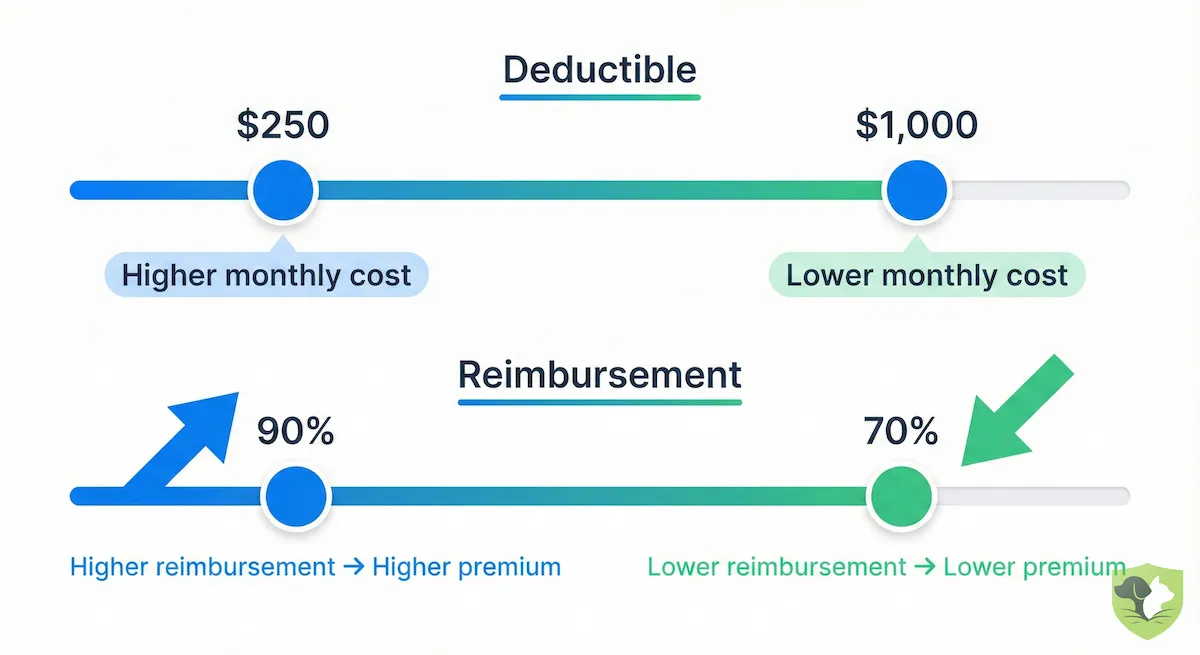

4. Coverage Levers: Deductibles, Limits & Reimbursements

Finally, you control part of the price through policy structure. Higher annual limits, lower deductibles, and higher reimbursement percentages usually raise the premium because the insurer is taking on more of the claim risk.

Deductible changes can be powerful, but the savings are not universal. MoneyGeek's standardized 2026 model found $500-deductible coverage averaged $47/month, while $1,000-deductible coverage averaged $32/month. That is a $15/month difference in that model, though individual insurers price deductible tiers differently. Choosing a higher deductible can make sense if you could still pay that amount in a bad month; otherwise, the lower premium may just move the problem to claim time.

Similarly, adjusting your reimbursement level from 90% down to 70% or 80% can lower the insurer's liability and reduce your monthly cost. The trade-off is simple: you keep more money monthly, but pay more out of pocket when an eligible claim happens.

Scenario Analysis: Real World Quotes for 2026

National averages are useful, but they do not pay your bills. To understand what you may actually pay, look at how location, breed, age, and coverage design stack together. The scenarios below are illustrative, not live quotes; the price ranges are grounded in the sourced market benchmarks above and should be checked against current quotes before buying.

Scenario A: The "Urban Professional" (High Risk, High Cost)

The Profile: A young French Bulldog living in a high-cost city.

The Plan: Unlimited coverage, $250 deductible, 90% reimbursement.

Monthly Cost: commonly above $100, and potentially higher depending on ZIP code and insurer.

The Logic: This is an expensive policy because the breed and plan design both push the premium upward. Forbes Advisor's age-3 French Bulldog sample averaged $112/month for unlimited coverage before layering in every ZIP-code and benefit variation.

The Math: If an eligible Frenchie claim involves BOAS surgery and spinal imaging, the bill can become large quickly. MoneyGeek says BOAS surgery can cost up to $5,000, and PetMD puts a typical dog MRI at $2,300 to $5,000 or more. On a $7,500 eligible bill, a 90% policy with a $250 deductible would reimburse roughly $6,525 before considering premiums, exclusions, waiting periods, annual limits, and state-specific terms.

Scenario B: The "Suburban Family" (Moderate Risk, Balanced Cost)

The Profile: A 3-year-old Labrador Retriever in a mid- or lower-cost market.

The Plan: $5,000 annual limit, $500 deductible, 80% reimbursement.

Monthly Cost: often around the middle of national quote samples; Forbes puts an age-3 Labrador at $56/month for $5,000 coverage with a $250 deductible, while a higher deductible may reduce the quote.

The Logic: This owner uses a capped limit and higher deductible to keep the monthly bill manageable. Labs can still create expensive claims: ACVS lists Labrador Retrievers among breeds with higher incidence of cranial cruciate ligament disease, and swallowed objects can also become surgical emergencies.

The Math: If the dog requires eligible foreign-body surgery costing $3,500, an 80% policy with a $500 deductible would reimburse about $2,400. That can offset several years of premiums, but only if the event is covered and the annual limit has enough room.

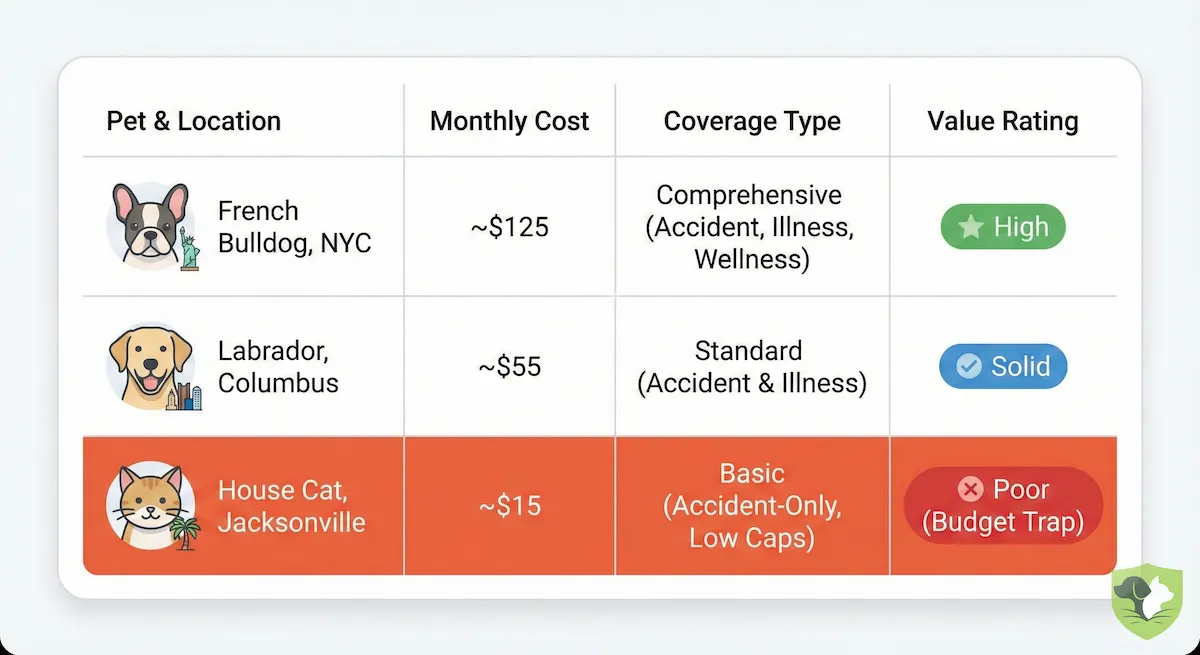

Scenario C: The "Budget" Trap (Low Cost, High Risk)

A 4-year-old Domestic Shorthair on accident-only coverage pays only about $9/month, but accident-only plans exclude illnesses, so a common urinary blockage ($1,425 to $4,000 to treat) would be paid entirely out of pocket. The cheapest plan is often the wrong one.

| Profile | Location | Cost | Plan | Verdict |

|---|---|---|---|---|

| French Bulldog (Young) | High-cost city | $100+ possible | Unlimited / 90% | High premium, but large breed-linked claims are exactly what this policy is meant to hedge. |

| Labrador (Adult) | Mid-cost or lower-cost market | Mid-range quote | $5k limit / $500 deductible / 80% | Balanced if the annual limit is enough for the owner's risk tolerance. |

| House Cat | Any market | ~$9 accident-only average | Accident-only | Cheap, but it leaves common illnesses such as urinary blockage uncovered. |

Expert Insights: The "Hidden" Costs Nobody Talks About

The monthly premium gets the attention, but the real cost of pet insurance is often hidden in claim rules and renewal behavior. The expensive surprises usually come from three places: bilateral exclusions, veterinary inflation, and wellness add-ons that are not the same thing as insurance.

1. The "Bilateral Exclusion" Trap

A bilateral condition is one that can affect paired body parts, such as knees, hips, eyes, or elbows. This matters because a pre-existing issue on one side can sometimes affect coverage for the other side.

The Trap: Some policies treat paired-body-part problems as related. Healthy Paws says that if a cruciate ligament on one leg is injured before enrollment or during its waiting period, the cruciate ligament on the other leg is excluded. Other insurers use different language, so read the bilateral and cruciate sections before buying if you have a large or athletic dog.

Example: You adopt a Labrador whose record mentions a left-knee limp before coverage. Next year, he tears the right CCL. Depending on the policy language and medical records, the insurer may treat the new claim as related to a pre-existing bilateral problem.

Who is stricter vs. more flexible?

- Stricter language: Policies with explicit bilateral or cruciate exclusions can remove coverage for the opposite side when the first side was pre-existing.

- More flexible language: AKC Pet Insurance advertises coverage for some pre-existing conditions after 365 days of continuous coverage, where available and subject to policy terms. This is unusual, and buyers should confirm the exact state policy.

2. Veterinary Inflation Is Not Just a Feeling

If your quote feels high, part of the reason is that veterinary care itself is more expensive. The most current BLS release available as of this update is the April 2026 CPI report, released May 12, 2026. BLS reported pet services including veterinary services up 5.2% year over year, and veterinarian services up 5.5%, while all items rose 3.8%.

- The Old Days: A limping dog might have received rest, medication, and basic X-rays.

- Current Specialty-Care Reality: That same dog may now be referred for advanced imaging, surgery, rehabilitation, and follow-up care. Dog MRIs can cost $2,300 to $5,000 or more, and TPLO surgery can reach $10,000.

The Reality: Insurers price premiums around the care owners are likely to seek and veterinarians are able to provide. More advanced care is good medicine, but it raises the size of possible claims.

3. Wellness Plans Are Separate Budgeting Tools

Wellness plans are not the same as accident-and-illness insurance. The NAIC Model Act defines wellness programs separately from pet insurance unless state law treats them as insurance. California went further: SB 1217 requires clearer separation between pet insurance and wellness programs for California consumers.

The Math Check: For many pet owners, wellness plans are closer to budgeting accounts with caps than true risk transfer.

- Typical Cost: Forbes Advisor reports average wellness-plan add-on costs of about $24/month for dogs and $22/month for cats.

- Typical Test: Compare the annual wellness premium with the exact preventive benefits you expect to use: vaccines, fecal tests, heartworm tests, flea/tick prevention, dental cleaning, and routine exams.

Verdict: Add wellness only if the numbers work for your pet. Treat accident-and-illness insurance as protection against the $5,000 or $10,000 event, not as a way to prepay every routine vaccine.

Top Provider Price Comparison (2026 Landscape)

Finding the "best" price is not just about sorting by the lowest monthly number. It is about finding the right financial fit for your pet's risks and your cash-flow limits. Below is a feature-focused landscape, not a universal ranking: prices change by ZIP code, breed, age, deductible, reimbursement rate, annual limit, and add-ons.

Budget & App-Forward Options: Lemonade & Figo

If your priority is a lower monthly payment and you are comfortable managing claims digitally, Lemonade and Figo are worth comparing.

- Lemonade:

- The Price Tag: Forbes Advisor's company table put Lemonade among the lower average dog and cat costs in its sample.

- The Trade-Off: The coverage can be modular. Lemonade describes add-ons for items such as vet visit fees, physical therapy, dental illness, and end-of-life/remembrance benefits.

- Claims Note: Lemonade emphasizes digital claims and automation, but medical-record review, exclusions, and waiting periods still matter.

- Figo:

- The Price Tag: Forbes Advisor's sample table lists Figo dog averages of $42/month for $5,000 coverage and $66/month for unlimited coverage, under its assumptions.

- The Waiting Period: Forbes Advisor lists Figo's accident waiting period as one day and illness waiting period as 14 days, with state and orthopedic variations to check in the policy.

Medical Safety Net: Trupanion

Trupanion usually competes on claims structure rather than sticker price. It can be expensive, but the design is distinctive.

- The Price Tag: Expect quotes to vary widely; high-risk breeds in high-cost cities can be expensive under unlimited coverage.

- The Value Proposition:

- Direct Pay: Trupanion says VetDirect Pay can pay participating veterinarians directly at checkout for eligible claims.

- Lifetime Per-Condition Deductible: Trupanion's deductible applies once per condition for the pet's lifetime, rather than resetting annually for the same eligible condition.

- No Payout Caps: Trupanion says it has no per-incident, annual, or lifetime payout limits, subject to the policy's terms and exclusions.

Older Pets: Spot, Pets Best & ASPCA

Senior-pet shopping is less about finding a magically cheap quote and more about eligibility, exclusions, and whether new conditions can still be meaningfully covered.

- The Price Tag: Senior premiums can be high, and prior conditions may be excluded. Compare quotes only after reviewing medical records.

- The Senior Advantage:

- No Upper Age Limit: Spot, Pets Best, and ASPCA Pet Health Insurance are all worth comparing for older pets because they advertise no upper age limit for new enrollment.

- Mobility Focus: Pets Best says prosthetic devices and wheelchairs can be covered when prescribed or provided by a licensed veterinarian for a covered accident or illness.

- Orthopedic Waiting Period: Spot's sample policy lists a 14-day waiting period for ligament and knee conditions, though state and policy versions can vary.

| Provider | Best For... | Cost Tier | Feature to Verify |

|---|---|---|---|

| Lemonade | Digital shoppers comparing lower-cost quotes | $ to $$ | Which add-ons are needed for exam fees, rehab, or dental illness |

| Figo | App-forward owners who value short accident waiting periods | $$ | State-specific waiting periods and orthopedic rules |

| Trupanion | High-risk breeds and chronic-condition planning | $$$ | VetDirect Pay participation and lifetime per-condition deductible |

| Spot | Seniors and rescues | $$ | No upper age limit and sample-policy knee/ligament language |

| Pets Best | Older pets and owners comparing broad benefit menus | $$ | No upper age limit, direct-pay option, and mobility-device language |

Is Pet Insurance Worth the Cost? (ROI Analysis)

The biggest mistake pet owners make is trying to "beat the house." If you are buying insurance hoping to get back exactly what you paid in premiums every year, you are doing the math wrong. Pet insurance is not an investment product; it is a hedge against a bill you could not comfortably absorb.

The "Savings Account" Fallacy

A common argument is, "I'll just put $50 a month into a savings account." That can work if you already have a large emergency fund on day one. It breaks down when the expensive event happens before the savings have accumulated.

- The Scenario: You save $50/month for your dog.

- The Reality: By year two, you have saved $1,200.

- The Crisis: Your dog tears a CCL or needs another major surgery. A TPLO knee surgery can reach $10,000.

- The Result: You are short by thousands of dollars unless you already had emergency money available.

To self-insure against a $10,000 oncology, orthopedic, or specialty-care bill, you would need to save $50 a month for more than 16 years before reaching that amount, not counting investment returns, inflation, or any smaller vet bills along the way.

When to Skip It

There are specific times when insurance may not be worth the cost.

- Geriatric Enrollment With Major Pre-Existing Disease: If you try to insure a 12-year-old dog with pre-existing diabetes, you may pay a high premium for a policy that excludes the diabetes and related history. In that case, a dedicated savings account may be a better fit.

- Low Appetite for Advanced Care: If you know you would not pursue chemotherapy, complex orthopedic surgery, advanced imaging, or specialty hospitalization, high-limit coverage may not match your values or budget. Accident-only coverage or a savings strategy may be more appropriate.

The "Peace of Mind" Dividend

Ultimately, the ROI of pet insurance is measured in hard decisions avoided. Cost already changes care decisions: Gallup and PetSmart Charities found that 52% of U.S. pet owners skipped or declined veterinary care in the past year, with cost as the leading barrier. Insurance cannot make every claim payable, but a good policy can reduce the chance that prognosis takes a back seat to the bank balance.

Conclusion

In 2026, the best public benchmark says U.S. accident-and-illness pet insurance averages about $62/month for dogs and $32/month for cats. That gives you a starting point, not a quote. Your actual price can shift sharply based on location, breed or species, age, deductible, reimbursement rate, annual limit, and add-ons.

The right question is not simply "is pet insurance expensive?" It is "what size vet bill would change my medical decision?" If a $5,000 to $10,000 eligible emergency would force debt, delay, or a painful care decision, a well-chosen policy deserves a serious look. If you can comfortably self-insure, or if the policy excludes the conditions you are most worried about, the monthly premium may be better directed elsewhere.

Frequently Asked Questions (FAQs)

Why did my pet insurance premium go up this year?

Premiums can rise because of your pet's age, your ZIP code, insurer rate filings, local veterinary costs, and policy design. BLS reported veterinarian services up 5.5% year over year in April 2026, which helps explain why renewal prices can climb even if you did not file a claim.

Is "Accident-Only" insurance worth it?

It can be, if your budget cannot support accident-and-illness coverage. NAPHIA's latest U.S. accident-only averages are about $16/month for dogs and $9/month for cats. The trade-off is big: accident-only coverage generally will not cover illnesses such as cancer, diabetes, allergies, urinary blockage, or kidney disease.

Does insurance cover spaying/neutering?

Generally, no. The NAIC Regulator's Guide lists spaying or castration among common exclusions. Some wellness add-ons can reimburse part of routine or preventive care, but those add-ons should be compared against the exact benefits you expect to use.

How do I choose between providers if my pet has a pre-existing condition?

The right choice depends on whether the condition is curable, chronic, or still showing signs.

- For curable conditions: Look closely at insurers that publish curable-condition language. ASPCA and Spot describe 180-day symptom-free and treatment-free rules for some curable conditions.

- For incurable conditions: Most insurers exclude chronic pre-existing conditions. AKC Pet Insurance advertises coverage for some pre-existing conditions after 365 days of continuous coverage, where available and subject to policy terms.

What specific illnesses or treatments are commonly excluded or easy to miss?

Beyond the universal pre-existing-condition issue, check these areas before buying:

- Exam Fees: Some policies cover treatment but not the exam fee. Healthy Paws explicitly says examination fees are not covered, while other insurers may include exam fees or offer them as an add-on.

- Bilateral Conditions: Knee, hip, eye, and elbow language matters. A prior issue on one side can affect the other side under some policies.

- Dental Illness: Dental accidents are often treated differently from dental illness. Fetch advertises dental illness coverage, while other plans may exclude, cap, or condition dental illness coverage.

How quickly do most insurers reimburse claims, and what documentation is typically required?

Speed varies by insurer, claim complexity, and whether medical records are complete.

- The Speed: Digital-first insurers may pay simple claims quickly, but complex claims can still require human review. Trupanion's VetDirect Pay can pay participating vets directly at checkout for eligible claims.

- The Paperwork: You typically need an itemized invoice, proof of payment, and medical records. Many first claims trigger a medical-history review to check for pre-existing signs, symptoms, or treatment.

Can I adjust my deductible or reimbursement rate after enrolling, or am I locked in?

You are often able to reduce coverage, but raising coverage can trigger underwriting or new waiting-period/pre-existing-condition issues depending on the insurer and state.

- Lowering Coverage (Cheaper): Raising your deductible or lowering your reimbursement percentage usually lowers premiums. Healthy Paws says customers with submitted claims can lower reimbursement and raise deductible.

- Raising Coverage (Better): Lowering your deductible, raising reimbursement, or increasing limits can be treated differently because the insurer is taking on more risk. Ask whether the change creates new waiting periods or new exclusions before you make it.

WhiskerCover is reader-supported. When you click on links to pet insurance partners on our site and purchase a policy, we may earn a commission at no extra cost to you. Learn more about how we make money.

Sources

- NAIC Pet Insurance Overview

- NAIC Pet Insurance Model Act

- NAIC Regulator's Guide to Pet Insurance

- NAPHIA 2025 State of the Industry Report

- NAPHIA 2025 Report Highlights PDF

- Bureau of Labor Statistics CPI News Release, April 2026

- MoneyGeek Average Pet Insurance Cost 2026

- Forbes Advisor Average Cost of Pet Insurance 2026

- Forbes Advisor Figo Pet Insurance Review

- Cornell Riney Canine Health Center: BOAS

- American College of Veterinary Surgeons: Cranial Cruciate Ligament Disease

- PetMD Dog MRI Cost

- Lemonade TPLO Surgery Cost Guide

- MoneyGeek BOAS Surgery Coverage and Cost Guide

- PetPlace Cat Urinary Blockage Treatment Cost

- Healthy Paws Coverage and Exclusions

- AKC Pet Insurance Pre-Existing Conditions

- California SB 1217

- Lemonade Pet Add-Ons

- Trupanion VetDirect Pay

- Trupanion Deductibles

- Trupanion Payouts

- Spot Pet Insurance Enrollment Age

- Spot Sample Policy

- Spot Pre-Existing Conditions

- Pets Best Coverage

- ASPCA Pet Health Insurance Pre-Existing Conditions

- Fetch Pet Insurance Dental Coverage

- Gallup / PetSmart Charities State of Pet Care Study