It is the question every pet parent fears. It's 2:00 AM, and the emergency vet hands you a tablet. The estimate for your dog's surgery isn't $500; for some specialty procedures, it can reach $10,000 or more.

Then comes the devastating pause: "How do you want to proceed?"

In 2026, this is the reality many owners are planning around. Modern specialty care can involve advanced imaging such as MRI, chemotherapy protocols, and orthopedic reconstruction. That does not mean every case needs the most expensive option, but the menu of possible care is broader, and often pricier, than it was a generation ago.

Veterinary prices are still rising faster than general inflation. BLS CPI data for April 2026 shows veterinarian services up 5.5% year over year, compared with 3.8% for all items; the broader "pet services including veterinary" category rose 5.2%.

If your pet stays healthy, you will likely lose money on premiums, and that is the best-case scenario.

The core thesis is simple: pet insurance in 2026 is not an investment strategy; it is a financial risk-transfer tool. It can turn a potential $5,000 to $20,000 household shock into a predictable monthly cost, reducing the chance that a large bill becomes the deciding factor in a medical decision.

Table of Contents

- The New Math of Vet Care: Why Costs Are Soaring

- The Financial Breakdown: Premiums vs. Payouts

- Is Dog Insurance Worth It?

- Is Cat Insurance Worth It? (The Indoor Cat Fallacy)

- Pros and Cons of Pet Insurance (The Unfiltered Truth)

- The "Gotchas": 4 Clauses That Kill Value

- Expert Insights: The 2026 Market Landscape

- Strategic Advice: How to Play the Game in 2026

- Conclusion: The Final Verdict

- Frequently Asked Questions (FAQs)

The New Math of Vet Care: Why Costs Are Soaring

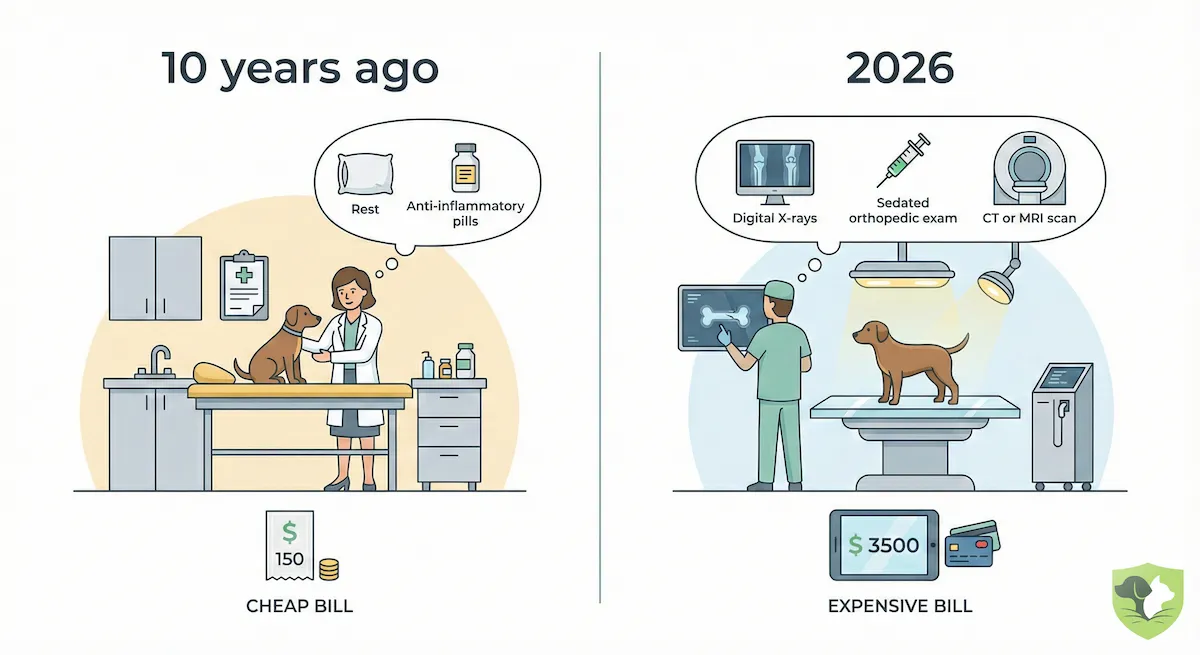

You aren't imagining it; the bill really is higher. If you owned a dog ten years ago, a limp might have been treated with rest and anti-inflammatories. Today, the same limp may lead to digital X-rays, a sedated orthopedic exam, and, in specialty cases, referral imaging or surgery.

This is partly a medical progress story and partly a cost story. AAHA reported that the average U.S. vet bill had risen more than 60% over the prior decade, while current BLS data shows veterinarian services still outpacing all-items inflation.

Here are the three factors that make modern vet bills feel so different:

1. The New "Gold Standard" of Care

Advanced care options that once felt rare are now part of the normal specialty-care conversation.

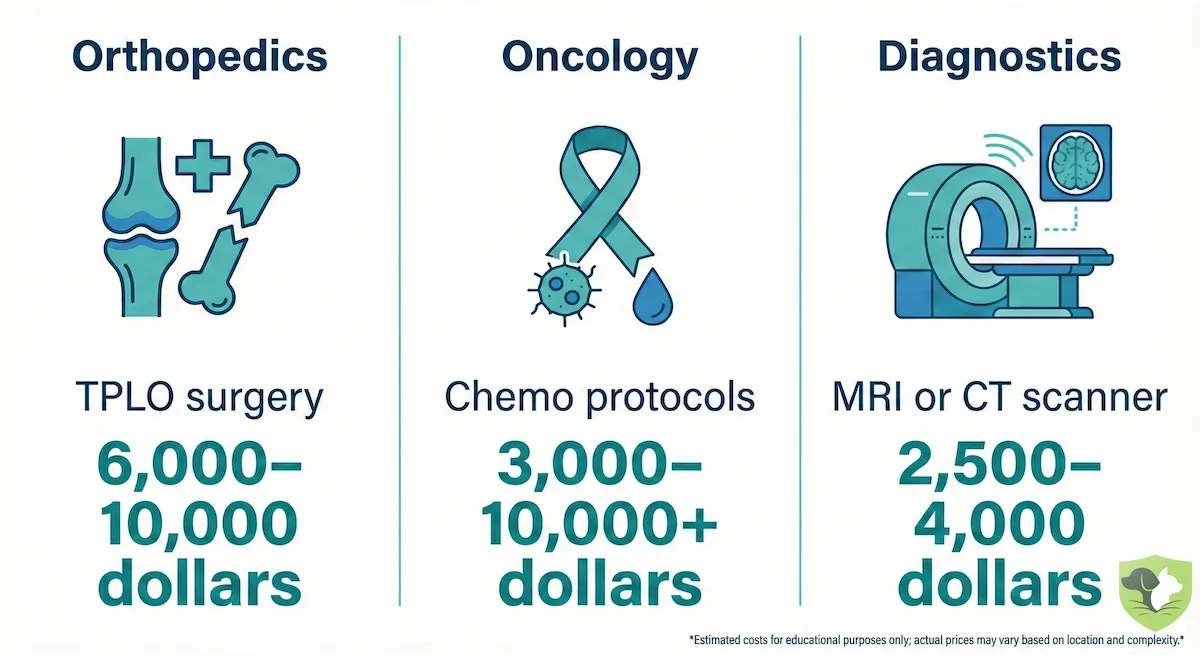

- Orthopedics: The American College of Veterinary Surgeons describes TPLO as one of the major surgical options for canine cranial cruciate ligament disease. Cost varies by hospital and region, but dog knee surgery can reach $10,000.

- Oncology: Cancer care can involve staging, surgery, chemotherapy, and repeat monitoring. For canine lymphoma, NC State's veterinary hospital lists rescue lymphoma treatments at roughly $600 to $1,000 per treatment, so multi-visit protocols can become a major bill.

- Diagnostics: PetMD lists a typical dog MRI range of about $2,300 to $5,000 or more, largely because MRI usually requires anesthesia, monitoring, specialized equipment, and interpretation.

2. Corporate Consolidation

Corporate and private-equity-backed ownership has become a bigger part of veterinary medicine, especially in specialty and emergency care. AAHA's Trends magazine summarizes the rise of corporate consolidation and private equity in veterinary practice, and the FTC has required divestitures in veterinary specialty and emergency markets where it alleged reduced competition.

Consolidation does not automatically mean worse care or a higher bill in every clinic. It does mean more owners now encounter larger hospital systems with advanced diagnostics, standardized workflows, and corporate pricing structures, so comparing estimates and asking what each diagnostic step changes can matter.

3. Labor and Overhead Pressure

Veterinary clinics are labor-heavy medical businesses. Local wages, staffing availability, rent, equipment, anesthesia monitoring, and overnight care all show up in the final invoice. That is why the same emergency can cost very different amounts in a rural clinic, a general practice, and a 24-hour specialty hospital in a high-cost metro area.

The Bottom Line: You are paying for a level of medical sophistication that often did not exist, or was not widely available, a generation ago. The sticker shock is the price of access to MRI machines, board-certified specialists, intensive monitoring, and life-extending treatments.

The Financial Breakdown: Premiums vs. Payouts

To determine true pet insurance value, we have to move beyond feelings and look at the ledger. The math of insurance is a trade: you pay a known, fixed premium to reduce exposure to an unknown, potentially catastrophic claim.

Here is what that trade looks like in 2026.

The Cost of Coverage

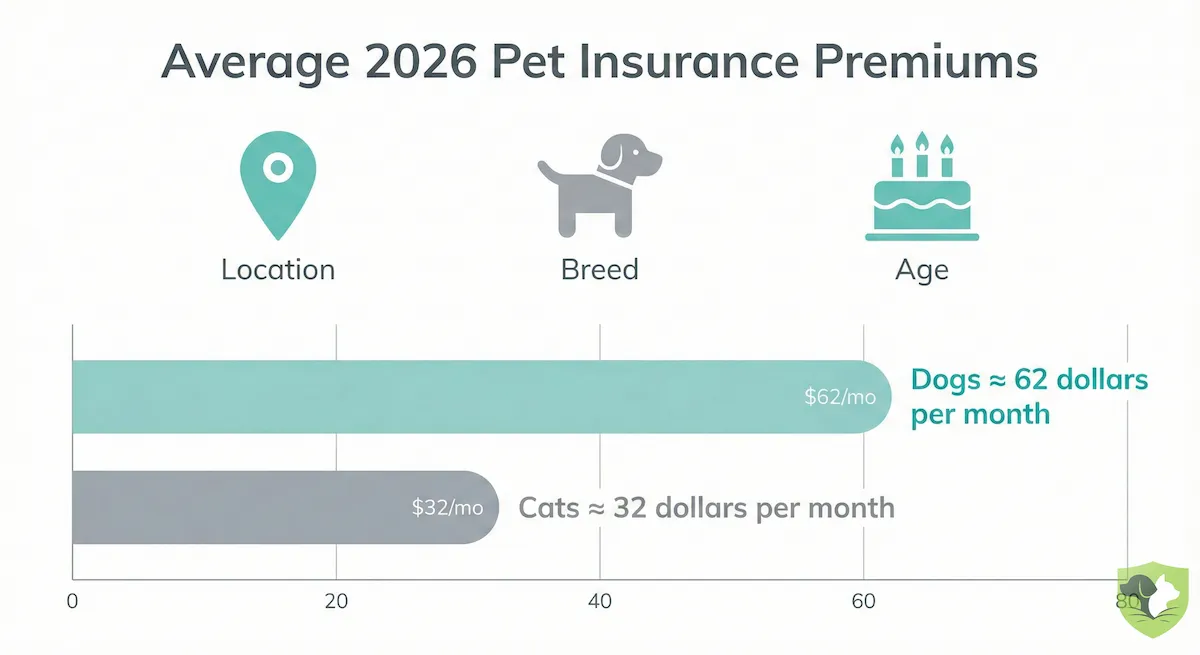

The best current public benchmark is NAPHIA's 2025 State of the Industry data. For U.S. accident-and-illness policies in 2024, NAPHIA reported average premiums of $749.29 per year for dogs and $386.47 for cats, or about $62.44/month for dogs and $32.21/month for cats. However, "average" is a dangerous metric. Your actual rate depends heavily on three variables:

- Location: The NAIC says pet insurance cost depends on variables including location, because local veterinary prices and rating territories affect the premium.

- Breed: Breed affects both claim risk and price. A French Bulldog may cost far more to insure than a small mixed-breed dog because of known breed risks such as brachycephalic obstructive airway syndrome.

- The "Loyalty Penalty" (Birthday Pricing): Premiums are not fixed forever. They can rise as your pet ages and as local veterinary costs rise. Forbes Advisor's sample pricing shows materially higher rates for older dogs than younger dogs under the same plan assumptions.

The "Self-Insurance" Myth

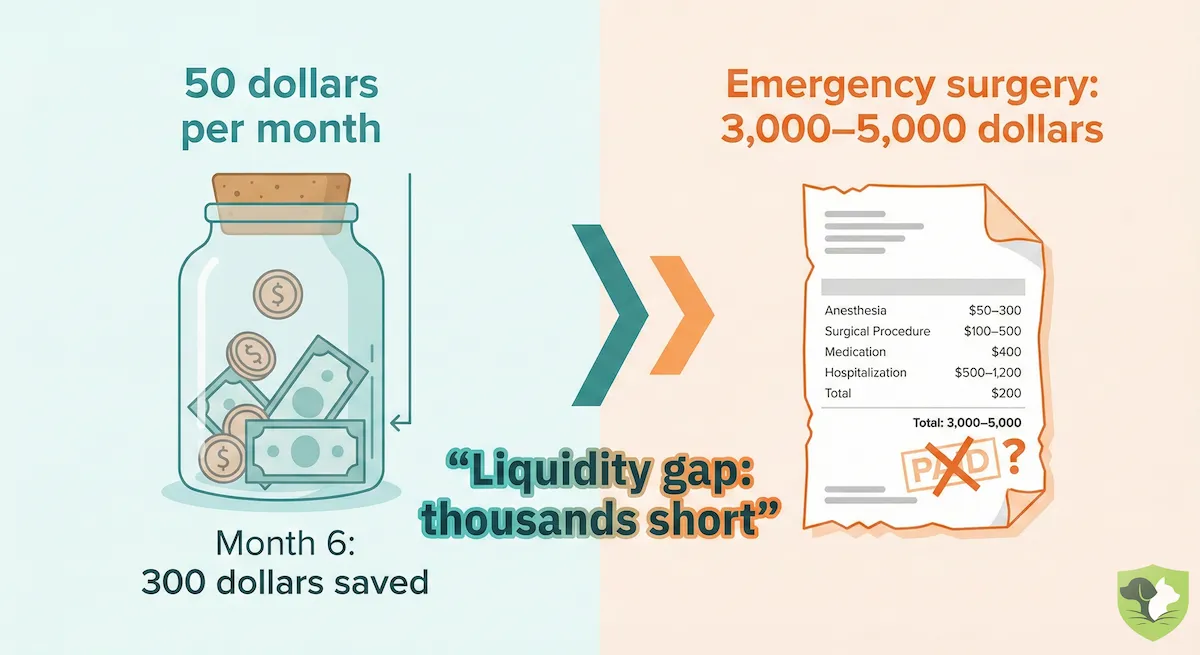

A common argument against insurance is the "Savings Account Strategy." The logic seems sound: Why pay an insurer $50 a month? I'll just put that $50 into a high-yield savings account.

Here is why that math often fails in the real world: liquidity speed. Federal Reserve data shows 63% of U.S. adults could cover a $400 emergency expense using cash or its equivalent in 2025. A $5,000 vet bill is a different problem entirely.

| Scenario | Timeline | Amount Saved/Paid | Vet Bill | Result |

|---|---|---|---|---|

| Savings Account | Month 6 | $300 saved | $5,000 surgery | $4,700 shortfall |

| Insurance | Month 6 | $300 in premiums | $5,000 surgery | Eligible reimbursement after deductible, coinsurance, limits, exclusions, and waiting periods |

To self-insure effectively, you need meaningful emergency money available on Day 1, not accumulated over five years. Insurance can provide access to the policy's coverage limit after waiting periods, though many plans still require you to pay the vet first and file for reimbursement.

The Break-Even Analysis

Does insurance ever pay for itself? If your pet is lucky and healthy, you will probably lose money. But it only takes one major eligible event to flip the equation.

Consider TPLO knee surgery for a dog:

- Total Cost: Depending on provider and region, dog knee surgery can reach $10,000.

- Premiums: At $60/month for 10 years, your premium spend is $7,200.

- Reimbursement reality: On an $8,000 eligible bill, an 80% policy with a $500 deductible might reimburse roughly $6,000, leaving you with about $2,000 plus premiums. A 90% policy would leave less, but every policy is governed by its own deductible, annual limit, exclusions, and reimbursement method.

That is where the financial value lies: not in the small stuff, but in the high-cost claims you cannot comfortably absorb alone.

Is Dog Insurance Worth It?

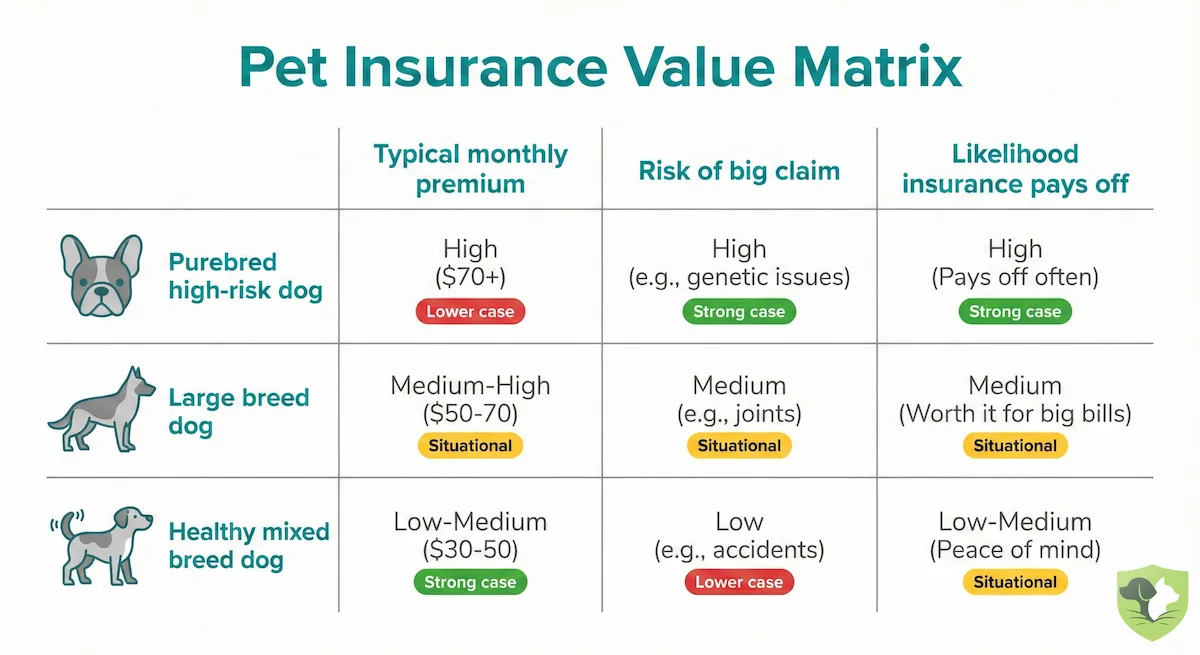

If you own a dog in 2026, the answer to is dog insurance worth it usually comes down to two factors: medical risk and financial resilience.

Dogs are more expensive to insure than cats on average. NAPHIA's latest U.S. benchmark puts accident-and-illness coverage at about $62/month for dogs versus $32/month for cats. But that average hides the real story. Your dog's breed, age, location, activity level, and medical record matter more than the national mean.

The Higher-Risk Purebred Profile

If you own a purebred, you may be paying a "breed tax." Insurers use breed-level claims data to price the probability of certain expensive conditions.

- The French Bulldog: Frenchies are often expensive to insure because they are a brachycephalic breed. Cornell lists French Bulldogs among the breeds most frequently affected by BOAS, a condition that can involve breathing difficulty, advanced diagnostics, and sometimes surgical correction.

- Large Breeds: Large and giant breeds carry more orthopedic exposure. Merck Veterinary Manual notes that hip dysplasia is most common in large-breed dogs, and ACVS lists Rottweilers, Newfoundlands, Mastiffs, Saint Bernards, Chesapeake Bay Retrievers, and Labrador Retrievers among breeds with higher incidence of cranial cruciate ligament disease.

For these dogs, insurance deserves a close look because a single eligible orthopedic, airway, or cancer claim can overwhelm a normal emergency fund.

The Mixed Breed Argument

Owners of mixed breeds often argue, "My dog is a healthy mutt; I don't need coverage." Mixed-breed dogs can be cheaper to insure, but mixed genetics do not protect against accidents.

The classic example is foreign body ingestion: swallowing a sock, corn cob, toy, or other object that does not pass. Forbes Advisor's vet-cost analysis lists swallowed foreign-object surgery at about $3,500 for dogs, and other emergency-cost datasets put some cases higher.

- The Cost: Often several thousand dollars once exam, imaging, anesthesia, surgery, hospitalization, and medications are included.

- The Math: At $50/month, it takes almost six years to save $3,500, and much longer if the bill lands closer to $5,000 or above.

Insurance can help only if the event is eligible and the policy was already active before the accident.

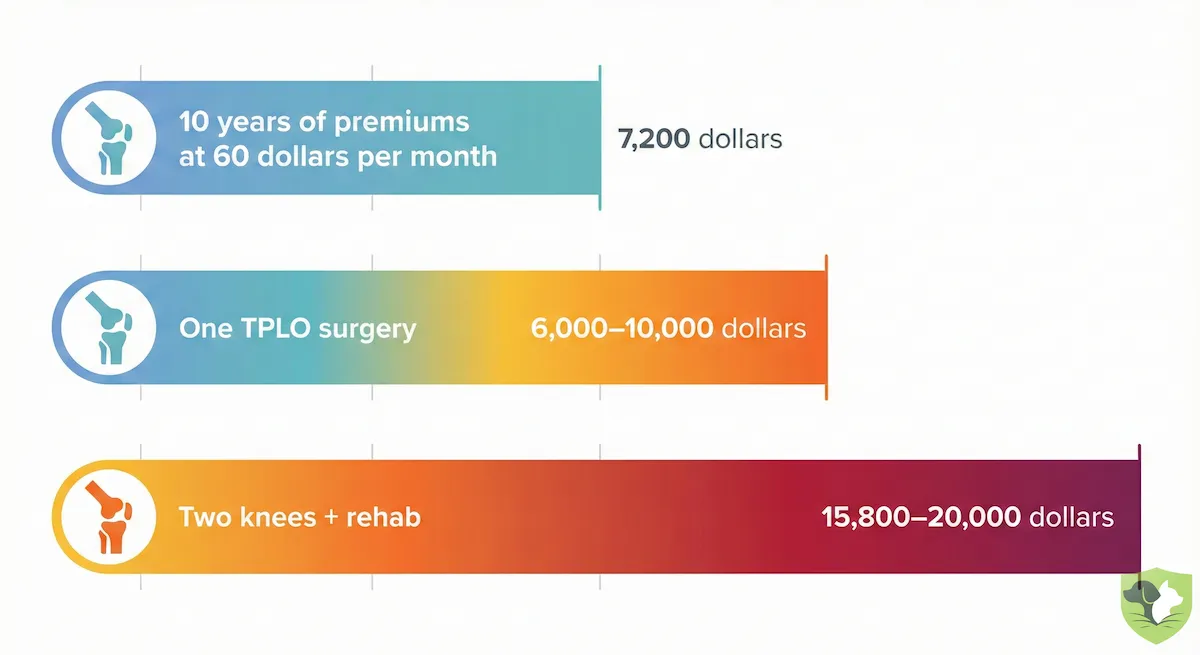

Case Study: The Expensive Knee

To understand the true financial risk of dog ownership, look at cranial cruciate ligament disease, the dog equivalent of an ACL problem. ACVS says cranial cruciate ligament rupture is one of the most common causes of hind-limb lameness, pain, and knee arthritis in dogs. In many larger, active dogs, TPLO is one common surgical option.

Here is the math for a larger dog:

- Surgery Cost: Can reach $10,000, depending on hospital, region, and complexity.

- Rehabilitation: Rechecks, pain medication, restricted activity, and rehabilitation can add meaningful cost after surgery.

- The Bilateral Trap: ACVS says 40% to 60% of dogs with cruciate disease in one knee will later develop a similar problem in the other knee.

For a bilateral rupture, the combined exposure can exceed a low annual limit. If you buy a $5,000 annual-limit policy for a large breed, you may still have a large out-of-pocket bill. This is why large-dog owners should compare higher or unlimited annual limits, not just the cheapest monthly premium.

Is Cat Insurance Worth It? (The Indoor Cat Fallacy)

If you ask a cat parent is cat insurance worth it, the hesitation is almost always the same: "He's an indoor cat. He sleeps on the sofa. What could possibly happen?"

This is the Indoor Cat Fallacy. We assume risk is tied to the outdoors: cars, fights, and falls. But for cats, especially male cats, some of the biggest risks are biological, not environmental.

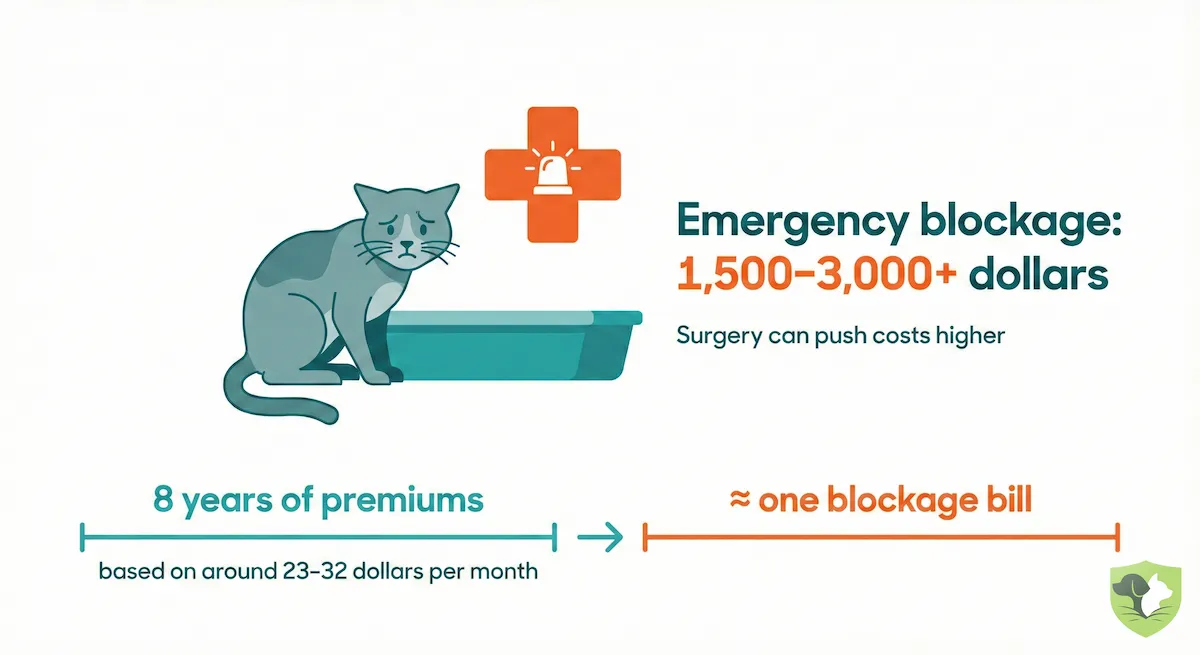

The $3,000 Litter Box Problem

The strongest argument for insuring a male cat is the urinary obstruction scenario. Cornell describes urethral obstruction as a true medical emergency; male and neutered male cats are at greater risk because their urethra is longer and narrower, and death can occur in less than 24 to 48 hours if a complete blockage is not relieved.

- The Cost: Treatment typically involves exam, diagnostics, sedation or anesthesia, catheterization, IV fluids, pain control, and hospitalization. PetPlace estimates that a three-day urinary blockage case can run about $1,425 to $4,000.

- The Math: With NAPHIA's average cat accident-and-illness premium at about $32/month, one serious urinary event can equal several years of premiums.

The Slow Burn of Chronic Illness

While dogs often create big orthopedic bills, cats are famous for chronic illness. Cornell says chronic kidney disease affects up to 40% of cats over age 10 and 80% of cats over age 15. Diabetes, hyperthyroidism, dental disease, and kidney disease can all create recurring bills for lab work, medication, prescription food, and monitoring.

Policies with a per-condition deductible, such as Trupanion's lifetime per-condition deductible, can be mathematically attractive for eligible chronic conditions because you do not pay that condition deductible again after it is met. The key word is eligible: pre-existing conditions, waiting periods, exam fees, and policy exclusions still matter.

The Cat-Specific Market Shift

The industry has started recognizing that cats are not simply "small dogs." Cat-focused brands such as Felix are part of that shift. Still, do not assume a cat-specific brand automatically covers every feline problem. Compare the sample policy, pre-existing-condition language, dental rules, and any end-of-life or wellness benefits before buying.

The Verdict: Because cat premiums are significantly lower than dog premiums, the threshold to break even is lower. You do not need a car accident to justify coverage; one bad weekend with a urinary issue can change the math.

Pros and Cons of Pet Insurance (The Unfiltered Truth)

Searching for "pros and cons of pet insurance" usually yields generic lists about peace of mind. But in 2026, the distinctions are sharper. Insurance is a regulated financial product, and like any financial product, it has tradeoffs you should understand before buying.

The Pros: Why It Can Save Lives

- Liquidity is the real product: The primary benefit is not routine savings; it is liquidity during a bad week. Gallup and PetSmart Charities found that 52% of U.S. pet owners skipped or declined veterinary care in the past year, and cost was the leading barrier among those who skipped or declined care.

- Access to advanced medicine: Without insurance, a referral MRI or surgery may be financially impossible. Dog MRIs can cost $2,300 to $5,000 or more, before any treatment that follows.

- Direct-pay options are improving: Most plans are still reimbursement-based, but Trupanion and Pets Best offer vet-direct payment options where the hospital participates and the claim is eligible. That can reduce the cash-flow problem at checkout.

The Cons: The Fine-Print Frustrations

- The reimbursement float: The NAIC says most pet insurance policies pay on a reimbursement basis. In practice, that often means you pay the vet, submit records and invoices, and wait for claim review.

- Premium volatility: Premiums can rise with pet age, location, veterinary inflation, and insurer rate filings. The NAIC Model Act requires disclosure when premiums may increase or coverage may decrease based on claim history, age, or geographic location, where adopted into state law.

- It does not cover everything: Standard accident-and-illness policies generally do not cover routine care unless you add wellness coverage. The NAIC separates accident-only, accident-and-illness, and wellness coverage, and each has different exclusions, limits, deductibles, and reimbursement rules.

The Verdict: The pro is that pet insurance can keep a major bill from becoming a medical decision. The con is that you must tolerate rising premiums, reimbursement mechanics, and policy language that can surprise you if you only read the marketing page.

The "Gotchas": 4 Clauses That Kill Value

If you skim the brochure and skip the fine print, you are gambling, not insuring. The difference between a payout and a denial often hides in four specific clauses.

1. The Pre-Existing Condition Trap (Notes Matter)

This is one of the biggest reasons pet insurance disappoints people. A pre-existing condition is not limited to a formal diagnosis. Under the NAIC Pet Insurance Model Act, prior advice, treatment, or verifiable signs and symptoms can matter before the policy starts or during a waiting period.

The 2026 Shift (Curable vs. Incurable): Some providers distinguish between temporary, curable histories and chronic or incurable conditions, but the timing rules are not identical.

- ASPCA and Spot: ASPCA Pet Health Insurance says some curable pre-existing conditions may be covered after 180 days symptom-free and treatment-free; Spot uses similar curable-condition language. Ligament and knee conditions may be treated differently, so check the policy.

- Embrace: Embrace says temporary pre-existing conditions may become eligible after 12 consecutive months without symptoms or treatment, but chronic conditions remain excluded.

2. The Bilateral Exclusion (The Knee Trap)

"Bilateral" means both sides. If your dog had signs of a left-knee problem before coverage, a future right-knee claim may be treated as related or pre-existing depending on the policy's bilateral-condition language and medical records.

The Trap: This matters because cruciate disease often affects both knees over time. ACVS says 40% to 60% of dogs with cruciate disease in one knee later develop a similar problem in the other knee.

The Waiting Period: Orthopedic waiting periods vary by insurer and state. Spot's sample policy lists a 14-day waiting period for accidents, illnesses, and knee or ligament conditions. Embrace lists a six-month orthopedic waiting period for dogs that may be reduced with an orthopedic exam, where available. Always check the sample policy for cruciate, knee, hip, and orthopedic language.

3. The Dental Gap

Dental disease is common, but coverage is spotty. You must distinguish between dental accidents and dental illness.

- Accidents: Many plans cover eligible dental trauma, such as a tooth broken in an accident.

- Illness: Periodontal disease, gingivitis, extractions, and oral disease may be excluded, capped, or subject to maintenance requirements. Pets Best, for example, describes separate rules for dental accidents and dental illness. Read the dental section before assuming extractions are covered.

4. The Wellness Plan Math Test

Wellness or preventive-care riders cover predictable items such as vaccines, checkups, routine tests, flea and tick prevention, or dental cleanings. They are usually capped-benefit budgeting tools, not catastrophic insurance.

The Reality: If you pay $25/month ($300/year) for wellness benefits and realistically use $220 of eligible reimbursement, you lose money. If you use $380 of benefits and the plan reimburses those categories, you may come out ahead.

The Caps: Many wellness plans cap payouts by item. Pets Best's routine-care examples show scheduled benefit amounts for specific preventive categories, which is why you have to compare annual premium against the exact benefits you expect to use.

Verdict: Use insurance for the big, unpredictable stuff. Treat wellness as a budgeting add-on that has to prove itself line by line.

Expert Insights: The 2026 Market Landscape

You can read a dozen "Top 10" lists, but they often miss the structural changes behind the scenes. The 2026 market is shaped by regulation, consolidation, and still-low adoption.

The "Big Three" Market Updates

-

The California Transparency Shift (SB 1217): California's Senate Bill 1217 strengthens pet-insurance disclosure rules in California. It is not automatically a national standard, but large national carriers may adapt some disclosures across states.

- The Change: California rules require clearer disclosures around rating factors and policy terms, including age-related pricing and other factors that can affect premiums.

- The Win: The law also separates pet insurance from wellness programs, reducing confusion between accident-and-illness coverage and routine-care benefits.

-

The "Illusion of Choice" (Consolidation): Different logos do not always mean completely separate ownership, administration, or risk structure.

- The Reality: Pets Best joined Independence Pet Holdings, and Independence Pet Holdings acquired Spot Pet Insurance. ASPCA Pet Health Insurance is a licensed program relationship, not the same thing as the ASPCA charity directly underwriting policies.

- Why It Matters: Do not choose based only on brand name. Compare sample policies, underwriters, waiting periods, dental rules, bilateral-condition language, direct-pay options, and claims requirements.

-

The Low-Penetration Stat: Despite the hype, pet insurance remains a niche product.

- The Stat: NAPHIA reported 7.03 million insured pets across North America at year-end 2024, including 6,405,541 insured pets in the U.S. U.S. penetration was 5.46% for dogs and 2.04% for cats.

- The Takeaway: The market is growing quickly but is still young. Low adoption means many owners still pay out of pocket, use credit, decline care, or rely on savings when large bills hit.

Strategic Advice: How to Play the Game in 2026

Your strategy must match your pet's life stage. One size does not fit all.

1. The Puppy or Kitten Strategy (The Clean Slate)

The Goal: Lock in coverage before health problems pile up in the medical record.

The Tactic: Enroll early, but do not delay vaccines, exams, parasite prevention, or needed care just to buy insurance first.

Why: Under the NAIC Model Act, prior advice, treatment, or verifiable signs and symptoms can matter for pre-existing-condition review. A minor note about itching, limping, vomiting, or urinary signs can become relevant later.

2. The Rescue Strategy (Curable-Condition Clauses)

The Goal: Insure a pet with some history without assuming every old issue is covered.

The Tactic: Compare providers that publish curable-condition language, such as ASPCA Pet Health Insurance, Spot, or Embrace.

Why: A rescue pet may have a chart note for a past ear infection, cough, parasite, or GI episode. Curable-condition clauses may allow some issues to become eligible again after a symptom-free and treatment-free period, but the period and exceptions vary by insurer.

3. The Big Dog Strategy

The Goal: Avoid buying a policy that runs out before the expensive part of care begins.

The Tactic: For Labs, Goldens, Rottweilers, Great Danes, and other large or active dogs, compare high or unlimited annual limits before optimizing for the cheapest premium.

Why: ACVS says 40% to 60% of dogs with cruciate disease in one knee later develop a similar problem in the other. A low annual limit can leave you exposed if two major orthopedic bills land close together.

Conclusion: The Final Verdict

So, is pet insurance worth it in 2026? If you look at it strictly as an investment, the answer is likely no. If your pet lives a long, healthy life and only visits the vet for annual shots, you will probably lose money on premiums. And that is the best-case scenario.

Because the alternative, "winning" at pet insurance, means your pet has suffered a serious illness or injury. You do not buy coverage because you want a claim. You buy it because a claim is the moment you least want money to decide what care is possible.

In a market where veterinarian services are still rising faster than overall inflation and a single specialty surgery can reach five figures, pet insurance is less about saving on the bills you expect and more about protecting yourself from the bills you cannot comfortably absorb.

Your Next Move: Before you click "buy" on a policy, audit your pet's medical records. Request the full history from your vet. Read it yourself. If there is a note about itchy skin, limping, vomiting, urinary signs, or a prior injury, ask the insurer how that history would be handled. Understanding your pet's risk profile on paper is the best defense against a surprise exclusion later.

Ultimately, pet insurance is about optionality. When the worst happens, the goal is to make decisions from prognosis and quality of life, not from panic over the invoice.

Frequently Asked Questions (FAQs)

Is pet insurance actually worth it in 2026?

If your pet stays healthy, you will likely lose money on premiums, and that is the best-case scenario. Pet insurance is not an investment; it is a hedge against catastrophe. It becomes "worth it" when an eligible $5,000 to $10,000 bill would otherwise force you into debt or a painful care decision.

How much does pet insurance cost on average?

The latest public NAPHIA benchmark uses 2024 U.S. accident-and-illness policies: $749.29 per year for dogs and $386.47 per year for cats, or about $62/month for dogs and $32/month for cats. Your quote can be much higher or lower depending on breed, age, ZIP code, deductible, reimbursement rate, and annual limit.

Does pet insurance cover pre-existing conditions?

Generally, no. Prior advice, treatment, or verifiable signs and symptoms can matter under the NAIC Model Act. Some insurers distinguish between curable and incurable histories, but the waiting period and exceptions vary. ASPCA and Spot use 180-day curable-condition language for some conditions; Embrace uses 12 consecutive months for temporary pre-existing conditions.

Why shouldn't I just put $50 a month into a savings account?

Because you need liquidity speed, not just accumulation. If you save $50/month, you will have $300 after six months and $600 after a year. If your dog needs a $5,000 eligible surgery in month six, insurance may help after deductible, coinsurance, limits, exclusions, and waiting periods; a brand-new savings account will not.

Is pet insurance worth it for senior dogs (8+ years old)?

It can be, but the math is harder. Senior premiums are higher, and conditions that appeared earlier in life are usually excluded as pre-existing. For older dogs, compare quotes against likely exclusions and consider whether the plan still protects you from new cancer, trauma, emergency, or specialty-care claims.

Does pet insurance cover routine vet visits and shots?

Not by default. Standard policies cover accidents and illnesses. Wellness add-ons can help with vaccines, exams, and preventive care, but they are usually capped-benefit budgeting tools. Compare the annual wellness premium with the exact reimbursements you expect to use.

Does pet insurance cover dental work?

It depends on the dental issue and policy. Many plans cover eligible dental accidents. Dental illness, periodontal disease, cleanings, and extractions vary widely and may be excluded, capped, or subject to annual dental exam requirements. Read the dental section before buying.

What is the bilateral exclusion?

A bilateral clause affects paired body parts, such as knees, hips, eyes, or elbows. If one side had symptoms before coverage started, a later claim on the other side may be treated as related or pre-existing depending on the policy language and medical records.

Do I have to pay the vet upfront?

Usually, yes. The NAIC says most pet insurance policies pay on a reimbursement basis. Some insurers, including Trupanion and Pets Best, offer vet-direct payment options at participating hospitals for eligible claims.

Why did my premium go up if I didn't file a claim?

Premiums can change because of pet age, location, local veterinary costs, coverage choices, and insurer rate filings, not just your individual claim history. Read the renewal and rating-factor language before buying so a future increase is not a surprise.

WhiskerCover is reader-supported. When you click on links to pet insurance partners on our site and purchase a policy, we may earn a commission at no extra cost to you. Learn more about how we make money.

Sources

- Bureau of Labor Statistics CPI News Release, April 2026

- NAPHIA 2025 State of the Industry Report

- NAPHIA 2025 Report Highlights PDF

- NAIC Pet Insurance Overview

- NAIC Pet Insurance Model Act

- NAIC Regulator's Guide to Pet Insurance

- AAHA Insights on Pet Insurance in 2025

- AAHA Corporate Consolidation and Private Equity Overview

- FTC Veterinary Services Consolidation Enforcement Action

- Gallup / PetSmart Charities State of Pet Care Study

- Federal Reserve $400 Emergency Expense Data

- American College of Veterinary Surgeons: Cranial Cruciate Ligament Disease

- Lemonade TPLO Surgery Cost Guide

- PetMD Dog MRI Cost Guide

- Cornell Riney Canine Health Center: BOAS

- Merck Veterinary Manual: Hip Dysplasia in Dogs

- Forbes Advisor Pet Insurance Statistics

- Forbes Advisor Is Pet Insurance Worth It?

- Cornell Feline Health Center: Feline Lower Urinary Tract Disease

- PetPlace Cat Urinary Blockage Treatment Cost

- Cornell Feline Health Center: Chronic Kidney Disease

- Trupanion Deductibles

- Trupanion Vet Direct Pay

- Pets Best Vet Direct Pay

- ASPCA Pet Health Insurance Pre-Existing Conditions

- Spot Pre-Existing Conditions

- Spot Sample Policy

- Embrace Pre-Existing Conditions

- Embrace Orthopedic Waiting Period

- Pets Best Dental Coverage

- Pets Best Routine Care

- California SB 1217

- Pets Best Joins Independence Pet Holdings

- Independence Pet Holdings Acquires Spot Pet Insurance

- ASPCA Pet Health Insurance Partnership

- Independence Pet Group Acquisition of Felix