Let’s be honest: the days of the $50 vet visit are gone.

If you're looking for breed-specific advice, check out our guides to the best dog insurance and Cat Insurance.

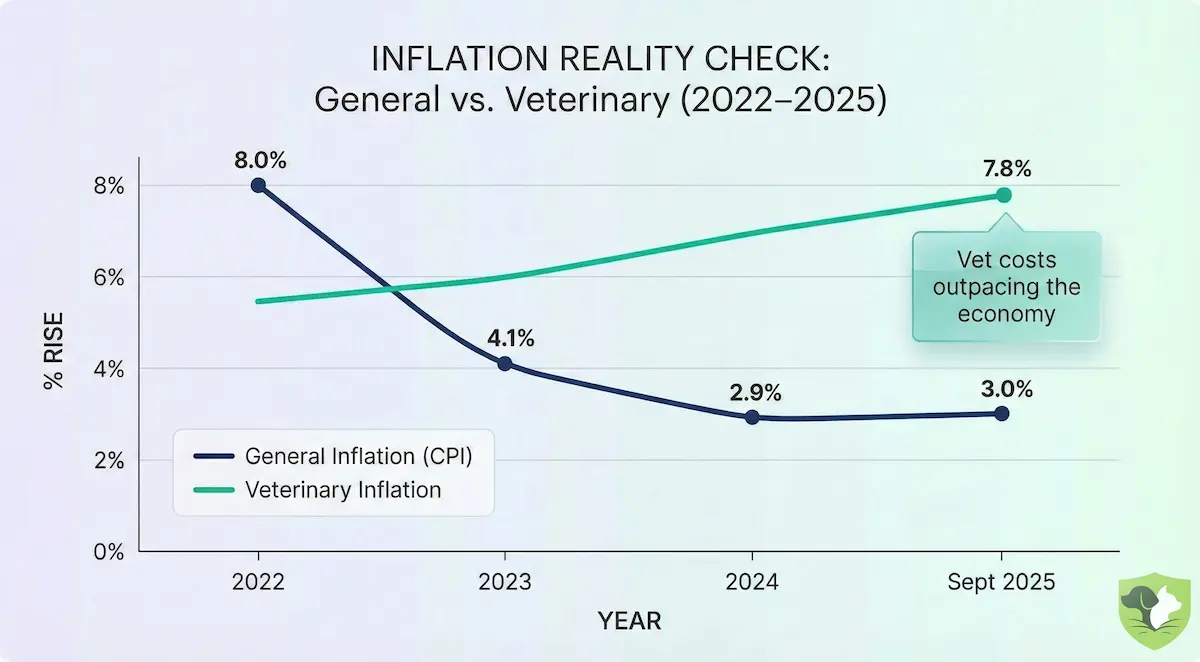

Veterinary care has continued getting more expensive. Recent BLS CPI data shows veterinarian services up 5.6% year over year, while broader pet services rose 7.8%. A standard dog knee surgery can reach $10,000, making emergency care a serious financial burden.

In 2026, pet insurance isn't just a "nice-to-have" for anxious pet parents; it is a critical financial safety net. But finding the right plan is harder than ever.

Table of Contents

- The Market's "Illusion of Choice"

- Quick Look: The Top Providers by Category (2026)

- Deep Dive: The Top 5 Companies Reviewed

- Expert Insights: The "Hidden Mechanics" of 2026 Policies

- The Economics of Pet Ownership in 2026

- How to Choose Based on Your Pet’s Life Stage

- Final Verdict: Is Pet Insurance Worth It in 2026?

- Frequently Asked Questions (FAQs)

The Market's "Illusion of Choice"

The market is filled with the 'illusion of choice.' Pets Best and Spot are part of Independence Pet Holdings’ pet-insurance portfolio, and ASPCA Pet Health Insurance is also associated with IPH’s pet-insurance brand portfolio through a licensed program structure. While their websites look different, their corporate or administrative ties can overlap.

IPH says its carrier-solutions business features the AM Best A- (Excellent) rated Independence American Insurance Company, which provides risk management, actuarial, and underwriting services to the pet insurance industry.

Corporate overlap does not mean the policies are identical. Shared ownership or administration can create overlap in claim operations, underwriting relationships, or back-end administration, but each brand’s policy terms, underwriter, exclusions, reimbursement rules, and state filings can still differ.

To see which plans truly deliver (beyond just marketing), we analyzed 2026 regulatory filings, actuarial data, and new transparency rules from California’s Senate Bill 1217.

Quick Look: The Top Providers by Category (2026)

If you're doom-scrolling and just need the highlights, here is the cheat sheet. We categorized these based on your pet's specific risk profile, focusing on medical history and breed-associated issues.

| Category | Top Pick | Why We Chose It |

|---|---|---|

| Total Peace of Mind | Trupanion | Trupanion is the standout for real-time vet-direct payment at checkout, where available through participating veterinary hospitals. Ideal for Frenchies, Goldens, and breeds with "genetic nightmares" because they have no payout limits. |

| Puppies & Tech Lovers | Lemonade | Fast digital claims; Lemonade says some simple, eligible claims can be handled instantly, but complex claims or missing records may take longer. Perfect for young, healthy pets if you hate paperwork. |

| Rescue & Senior Dogs | Spot | Some insurers have upper enrollment ages that can affect senior pets, while Spot has no upper age limit for new enrollments, making it useful for senior adoptions. |

| Mobility & Rehab | Pets Best | If your dog needs an eligible wheelchair or prosthetic device later in life, Pets Best can be worth comparing. Great for big dogs prone to hip issues. |

| "Pre-Existing" Histories | ASPCA | Have a rescue with a spotted past? If they’ve been symptom-free for 180 days, ASPCA may cover their "curable" conditions again. |

Deep Dive: The Top 5 Companies Reviewed

We analyzed policy documents and 2026 market data to break down the leading providers. Instead of a generic ranking, we evaluated each carrier based on its specific underwriting strengths and potential drawbacks for different types of pet owners.

1. Trupanion: The Medical-Grade Standard

Why it’s here: Trupanion operates differently from traditional property insurers, functioning closer to a human medical benefits provider. Their integration with veterinary practice software enables "Vet Direct Pay," allowing participating veterinary hospitals to be paid directly at checkout for eligible claims. This can reduce or eliminate the need to float thousands of dollars on a credit card while waiting for reimbursement.

- The "Lifetime Per-Condition" Deductible: Unlike annual deductibles that reset every year, Trupanion charges a deductible once per specific condition for the life of the pet. If your dog develops chronic allergies at age two, you pay the deductible once, and eligible future treatments for that condition are covered at 90% for life.

- Unlimited Payouts: There are no annual, per-incident, or lifetime caps on coverage, which is mathematically critical for breeds prone to costly surgeries, such as French Bulldogs and Great Danes.

- Considerations: The premium cost can be high for some breeds, locations, and enrollment ages. However, this higher premium can be viewed as an investment in peace of mind, particularly for those who prioritize comprehensive coverage. While Trupanion doesn't cover veterinary exam fees for sick visits, which can add $50 to $150 per incident to your out-of-pocket costs, its unique payment structure and coverage options provide significant value for owners who wish to mitigate high veterinary expenses long-term.

Best For: Owners of purebreds with known genetic risks and those who prioritize financial peace of mind over monthly cash flow.

2. Lemonade: The Digital Disruptor

Why it’s here: Lemonade has captured the market for tech-savvy owners by leveraging artificial intelligence to drive down operating costs and increase speed. Their "AI Jim" system can handle some simple, eligible, well-documented claims almost instantly. That does not mean every pet claim is paid in seconds; medical-record review, pre-existing-condition checks, invoices, and claim complexity can slow the process.

- The "A La Carte" Model: Base policies are stripped down to keep entry prices low. Lemonade advertises pet insurance starting at $10/month, but real quotes can exceed $20/month, especially for dogs, older pets, higher annual limits, and higher-cost ZIP codes. Essential coverages like vet exam fees, physical therapy, and dental illness must be added as separate "riders" or add-ons.

- Considerations: The automated claims process still depends on documentation. Fast digital claims do not mean medical-history review disappears; insurers can still request records, review prior symptoms, and delay or deny claims if records are missing or suggest a pre-existing condition. Before recommending Lemonade for a senior pet, check eligibility directly because upper enrollment rules may vary by pet, breed, and location.

Best For: Owners of puppies and kittens with no prior medical history who want a fast, mobile-first experience.

3. Spot Pet Insurance: The Flexible Powerhouse

Why it’s here: Spot addresses two major pain points in the 2026 market: age limits and orthopedic waiting periods. Unlike many competitors, Spot has no upper age limit for new enrollments, making it one of the few viable options for adopting senior pets.

- The Orthopedic Edge: Cruciate ligament waiting periods vary widely by insurer and state; some are extended, while others are much shorter. Spot’s sample policy lists a 14-day waiting period for ligament and knee conditions, which can be useful for active breeds prone to CCL injuries. Labradors are a higher-risk breed for cranial cruciate ligament rupture; one University of Wisconsin School of Veterinary Medicine source estimates that about 5%–10% of Labradors may experience a cruciate ligament rupture during their lifetime.

- Customizable Limits: You can choose an "Unlimited" annual limit plan, though premiums for these comprehensive policies can be high.

- Considerations: While flexible, the "Unlimited" plans are often priced at the top of the market.

Best For: Senior dog adoptions and active breeds (such as Labradors and Rottweilers) at high risk of knee injuries.

4. ASPCA Pet Health Insurance: The Compassionate Choice

Why it’s here: ASPCA’s insurance is recognized for its fair stance on pre-existing conditions, providing second chances where many competitors do not.

- Curable Conditions Clause: While "incurable" pre-existing conditions like diabetes are typically excluded, "curable" conditions like ear infections, UTIs, or kennel cough can be re-covered if the pet remains symptom-free and treatment-free for 180 days.

- Horse Coverage: ASPCA Pet Health Insurance also offers horse insurance, which can matter for households with horses as well as cats or dogs.

- The Downside: ASPCA Pet Health Insurance does not offer the same real-time checkout payment structure that Trupanion markets through participating veterinary hospitals.

Best For: Rescue pets with minor medical histories that need a policy that forgives past, resolved issues.

5. Pets Best: The Mobility Specialist

Why it’s here: Following its acquisition by Independence Pet Holdings, Pets Best still highlights mobility support in its coverage materials.

- Mobility Coverage: Their policies specifically cover prosthetic devices and wheelchairs. Coverage details for mobility devices vary by insurer, so this is worth checking for aging large breeds.

- Direct Pay Option: Like Trupanion, they offer a "Vet Direct Pay" solution to reimburse veterinarians directly, reducing your upfront burden.

- The Downside: Recent customer reviews and complaints include reports of claim delays, phone wait times, and service frustration, although experiences are mixed. Premium changes can also vary by state, pet age, breed, local veterinary costs, and policy design.

Best For: Breeds prone to hip dysplasia, spinal issues, or those likely to need mobility assistance in their senior years.

Expert Insights: The "Hidden Mechanics" of 2026 Policies

The fine print in pet insurance contracts determines if your claims get paid—but most reviews stop at premiums. We analyzed the exact exclusionary clauses in contracts, uncovering the hidden mechanics that frequently catch owners off guard.

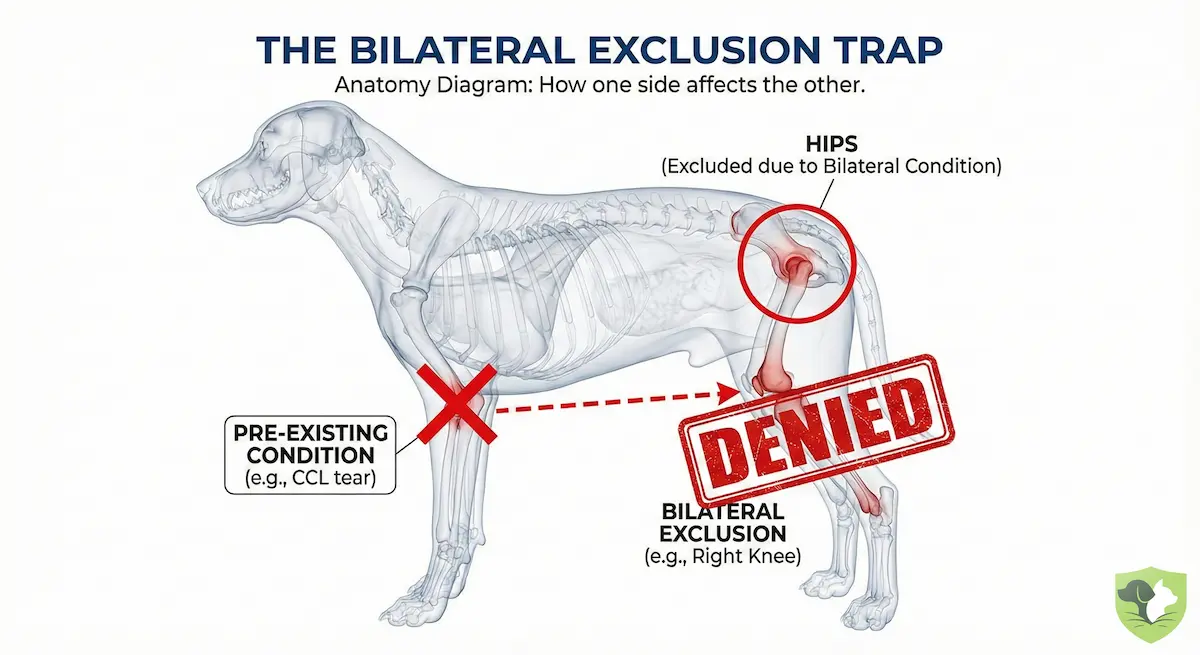

The "Bilateral Exclusion" Trap

Missing or incomplete medical records are a major source of claim delays and can contribute to pre-existing-condition disputes, especially for expensive orthopedic claims.

How it works: A "bilateral" condition affects paired body parts, such as the knees (cruciate ligaments) or the hips. If your dog shows signs of a limp on their left leg before getting insurance, some policies may treat a later right-leg claim as related or pre-existing, depending on the policy’s bilateral-condition language and medical records.

The Risk: For breeds like Labradors or Rottweilers, a torn ACL in one knee significantly increases the statistical probability of tearing the other. A bilateral exclusion means you could be on the hook for a $6,000–$8,000 surgery down the road.

The Solution: AKC Pet Insurance may offer limited coverage for some pre-existing conditions after 365 days of continuous coverage, where available and subject to policy terms. MetLife may cover a condition on the opposite side of the body only if that condition was not pre-existing under the policy terms. Check the bilateral-condition and pre-existing-condition language in the sample policy.

Curable vs. Incurable: The "Clean Slate" Clause

Historically, a "pre-existing condition" could follow your pet for the life of the policy. In 2026, some policies distinguish between incurable and curable histories.

- Incurable: Conditions like diabetes, hip dysplasia, and cancer are typically excluded if symptoms appear before enrollment.

- Curable: Episodic issues like kennel cough, ear infections, or urinary tract infections (UTIs) can often be covered again.

How to Leverage It: Providers like ASPCA, Spot, and Hartville will reinstate coverage for these conditions if your pet remains symptom-free and treatment-free for 180 days.

Pro Tip: The burden of proof is on you. You should ask your vet to document a "resolution" or "clean bill of health" in your records so the claim file clearly shows when a curable issue ended.

The "Transparency" Shift: Impact of California SB 1217

Even if you don't live in California, the state's implementation of Senate Bill 1217 is worth watching because national carriers may adapt disclosures across multiple states. This law adds disclosure rules around the math behind your bill.

Rate Hike Realities: In California, pet insurers must provide clearer disclosures about rating factors such as age-banding and veterinary-cost changes. This helps policyholders understand whether a renewal increase is tied to rating factors rather than a single claim.

The Wellness Split: Under California’s new rules, "Wellness Plans" (for vaccines/checkups) are treated distinctly from "Insurance" (for accidents/illness). Why does this matter? It makes bundled pricing easier to evaluate. You can more clearly compare the annual wellness premium with the capped benefits you realistically expect to use, such as vaccines, annual exams, fecal tests, heartworm tests, dental cleaning, or preventive medication.

The Economics of Pet Ownership in 2026

Let’s face it—veterinary care now means costs rivaling a second mortgage, not just pricier kibble. It’s not just that prices are up (though they are); it’s that the standard of care has changed. In 2026, specialty practices may use MRIs, CT scans, and complex oncology protocols that were once far less common in pet care. That better care saves lives, but it wreaks havoc on your bank account.

Case Study: The $20,000 Knee (Yes, Really)

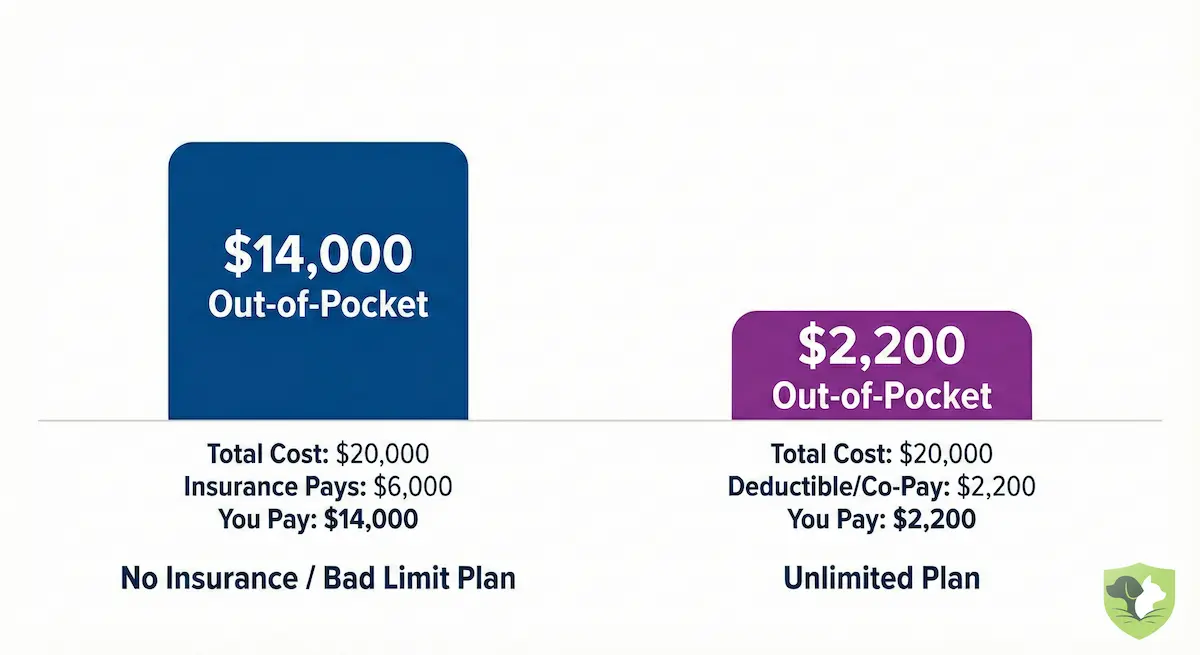

To understand why "Unlimited" payouts matter, let’s look at a costly orthopedic scenario for large dogs: the Cranial Cruciate Ligament (CCL) rupture. Think of it as an ACL tear for dogs. Here is an example for a 3-year-old Rottweiler with eligible TPLO-related bills:

Example only: if eligible TPLO-related bills total $20,000, a plan with a $5,000 annual limit could still leave roughly $15,000 before deductible, coinsurance, exclusions, and non-covered fees. A plan with unlimited annual coverage, 90% reimbursement, and a $250 deductible could leave roughly $2,225, assuming the claim is eligible and all charges are covered.

This is a simplified illustration, not a quote or guarantee. Actual reimbursement depends on the policy’s annual limit, deductible, reimbursement rate, exam-fee coverage, rehab coverage, waiting periods, bilateral-condition rules, pre-existing-condition review, and state-specific policy terms.

The Insurance Reality Check:

The point is not that every TPLO claim will look like this. The point is that annual limits, deductibles, reimbursement percentages, and exclusions can change the owner’s share by thousands of dollars.

The Takeaway: For big dogs, an "Unlimited" plan can be worth pricing against cheaper plans with lower annual limits, especially if orthopedic or specialty-care risk is high.

Case Study: The Cat Bills Owners Forget to Budget For

Orthopedic emergencies grab the headlines, but cats run up their own five-figure risks. Feline lower urinary tract disease (FLUTD) is a common example: a urinary blockage is a true emergency, and PetPlace estimates a three-day blockage case at about $1,425 to $4,000. Layer in chronic conditions like kidney disease, hyperthyroidism, or diabetes that need years of monitoring, and a high-limit or unlimited plan can matter just as much for a cat as for a big dog.

The "Loyalty Penalty" (Why Rates Hike)

Have you ever noticed that your streaming service gets more expensive the longer you keep it? Pet insurance often does the same, but with higher stakes. This is called the "Loyalty Penalty." One Forbes Advisor age-rating dataset shows that the age factor for a 7-year-old dog was 71% above the base rate used for ages 1 and 2.

The "Lock-In" Effect: As your pet ages, they may develop minor health issues. If you try to switch insurance companies to find a cheaper rate, those issues are flagged as "pre-existing conditions" and excluded by the new carrier. That can make switching difficult.

The "Bait and Switch": Premiums can rise at renewal as pets age and local veterinary costs increase. The exact change depends on the insurer, state, pet age, breed, local veterinary inflation, and policy design.

Who Avoids This? Trupanion says it does not raise rates based on your pet's birthday and instead prices around broader veterinary-cost factors. This can make them more expensive on Day 1, but worth comparing for owners who care most about long-term pricing rules and no payout limits.

How to Choose Based on Your Pet’s Life Stage

One-size-fits-all advice is the enemy of good insurance. A bubbly 10-week-old Golden Retriever needs a completely different strategy than a 12-year-old rescue mix with "mystery" stiff hips. Here is how to play your hand based on where your pet is in life.

The "Puppy Strategy" (Ages 0–1)

The Goal: Beat the medical record. The Strategy: You want to enroll your puppy as early as practical, ideally before symptoms or diagnoses appear in the medical record. Why? Because a vet note such as "noted slight limp" or "scratching ears" can become a pre-existing-condition issue later, depending on the policy and whether the condition is curable.

The Play:

- Lemonade can be competitively priced for some young, healthy pets, especially if you choose lower limits or fewer add-ons.

- MetLife can be worth comparing if you adopt littermates and want a policy structure built for multiple pets.

The "Genetic Time Bomb" (Purebreds)

The Goal: Maximum liability protection. The Strategy: If you own a French Bulldog, Bernese Mountain Dog, or Doberman, breed-associated health risks should shape your coverage choice. Frenchies, for example, are known for spinal and allergy risks that can become expensive over a lifetime.

The Play:

- Trupanion is the gold standard here. Their "Lifetime Per-Condition Deductible" means that once you pay the deductible for an eligible chronic breed issue (like allergies), you do not pay that condition deductible again.

- Plus, their direct pay feature can reduce the amount you need to put on a credit card when a participating hospital and eligible claim are involved.

The "Senior Rescue" (Ages 6+)

The Goal: Just getting approved. The Strategy: This is the hardest category. Some insurers have upper enrollment ages that can affect senior pets, while others advertise no upper age limit. You need a provider with senior-pet eligibility that fits your dog’s age, medical history, and budget.

The Play:

- Spot and Pets Best are strong options to compare here. Neither carrier imposes an upper age limit for new enrollments.

- Pro Tip: If your senior rescue has a history of minor issues (like ear infections), look at ASPCA or Spot. Their "curable" condition clauses allow coverage to kick in for those old issues after a 180-day symptom-free period.

Final Verdict: Is Pet Insurance Worth It in 2026?

Real talk: If you have $20,000 sitting in a savings account specifically labeled "Major Orthopedic Surgery," you may not need pet insurance. For many other pet owners, it is worth serious consideration.

The math has changed. With BLS data showing veterinarian services up 5.6% year over year and broader pet services up 7.8%, and standard emergency surgeries costing as much as a used sedan, the financial risk is hard to ignore. For many owners, pet insurance is less about "saving money" on an annual vet visit and more about reducing the risk that a large emergency bill drives a painful care decision.

The "One Thing" You Must Do: Before you buy any policy, audit your pet's medical records. Read every note your vet has ever written. If there is a mention of "itching" from three years ago, that could become part of a pre-existing-condition review for a future allergy claim. Know what you are buying so you aren't blindsided by a denial later.

Our Final Advice:

- Scrutinize the "Wellness" Plans: Wellness plans are usually budgeting tools, not true insurance. Compare the annual wellness premium with the exact capped benefits you realistically expect to use, such as vaccines, annual exams, fecal tests, heartworm tests, dental cleaning, or preventive medication.

- Don't Wait: Insurance works best when you don't need it. The longer you wait, the more "pre-existing conditions" your pet may accumulate, which can create exclusions under a new policy.

Frequently Asked Questions (FAQs)

Does pet insurance cover pre-existing conditions?

Generally, no. If your pet showed symptoms before the policy started, it is typically excluded. However, some policies distinguish between incurable and curable histories. Incurable: Conditions such as diabetes or arthritis are usually incurable. One notable exception is AKC Pet Insurance, which may cover some pre-existing conditions after 365 days of continuous coverage, where available and subject to policy terms. Curable: Companies like ASPCA and Spot have a "curable" clause. If your pet is symptom-free and treatment-free for 180 days, they may reinstate coverage for episodic issues such as ear infections or kennel cough.

How do I decide between two similar plans if my pet fits multiple risk categories?

If you are stuck between two quotes that look identical, look at the deductible structure and the underwriter. The Tie-Breaker: If you have a breed prone to chronic issues (like allergies), choose a Lifetime Per-Condition Deductible (Trupanion). You pay the condition deductible once for eligible treatment and do not pay that same condition deductible again. For clumsy pets prone to random accidents, an Annual Deductible (Lemonade, Spot, Pets Best) can be easier to compare because it caps your deductible exposure for the year. The "Hidden" Parent: Be aware of the "illusion of choice." Pets Best, Spot, and ASPCA Pet Health Insurance have overlapping corporate or administrative ties through Independence Pet Holdings, but they are not identical products. If you are splitting hairs between them, compare each brand’s sample policy, underwriter, exclusions, waiting periods, and reimbursement rules.

What is the waiting period for knee injuries (ACL/CCL)?

This is the "gotcha" clause. Cruciate ligament waiting periods vary widely by insurer and state; some are extended, while others are much shorter. Spot lists a 14-day waiting period for ligament and knee conditions in its sample policy, while other insurers may use longer orthopedic or cruciate waiting periods. Always check the sample policy for cruciate, knee, hip, and orthopedic language.

Why did my premium go up?

It is usually a mix of inflation, aging, location, breed, and policy design. Recent BLS data shows veterinarian services up 5.6% year over year, while pet services rose 7.8%. Insurers may pass some of those costs through to policyholders. Plus, as your pet gets older, they are statistically more likely to get sick, so premiums can rise; one Forbes Advisor age-rating dataset shows a 7-year-old dog age factor 71% above the base rate used for ages 1 and 2.

Are there ways to lower premiums without sacrificing essential coverage?

Yes, but be careful not to strip away the catastrophic protection you actually need. Tweak the Deductible: Raising your deductible from $250 to $500 or $750 is often a straightforward way to lower your monthly premium. Check the "Wellness" Rider: Wellness add-ons are capped-benefit budgeting tools. Compare the annual premium with the exact benefits you expect to use before adding one. The "Nuclear" Option: If a full policy is out of budget, consider an Accident-Only plan. It won't cover cancer or illness, but it can help with eligible accident claims.

What documentation do I need to ensure my claims are approved?

Missing paperwork is one of the most avoidable claim problems. Fast digital claims do not mean medical-history review disappears; insurers can still request records, review prior symptoms, and delay or deny claims if records are missing or suggest a pre-existing condition. The "Golden Record": Many insurers may request roughly 12–24 months of medical history, but exact record requirements vary by insurer, pet age, claim type, and state. Some claims may require more complete records. The Pro Move: Do not wait for an emergency. Ask whether the insurer offers a "Medical History Review" or similar underwriting review after purchase. This can help surface potential pre-existing-condition exclusions earlier, before a major claim is pending.

Is a wellness plan worth it?

Wellness plans are usually budgeting tools, not true insurance. To test whether one makes sense, compare the annual wellness premium with the exact capped benefits you realistically expect to use, such as vaccines, annual exams, fecal tests, heartworm tests, dental cleaning, or preventive medication. Example only: if a wellness add-on costs $300 per year but you only use $220 of eligible benefits, you lose money. If you use $380 of eligible benefits and the plan reimburses those categories, you may come out ahead.

WhiskerCover is reader-supported. When you click on links to pet insurance partners on our site and purchase a policy, we may earn a commission at no extra cost to you. Learn more about how we make money.

Sources

- Bureau of Labor Statistics CPI Table 7

- NAPHIA Industry Data

- NAPHIA 2025 State of the Industry Report

- California SB 1217

- Independence Pet Holdings

- Pets Best Joins Independence Pet Holdings

- Independence Pet Holdings Acquires Spot Pet Insurance

- ASPCA Pet Health Insurance Partnership

- Trupanion VetDirect Pay

- Trupanion Claims

- Trupanion Payouts

- Trupanion Deductibles

- Trupanion Pricing Promise

- Lemonade Pet Insurance

- Lemonade Pet Insurance Cost

- Lemonade Form 10-K

- Lemonade Pet Medical Records

- Lemonade Pet-Insurance Optimized Medical Records

- Lemonade Pet Add-Ons

- Lemonade Preventative Care Options

- Lemonade TPLO Surgery Cost

- Spot Pet Insurance Enrollment Age

- Spot Sample Policy

- Spot Pre-Existing Conditions

- Spot Underwriting

- ASPCA Pet Health Insurance Pre-Existing Conditions

- ASPCA Pet Health Insurance Coverage

- ASPCA Pet Health Insurance Preventive Care

- ASPCA Pet Health Insurance Horse Insurance

- Pets Best Coverage

- Pets Best Vet Direct Pay

- Pets Best FAQ

- Pets Best Routine Care

- Pets Best Sample Policy

- Embrace Orthopedic Waiting Period

- Pumpkin Pet Insurance FAQs

- AKC Pet Insurance Pre-Existing Conditions

- MetLife Pre-Existing Conditions

- MetLife Bilateral Conditions

- American College of Veterinary Surgeons CCL Disease

- Forbes Advisor Pet Insurance Age Rating Factors

- Trustpilot Pets Best Reviews

- BBB Pets Best Complaints

You may be interested...

More published guides that build on this topic.

Best

Best

Best Pet Insurance for Large Dogs (2026): Picks by Breed and Risk

Large dogs face $5,000–$15,000 orthopedic and bloat bills. We rank insurers on what matters for big breeds — orthopedic waits, annual limits, and direct pay.

Best

Best

Best Cheap Pet Insurance Plans in 2026: Real Protection on a Budget

Find the cheapest pet insurance that still gives real protection in 2026. Learn which budget plans pay out, how to tune deductibles, and what red flags to avoid.