Accident & illness (A&I) insurance is the standard, comprehensive tier of pet insurance — it reimburses you for both injuries (broken bones, swallowed objects, bite wounds) and illnesses (from ear infections to cancer), while excluding pre-existing conditions and routine care. It's the broader, costlier alternative to accident-only coverage, which never pays for illness.

Choosing a coverage tier shouldn't feel like a gamble on your pet's future — so here's the plain version, with no brand pitch.

Here's what you'll learn:

- Exactly what A&I covers — and what it never will, including the pre-existing rule that trips up most first-time buyers

- What "80% reimbursement" actually pays once the deductible and eligible-charge math is done

- What it costs, and whether A&I, accident-only, or neither is the right call for your pet

Table of Contents

- Accident-only vs accident & illness vs wellness: the three types

- What accident & illness insurance covers

- What it doesn't cover

- What "80% reimbursement" really means

- How much does accident & illness insurance cost?

- Waiting periods and why you can't buy it after the accident

- Is accident & illness insurance worth it — and who should buy it?

- Frequently Asked Questions

- Sources

Accident-only vs accident & illness vs wellness: the three types

Pet insurance comes in tiers, and the search results constantly blur them. Here's the plain version of what you're actually choosing between:

- Accident-only — covers injuries from mishaps (broken bones, swallowed objects, bite wounds) and nothing else. No illness, ever. It's the cheapest tier.

- Accident & illness (A&I) — the comprehensive standard: injuries plus diseases, from ear infections and allergies to chronic conditions and cancer. When people say "pet insurance," this is usually what they mean.

- Wellness — not insurance at all. Routine care (vaccines, dental cleanings, annual checkups) is sold separately — usually as an optional add-on or standalone wellness plan, not as part of base insurance.

| Tier | What it covers | Avg. monthly premium | Best for |

|---|---|---|---|

| Accident-only | Injuries only — no illness | ~$16 dog / ~$9 cat | Tight budgets; young, low-risk pets |

| Accident & illness | Injuries + illnesses, incl. chronic disease and cancer; not pre-existing or routine care | ~$62 dog / ~$32 cat | Most pets — illness is where the big costs hit |

| Wellness rider (add-on) | Routine care: vaccines, dental cleaning, checkups | An extra fee on top of a base plan | Budgeting predictable annual costs |

Those premiums are 2024 U.S. averages from NAPHIA; your actual quote swings with age, breed, and ZIP. Is accident-only worth it? For a young, healthy pet on a strict budget it's a legitimate floor — but it pays nothing toward an illness — and illness is where the costliest, most common claims land — so the gamble gets riskier as your pet ages. We weigh that trade-off in our accident-only guide. And the conflation that trips up nearly everyone: routine care is a rider, not insurance — buying A&I does not cover annual checkups unless you add the wellness option.

What accident & illness insurance covers

A&I is broad, but "comprehensive" doesn't mean unlimited or all-inclusive. Here's the typical scope — always confirm the specifics against a carrier's sample policy, because the exact wording varies.

Accidents

Sudden injuries: broken bones, lacerations and bite wounds, foreign-body ingestion (the swallowed sock or toy), and toxicities like chocolate, antifreeze, or xylitol. One wrinkle — whether a swallowed object is filed as an "accident" or an "illness" can differ by carrier. It rarely changes whether it's covered, but it can change which waiting period or deductible applies.

Illnesses

This is the half accident-only skips: infections (ear, skin, urinary), gastrointestinal problems, allergies, chronic conditions such as diabetes, arthritis, and thyroid disease, and cancer — diagnostics through treatment. For most pets, this is where the lifetime claim dollars actually go.

Hereditary and breed-related conditions

Most A&I plans also cover hereditary and congenital conditions — hip and elbow dysplasia, intervertebral disc disease (IVDD), brachycephalic (flat-faced) airway syndrome, patellar luxation — as long as they aren't pre-existing. The catch: carrier language varies, and some apply longer orthopedic waiting periods, so confirm your breed's signature conditions are named as covered before you enroll.

Dental illness

Dental coverage varies a lot: some A&I plans include dental illness (gingivitis, periodontal disease, fractured or infected teeth), often capped and conditional, while others exclude it or require an add-on. Embrace, for example, covers dental illness up to $1,000 per policy year, separate from accidental dental trauma, and routine cleanings aren't covered at all (those need a wellness rider). Many carriers also tie dental coverage to a recent dental exam or healthy-teeth record — read that fine print.

What it doesn't cover

The honest half. Even comprehensive A&I leaves real, predictable gaps:

- Pre-existing conditions — anything your pet showed signs of before coverage began, or during a waiting period. "Signs" is the operative word: insurers work at the symptom level, not the diagnosis level, so a chart note about limping or itching can count even if no condition was ever formally named. (Our pre-existing conditions guide covers the nuances.)

- Routine and wellness care — vaccines, checkups, flea and tick prevention, spay/neuter, routine dental cleanings. These are predictable costs, so they live on a separate wellness rider, not the insurance itself.

- Exam and consultation fees — some carriers reimburse the vet's exam fee, many don't. This one genuinely varies by carrier, so check.

- Cosmetic and elective procedures — tail docking, ear cropping, declawing.

- Breeding and pregnancy — costs tied to breeding, whelping, or queening.

The correction that matters most: buying the illness tier does not unlock pre-existing coverage. That exclusion applies to every tier — accident-only, A&I, and A&I-with-wellness alike. A few carriers will reconsider a curable condition after a long symptom-free stretch, but chronic conditions generally stay excluded — which is why when you enroll matters as much as what you buy.

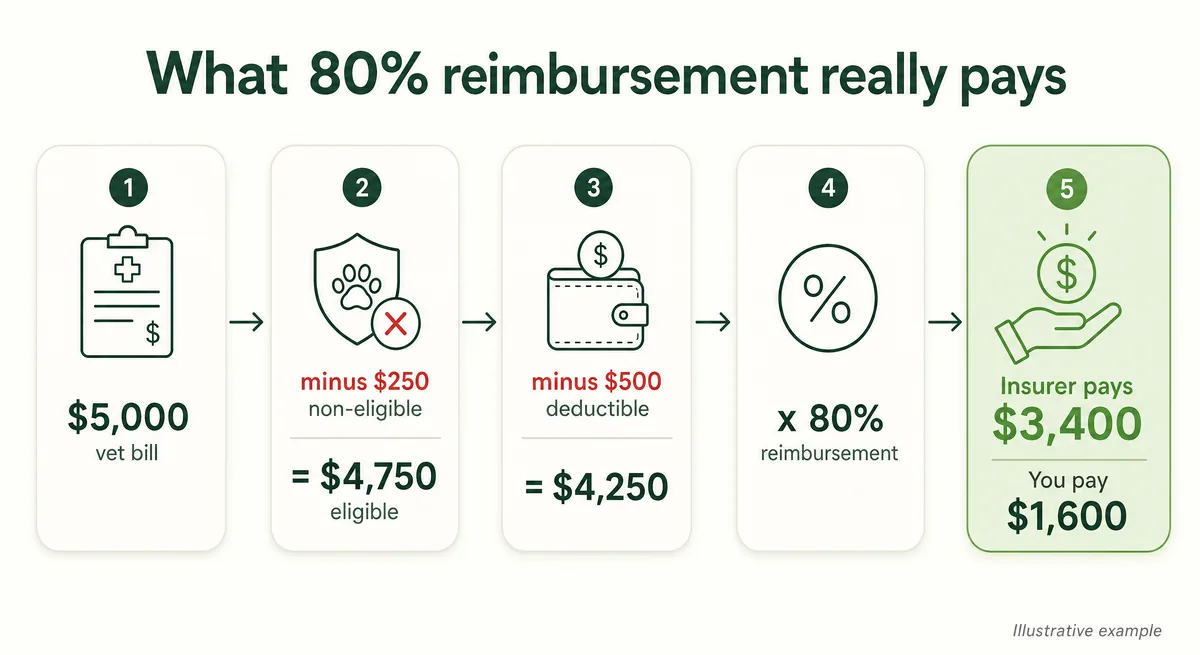

What "80% reimbursement" really means

Here's the number that surprises people: an "80% reimbursement" plan almost never hands back 80% of your vet bill. Reimbursement is calculated on eligible charges — the bill minus anything the policy doesn't cover — and only after your deductible. Walk it through.

Say your dog's treatment costs $5,000. First, strip out non-eligible items — say $250 in exam fees the plan doesn't reimburse — leaving $4,750 in eligible charges. Subtract your annual deductible (the amount you pay each policy year before coverage kicks in), say $500: now $4,250. Apply the 80% reimbursement rate, and the insurer pays $3,400. You're out $1,600 — the $250 exam fee, the $500 deductible, and 20% of the rest. Not the $1,000 that "80% off" implies.

The math swings the other way in a true catastrophe, which is the whole point of insurance. A $7,000 MRI and surgery on a 90% plan with a $250 deductible — assuming you're under your annual limit (the most the policy pays per year) — comes back around $6,075, leaving you about $925.

So compare plans on four levers, not just the headline percentage:

- Annual limit — the yearly payout cap, from a few thousand dollars to unlimited.

- Reimbursement rate — usually 70%, 80%, or 90%.

- Deductible amount — what you pay first each year.

- Deductible type — annual (once per policy year) vs per-condition (a separate deductible for every diagnosis, which adds up fast).

These interact: a 90% plan with a $5,000 annual cap can pay out less than a 70% plan with unlimited coverage. And choose your limit carefully up front: raising it later may be restricted, may require new underwriting, and may not extend to conditions your pet already has. Read your policy like an adjuster, not a brochure.

How much does accident & illness insurance cost?

The 2024 U.S. average for an accident-and-illness plan is about $62 a month for a dog and $32 for a cat (NAPHIA). Real quotes swing widely around that — roughly $20 to $70 or more a month — because the price is built from your specific pet, not a flat rate.

Four things move your premium:

- Age — older pets cost more to insure.

- Species and breed — large or predisposed breeds carry higher expected claims.

- Location — your ZIP code's vet prices feed straight into the rate.

- Plan settings — a higher reimbursement rate, a lower deductible, or a higher annual limit all raise the premium.

What mostly doesn't set your price: how many claims you've filed. Pet insurers generally rate on age, breed, and local vet costs — not on your individual claim history — so in most cases using the policy doesn't single you out for a hike.

Going accident-only instead costs far less — about $16 a month for a dog and $9 for a cat on average, roughly a quarter of the comprehensive premium — but it pays nothing toward illness. And the reason the comprehensive premium is worth weighing: a single covered event isn't cheap. Nationwide pegs common accident costs at $565 to $1,921 and a typical ER visit at $2,000 to $5,000 — and illnesses like cancer run far higher.

Waiting periods and why you can't buy it after the accident

A waiting period is the gap between the day your policy starts and the day a given type of claim becomes eligible. It's tiered, and the tiers matter:

- Accidents — usually the shortest wait, but it ranges from a couple of days to about 14, depending on carrier and state.

- Illnesses — usually around 14 days.

- Orthopedic conditions — often much longer: six months at carriers like Embrace (sometimes reducible with an exam), and up to twelve at others. State rules vary.

Here's the trap inside that window: anything your vet documents during the waiting period — even a symptom noted, never mind a diagnosis — can be treated as pre-existing and excluded going forward. Skipping the vet to keep the chart clean is a workaround owners trade online, but it's the wrong move: it risks your pet's health and rarely fools an underwriter. The better play is a pre-enrollment wellness exam that gives you a clean, documented baseline before coverage starts.

And no, you can't buy a policy after the injury happens. That isn't the insurer being cruel — it's how insurance works at all. Premiums stay affordable only because everyone pays into the pool before the emergency; if you could buy coverage mid-crisis, no one would insure ahead of time and the whole model would collapse. Enroll while your pet is healthy.

One reality for the long run: premiums rise as your pet ages, and policy terms can drift at renewal — so the plan you choose now is a long-term relationship, not a one-year decision.

Is accident & illness insurance worth it — and who should buy it?

It depends on your pet's age and your finances. Four honest cases:

- A young, healthy pet — A&I is usually the right default. Illness — not accidents — is where the expensive, recurring claims tend to land, and enrolling before any symptom locks in the broadest coverage at the lowest premium.

- A tight budget — accident-only is the honest fallback. It won't touch an illness, but it beats nothing when a $2,000 ER bill lands.

- An older or already-diagnosed pet — run the breakeven math before you buy. Premiums climb with age, and anything already on the chart is excluded, so a senior policy can be economically upside down. That's not an automatic no — just do the arithmetic first.

- A self-insurer with deep reserves — if you can comfortably absorb a $20,000 emergency in cash, setting that money aside instead is a legitimate alternative.

What A&I actually buys is protection against the rare, ruinous event — and those are real. Owners on Reddit describe roughly $31,000 in ER bills with about $28,000 reimbursed, and a $17,000 emergency stay where the owner paid around $1,600. Insurance rarely "wins" in a normal year; it wins in the worst one.

The short version: young and pre-symptom, buy A&I; tight budget, choose accident-only honestly; older and already charted, run the breakeven math first. From here, see what coverage costs and how to compare plans.

Frequently Asked Questions

What does accident & illness pet insurance cover?

Both injuries and illnesses. On the accident side: broken bones, swallowed objects, lacerations, and toxicities. On the illness side: infections, allergies, gastrointestinal problems, chronic conditions like diabetes and arthritis, and cancer — diagnosis through treatment. Most plans also cover hereditary conditions, such as hip dysplasia, as long as they aren't pre-existing. What it leaves out: pre-existing conditions and routine or wellness care.

Does pet insurance cover pancreatitis?

Yes — pancreatitis is treated as an illness, so an accident-and-illness plan covers it as long as it isn't a pre-existing condition and you're past the illness waiting period. The catch is timing: if your pet was diagnosed with, or showed symptoms of, pancreatitis before your coverage began, it's excluded. Enrolling before any digestive trouble appears is what keeps it covered.

Is accident-only pet insurance worth it?

It can be, in the right situation. For a young, healthy pet whose owner is on a strict budget, accident-only is a legitimate floor — it covers broken-bone and swallowed-object emergencies cheaply. But it pays nothing toward illness, and illness (not accidents) is where the costliest claims tend to land, so the gamble grows as your pet ages. Our accident-only guide weighs it in full.

Does any pet insurance cover hip dysplasia?

Yes. Most accident-and-illness plans cover hip dysplasia as a hereditary condition, provided it isn't pre-existing and you've cleared the waiting period — which for orthopedic conditions can run six to twelve months at some carriers. Because dysplasia often shows up young, the move is to enroll before the first limp or X-ray note.

Can I add a wellness plan later?

Usually yes. Wellness (routine care) is an optional rider, and most carriers let you add it at renewal — though timing and availability vary by company. Just know what it does and doesn't do: it reimburses predictable costs like vaccines and dental cleanings, but it isn't insurance, and it doesn't unlock coverage for pre-existing conditions.

Does filing claims raise my premium?

Generally, no. Most pet insurers set your rate on age, breed, location, and local veterinary-cost inflation — not on how many claims you've filed. Your premium will climb as your pet gets older, but that's the aging, not a penalty for using the policy. Filing legitimate claims is exactly what you're paying for.

What's the difference between accident-only and accident & illness?

Coverage breadth. Accident-only pays for injuries — broken bones, swallowed objects, bite wounds — and nothing else. Accident & illness adds the entire disease side: infections, allergies, chronic conditions, and cancer. A&I costs more (roughly $62 a month for a dog versus about $16 for accident-only, on average), but it covers far more of what pets actually get sick from.

Sources

- Average Pet Insurance Premiums (2024 State of the Industry) — NAPHIA

- What Does Embrace Offer in Terms of Dental Illness Coverage? — Embrace Pet Insurance

- Accident-Only Pet Insurance — Nationwide

- What Is the Waiting Period for Orthopedic Conditions? — Embrace Pet Insurance

- Is pet insurance worth it? (r/petinsurancereviews) — Reddit