If you're holding a renewal letter with a premium 50–100% higher than last year — or a non-renewal notice ending your plan whether you like it or not — wanting to shop for something cheaper is completely reasonable. You insured your pet like you were supposed to, and now it can feel like you're being punished for it.

Before you do anything, the hard truth: switching pet insurance doesn't move your old coverage to a new company. You're buying a brand-new policy, underwritten from scratch — so your pet's pre-existing conditions, the waiting periods you already cleared, and your progress toward this year's deductible don't come with you. A cheaper quote can quietly cost far more than it saves.

That doesn't mean you should never switch. It means switching with your eyes open. Here's what actually happens when you do, in four steps:

- Compare plans on structure, not just price. A lower premium can hide a worse deductible type, a stingier payout method, or coverage gaps that matter for your pet.

- Review your pet's records and ask the new carrier for a pre-existing read-out. It's usually non-binding, but it tells you what they're likely to exclude before you commit.

- Bind the new policy and let its waiting periods start before you cancel the old one. Overlap the two; never leave a gap. You may pay both for a few weeks — that's the price of staying protected.

- Cancel the old policy once the new coverage is fully active, and ask for your pro-rated refund.

The rest of this guide helps you make the call: how to triage your situation by your pet's history, the safe-switch sequence step by step if you proceed, what to compare beyond the monthly price, and the honest alternatives for when switching would cost you more than it's worth.

Table of Contents

- Can you switch pet insurance at any time?

- Should you switch? Run this check first

- What you can lose when you switch (the risks)

- How to switch safely, step by step

- The exceptions: when pre-existing conditions CAN follow you

- If your insurer dropped or migrated your plan

- Alternatives to switching

- Frequently Asked Questions

- Sources

Can you switch pet insurance at any time?

Yes — you can switch pet insurance at any time. U.S. pet policies don't lock you into a long-term commitment — you can cancel whenever you want — though many run on annual terms billed monthly, so check each policy's cancellation and refund rules. But switching means buying a brand-new policy, not transferring your old one: pre-existing conditions, the waiting periods you've already cleared, and your deductible progress don't come with you.

That distinction is the whole game. When you renew with your current insurer, the conditions it has already been covering generally stay covered. Move to a different company and that company runs a fresh underwriting review of your pet's history, then re-applies its own exclusions and waiting periods from scratch — no industry mechanism ports your accrued coverage from one unrelated insurer to another. It's why a long-held policy can be worth more than its premium suggests: part of what you pay for is keeping the conditions your pet already has inside the covered column. (We unpack what counts as a pre-existing condition in detail below.)

And getting approved is not the same as getting paid. A new insurer will almost always issue you a policy — that part is easy. The real test comes at claim time, when the adjuster reads your pet's records and can decline anything tied to a problem that appeared before your new coverage began. "Can I get a policy?" and "Will this policy actually pay for my pet's existing issue?" are two very different questions, and confusing them is the most expensive mistake switchers make.

Should you switch? Run this check first

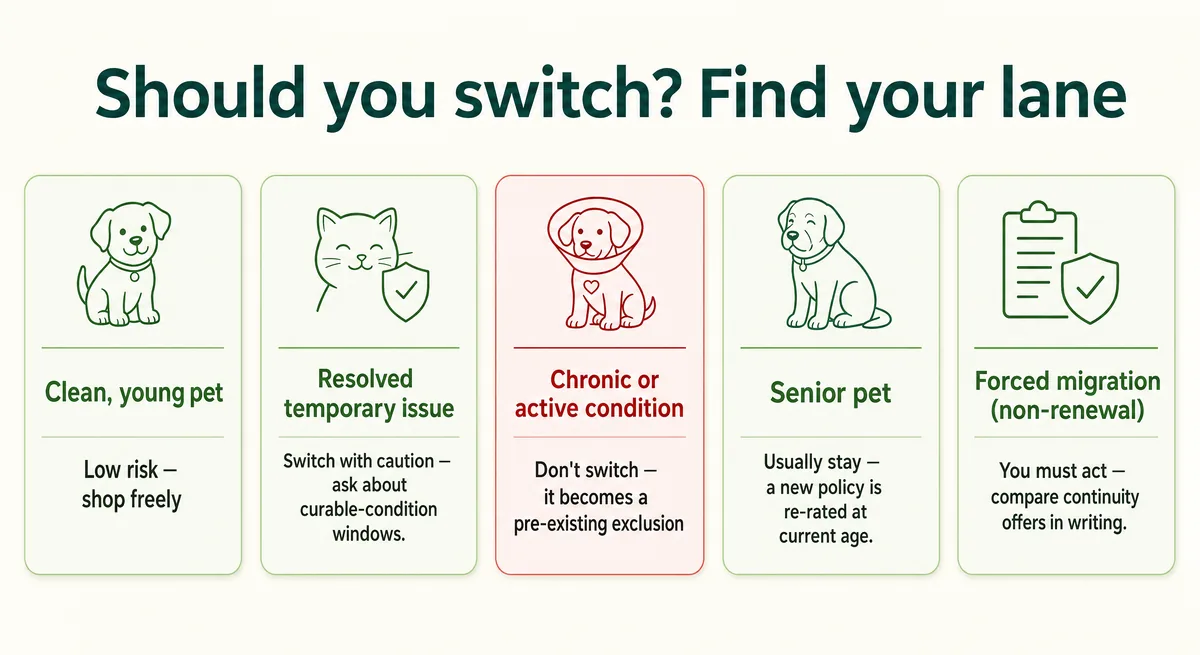

Before you compare a single quote, figure out which lane you're in — your pet's medical history drives this decision far more than the price difference. Roughly five situations cover most owners:

- Clean, young pet, nothing charted — low risk; shop freely (just compare structure, not only price).

- A resolved, temporary issue (an old ear infection, a one-off upset stomach) — switch with caution, and ask each carrier about its curable-condition window.

- A chronic or active condition (allergies, diabetes, kidney disease) — the dangerous lane; that condition almost certainly becomes a pre-existing exclusion at a new insurer.

- A senior pet — a new policy is priced at your pet's current age, so the cheaper quote often evaporates (more below).

- A forced migration — your insurer non-renewed you or is ending your plan, so you have to act; compare the continuity terms carefully (more on this further down).

Good reasons to switch

Switching makes sense when the numbers and the service genuinely justify it: a renewal increase well above market for a comparable policy, a carrier that quietly downgraded your benefits, repeated claim delays or denials, or a move to an area where your insurer is no longer competitive. Experian boils it down to four questions worth asking first: is the premium actually high for the market, do you like your insurer, does your pet have medical issues, and do you still need the coverage at all?

When you should NOT switch

Hold off if your pet is in active treatment, mid-diagnostics, or carries a chronic condition — you'd be handing a new insurer a reason to exclude exactly what you most need covered. Be especially careful with a senior pet: most carriers use attained-age pricing, so a new policy is rated at your pet's current age. Experian's example shows the same dog running about $53 a month at age 2 but roughly $135 at age 10, and vet costs rose 8.4% in one year — so a cheaper quote today tends not to stay cheap.

The 60-second break-even math

Here's the rule: the premium cut you need to break even is roughly the annual reimbursement you'd lose on excluded conditions, divided by your current annual premium. Here's an illustrative case — a dog with managed allergies (every number illustrative):

| Stay (renew) | Switch to a cheaper plan | |

|---|---|---|

| Annual premium | ~$749 (near the average dog A&I premium) | ~$540 |

| Allergy care covered? | Yes — continues | No — now pre-existing |

| Reimbursement kept per year | ~$600 | $0 |

| Net position vs staying | — | about $390 worse off |

You'd save about $209 in premium but forfeit roughly $600 in allergy reimbursement — a net loss of around $390 a year. To break even you'd need nearly an 80% premium cut (a plan near $12 a month), which essentially never happens. That's the nuance most owners miss: real quote differences rarely come close to the reduction needed to offset even one excluded chronic condition. Average accident-and-illness premiums run about $749 a year for dogs and $386 for cats — little room beneath that to out-save the coverage you'd lose.

Multiple pets? Decide per pet, not per household: shop the young, healthy one if it helps, but keep the pet with a chronic condition on its existing policy.

What you can lose when you switch (the risks)

Switching carries real risk, but the risks are specific, not vague — so here's exactly what's on the table when you move to a new insurer, laid out so you can weigh it clearly rather than fearfully.

Pre-existing conditions get re-reviewed — symptoms count, not just diagnoses

Your new insurer requests and reads your pet's full medical record, and "pre-existing" is broader than most owners expect: any illness, injury, or symptom noted before coverage starts — no formal diagnosis required. A single charted line like "loose stool" or "mild limp" can be used to exclude a whole body system later, and even a "monitor this" note or a recommended follow-up can count. In practice many carriers focus on the last 12 months of records, but the policy language usually reserves the right to review all of them.

Curable vs. incurable conditions

Chronic, incurable conditions — allergies, diabetes, arthritis, kidney disease, and usually dental — are typically excluded permanently once they count as pre-existing. Curable conditions (think ear infections or some urinary and stomach upsets) may be reinstated after your pet stays symptom-free and treatment-free for a set window, often 180 to 365 days. But it's carrier-specific, and the insurer decides what "cured" means, so document the vet-confirmed resolution date. We pull the carrier-by-carrier windows together further down.

Waiting periods reset

When you switch, every waiting period starts over. Accident waits are usually short — often just a few days — illness waits are commonly around 14 days, and orthopedic problems like cruciate tears or hip dysplasia can carry 6- to 12-month waits at many carriers. Anything that first appears during a new waiting period can be treated as pre-existing.

Rules also vary by state — California now bans accident waiting periods and limits illness and orthopedic ones — so check what applies where you live.

Bilateral exclusions

Some conditions affect a matched pair of body parts, and insurers treat the pair as one. If your dog tore the cruciate ligament in its left knee under your old policy, a new insurer will often exclude the right knee too — even though it has never been injured. The same logic applies to many eye conditions. (See our guide to dog ACL surgery for how expensive that one knee can get.)

Deductible and annual-limit progress resets

Everything you've paid toward this year's deductible and annual limit resets to zero at a new insurer — you start those accumulators over. A non-obvious trap lives here too: raising your own annual limit (say, $5,000 to unlimited) can re-underwrite you into a brand-new policy, which makes everything already on record pre-existing. Tweaking your deductible or reimbursement percentage sometimes doesn't trigger that — so before you change anything, call and ask specifically which changes re-underwrite your policy.

Your new premium is priced at your pet's current age

Most insurers use attained-age pricing, so a replacement policy is rated at your pet's age today — not the age you first enrolled at. That's why a cheaper headline quote for an older pet so often evaporates once the age factor is applied (we ran those numbers in the section above). A minority of carriers use issue-age pricing, which stays flatter over time but still adjusts for vet inflation and your region — so neither model is truly "locked in."

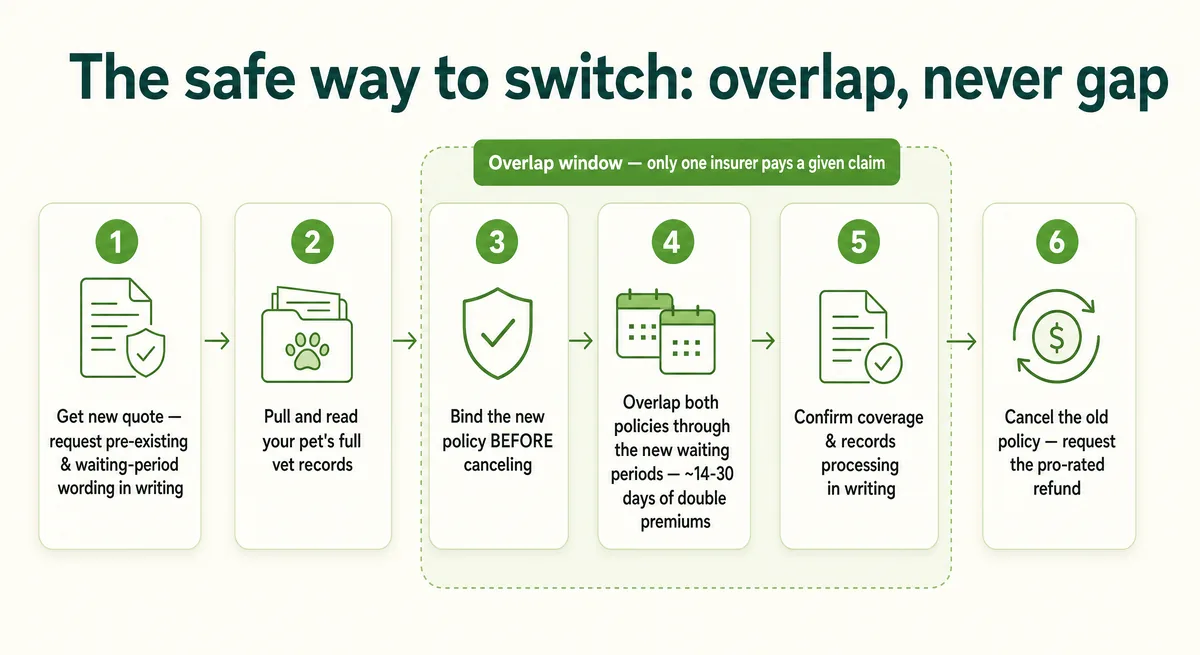

How to switch safely, step by step

The golden rule of switching is simple: overlap, never gap. You want your new policy fully active — past its waiting periods — before you cancel the old one, so any problem that crops up mid-switch always has a policy to land on. Here's the safe sequence:

- Get the new quote and the fine print in writing. Ask for the policy's exact pre-existing and waiting-period wording, not just the monthly price.

- Know what your pet's records actually say. Pull the full history and read the notes — a single "monitor this" line can shape what the new carrier excludes.

- Bind the new policy before you cancel the old one. Most carriers will let you hold two policies on the same pet during the transition.

- Overlap both policies until the waiting periods that matter to your pet have passed. For accidents and most illnesses that's often only 14–30 days of double premiums — but orthopedic and cruciate/hip-dysplasia waits can run 6–12 months, so if those are a real risk for your pet, plan to overlap far longer (or knowingly accept an unavoidable gap on that one body system rather than pay double for a year).

- Confirm coverage and records processing in writing. Get written answers on what is and isn't covered before you let the old policy go.

- Cancel the old policy and request your pro-rated refund. Put the cancellation in writing, ask what notice method the carrier requires, state the effective date you want, and get written confirmation of that date and the refund calculation — the effective date can change how much premium you get back.

One firm caveat during the overlap: you can't collect twice for the same bill. Tell each insurer about the other policy and follow its coordination rules — seeking double reimbursement for one claim is insurance fraud, and some carriers won't pay at all on a double-enrolled pet.

It's also worth knowing that your pet's history follows the pet, not the policy. Changing vets doesn't wipe the record, and leaving conditions off an application — or asking a vet to — is fraud, not a loophole. That reality is actually protective: an honest, complete record is exactly what lets a legitimate claim get paid down the road.

Keep this paperwork on hand through the switch:

- Declarations pages from both the old and new policies

- Your pet's full veterinary records and recent EOBs (explanation-of-benefits statements)

- The new carrier's written answers on coverage and waiting periods

- Written confirmation of your old policy's cancellation date

The exceptions: when pre-existing conditions CAN follow you

A few narrow paths let some pre-existing conditions carry over — but treat every one as "verify in writing," not a promise. These terms are eligibility-gated and they change, so confirm the current rules with the carrier before you count on any of them.

| Carrier | The exception | The catch |

|---|---|---|

| ASPCA, Pumpkin, Spot | A curable condition can stop counting as pre-existing after about 180 symptom- and treatment-free days | Knee and ligament conditions are the usual exception — they stay permanently excluded |

| Embrace, Figo | Curable conditions reconsidered after roughly 12 symptom-free months | Figo also waives the hip-dysplasia wait with vet sign-off — confirm the exact window with each |

| AKC | Covers pre-existing conditions after 365 days of continuous coverage | Eligibility is gated — enrollment age limits, a dental-illness exclusion, and state-by-state terms that can change — so confirm AKC's current rules in writing |

| MetLife (No Loss, No Gain) | Can continue a condition your prior insurer already covered | Group, employer, or association plans only; needs continuous, unlapsed coverage plus proof — and affiliate channels are tightening |

Two things to keep in mind. With curable windows, the insurer — not your vet — decides what counts as "cured," so document the symptom-free resolution date in writing. And No Loss, No Gain exists only through group channels because pooling many employees together lets the insurer absorb pre-existing conditions it would never take on one policy at a time.

There's a bit of good news for adopters: a rescue pet's earlier conditions aren't automatically excluded forever — if a curable issue stays resolved through the symptom-free window, coverage for it can come back. As with everything here, get the carrier's answer in writing, because these eligibility terms change from year to year — the AKC and MetLife rules in particular have been shifting.

If your insurer dropped or migrated your plan

A forced switch is a different animal from a voluntary one — the decision was made for you, and the question shifts from "should I move?" to "how do I move without losing what my pet already has?" This became real for a lot of owners recently: in 2024 Nationwide announced it would non-renew about 100,000 pet policies, citing inflation and rising vet costs, and a lawsuit alleges the cancellations wrongfully targeted pets by age and medical condition — a claim the company disputes and a court has not decided.

If you're handed a migration or replacement offer, read it for one thing first: continuity language. The gold standard is a No-Loss-No-Gain-style clause that carries your already-covered conditions into the new plan — ask for it in writing, because a "replacement" without it is just a fresh policy with fresh exclusions.

If there's no continuity offer, you're shopping the open market under time pressure. Move quickly, but in the safe order from the steps above, and use the carrier-exception table to find a plan that actually fits your pet's history. Some owners also screen for stability itself — asking which insurers are least likely to pull the same move. Private-equity ownership is one lens people use for that, though you should confirm any specific carrier's situation before you rely on it.

Alternatives to switching

Sometimes the smartest move isn't switching at all — it's restructuring what you already have. If your pet has any charted condition, this is usually the better play: it keeps your existing coverage intact while lowering the bill. Start by calling your current carrier and asking what's possible:

- Raise your deductible — but enough to matter. Small increases often barely move the premium, so ask your carrier to quote several deductible levels (say $250, $500, $750, and $1,000) and compare; the savings vary widely by carrier and pet.

- Lower your reimbursement percentage (say, 90% down to 70%) to trim the premium while keeping the policy — and its covered conditions — in place.

- Drop wellness or routine-care riders you aren't using; those add premium for predictable costs you can budget for directly.

- Shift toward catastrophic coverage — a high-deductible illness plan, or accident-only — so you stay protected against the bills that actually break a budget.

You can also self-insure the small stuff: bank the difference for routine and minor costs while keeping real illness coverage. Be honest about the math, though — one serious incident (cancer care, a major orthopedic repair, a swallowed-object surgery) can run $5,000 to $20,000 or more, and that exposure is exactly what insurance exists to absorb. If the real problem is fronting the bill at checkout, the fix may be moving up to a carrier that pays your vet directly, rather than switching for a lower price.

For a multi-pet household, decide per pet, not per household: keep the pet with a chronic condition on its current plan and shop only the young, healthy one. And one reminder from earlier — if you restructure by raising your annual limit, ask first, because that can re-underwrite you into a brand-new policy and reset everything to pre-existing.

Frequently Asked Questions

Can I switch pet insurance with pre-existing conditions?

Yes, you can buy a new policy, but any condition already in your pet's medical record will almost certainly be excluded as pre-existing by the new insurer. Curable issues — like a past ear infection — may regain coverage after a carrier-specific symptom-free window, while chronic conditions such as allergies or diabetes are typically excluded for good. If your pet is actively using coverage for a chronic condition, switching usually costs you far more than it saves.

Can I switch from one pet insurance to another?

Yes — you can move anytime. U.S. pet policies don't lock you into a long-term commitment, though many run on annual terms billed monthly, so check the cancellation and refund terms first. Just remember a switch means buying a brand-new policy, not transferring your old one: pre-existing conditions, cleared waiting periods, and deductible progress don't carry over. Bind the new policy and let its waiting periods start before you cancel the old one, so you never leave a coverage gap.

What happens if I change my pet insurance?

When you change insurers you start a fresh policy: waiting periods reset, your deductible and annual-limit progress zero out, and the new carrier re-reviews your pet's records and re-applies exclusions. Anything that surfaced before the new coverage began — even a symptom noted in the file — can be treated as pre-existing. Overlapping the two policies through the new waiting periods is how you avoid a gap.

Is it worth it to switch pet insurance?

It depends almost entirely on your pet's medical history. For a young, healthy pet with a clean record, switching to a better-structured plan can be worth it — just compare coverage, not only price. For a pet with a chronic or active condition, it usually isn't: the reimbursement you'd forfeit on a newly-excluded condition typically dwarfs any premium savings. Run the break-even math before you move.

Will pet insurance cover arthritis after I switch?

Usually not. Arthritis is a chronic condition, so once it's in your pet's record a new insurer will almost always treat it as a pre-existing condition and exclude it permanently. Curable problems can sometimes be reinstated after a symptom-free window, but ongoing conditions like arthritis, allergies, or diabetes generally can't. If arthritis is already being managed, staying with your current insurer usually protects that coverage.

Can I have two pet insurance policies at once?

Yes, and briefly running two is actually the safe way to switch — you keep the old policy active until the new one clears its waiting periods, which avoids any gap. The catch: you can't collect twice for the same bill. Tell each insurer about the other policy and follow its coordination rules, because seeking double reimbursement is insurance fraud. Some carriers also won't pay anything on a double-enrolled pet, so confirm the rules with each.

Do I get a refund when I cancel?

Often yes — most insurers refund the unused portion of any prepaid premium on a pro-rated basis, but you usually have to request it. Some charge a small cancellation fee or bill the remaining premium for the period, so ask exactly what you're owed. Put the cancellation in writing and make sure the effective date is the day you sent notice, not the day it happens to be processed.

Does changing vets reset my pet's pre-existing conditions?

No. Your pet's medical history follows the pet, not the clinic — a new insurer can request records from every vet your pet has seen. Leaving conditions off an application, or switching vets to hide them, is insurance fraud, not a workaround. That reality is actually protective: a complete, honest record is what lets a legitimate claim get paid later.

Sources

- How to Switch Pet Insurance Providers — MetLife Pet Insurance

- Can I Switch Pet Insurance Providers? — PetPlace

- Should You Change Pet Insurance if Your Rate Increases? — Experian

- State of the Industry Report 2025 — NAPHIA

- What to Know About Switching Pet Insurance Carriers — Figo Pet Insurance

- California Insurance Code § 12880.7 — Justia (California Insurance Code)

- The Best Pet Insurance — NYT Wirecutter

- Nationwide dropping pet insurance for 100,000 pets — Fox Business

- Nationwide Lawsuit Alleges Insurer Wrongfully Canceled Whole Pet Policies — ClassAction.org

- Pet Insurance and Pre-existing Conditions — ASPCA Pet Health Insurance

- Pumpkin Pet Insurance FAQs — Pumpkin

- Pet Insurance That Covers Curable Pre-Existing Conditions — Embrace Pet Insurance