Accident-only pet insurance covers vet bills from sudden, unexpected injuries — broken bones, toxic ingestion, bite wounds, swallowed objects — at a fraction of a full policy’s price. It does not cover illness of any kind: no cancer, no infections, no chronic conditions.

Whether that narrower net is a smart buy or a false economy depends on your pet and budget. Below: what these plans pay for, what they cost in 2026, which US carriers sell them, how those plans compare — and when accident-only is worth it versus when to skip it. For the full coverage picture, start with our guide to what pet insurance covers.

Table of Contents

- What accident-only pet insurance covers

- What accident-only pet insurance does NOT cover

- How much does accident-only pet insurance cost in 2026?

- Accident-only vs. accident & illness — which is right for you?

- The 2026 carrier comparison

- When accident-only is actually worth it — and when it isn't

- How emergency payment actually works

- Waiting periods and the NAIC context

- How to enroll and what to expect at claim time

- Frequently Asked Questions

- Sources

What accident-only pet insurance covers

Accident-only is the narrowest of the three coverage tiers — below accident-and-illness and the comprehensive plans that bundle wellness. It reimburses treatment for sudden physical injuries, and nothing else; we compare it against accident-and-illness later in this guide. One rule travels across every tier: a condition that meets the issued form’s pre-existing-condition definition is excluded. Prior signs, advice, diagnosis, or treatment can matter even without a final diagnosis, but documentation alone does not replace the form’s definition.

Covered perils

Carrier policy forms overlap on a canonical list — Spot’s accident-only plan and its peers cover six core perils:

- Broken bones — falls, stairs, car strikes, rough play.

- Bite wounds — dog-park scuffles, cat fights, wildlife.

- Toxic ingestion — chocolate, xylitol, antifreeze, lilies.

- Foreign-body ingestion — socks, corn cobs, squeaker toys; the classic five-figure surgery.

- Lacerations — fence wire, glass, anything sharp.

- Heatstroke — sudden heat exposure treated as an accidental event.

Covered diagnostics and treatments

For a covered accident, plans typically pay for the medicine around it: X-rays and MRI/CT imaging, surgery, anesthesia, hospitalization, and prescription medication for the injury itself. The fine print varies on two line items — Pets Best’s sample accident policy excludes office-visit exam fees and take-home medications even on a covered claim, while Spot’s policy folds exams into treatment. Check those two lines before you buy.

What counts as an “accident” in real life

Policy forms define an accident as sudden, unexpected, tied to a specific time and place, and caused by something beyond your control. At claim time, clear event and medical documentation matters; the legal burden and proof standard vary by state and form, and some state statutes place specified pre-existing-condition proof duties on the insurer. Four scenarios from US pet-insurance subreddit threads show where it bites:

- An unwitnessed hip injury — the carrier wanted proof tying it to a specific accident, though the dog had been fine moments earlier.

- A cruciate tear after a single prior limp note — one old chart line can reframe the claim as illness or pre-existing.

- A swallowed object nobody saw go down — unwitnessed ingestion invites the same proof challenge.

- A Lab with repeat ingestion history — episode two or three can be reclassified as a behavioral pattern rather than an accident.

None of this means accident claims don’t pay — clear, well-documented events generally do. The gap between “an accident happened” and “the carrier can verify a sudden accidental cause” is where this product is won or lost, so get the event into the vet record with a date, time, and cause while it’s fresh.

What accident-only pet insurance does NOT cover

The rule is simple: if it isn’t a sudden physical injury, an accident-only plan won’t pay for it. That leaves out the large, expensive world of illness — plus a few gray-zone cases worth knowing before you buy.

Illness, chronic, hereditary, and pre-existing conditions

These four categories are excluded on every accident-only policy, no exceptions:

- Illness — infections, cancer, diabetes, kidney disease.

- Chronic conditions — allergies, arthritis, recurring ear or skin problems.

- Hereditary and breed-specific — hip dysplasia, heart defects.

- Pre-existing conditions — anything already on the record when coverage began.

“Pre-existing” is broader than most owners expect. The NAIC’s model law defines it by a vet’s advice or treatment or verifiable signs and symptoms before your effective date or during the waiting period — so a limp your vet noted last year can count, with or without a formal diagnosis.

Edge cases — dental, orthopedic, cancer, and bloat

The boundary blurs in four predictable places. A tooth fractured in an accident is usually treated as an injury and can be claimable; routine dental disease is an illness and never is. Knee and ligament injuries are a known trap — some accident forms exclude cruciate-ligament and disc injuries outright, and others apply bilateral-condition rules, where a problem documented on one knee bars a future claim on the other. Cancer stays an illness even when an owner ties it to a swallowed toxin; whether that ever counts as accident-caused is a causality dispute decided policy-by-policy, so don’t assume it. And bloat (GDV), despite striking like an emergency, is an internal disease process rather than an external injury — carriers generally classify it as illness, which puts it outside accident-only coverage.

How much does accident-only pet insurance cost in 2026?

Accident-only is the cheapest tier of pet insurance. Most owners pay roughly $7 to $25 a month — a fraction of full accident-and-illness premiums. Industry averages sit lower still, and your pet’s age, breed, state, and plan design decide where in that band you land.

National averages

The cleanest public benchmark comes from NAPHIA, the industry trade group. Its 2025 weighted-average accident-only premiums were $190 a year for dogs and $112 for cats — about $15.83 and $9.33 a month. Compared with 2024, the 2025 dog average fell from $193 to $190 while the cat average rose from $110 to $112. These are book-of-business averages, not quotes for a particular pet.

Monthly carrier floor and ceiling

That $7–$25 band hides a wide spread, because the premium simply buys a plan design. Three published policy-form examples show the shape of it:

- Embrace — $5,000 annual limit, $100 deductible, 90% reimbursement, marketed for older pets.

- Pets Best (sample form) — $10,000 annual limit, $250 deductible, 90/10 coinsurance.

- Odie — a fixed $10,000 limit, $250 deductible, 90% plan.

Here is how calculation order changes the result on a $3,000 eligible accident with the full $250 deductible remaining and 90% reimbursement. A deductible-first form pays ($3,000 − $250) × 90% = $2,475, leaving you $525. A percentage-first form pays ($3,000 × 90%) − $250 = $2,450, leaving you $550. Exclusions and limits can change either result; the issued form controls.

What moves the price

Six levers set your quote: your pet’s age and breed, your state, and the three you control — deductible, reimbursement percentage, and annual limit (most plans cap it; a few sell unlimited). Location alone can swing a premium, the same reason pet insurance costs differ nationwide. Accident-only mutes one big lever, though: with illness off the table, breed-linked disease risk barely moves your price.

Accident-only vs. accident & illness — which is right for you?

It comes down to one question: is your bigger fear a sudden injury, or a long illness? Accident-only covers the first and ignores the second. Accident-and-illness covers both — for roughly about 4.4 times the price in the 2025 NAPHIA dog averages ($836 a year versus $190 for accident-only).

Personal-finance editorials like Bankrate frame this as a “which is right for you” choice rather than a clear winner — and that is the honest read. It depends on your situation:

- Lean accident-only if money is tight, your pet has aged out of full coverage, or your one real fear is a five-figure trauma bill.

- Lean accident-and-illness if you want protection against the cancers, diabetes, and chronic conditions that drive most vet spending — and the higher premium fits your budget.

If illness is the worry that keeps you up at night, full accident-and-illness coverage — which we cover in its own dedicated guide — is the better fit.

The 2026 carrier comparison

No carrier wins accident-only outright — plans differ most on annual limit, waiting period, and whether an older pet can even enroll. Here is how five U.S. carriers’ published accident-only plans line up.

| Carrier | Annual limit | Deductible | Reimbursement | Accident waiting period | Senior age cap | Notable |

|---|---|---|---|---|---|---|

| Pets Best | $10,000 (sample) | $250 (sample) | 90% | 3 days | Not published | Sample form excludes cruciate-ligament & disc injuries, exam fees, take-home meds |

| Embrace | $5,000 | $100 | 90% | 0 days after the policy effective date in current published materials; issued state form controls | Sold to pets 15+ | Current published materials include exam-fee and prescription-drug coverage by default but allow those benefits to be removed; state/form rules control |

| PetPartners | Unlimited | $100 | 90% | 2–3 days | No maximum age | AccidentCare plan; also a $3,000/incident, $11,000/yr tier |

| Odie | $10,000 | $250 | 90% | 3 days in the current Trisura sample | None (marketing) | Fixed-rate plan; markets “no breed or age limits” |

| Spot | Not published | Not published | Not published | 14 days (varies by state) | Not published | Applies bilateral rules to knee & ligament conditions |

A few patterns matter more than the brand names. A high or unlimited annual limit — PetPartners, or the $10,000 plans — is what does the most to blunt a five-figure trauma bill; a capped plan still leaves anything above the limit, plus your deductible and coinsurance, on you. Accident timing spans zero to roughly 14–15 days across current forms, with state law sometimes prohibiting a wait and some carriers using a delayed effective date instead. If your pet is a senior, enrollment age is the other gate: PetPartners and Embrace court older pets, while many full plans would turn them away.

How to read this: figures come from public policy forms and carrier marketing pages as of July 2026; “Not published” means the carrier doesn’t disclose it openly. Limits, deductibles, and waiting periods change and vary by state, so confirm them with the carrier in writing before you enroll.

When accident-only is actually worth it — and when it isn't

Accident-only isn’t universally smart or foolish — it’s the right call for a few specific situations and the wrong one for others. Here is the honest split.

Your senior pet has aged out of full coverage

Full accident-and-illness plans get harder to buy — or pricier — as a pet ages, while accident coverage often has no age ceiling: Embrace markets its accident-only plan to pets 15 and up, and PetPartners advertises no maximum age. The counterpoint is real, though: in one r/petinsurancereviews thread, owners argued that illness, not injury, is a senior pet’s likeliest expense — so accident-only can insure the wrong risk.

Tight budget, catastrophic-only fear

When the thing that scares you is a $5,000–$15,000 trauma bill but the monthly accident-and-illness premium is out of reach, accident-only at roughly $7–$25 a month (the range from the cost section) is a genuine bridge. Owners in that same thread call it a “better than nothing” hedge — one reported it covering a $2,000 emergency surgery.

An A&I exclusion left a narrow gap

The rarest case, and we’ll be blunt: it seldom pays off. A breed or bilateral-condition exclusion on a full policy leaves a hole — but accident-only won’t fill an illness hole, so most owners in this spot can skip it.

Your pet lives an accident-prone life

Rural roaming, off-leash hikes, multi-pet chaos, climbers, and dedicated scavengers all tilt the math toward accident-only — higher injury frequency is exactly what it’s built for. The classic case is the Labrador who eats what it shouldn’t, where a single foreign-body surgery runs five figures.

When accident-only is NOT worth it

Three situations where we’d tell you to skip it:

- Illness is the real risk. If cancer, diabetes, kidney disease, or allergies are your worry, accident-only pays nothing toward any of them.

- Your pet has a documented repeat pattern. A charted history of ingestion or orthopedic trouble can get the second or third episode reclassified as behavioral or pre-existing.

- You can’t front the cash. Most accident-only plans reimburse after you pay, and owners report few vets accept direct pay — so without savings or CareCredit, the policy can’t rescue you in the moment.

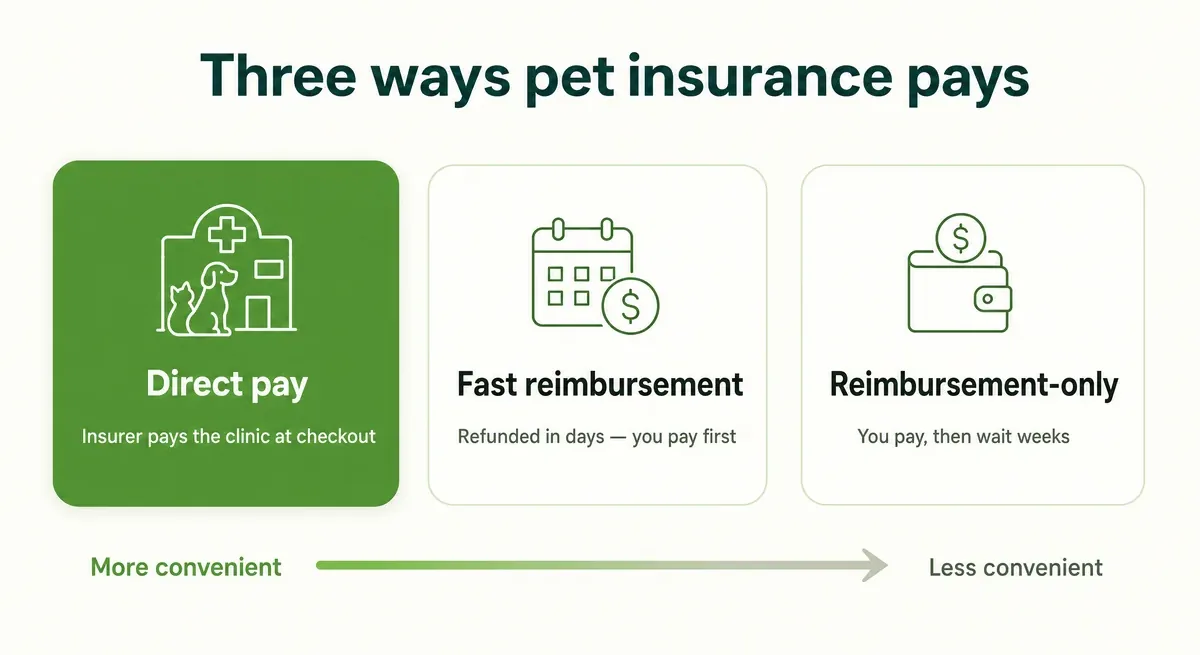

How emergency payment actually works

Here’s the question that matters at 2 a.m.: will you still have to put $10,000 on a card at the counter? With most accident-only plans, the honest answer is yes — the insurer pays you back, not the vet. Pet insurance runs on three payment models, and only one spares you from fronting the whole bill.

- Real-time checkout adjudication — Trupanion VetDirect Pay can pay participating clinics at checkout (Trupanion is not an accident-only seller). This is different from a claim approved later and routed to a vet.

- Fast reimbursement — app-driven carriers like Pumpkin, MetLife, and Lemonade can refund you within days, but you still pay the vet first.

- Reimbursement-only — the default for most accident-only plans. You pay, submit a claim, and wait weeks for the money.

That gap between the bill and the reimbursement is the real catch. When direct pay isn’t an option and savings can’t absorb the hit, owners lean on CareCredit or Scratchpay to bridge it. If accident-only is your catastrophe plan, line up that bridge before you ever need it.

Waiting periods and the NAIC context

An accident-only policy may have a short waiting period, no accident wait after effectiveness, or a delayed effective date. The issued state form decides. Examples from current or cited forms include:

- Pets Best — 3 days in the cited Georgia sample

- Embrace — current published materials say accident coverage starts on the policy effective date; issued state terms control

- Odie — 3 days in the current Trisura sample

- Spot — 14 days in many states, with state variation

The NAIC Pet Insurance Model Act prohibits accident waiting periods, but a model is not federal law; it operates only through state enactment. The NAIC's Summer 2025 state-action chart classified 16 jurisdictions as model adoptions: California, Delaware, Florida, Hawaii, Louisiana, Maine, Maryland, Mississippi, Montana, Nebraska, New Hampshire, Ohio, Pennsylvania, Rhode Island, Vermont, and Washington. That is a dated NAIC classification, not a substitute for current state law. Check enactment and effective dates, then read the issued policy's effective date and accident terms.

How to enroll and what to expect at claim time

Signing up takes minutes; the claim is where the real work happens. Here is the honest flow, from enrollment to payout.

Enrollment process

Most accident-only plans enroll online in minutes, with no vet exam required to start. Coverage runs from an effective date, and the waiting period we covered above counts from that date — so buy before you need it, never mid-crisis. Before you pay, read the declarations page: it spells out your deductible, reimbursement percentage, annual limit, and the exact day coverage begins.

What records the carrier will request

Carriers generally don’t pull your pet’s medical history to enroll — they request the full record when you file your first claim. That’s when prior notes get read, and a symptom logged before any formal diagnosis can still be flagged as pre-existing. The takeaway, echoed across owner accounts on Quora: buying the policy is easy; whether a given claim is paid turns on what the chart already says. Never thin out the record to protect a claim — get the care, then enroll with the history you have.

If your claim is denied — the appeal pathway

A denial isn’t always final. Gather the records, ask your vet for a letter explicitly tying the injury to a sudden, specific accident, lay out the timeline with dates, and appeal in writing. Owners in US pet-insurance subreddit threads describe appeals as slow and documentation-heavy — yet some are overturned once the paperwork clearly establishes the cause. Treat it as a viable path, not a guarantee.

Frequently Asked Questions

Should I get accident-only pet insurance?

It depends on your pet's main risk and your budget. Accident-only is a smart fit for a senior pet that has aged out of accident-and-illness coverage, a tight budget where the real fear is a sudden multi-thousand-dollar trauma bill, or an accident-prone lifestyle — off-leash, rural, multi-pet, or a known scavenger. It's the wrong fit if your pet's likeliest costs are illness (cancer, diabetes, allergies), which it never covers, or if you have no cash to front a bill on a reimbursement-only plan.

What does accident-only dog insurance cover?

Accident-only dog insurance covers sudden physical injuries — broken bones, bite wounds, toxic ingestion, foreign-body ingestion (the classic swallowed-sock surgery), and lacerations — plus the diagnostics and treatment they require, such as X-rays, surgery, and hospitalization. It does not cover illness. Coverage begins on the issued policy's effective date and after any applicable accident wait; a documented injury that predates that coverage is excluded.

What does accident insurance cover for dogs?

Beyond the injury itself, accident insurance for dogs pays for the care a covered accident requires: emergency exams (at some carriers), X-rays and advanced imaging, surgery, anesthesia, hospitalization, and prescription medication for that injury. How much comes back to you depends on your deductible, reimbursement percentage, and annual limit. It won't touch illness, routine or wellness care, or pre-existing conditions — those need accident-and-illness or comprehensive coverage.

Does accident-only cover pancreatitis?

No. Pancreatitis is an illness, not an accident, so no accident-only policy covers it — even when it strikes suddenly and lands you in the ER. The same is true of other sudden-feeling illnesses like bloat (GDV) at most carriers. If illness is a genuine risk for your pet, accident-and-illness coverage is the product that pays for it; if your pet already has a history, check how pre-existing conditions are handled before you buy.

Can I switch from accident-only to accident-and-illness later?

Usually yes, but the switch is treated as new enrollment, not an upgrade. Fresh waiting periods apply to the illness coverage, and anything that appeared while you held the accident-only policy — including symptoms noted before a formal diagnosis — can be excluded as pre-existing on the new plan. The cleaner your pet's records when you switch, the more the upgrade actually buys you.

Is there a waiting period?

Not always. Current forms include zero-day accident clocks and waits up to roughly 14–15 days; other products delay the policy's effective date. The NAIC model prohibits accident waits in adopting states, and the NAIC's Summer 2025 chart counted 16 model-adoption jurisdictions. The applicable state law and issued form control, so enroll before a crisis and verify both the effective date and any accident wait.

Sources

- Accident-Only Pet Insurance Plan — Spot Pet Insurance

- Accident-Only Policy Booklet — Sample (GA) — Pets Best

- Need opinions on denied accident claim for my dog (Pets Best) — Reddit r/petinsurancereviews

- Best accident only insurance? — Reddit r/petinsurancereviews

- Lab with known ingestion of foreign objects — Reddit r/petinsurancereviews

- NAIC Pet Insurance Model Act — National Association of Insurance Commissioners

- Pet Insurance State of the Industry Report 2025 — Highlights (YE 2024) — North American Pet Health Insurance Association (NAPHIA)

- What Is Embrace's Accident-Only Pet Insurance Plan? — Embrace Pet Insurance

- Accident-Only Plan — Odie Pet Insurance

- Is Accident-Only or Accident and Illness Pet Insurance Right for You? — Bankrate

- Accident-Only Pet Insurance Plan — PetPartners

- Accident Only plans (Chewy Care Plus) — Reddit r/petinsurancereviews

- How does pet insurance know if your dog has a pre-existing condition at the time of enrollment? — Quora

- Direct Vet Pay through Pets Best — Reddit r/petinsurancereviews

- VetDirect Pay — Trupanion

- Waiting Periods — Embrace Pet Insurance

- Accident & Illness Policy Sample (UIIPOLICY 1.1.26) — Odie / Trisura

- Pet Insurance Model Act — State Adoption Page (Summer 2025) — National Association of Insurance Commissioners

- Pets Best Denying Claim — Reddit r/petinsurancereviews

- State of the Industry Report 2026 Highlights (2025 data) — NAPHIA