Pet insurance in Texas typically costs $31 to $153 per month, with dogs averaging about $64 a month. Four things move your number: where in Texas you live (down to the ZIP code), your pet’s age, its breed, and the plan design you choose — deductible, reimbursement rate, and annual limit.

This guide covers what coverage actually costs in each major Texas metro, how a policy behaves at a Texas vet or ER counter, which providers fit which kind of owner, and what Texas law does — and doesn’t — protect you from.

Table of Contents

- How much does pet insurance cost in Texas?

- What pet insurance covers in Texas

- How pet insurance works at a Texas vet or ER counter

- Best pet insurance providers in Texas (2026)

- Texas pet insurance laws and regulations

- Will my premium rise — and can I switch later?

- Is insurance still worth it for an older or medically-messy Texas pet?

- How to compare Texas plans — the levers that actually matter

- Frequently Asked Questions

- Sources

How much does pet insurance cost in Texas?

There is no single Texas premium that predicts what one pet will pay. The latest industry baseline is NAPHIA's 2025 U.S. accident-and-illness average: $69.67 per month for dogs and $36.25 for cats. That is a national, all-market benchmark—not a Texas carrier quote or a 2026 price survey.

One standardized Texas benchmark

MoneyGeek's Texas model, updated April 28, 2026, discloses a consistent baseline: modeled prices drawn from more than 67,000 profiles across 18 providers, using a 6-year-old Labrador Retriever and a 7-year-old Ragdoll, a $5,000 annual limit, $500 annual deductible, and 80% reimbursement. Under those source-specific assumptions, it reports:

| Modeled Texas benchmark | Monthly premium | What it means |

|---|---|---|

| Dog profile | $64 | 6-year-old Labrador; standardized $5K / $500 / 80% settings |

| Cat profile | $33 | 7-year-old Ragdoll; same benefit settings |

| Combined source benchmark | $49 | MoneyGeek's aggregate of those baseline profiles—not an all-pet quote |

Those figures are modeled observations from one secondary source. They are useful planning context, but they do not establish which carrier is cheapest, what a different breed or ZIP will pay, or how a renewal will change.

How age and breed move that same model

Holding the source's benefit settings constant, MoneyGeek reports an age-segment average of about $36.25 at age 1 and $153 at age 15. Its breed table ranges from about $34 for a Chihuahua to $125 for an Olde English Bulldogge; a Labrador is about $64, a French Bulldog $94, and a Domestic Shorthair cat $31. These are modeled segments, not carrier quotes. The age series is not the renewal history of one pet or proof that every insurer uses the same rating method: most carriers may use attained age, while Trupanion says birthdays and an individual pet's claims are not direct renewal factors, although its cohort and location rates can still change.

How to compare actual Texas quotes

Use the same quote date, ZIP code, species, breed, sex, date of birth, annual limit, reimbursement percentage, deductible amount and type, exam-fee option, wellness add-ons, and enrollment channel at every carrier. Record the legal insurer and policy edition too. Pull at least three same-day quotes and compare the issued benefits—not a city average, a carrier advertisement, or an owner's unmatched anecdote.

Location still matters: carriers can use territorial and veterinary-cost factors, so two Texas ZIP codes may return different prices even for the same pet and settings. That is a reason to quote your actual address, not a reason to splice unrelated Houston, Dallas, Austin, and owner-reported figures into one range.

What pet insurance covers in Texas

A Texas policy buys the same core product sold everywhere — reimbursement for unexpected vet bills — but the checklist is local: heartworm country, snake country, hundred-degree summers, and hurricane season.

Accident-only vs. accident-and-illness vs. wellness add-ons

Accident-and-illness is the default: injuries plus disease, parvo to cancer. Accident-only covers trauma — road accidents, swallowed objects, bites — at a fraction of the price. Wellness add-ons prepay routine care (exams, vaccines, preventives); they are budgeting tools, not insurance. NAPHIA’s 2025 U.S. averages show the gaps:

| Plan type | Dogs (annual) | Cats (annual) |

|---|---|---|

| Accident-and-illness | $836 | $435 |

| Accident-only | $190 | $112 |

| Accident-and-illness + wellness | $1,414 | $859 |

Accident-only suits owners hedging pure trauma risk; most buyers want accident-and-illness; add wellness only if the bundle beats paying directly — more in our guide to what pet insurance covers.

Texas-specific hazards the policy should handle

Texas leads the nation in heartworm incidence, per the American Heartworm Society. Preventives sit in wellness add-ons; heartworm treatment may be eligible under illness coverage if the infection is not pre-existing or otherwise excluded; preventive-care compliance and policy terms matter.

Snake bites cluster in the Hill Country and West Texas; antivenom alone is commonly estimated at $1,500 to $5,000 per vial, and envenomation is typically payable under accident coverage — confirm your policy’s accident definition says so. Heat stroke lands the same way. Along the Gulf Coast and border, kissing bugs transmit Chagas disease — studied in Texas dogs by Texas A&M researchers — which can mean lifelong cardiac care. Before hurricane season, know how your carrier handles care and boarding if you evacuate.

Waiting periods

Does coverage start immediately? It depends. Most policies have one or more category-specific waiting periods, but some accident or wellness coverage can begin on day zero; Texas does not set a pet-insurance waiting-period schedule. Accidents often start within zero to five days (MetLife advertises day-zero accident coverage in Texas); illness commonly waits around 14 days; orthopedic conditions can wait six months (U.S. News notes a six-month hip-and-knee period at one major carrier); wellness often begins immediately. Exact periods are carrier-specific — read the policy. Texas law sets no waiting period of its own.

Pre-existing conditions — at the symptom level

The question owners actually ask isn’t “is my diagnosed disease covered?” It’s “can that diarrhea note from last spring be connected to a claim later?” — the exact worry running through owner discussions about ear infections, vomiting notes, and old limps. You can almost always buy the policy; what’s at stake is whether a flagged condition will be covered.

Insurers may review the chart at enrollment, with an early claim, or when a related claim requires it; the timing varies. An isolated upset-stomach episode is treated differently from a recurring GI pattern — one-offs tend to stay one-offs, patterns are more likely to support a related exclusion, subject to the issued policy. The sharpest version is the bilateral rule: for paired conditions like cruciate tears, hip dysplasia, and luxating patellas, a “slight limp” noted on one side before coverage can cause both sides to be treated as related under some policy forms. Cure-out rules and limited exceptions vary. In one documented cruciate case, an owner recovered over $3,500 of a $3,900 surgery bill because the chart held no prior notation on either knee.

Keep perspective: most claims are paid, and the anxiety lives in edge cases. Never thin out the vet record to protect insurability — get the care, then enroll with the chart you have. Our pre-existing conditions guide covers the lookback rules in depth.

How pet insurance works at a Texas vet or ER counter

At almost every Texas clinic, pet insurance is reimbursement-first: you pay the bill, submit the claim, and the insurer pays you back. The policy doesn’t need to be “accepted” by the vet — you can use any licensed Texas vet — but the money leaves your account first.

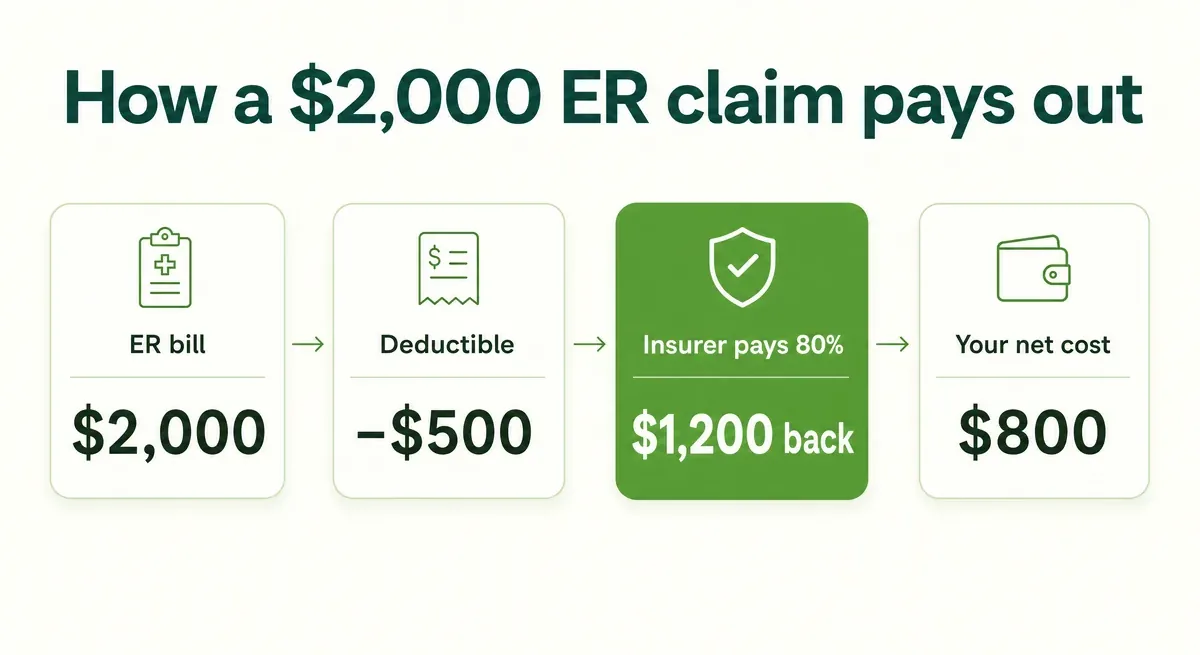

The math on a typical claim: a $2,000 ER bill with a $500 deductible and 80% reimbursement returns $1,200 — the insurer pays 80% of the $1,500 above your deductible — so your net cost is $800.

Trupanion’s participating-clinic tool can adjudicate eligible charges in real time — owners describe it clearing a $7,000 eye-surgery bill in minutes — and Pets Best offers a different payment route: after claim processing and approval, a signed release can route approved payment to the vet, which does not by itself bridge checkout. Participation and workflow are clinic-specific: the same threads include veterinary staff whose clinics refuse direct pay over billing and software friction. If direct pay is the reason you’re choosing a carrier, call the specific Texas hospital you’d actually use — before the crisis, not during it.

Two more levers smooth the cash-flow gap. For scheduled procedures, some carriers offer preauthorization or a coverage review. It can clarify likely eligibility but is not a guarantee of final payment, which still depends on the policy and complete records. And financing — CareCredit and Scratchpay come up in nearly every Houston emergency thread — is the backup that buys time while a claim processes. Treat it as a complement to insurance, not a substitute: financing defers the bill; insurance is what shrinks it.

Best pet insurance providers in Texas (2026)

There is no universal #1 in Texas — the right carrier depends on what you’re protecting against: cash-flow shock, catastrophic bills, a senior pet, or a houseful of animals. These picks rest on operational signal from Texas owner reports on Reddit and Quora plus our research inputs; we did not run primary Texas quote sampling. For full side-by-side comparisons, see our best pet insurance guide.

App-first and Costco-channel quote candidates: Lemonade or Figo

Austin owners reported about $35 per month for a German Shepherd puppy on Lemonade and about $28 for Figo through Costco. Those owner examples use different channels and undisclosed benefit settings, so they are not a matched carrier-price ranking. The tradeoff is annual caps: cheap tiers often carry limits one surgery can exhaust. Check the cap before celebrating the premium, or start with our cheap pet insurance guide.

Best for unlimited annual limits: Trupanion or Healthy Paws

Trupanion pairs a per-condition deductible with no annual payout cap — built for catastrophic tail risk. Healthy Paws offers an unlimited annual-limit option, but capped options can also appear depending on the pet and issued policy. Renewal increases recur in the cited owner reports, but those reports do not establish a representative increase or complaint rate. An unlimited selected tier can cost more; compare it with capped choices using identical settings.

Vet-payment workflows: Trupanion real time; Pets Best after approval

Trupanion’s VetDirect is the most-named direct-pay program in owner threads — and at a participating hospital it can adjudicate eligible charges in real time. Pets Best uses a different workflow: after claim processing and approval, a signed release can route approved payment to the vet, which does not by itself bridge checkout. Participation and timing are clinic-specific, so confirm the exact process with the Texas hospital you’d actually use before you need it.

Best for older pets: ASPCA

ASPCA Pet Health Insurance stands out for senior enrollment — it advertises no upper age limit for new policies, rare in this market, and an Austin owner’s end-of-life experience with it was one of the warmest reports in our thread sample. Senior quotes are often high at attained-age carriers, but pricing methods vary; Trupanion does not use birthdays as a direct factor.

Multi-pet comparison: an Embrace discount vs. a Healthy Paws high-limit option

Embrace may offer a multi-pet discount in an eligible quote, while Healthy Paws may offer an unlimited annual-limit selection but should not be assumed to discount multiple pets. Compare the combined matched quotes and each pet's separate deductible and terms. Go in with eyes open: one Austin household reported Healthy Paws climbing from roughly $300 per month for three dogs to $500 for two after a cancer year. We won’t invent discount percentages — carriers publish the specifics in the quote flow.

Best app-first experience: Lemonade or Spot

Lemonade and Spot offer app-first onboarding and claims tools, but no matched public dataset establishes a universal claim-speed lead. The honest caveat from owner reports: one nearly $15,000 abdominal-mass claim sat in review for more than six weeks before approval. That is one account, not a carrier average. Fast apps don’t guarantee fast adjudication on hard cases.

Texas pet insurance laws and regulations

Texas regulates pet insurance more lightly than most buyers assume. Under 28 TAC §5.5002, amended in 2021, the Texas Department of Insurance classifies pet insurance as “non-regulated” inland marine insurance — in plain English, carriers don’t need TDI’s prior approval of their rates or policy forms before selling to you.

Texas also has not adopted the NAIC Pet Insurance Model Act — the model law that standardizes disclosures on claim-payment basis, waiting periods, and pre-existing definitions — as of the NAIC’s state tracking in summer 2025. That doesn’t mean no oversight: TDI still enforces general claims-handling, unfair-trade-practice, and market-conduct standards, and runs a consumer complaint process with public complaint indexes. A separate 2024 NAIC reporting change — pet insurance got its own statutory reporting line, 9.2 — improves industry data transparency nationally, but that’s a different lever from the Texas classification rule.

How to file a complaint with TDI

Gather your policy documents and claim correspondence, contact the insurer first and document its response, then submit a complaint at tdi.texas.gov. Two honest notes: TDI’s complaint indexes are a useful pre-purchase research tool — you can check a carrier’s complaint record before you buy — and filing doesn’t guarantee an outcome. It triggers a review, not a refund.

What “non-regulated” means for you as a buyer

With no prior rate-and-form approval, the consumer-protection lever in Texas is contract comprehension, not regulation. Before enrolling, confirm in writing: the reimbursement basis (actual invoice vs. a benefit schedule), the waiting periods for each category, the pre-existing definition and its lookback window, and whether wellness is insurance or a separate prepaid plan. TDI’s own consumer guidance asks the same questions — the policy you understand is the protection you actually have.

Will my premium rise — and can I switch later?

Plan for the possibility of increases, but the mechanism is not universal. Most carriers use attained-age pricing, so a puppy quote often rises as the pet ages. Trupanion says birthdays and an individual pet's claims are not direct pricing factors, although cohort, location, and veterinary-cost changes can still produce large increases. In owner-reported renewal histories, some premiums doubled or quadrupled over five to seven years. Those reports involve different pets, locations, policy settings, and carriers, so they show possible outcomes rather than a forecast or like-for-like comparison. Whether your own claims history also moves the price depends on the carrier’s rating design: some price on pool-wide experience, some look closer to home. Rating rules vary by insurer and state; do not infer the cause of an increase from one anecdote.

Non-renewal happens too. Nationwide dropped roughly 100,000 pet policies in 2024, and owners were still untangling it a year later, with replacement offers that cost more and covered less.

Switching carriers later is possible — but never free. Related prior signs, advice, treatment, and diagnoses will usually be reviewed as pre-existing by the next carrier, subject to cure-out rules and limited state/form-specific exceptions, so a pet with three years of chart history shops with a handicap. The honest budgeting move: price the senior-years premium, not the teaser quote, and treat a switch as most valuable early, while the record is still clean.

Is insurance still worth it for an older or medically-messy Texas pet?

Two honest answers. First: pet insurance is most valuable bought early, before the chart fills up and senior pricing kicks in — nothing below changes that. Second: a policy can still protect an older pet, but only against future, unrelated catastrophes. Mainstream plans usually exclude the condition and related history that already exist, although cure-out rules and AKC's limited 365-day continuous-coverage pathway can create state/form-specific exceptions.

The cautionary version plays out in an Austin thread about a nearly 17-year-old dog, where the consensus was that useful coverage was no longer realistic. Between “too late entirely” and “still worth it,” the deciding question is what an unexpected five-figure vet event would do to your finances — owners and veterinarians alike frame insurance as protection against impossible decisions, not as a way to save money.

If your pet already carries an extensive pre-existing history, self-insuring — a dedicated savings account fed by what the premium would have cost — is a rational choice, not a failure. If you want coverage anyway, ASPCA is among the few carriers with no upper enrollment age, though senior premiums run high there too. Either way, don’t delay care to protect eligibility — the exam your pet needs today matters more than the exclusion it might create.

How to compare Texas plans — the levers that actually matter

Whatever quote tool you end up in, seven levers decide what the policy is actually worth. Check them in this order:

- Deductible structure. Annual resets every year; per-condition (Trupanion’s model) can favor chronic conditions.

- Reimbursement percentage. 70%, 80%, or 90% — the lever that scales every future payout.

- Annual limit. Capped tiers are cheaper right up until the one bill that blows past the cap.

- Exam-fee coverage. Many policies exclude the visit fee itself; Embrace offers it as an optional add-on — make sure it’s actually selected.

- Waiting periods. All four categories: accident, illness, orthopedic, wellness.

- Direct-pay availability. Confirmed at your actual hospital, not just on the carrier’s site.

- Pre-existing language. The lookback window and the bilateral-condition clause — the two lines that decide your future claims.

Wherever you are in the decision — ready to quote a carrier from the shortlist above, still weighing whether pet insurance fits at all, or rereading the senior-pet section with an old friend on your lap — one habit protects you in Texas’s lightly regulated market: get the waiting periods and the pre-existing definition in writing before you enroll.

Frequently Asked Questions

How much does pet insurance cost in Texas?

MoneyGeek's standardized Texas model reports $31 to $153 per month across its modeled profiles. Its $49 combined benchmark — $64 for its dog profile and $33 for its cat profile — uses a 6-year-old Labrador, a 7-year-old Ragdoll, a $5,000 annual limit, $500 deductible, and 80% reimbursement. These are source-specific planning figures, not a quote or carrier ranking; compare same-day matched quotes for your pet and ZIP. Our pet insurance cost guide breaks down each driver.

Does pet insurance cover hip dysplasia?

Usually yes, under accident-and-illness plans — Lemonade’s Texas policy, for example, lists hip dysplasia among covered conditions. The catch is timing: if related symptoms were documented before coverage began or during an orthopedic waiting period, mainstream plans usually exclude the condition, subject to cure-out rules and limited exceptions — and bilateral rules can extend an exclusion on one hip to both. Details in our pre-existing conditions guide.

Does pet insurance cover diabetes?

Usually yes under accident-and-illness plans, when the diagnosis comes after the illness waiting period. Insulin, glucose monitoring, and related visits may be eligible when diabetes begins after coverage and the illness wait. Earlier related signs can make it pre-existing under mainstream plans; limited state/form-specific exceptions exist. MoneyGeek’s diabetes coverage guide compares carrier policies, and our guide to what pet insurance covers shows where chronic conditions fit.

What pet insurance covers Addison's disease?

Addison’s disease may be eligible under accident-and-illness coverage once the illness wait has passed, subject to the plan's pre-existing-condition and other terms. Embrace explains its Addison’s coverage publicly. Compare options in our best pet insurance guide.

Do Texas vets accept pet insurance?

“Accepted” is the wrong mental model — most pet insurance reimburses you, not the vet, so you can use any licensed Texas veterinarian. You pay the bill, submit the claim, and get paid back. Some Texas hospitals also participate in direct-pay programs like Trupanion’s VetDirect; verify with the specific clinic before you need it.

Is pet insurance worth it in Texas?

It’s most valuable when bought early — before chart notes and senior pricing — and for owners without the cash cushion to absorb a sudden $5,000–$10,000 emergency, which Texas ERs do produce. For a young, healthy pet it’s inexpensive tail-risk protection; for an older pet with documented conditions, weigh it against self-insuring. Our is pet insurance worth it guide walks through the math.

Sources

- Average Pet Insurance Cost in Texas (2026) — MoneyGeek

- Best Pet Insurance in Texas for 2026 — U.S. News & World Report

- Pet Insurance in Texas — Lemonade

- What are you paying for pet insurance? And through whom? — Reddit r/Austin

- Anyone know where one could take a dog for emergency surgery that is affordable? — Reddit r/houston

- Best pet insurance for Texas? — Reddit r/petinsurancereviews

- Pet Insurance in the U.S. — Industry Data — NAPHIA

- Heartworm Incidence Maps — American Heartworm Society

- Kissing Bugs and Chagas Disease in the United States — Texas A&M University

- Pet Insurance in Texas — MetLife Pet Insurance

- Is pet insurance worth it? — Reddit r/petinsurancereviews

- Trupanion Direct Pay Legitimacy — Reddit r/petinsurancereviews

- Vet Direct Pay — Pets Best

- Lemonade Pet Insurance? — Reddit r/petinsurancereviews

- The Best Senior Dog Insurance — ASPCA Pet Health Insurance

- 28 TAC §5.5002 — Inland Marine Insurance — Texas Administrative Code

- Pet Insurance — NAIC

- Get Help With an Insurance Complaint — Texas Department of Insurance

- Pet Insurance: Questions to Ask — Texas Department of Insurance

- Premium increases - Trupanion — Reddit r/petinsurancereviews

- Does pet insurance go up if you use it? — Quora

- Nationwide is canceling my pet insurance — Reddit r/Insurance_Companies

- Please help, I need to find a vet for my dog — Reddit r/Austin

- What is the importance of having pet insurance? How necessary is it? — Quora

- Embrace Pet Insurance Coverage — Frequently Asked Questions — Embrace Pet Insurance

- Nationwide to drop about 100,000 pet insurance policies — CBS News

- Does Pet Insurance Cover Diabetes? — MoneyGeek

- Find Out If Addison's Disease is Covered by Pet Insurance — Embrace Pet Insurance

- State of the Industry Report 2026 Highlights (2025 data) — NAPHIA