Pet insurance is property-and-casualty insurance in a health-insurance costume. Unlike human health coverage, no U.S. law requires it to cover pre-existing conditions; you typically pay any licensed vet up front and get reimbursed afterward; and whether a claim is paid is decided by the policy form — not the brochure.

Owners learn this on exact dates. One dog tore a knee ligament five days before the orthopedic waiting period ended — turning a covered surgery into roughly $3,000 out of pocket.

The Fine-Print Index is our audit of those clauses — waiting periods, the second-knee rule, curable pre-existing windows, and exam fees — across the 22 U.S. carriers actively writing new policies. Every cell below carries a verdict label: CONFIRMED values are quoted from a binding policy document, and the few we could trace only to marketing pages are flagged † and excluded from every count.

The three findings worth quoting: across the 22 U.S. carriers actively writing policies, the special orthopedic/cruciate wait runs from zero days to a full 12 months for a single condition; only 3 carriers' binding forms permanently exclude every pre-existing condition (Trupanion, Pets Best, Odie); and — despite the reputation — only 2 of 22 bar the healthy second knee automatically (Spot, Pumpkin). The rest only do so if the first knee was already a problem before you enrolled.

Table of Contents

- How we built this index (and how to read it)

- The Fine-Print Index: all 22 carriers at a glance

- Waiting periods by company

- The orthopedic wait: the separate clock that catches everyone

- Will they cover the other knee? The bilateral rule, decoded

- "Curable" pre-existing conditions: who lets them come back

- Exam fees: the loophole on every single claim

- What restarts the clock: switching, exits, and underwriter changes

- What the comparison sites (and Google's AI) get wrong

- The rules are changing: NAIC Model Act #633 and state law

- Frequently Asked Questions

- Cite or embed this Index

- Methodology & sources

- Sources

How we built this index (and how to read it)

We audited 24 U.S. pet insurance brands and read the current binding paperwork for each — sample policies, certificates of insurance, and state insurer disclosures — not marketing pages or FAQ answers. Twenty-two of those brands are actively writing new policies, and every count in this article uses those 22 as its base.

Each cell in the Index carries a verdict label that tells you what kind of document backs it:

| Label | What it means | How we treat it |

|---|---|---|

| CONFIRMED | Quoted from a binding policy form, with the form number | Counts toward every headline stat |

| VARIES | The binding value differs by state, product tier, or form edition | Shown as a range or split out — never silently collapsed to one number |

| SOFT † | Found only in the carrier's marketing or help pages, not in a binding form we could reach | Marked with a dagger (†) and excluded from every count |

Two brands that still show up on "best pet insurance" lists have quietly stopped writing new policies — 24PetWatch (its book folded into Hartville) and Bivvy (its members moved to Spot). They appear in a separate flagged block below and are not counted; the switching section covers what happened to their policyholders.

Everything here reflects the documents as of July 1, 2026. Policy forms change, and where the newest form a carrier publishes is more than about two years old, we say so in the methodology notes at the end.

The Fine-Print Index: all 22 carriers at a glance

Here is the whole audit in one table: what each of the 22 active U.S. carriers' binding paperwork actually says about the six clauses that decide claims — from Trupanion's no-waiting-period structure to Nationwide's 12-month cruciate clock.

How to read it: unlabeled cells are CONFIRMED from a binding policy form. "Varies" means the binding value differs by state, product tier, or form edition. † marks SOFT cells — found only in marketing or help pages — which are excluded from every count in this article. Form numbers and source links for every cell are in the Methodology & sources section.

| Carrier | Underwriter | Accident wait | Illness wait | Orthopedic / cruciate wait | Bilateral (second-knee) rule | Curable window | Exam fees |

|---|---|---|---|---|---|---|---|

| Trupanion | American Pet Insurance Co. (APIC/ZPIC) | No waiting periods — ~12-day delayed start (varies) | Same; CA discloses 30 days (varies) | None | Conditional | Never | Never |

| Nationwide | National Casualty Co. (VPI in CA) | 0 days | 14 days | 12 months — cruciate/meniscus only, not waivable | Conditional | 180 days; chronic never | Base |

| Embrace | American Modern Home Ins. Co. | 48 hours or 14 days (varies) | 14 days | 180 days, dogs, 4 named conditions; reducible to 14 days via exam | Conditional | 365 days; ortho/cancer/renal carved out | Add-on |

| Healthy Paws | Westchester Fire Ins. Co. (Chubb) | 15 days (varies) | 15 days | 12 months — hip dysplasia only (varies); no hip coverage if enrolled at 6+; other ortho 15 days | Conditional (cruciate only) | 365 days † | Never |

| Lemonade | Lemonade Ins. Co. (Metromile, some states) | 0 days | 14 days | 30 days, all orthopedic, waivable via exam | Conditional | 365 days; chronic/joint never | Add-on |

| Pets Best | IAIC (new business: MS Transverse) | 3 days | 14 days | 180 days — cruciate only; waivable | Conditional | Never | Add-on |

| Figo | Independence American (IAIC) | 1 day / 0 days (varies by form) | 14 days | 180 days, dogs, waivable ≤30 days / 30 days on newer forms (varies) | None in default form / automatic knee on newer forms (varies) | 365 days; knee/ligament never | Add-on |

| AKC Pet Insurance | IAIC (PetPartners-administered) | 2 days | 14 days | 180 days cruciate + 180 days IVDD | Conditional / automatic knee on newest form (varies) | 365 days of continuous coverage (varies; absent in FL form) | Add-on |

| PetPartners | Independence American (IAIC) | 2 days | 14 days | 180 days cruciate + 180 days IVDD; waivable on newest form | Conditional / automatic knee on newest form | 365 days of continuous coverage; IVDD/knee carved out | Add-on |

| Wagmo | IAIC (US Fire in NY/WA) | 14 days | 14 days | None — rides the 14-day wait | Conditional; knee/ligament treated as one condition | 180 days; chronic + knee never | Base |

| ASPCA Pet Health | IAIC / US Fire by state | 14 days | 14 days | None on current form (12-month knee on legacy CA product — varies) | Conditional | 180 days; chronic + knee never | Base |

| Spot | Independence American (IAIC) | 14 days | 14 days | None — rides the 14-day wait | Automatic (knee/ligament) | 180 days; chronic + knee never | Base |

| Pumpkin | US Fire (CA) / IAIC (TX) | 14 days | 14 days | None — rides the 14-day wait | Automatic (knee) | 180 days; knee never | Base |

| Hartville | IAIC / US Fire | 14 days | 14 days (varies) | 14 days (12-month knee in CA — varies) | Conditional | 180 days | Base |

| MetLife Pet | Metropolitan General + IAIC, by state | 0 days (MetGen) / 1 day (IAIC) — varies | 14 days | None (MetGen) / 6 months dogs, all ortho (IAIC) — varies | Not specified † | None (MetGen) / 6 months, temporary conditions (IAIC) — varies | Base |

| Fetch by The Dodo | AXIS Insurance Co. | 0 days (accidents exempt) | 15 days | 180 days, all orthopedic; knees waivable; 30 days in FL (varies) | Conditional | 365 days, annual-exam conditioned | Base |

| Prudent Pet | Markel American Ins. Co. | 5 days | 14 days | 180 days — knee conditions; waivable ≤30 days | Conditional (knee) | 365 days † (not in binding form); knee never | Add-on † |

| Kanguro | Cimarron Insurance Co. | 2 days | 14 days | 180 days — cruciate/knee; reducible to 14 days | Conditional | 365 days; knee/ligament never | Base |

| Odie | Trisura Insurance Co. | 3 days | 14 days | 180 days — cruciate only; waivable | Conditional | Never | Add-on |

| USAA Pet | American Modern (Embrace-administered) | 0 days | 14 days | 180 days, dogs, 4 named conditions; exam-reducible in eligible states | Conditional | 365 days; the 4 ortho conditions never | Add-on |

| Companion Protect | CSAA General Ins. Co. (AAA-branded) | 0 days | 15 days | 30 days, all orthopedic | Not specified † | Never † | Base † |

| Chewy CarePlus | APIC (Trupanion tiers) / Lemonade–Metromile tier | 0 days | 12 days (Trupanion) / 14 days (Lemonade) | None (Trupanion) / 30 days (Lemonade) — varies | None stated (Trupanion) / conditional (Lemonade) | Never (Trupanion) / 365 days (Lemonade) | Varies by tier |

Exited carriers (flagged, not counted)

| Carrier | Underwriter | Accident | Illness | Ortho | Bilateral | Curable | Status |

|---|---|---|---|---|---|---|---|

| 24PetWatch | North River (Crum & Forster) | 0 days | 14 days / 30 days (Essential) | None | Conditional | 24 months, discretionary | Discontinued 2025 → Hartville |

| Bivvy | CUMIS Insurance Society | 14 days † | 30 days † | 180 days, dogs (varies) | Not specified | 12 months † | Discontinued 2023 → Spot |

One warning before you use the underwriter column as a shortcut: the same underwriter does not mean the same policy. USAA's pet policy and Embrace both run on the same American Modern policy chassis — yet USAA applies no accident waiting period while Embrace's own state disclosure lists 48 hours or 14 days, depending on the state. The underwriter tells you who pays claims; it does not tell you your terms.

How to use the Index before you buy

- Enroll before any symptoms. Every restrictive clause keys off what your vet noted before coverage begins — including during the waiting period. A "slight limp" in the chart can exclude a knee surgery years later.

- If your breed is prone to knee or hip problems, read the orthopedic column first. A 12-month, non-waivable wait is a different product from a 14-day one — even at the same premium.

- Check the exam-fee column. On frequent small claims, a base-included exam fee is worth more than a slightly higher reimbursement percentage. When you're ready to weigh price and coverage together, start with our best pet insurance picks.

Each column is decoded in its own section below — what the clause means in plain language, who sits in which bucket, and the exact policy wording that decides it.

Waiting periods by company

A waiting period is the stretch of time after your pet insurance policy starts during which claims are not yet covered. Anything that shows signs during it is treated as pre-existing — at most carriers, permanently. Nearly every policy runs separate clocks: one for accidents (0–14 days), one for illnesses (usually 14 days), and often a much longer one for orthopedic conditions.

One protection worth knowing up front: under the NAIC model definition — now law in 16 states, and how the forms we read are written — waiting periods "may not be applied to renewals of existing coverage." The clock runs when your coverage starts, not every year; switching carriers is a different story, covered below.

The accident clock is where carriers differ most:

| Accident wait | Carriers (binding forms) |

|---|---|

| 0 days | Nationwide, Lemonade, Fetch, USAA, Companion Protect, Chewy CarePlus |

| 1–5 days | Figo (1), AKC (2), PetPartners (2), Kanguro (2), Pets Best (3), Odie (3), Prudent Pet (5) |

| 14–15 days | Wagmo, ASPCA, Spot, Pumpkin, Hartville (14); Healthy Paws (15) |

| Varies | Embrace (48 hours or 14 days by state), MetLife (0 or 1 day by underwriter), Trupanion (no waiting periods — ~12-day delayed start instead) |

Illness waits cluster tightly around two weeks: 14 days at most carriers, 15 at Healthy Paws, Fetch, and Companion Protect, and 12 on Chewy CarePlus's Trupanion tiers. The 30-day illness figures you'll sometimes see quoted are edge cases — Trupanion's California disclosure† and a couple of legacy products — not the market norm.

Trupanion is the structure everyone misquotes. Its binding form has no waiting periods at all; instead, the policy simply doesn't take effect until 12 days after you enroll — or immediately, if you enroll with an Exam Day Offer at the vet's office. The "5-day accident wait" that circulates online is a stale marketing figure, not what the form says.

Which carriers cover accidents from day one?

Six carriers' binding forms apply no accident waiting period: Nationwide ("Accident coverage is not subject to a waiting period"), Lemonade, Fetch (accidents "resulting from an unexpected event do not have a waiting period"), USAA, Companion Protect, and Chewy CarePlus. MetLife is 0 days where its Metropolitan General form applies (1 day on its IAIC form), and Figo's newer state forms drop to 0 days as well. Trupanion belongs in this conversation too — no accident wait at all, just the delayed start described above.

What no carrier offers through an ordinary online signup is same-day illness coverage. The one structural exception: Trupanion's form has no waiting periods at all, so enrolling through its in-clinic Exam Day Offer makes the policy effective immediately — otherwise its ~12-day delayed start applies. Every other form we read carries an illness wait of 12–15 days, so treat "no waiting period pet insurance" ads accordingly.

What to do with this: enroll before you need the coverage, because a symptom noted during the wait becomes pre-existing (more on that in the curable-conditions section). And if you're changing carriers mid-year, remember that every clock restarts with the new policy — don't cancel the old one until the new waits have run. If you're still weighing plan types, our accident-only and accident & illness guides cover what each actually pays for.

The orthopedic wait: the separate clock that catches everyone

Most carriers run a second, much longer waiting period for orthopedic problems — torn cruciate ligaments (the classic dog knee injury), luxating patellas, sometimes hips and spines. It ranges from no special wait at all to a full 12 months, and the scope differs so much between carriers that a single "cruciate wait" number is meaningless. Here are the real tiers:

| Tier | Scope | Carriers |

|---|---|---|

| No special wait | Knee and other orthopedic conditions ride the standard wait | Trupanion, Wagmo, Spot, Pumpkin; also true on the current or default forms at ASPCA, Hartville, MetLife (MetGen), and Chewy's Trupanion tiers — all state- or form-dependent (varies) |

| 30 days | All orthopedic conditions | Lemonade (waivable via exam); Companion Protect (not waivable); Figo's newer state forms (varies) |

| 180 days | Cruciate/knee only | Pets Best, Odie, Kanguro, Prudent Pet — all waivable or reducible; AKC and PetPartners add a second 180-day clock for IVDD |

| 180 days | Dogs, broader orthopedic list | Embrace and USAA (4 named conditions, reducible to 14 days via exam); Fetch (all orthopedic, knees waivable) |

| 12 months | One single condition — not waivable | Nationwide (cruciate/meniscus); Healthy Paws (hip dysplasia — varies by state) |

Two details in the fine print do most of the damage. First, an accident doesn't necessarily rescue you: Pets Best's form defines a "Cruciate Ligament Event" as "always treated as a medical condition" — an injury reclassified as an illness so the longer clock applies. A Lemonade owner learned the same lesson when a dog fractured a femur slipping on ice during the 30-day orthopedic wait: support chat said accident-related orthopedic care was covered; the claim was denied anyway.

Second, the longest clocks cannot be waived. Nationwide's cruciate coverage "may only be available for enrollment 12 months after the initial policy inception date" — its exam waiver touches the illness wait, not this. Healthy Paws' base form runs a 12-month wait for hip dysplasia specifically (30 days and waivable in California), and adds that hip dysplasia isn't covered at all for pets enrolled at age six or older. If a torn ACL is what you're insuring against, the surgery routinely runs $4,000–$7,000 — this clause is the whole ballgame.

How to waive it (who offers an exam waiver, and the deadline)

Several carriers waive or shrink the orthopedic wait if a vet examines your pet early and finds no pre-existing knee trouble — but every offer has a deadline:

- Embrace / USAA: an Orthopedic Report Card exam after the start date cuts the 180-day wait to 14 days (eligible states).

- Lemonade: a comprehensive exam plus its Waiting Period Waiver Form, submitted within 2 days of the exam.

- Figo: an Orthopedic Waiver Form within 30 days of the effective date (default form).

- Prudent Pet: a vet exam in the first 30 days whose record notes no pre-existing knee conditions.

- Pets Best: waived or reduced when a participating vet certifies your pet's health before purchase, or with uninterrupted prior coverage.

- Kanguro: reduced to 14 days if you submit a complete medical history showing no prior knee problems.

Do it in the first week. The waiver exam is the cheapest insurance move available — and in the denial threads, the owners who skipped it say the same thing: they never thought they'd need it for a young, healthy pet.

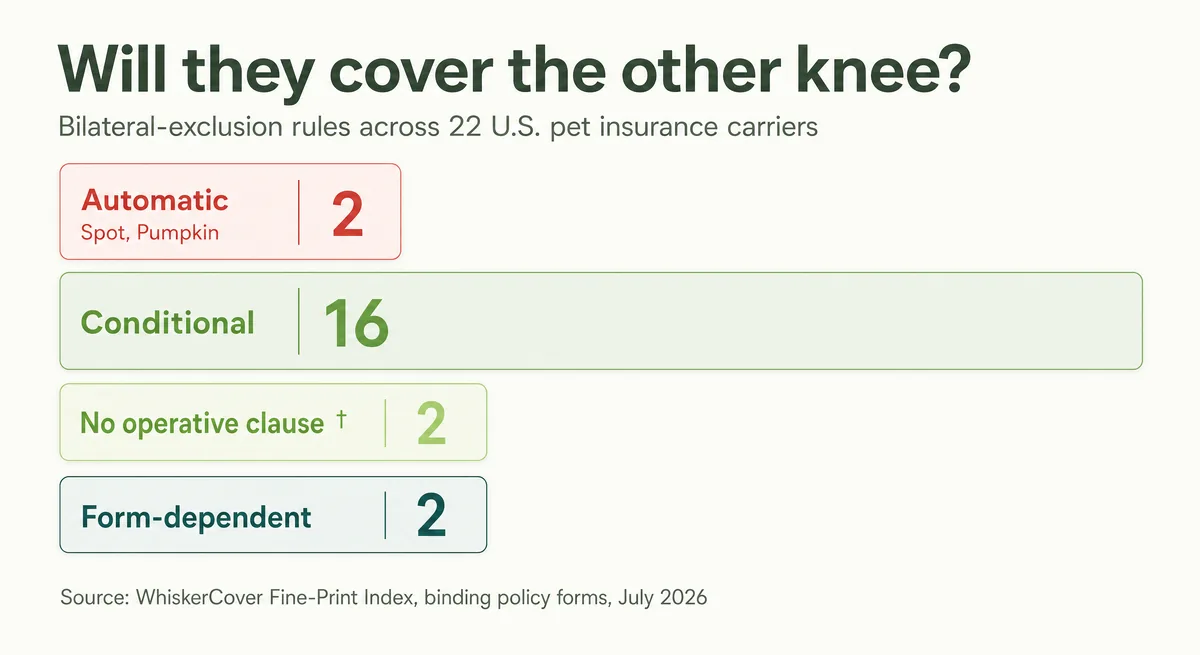

Will they cover the other knee? The bilateral rule, decoded

Usually, yes — but not always, and the difference is a single clause. Insurers call conditions that can affect both sides of the body — knees, hips, eyes, ears — bilateral conditions, and most policies carry a bilateral exclusion. What matters is which of two very different versions of that clause your carrier writes.

The automatic version links the two sides no matter what. Spot's form says knee and ligament conditions "are considered bilateral conditions and related, regardless of cause; meaning an occurrence on one side of the body affects both sides of the body." The conditional version bars the second knee only if the first was already a problem before you were covered: Embrace's form, for example, applies it when the pet "has had Clinical Signs, prior to being insured, of a Bilateral Condition on one side of the body." If the first tear happens while you're covered and past the waits, the second knee stays covered.

Across the 22 active carriers, the split looks like this: only 2 bar the healthy second knee automatically (Spot and Pumpkin); 16 apply the conditional version; 2 have no operative bilateral clause in any binding form we could reach (MetLife†, Companion Protect†); and 2 depend on which form edition your state gets (Figo, AKC).

| Rule flavor | What it means for the second knee | Carriers |

|---|---|---|

| Automatic (2) | Excluded once the first knee is affected — even if the second was always healthy | Spot, Pumpkin (knee/ligament conditions) |

| Conditional (16) | Excluded only if the first knee was pre-existing or showed signs during a waiting period | Trupanion, Nationwide, Embrace, Healthy Paws, Lemonade, Pets Best, PetPartners, Wagmo, ASPCA, Hartville, Fetch, Prudent Pet, Kanguro, Odie, USAA, Chewy CarePlus (Lemonade tier) |

| No operative clause † (2) | Only the ordinary pre-existing rule applies | MetLife†, Companion Protect† |

| Form-dependent (2) | Conditional on older forms; automatic for knees on the newest templates | Figo, AKC |

One honest footnote to the conditional group: several of its members (Wagmo, ASPCA, Prudent Pet, and PetPartners' newest form) define knee and ligament conditions as related once one side is triggered — conditional in mechanism, but close to automatic in feel once a pre-existing knee is on file. The per-carrier rows in the matrix above carry each carrier's exact flavor.

This clause produces the most predictable denial in pet insurance. One Lemonade owner put it plainly: "I submitted a claim to Lemonade and was denied due to a 'Pre-existing Bilateral Condition.' But that leg was always fine" — the first tear pre-dated the policy by three years, which is exactly what the conditional clause keys on. And the number owners trade in the forums — that roughly 60% of dogs who blow one cruciate eventually blow the other — is community folklore, not an actuarial statistic; we couldn't trace it to a published study, so treat it as a rough warning, not a probability.

So the widely repeated line that "18 of 22 carriers have a bilateral exclusion" is technically true and materially misleading. The clause exists almost everywhere; the version that punishes a perfectly healthy second knee exists at exactly two carriers. Read your form's "Bilateral Condition" definition and find the trigger — "regardless of cause" is the phrase that should give you pause.

"Curable" pre-existing conditions: who lets them come back

A curable pre-existing condition is one your policy will cover again after your pet stays symptom-free and treatment-free for a set window — usually 180 or 365 days, subject to each policy's exclusions. Three carriers' binding forms offer no curable window at all: Trupanion, Pets Best, and Odie. And nearly every window that does exist carves out knees.

| Window | Carriers | What never comes back |

|---|---|---|

| Never | Trupanion, Pets Best, Odie | Everything pre-existing stays excluded |

| 180 days | Spot, Pumpkin, ASPCA, Hartville, Wagmo; Nationwide (by written reconsideration request) | Chronic conditions everywhere; knee/ligament conditions at all of them |

| 365 days | Embrace, USAA, Lemonade, Figo, Kanguro, Fetch (annual-exam conditioned); AKC via a continuous-coverage pathway (varies) | The named orthopedic conditions, chronic/joint disease, knee/ligament — carrier by carrier |

| Marketing-only † | Healthy Paws (365d †), Prudent Pet (365d †), Companion Protect (Never †); MetLife varies by underwriter | Not in a binding form we could reach — excluded from the counts above |

The carve-outs are the real story: "curable" has a knee-shaped hole. An ear infection that clears up can be covered again after the window; a torn cruciate cannot. Spot's form says it directly — the 180-day rule "does not apply to chronic conditions or ligament and knee conditions" — and Embrace's marks its four orthopedic conditions as pre-existing "for the life of the policy."

The second trap is how "pre-existing" gets decided in the first place. Under the NAIC model definition, a condition is pre-existing if your pet had "signs or symptoms directly related to the condition" before coverage begins — including during any waiting period — no diagnosis required. Your vet's notes are the contract: a Spot policyholder had a $380 dermatitis-and-ear-infection claim denied off a single prior-year ear infection in the chart. If a symptom sits in the chart, assume the carrier will count the symptom-free window from that note — diagnosis or not.

Two reputations deserve correcting. Healthy Paws is widely believed to be a fourth "Never" — in fact its binding form shows a permanent pre-existing exclusion, while a 365-day cure window appears only in its help pages†, so it is neither a confirmed Never nor a confirmed window. And AKC's current forms are the one broad exception in the market: pre-existing conditions become eligible again after 365 days of continuous coverage — but the pathway is form- and state-dependent (it's absent from the Florida sample), so verify it exists in your state's paperwork before counting on it.

One thing that is not a workaround: hiding a symptom by switching vets. Concealing records or answering application and claim questions falsely is misrepresentation that can rise to insurance fraud — and carriers request full histories from every clinic your pet has visited when the first significant claim arrives. For the fundamentals, our pre-existing conditions guide covers what counts, what doesn't, and what to do if your pet already has a chart.

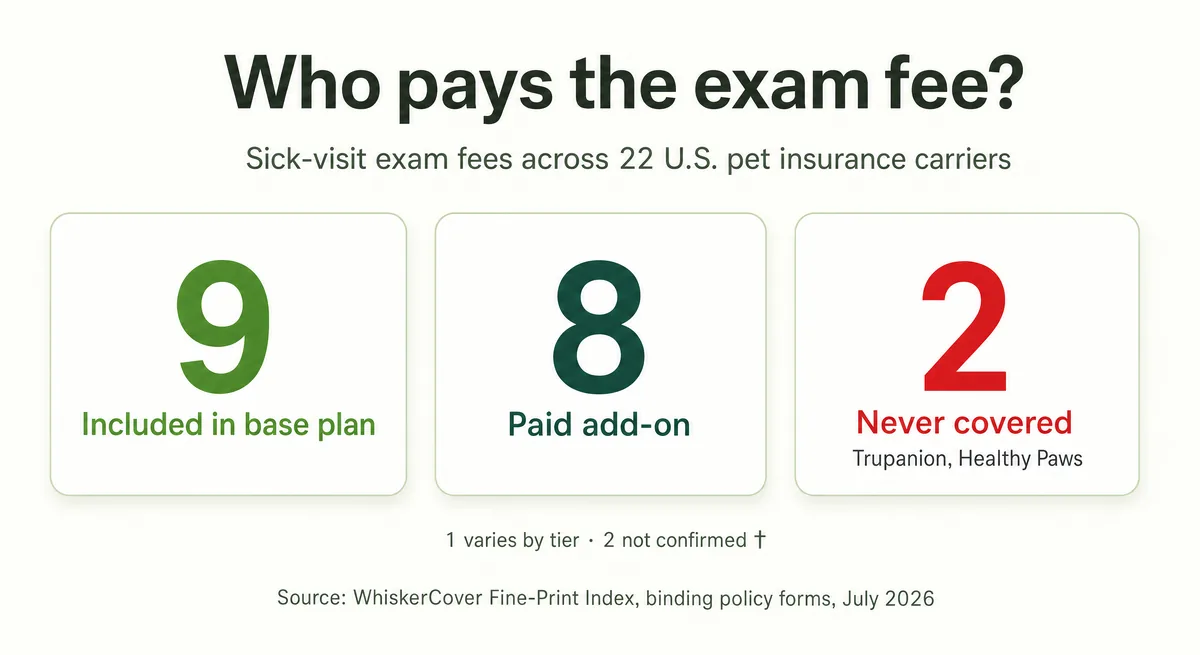

Exam fees: the loophole on every single claim

Almost every claim starts the same way: a vet examines your pet, and that exam — the office-visit or consultation charge — lands on the invoice before any treatment does. Whether your policy reimburses it is a three-way split. Of the 22 active carriers, 9 include exam fees in the base plan (Nationwide, Wagmo, ASPCA, Spot, Pumpkin, Hartville, MetLife, Fetch, Kanguro), 8 sell them back as a paid add-on (Embrace, Lemonade, Pets Best, Figo, AKC, PetPartners, Odie, USAA), and 2 never cover them at all — Trupanion and Healthy Paws. Chewy CarePlus varies by tier, and two cells are marketing-only (Companion Protect base†, Prudent Pet add-on†).

Trupanion's binding form doesn't hide the position: "We do not cover Examination fees of any kind… We consider Examination fees to be Your Share of Your Pet's medical needs."

On a routine claim that's an annoyance. On a long treatment protocol it compounds into a toll: one Trupanion policyholder running a 26-week lymphoma chemo protocol found that every weekly infusion carried a "recheck" exam line the policy never covers — "around $400 a week" out of pocket, on a plan that pays 90% of covered costs. (Owners in that thread note a quirk our matrix confirms: Trupanion bought through Chewy's CarePlus Complete tier does cover exam fees.)

Here's the arithmetic — illustrative math, not a claims statistic. Take a $600 sick visit where $150 is the exam fee. A "90%" plan that excludes exam fees reimburses 90% of $450, or $405 — which is 67.5% of the real bill. That is how a 90% plan quietly pays about 70% in practice, before deductibles.

Two clarifications so this lands fairly. First, the sick-visit exam fee is not the annual wellness checkup — routine wellness exams are a separate rider at essentially every carrier, and bundling them in would just move the cost into premiums. Second, terms predict outcomes in both directions: the same Trupanion structure that never pays exam fees also has no orthopedic wait and no payout caps, and its satisfied customers are just as specific — one owner reports "$54,400 paid for 4 TPLOs + cancer across 3 dogs." Read the cell, not the brand reputation.

What restarts the clock: switching, exits, and underwriter changes

Switching carriers restarts the clocks. Unless the new carrier credits continuous prior coverage or grants a waiver exam (a few do — see the orthopedic section above), the new policy re-runs its waiting periods, re-opens the pre-existing look-back, and — this is the part that stings — turns conditions your old carrier covered into pre-existing conditions at the new one. The NAIC model rule that waiting periods "may not be applied to renewals" — where enacted — protects renewals with the same insurer; a new carrier is a new clock.

And you don't always choose the switch. 24PetWatch stopped writing its own-brand policies and its book was folded into Hartville; in one thread from that migration, two Colorado owners report TPLO knee surgeries denied because a 2023 CCL claim "was excluded from rollover when they switched companies" — a $4,000 surgery, covered history and all, reclassified in the move. Bivvy's exit in 2023 moved its members to Spot the same way. Underwriters move under brands, too: Pets Best's new business shifted from Independence American to MS Transverse in September 2025 — the brand on your card stays the same while the paper behind it changes, and terms live in the paper.

None of this means never switch — premium hikes are real, and staying locked into a bad plan has its own cost. It means switch informed:

- Pull your pet's full records first and read every note — the new carrier will. A stray symptom line is tomorrow's pre-existing condition.

- Overlap the policies: keep the old one active until the new policy's waiting periods — including the orthopedic clock — have fully run.

- Sign the new carrier's waiver exam on day one, where offered (see the orthopedic section above for who offers one and the deadlines).

- Price the lock-in, not just the premium: a condition covered today may never be covered again after the move.

We walk through the full decision — when switching pays off, when it's financially dangerous, and the records checklist — in our switching pet insurance guide and its companion on how pet insurance works if you switch.

What the comparison sites (and Google's AI) get wrong

Most of the waiting-period numbers circulating online trace to marketing pages and to other comparison sites — not to policy forms. Google's AI Overviews then quote those aggregators, and the wrong figure becomes the figure everyone "knows." We checked the most-repeated claims against the binding documents; here is where they part ways:

| The claim in circulation | What the binding form says |

|---|---|

| "Trupanion: 5-day accident wait, 30-day illness wait" (Google's AI Overview, echoing marketing framing) | "This policy does not have any waiting periods" — coverage starts ~12 days after enrollment (immediately with an Exam Day Offer). The 30-day illness figure is a California disclosure, not the national form. |

| "Lemonade: 2-day accident wait" | 0 days — the form's waiting-period schedule lists only illness (14 days) and orthopedic (30 days); accidents are covered from the start date. |

| "Companies like Trupanion will usually exclude the other knee" | Conditional only — the second side is barred solely if signs showed "on either side of their body before Your Pet's Effective Date." Trupanion also has no special cruciate wait at all. |

| "The cruciate waiting period is 6–12 months" | There is no one number. Four carriers apply no special wait, Lemonade 30 days, nine carriers 180 days (ten counting Figo's default form) at very different scopes, and only Nationwide reaches 12 months — for cruciate/meniscus alone. |

| "Nationwide accident: 24 hours (or 14 days)"; "USAA accident: 2 days" | Both are 0 days on the current binding forms — "Accident coverage is not subject to a waiting period" (Nationwide), and no separate accident wait in the PET50 form (USAA). The old figures are stale form generations. |

None of this makes the aggregators villains — a few thin tables genuinely try. But their cells cite "publicly available information," the AI Overview cites them, and the loop closes with an owner budgeting around a number that was never in any contract. When a figure here disagrees with one you've read elsewhere, the tiebreaker is simple: ask which of the two is quoting a policy form. That standard is the entire reason this index exists.

The rules are changing: NAIC Model Act #633 and state law

The fine print above isn't static — a model law is slowly standardizing it. The NAIC Pet Insurance Model Act (#633), adopted in August 2022, defines "pre-existing condition," "orthopedic," and "waiting period" in statute, caps illness and orthopedic waiting periods at 30 days, and prohibits accident waiting periods outright in the states that enact it.

As of this audit, 16 states have adopted the Model Act: California, Delaware, Florida, Hawaii, Louisiana, Maine, Maryland, Mississippi, Montana, Nebraska, New Hampshire, Ohio, Pennsylvania, Rhode Island, Vermont, and Washington. (California's version is SB 1217, enacted in 2024 and effective January 1, 2025.) Illinois and Virginia — often listed as adopters — have not adopted it. This map is why so many cells in the Index read "varies" — and why some carriers' newer state editions look nothing like their default forms: Figo's 30-day orthopedic editions and Fetch's 30-day Florida wait both live in adopting states, while the same carriers' default forms run 180 days elsewhere.

Accountability data is arriving too. The NAIC's Market Conduct Annual Statement added a pet insurance line covering 2024 data, first filed April 30, 2025 — with a $0 premium threshold, so essentially every pet insurer files. It tracks claims closed without payment by reason code: ineligibility, pre-existing condition, waiting period, benefit-limit, below-deductible, and hereditary/chronic exclusions. In plain terms: regulators are now counting exactly the denials this article catalogs.

For scale, this is no longer a niche product. Per NAPHIA's 2025 State of the Industry report, U.S. pet insurance wrote about $4.7 billion in premium in 2024 (up 21.4%), covering roughly 6.4 million pets — still only 3.9% of the nation's dogs and cats — at an average accident-and-illness premium of $749.29 for dogs and $386.47 for cats per year.

Frequently Asked Questions

What is usually not covered by pet insurance?

Pre-existing conditions are the big one — anything that showed signs before your coverage started, including during a waiting period. Beyond that, the common gaps are clause-driven: conditions arising during waiting periods, the "other side" of a bilateral condition at some carriers, exam fees (never covered at Trupanion and Healthy Paws, an add-on at eight others), and routine or wellness care unless you buy a separate rider. The exact rules differ carrier by carrier, which is what the Index above maps.

Can I get pet insurance and use it straight away?

For illnesses, almost never — carriers apply illness waiting periods of 12 to 15 days, and Trupanion (whose form has no waiting periods) instead delays the whole policy's start by about 12 days; only its in-clinic Exam Day Offer makes coverage effective immediately. For accidents, six carriers cover from day one: Nationwide, Lemonade, Fetch, USAA, Companion Protect, and Chewy CarePlus. Nothing you buy today covers a problem your pet already has.

What is the shortest waiting period for pet insurance?

Zero days for accidents — Nationwide, Lemonade, Fetch, USAA, Companion Protect, and Chewy CarePlus all cover accidents from the policy's start date. For illness, the shortest confirmed wait is 12 days (Chewy CarePlus's Trupanion tiers); most carriers run 14. No carrier truthfully offers a zero illness wait, so treat "no waiting period pet insurance" ads as marketing shorthand.

Why is there a separate waiting period for cruciate or orthopedic problems?

Because torn knee ligaments are the most predictable big claim in pet insurance, many carriers run a second, longer clock for them. The scope varies enormously: four carriers apply no special wait, Lemonade waits 30 days, nine carriers wait 180 days (ten counting Figo's default form) (some cruciate-only, some all-orthopedic for dogs), and Nationwide's cruciate/meniscus wait runs a full 12 months and cannot be waived. Several carriers will shrink the wait if a vet certifies your pet's knees early — see the waiver list above.

Will pet insurance cover my dog's other knee?

At most carriers, yes — if the first knee problem happened while you were insured and past the waiting periods. Only 2 of 22 carriers (Spot and Pumpkin) exclude the healthy second knee automatically once one knee is affected, regardless of cause. Sixteen carriers apply a conditional rule: the second knee is barred only if the first was pre-existing. Check your form's "Bilateral Condition" definition; "regardless of cause" is the phrase that signals the strict version.

What counts as a pre-existing condition?

Any condition your pet showed signs or symptoms of before coverage began — including during any waiting period — even without a diagnosis. That's the NAIC model definition, and it means your vet's chart notes function as the contract: a single "loose stool" or limp notation can anchor a later denial. Carriers pull full medical records when the first significant claim arrives. Our pre-existing conditions guide covers what to do if your pet already has a chart.

Can a cured condition be covered again?

Often, yes — if your carrier's form has a curable window and your pet stays symptom-free and treatment-free through it. The confirmed windows run 180 days (Spot, Pumpkin, ASPCA, Hartville, Wagmo; Nationwide by written reconsideration request) or 365 days (Embrace, Lemonade, Figo, Kanguro, USAA, Fetch — plus AKC and PetPartners via continuous-coverage pathways). Three carriers never re-cover a pre-existing condition: Trupanion, Pets Best, and Odie. And nearly every window carves out knee and ligament conditions — an ear infection can reset; a torn cruciate can't.

Does pet insurance cover exam fees?

It depends on the carrier, and it's a three-way split: 9 of 22 include sick-visit exam fees in the base plan (Nationwide, Wagmo, ASPCA, Spot, Pumpkin, Hartville, MetLife, Fetch, Kanguro), 8 sell them as a paid add-on (Embrace, Lemonade, Pets Best, Figo, AKC, PetPartners, Odie, USAA), and 2 never cover them (Trupanion, Healthy Paws). On a long treatment plan, an uncovered exam fee recurs on every single visit — it's worth pricing before you enroll.

Can I avoid or reduce a waiting period?

Sometimes — several carriers waive or shorten the orthopedic wait if a vet examines your pet early and notes healthy knees: Embrace and USAA (Orthopedic Report Card exam, eligible states), Lemonade (waiver form within 2 days of the exam), Figo (waiver form within 30 days), Prudent Pet (exam in the first 30 days), Pets Best (pre-purchase vet certification), and Kanguro (submitting complete medical history). Do it in the first week. Nationwide's 12-month cruciate clock is the exception — no exam waives it.

Do waiting periods start over if I switch pet insurance?

Yes. A new carrier means every waiting period runs again, the pre-existing look-back reopens, and conditions your old policy covered become pre-existing at the new one. The NAIC rule that waiting periods can't apply to renewals only protects renewals with the same insurer. If you switch, keep the old policy active until the new policy's waits — including the orthopedic clock — have fully run.

Will any pet insurance cover pre-existing conditions?

One carrier has a broad pathway: AKC Pet Insurance's current forms make pre-existing conditions eligible again after 365 days of continuous coverage — but it's form- and state-dependent (absent from the Florida sample), so verify it in your state's paperwork. Elsewhere, only curable conditions can return, after a 180- or 365-day symptom-free window. Hiding a condition by switching vets is not a workaround — concealing records is misrepresentation that can void coverage, and carriers request records from every clinic your pet has visited.

What voids pet insurance or gets claims denied?

Almost every denial maps to a policy term: the condition was pre-existing (signs before coverage, including during a waiting period), the claim fell inside a waiting period, a bilateral clause linked it to an earlier problem, the line item was an excluded exam fee, or a benefit limit was reached. Misrepresenting your pet's history on the application can void the policy entirely. Since 2025, regulators track denial reasons through the NAIC's Market Conduct Annual Statement — the same categories this article decodes.

Are many pet insurance brands actually the same company?

Many share an underwriter, but not the same terms. Figo, AKC and PetPartners run on Independence American (IAIC) paper — and Pets Best's new business moved to MS Transverse in September 2025; ASPCA, Spot, Pumpkin and Hartville sit on the same Crum & Forster form family; Embrace and USAA share American Modern's policy chassis. Yet the terms still differ where it counts: USAA applies no accident waiting period while Embrace's state disclosure lists 48 hours or 14 days — on the same underwriter. The underwriter tells you who pays claims, not what your terms are.

Methodology & sources

Every cell in this Index traces to a specific document. Here are the receipts — the binding form (or, where noted, insurer disclosure) behind each carrier's row, with the form number and edition we audited as of July 1, 2026:

Three carriers publish notably old paperwork, and their rows inherit that risk: Prudent Pet's live sample is the 2016 form generation, Healthy Paws' is dated 07/18 (re-served December 2025), and the Embrace/USAA PET50 edition is 01/23. Where a newer binding document exists in your state, it controls. Regulatory facts come from the NAIC (Model Act #633, the ST-633 adoption page, and MCAS materials) and NAPHIA's State of the Industry report — all linked in the Sources list below.

WhiskerCover is a licensed insurance agency, and this Index is deliberately non-commercial — no carrier paid for placement and none of the links above are affiliate links. Accuracy is the whole point: a confidently wrong cell is worse than a blank one. Our editorial policy covers how we source and correct.

If you're a journalist, a vet team, or a rescue putting together adoption packets: cite or reproduce this index with attribution to WhiskerCover, and if you find a cell that a current binding form contradicts, tell us — the escalation path here is re-reading the form, and we correct publicly.

And if you came here mid-decision: ready to choose a plan, our carrier comparison weighs these rules alongside pricing and claims reputation; already dealing with a denial, start with the appeal-and-records checklist in the switching guide before you consider moving carriers.

Cite or embed this Index

Writing about pet insurance — a blog post, a vet-clinic handout, a rescue’s adoption packet? You’re welcome to cite or reproduce this Index with attribution to WhiskerCover; if you find a cell a current binding form contradicts, tell us and we correct publicly. To drop the headline findings straight into your own page, copy the embed code with the button below — it carries a link back to the full, sourced data.

This is what it looks like:

| 0–12 mo | orthopedic/cruciate waiting-period range — Nationwide’s 12-month cruciate wait can’t be waived |

| 2 of 22 | bar the healthy second knee automatically (Spot, Pumpkin) — the rest only if it pre-dated your policy |

| 3 | carriers never re-cover a pre-existing condition (Trupanion, Pets Best, Odie) |

| 2 | never reimburse the exam fee on any claim (Trupanion, Healthy Paws) |

Sources

- Pet Insurance Model Act (#633) — NAIC

- Torn CCL five days before the waiting period ended (owner thread) — Reddit r/petinsurancereviews

- Trupanion policy form TRU (C) 00001 V02.202206 (regulator-filed copy) — Maine Bureau of Insurance

- Nationwide Modular Pet Insurance coverage form VS-G-15 (3-26) — Nationwide

- American Modern sample policy PET50 (01/23) — Embrace/USAA chassis — Embrace Pet Insurance

- Embrace insurer disclosure of important policy provisions (California) — Embrace Pet Insurance

- Trupanion insurer disclosure TRU (C) 00012 ME (regulator-filed copy) — Maine Bureau of Insurance

- Lemonade sample pet policy LEM-PET 09-23 — Lemonade

- Fetch sample policy form GPTM 050 0125 A — Fetch by The Dodo

- AAA Pet Insurance insurer disclosure (CSAA General Insurance Company) — CSAA / Companion Protect

- Chewy CarePlus (Trupanion) sample policy provisions — Chewy

- MetLife Pet sample policy PET21-01-V (Metropolitan General) — MetLife Pet Insurance

- Pets Best policy booklet IAIC-PB10001-ILL (Delaware sample) — Pets Best

- Femur fracture denied during the 30-day orthopedic wait (owner thread) — Reddit r/petinsurancereviews

- Healthy Paws sample policy LD-50812 (07/18) — Healthy Paws

- Figo sample policy IAIC FPI POL 0320 — Figo

- Kanguro sample policy PETPOL TRAD-ENG (02/25) — Kanguro

- Pumpkin sample policy PET-P-20000-1024 (Texas, March 2026) — Pumpkin

- Second CCL denied as 'Pre-existing Bilateral Condition' (owner thread) — Reddit r/petinsurancereviews

- $380 claim denied off a prior-year ear infection (owner thread) — Reddit r/petinsurancereviews

- Healthy Paws frequently asked questions (curable-conditions policy) — Healthy Paws

- AKC Pet Insurance sample policy IAIC PPI AI POL 007 1120 (Arizona) — AKC Pet Insurance / PetPartners

- 26-week chemo protocol and the never-covered weekly recheck fee (owner thread) — Reddit r/petinsurancereviews

- Trupanion cancellation thread with satisfied-customer counterpoint ($54,400 paid) — Reddit r/petinsurancereviews

- 24PetWatch-to-Hartville migration TPLO denials (owner thread) — Reddit r/Insurance

- Bivvy pet insurance review (discontinuation and Spot migration) — Canine Journal

- Pets Best underwriters & licensing — Pets Best

- Model Act #633 state adoption page (ST-633) — NAIC

- Market Conduct Annual Statement — 2024 data year (pet insurance line) — NAIC

- State of the Industry Report 2025 (data year 2024) — NAPHIA

- PetPartners sample policy IAIC PPI AI POL (007 series) — PetPartners

- Wagmo sample policy PET-P-20000-1024 (Texas) — Wagmo

- ASPCA / Hartville sample policy PET-P-20000-1024 (V47, Texas) — Hartville / ASPCA Pet Health Insurance

- Prudent Pet sample policy MPT1001-1016 (Ultimate Plus) — Prudent Pet

- Odie sample policy TRSA-OPI-PC101-ILL (Trisura, effective 1.1.26) — Odie Pet Insurance