If you're reading this, something probably pushed you here: a renewal letter with a bigger number, a plan being retired, or a claim that came back denied. You want out — but you're worried about losing coverage for the very condition that made the policy worth having in the first place.

Here's the one thing to understand before anything else: switching pet insurance isn't a transfer. You're canceling one contract and starting a brand-new one with a different company — and your coverage, the waiting periods you've already cleared, and your pet's covered conditions don't come along for the ride.

That sounds alarming, but a switch can absolutely be done right. This guide walks the whole process step by step: what actually happens when you switch, how the new insurer decides what counts as "pre-existing," what resets and what doesn't, the documents that make your first claim actually pay, and when you're better off not switching at all — or just adjusting the plan you already have.

Table of Contents

- The short answer

- What actually happens when you switch (the mechanics)

- How the new insurer decides what's "pre-existing" (claim-time underwriting)

- What resets — and what doesn't

- Pre-existing conditions vs waiting periods vs age/breed exclusions

- Before you switch — can you adjust your current policy instead?

- How to switch without losing coverage (step by step)

- The document checklist (and what each proves)

- Overlap, two policies, and changing clinics

- When switching is safe vs dangerous (per-pet triage)

- Limited exceptions that can preserve coverage

- If your insurer is non-renewing or changing your plan (involuntary switching)

- Is switching actually worth it?

- Frequently Asked Questions

- Sources

The short answer

Switching pet insurance means canceling one policy and starting a brand-new one — your coverage doesn't transfer. Here's how it works:

- The new insurer issues a fresh contract and runs its own underwriting and medical-records review.

- Waiting periods restart — accidents are usually covered within a few days, illnesses after a short waiting period (commonly about two weeks).

- Conditions your pet was already treated for are typically excluded as pre-existing.

- Never cancel the old policy until the new one is active and past its waiting periods — overlap the two so you don't open a coverage gap.

What actually happens when you switch (the mechanics)

Here's the mechanical reality behind that reframe: switching isn't a transfer, and it isn't a renewal with a new company. You cancel one contract and the new insurer writes a brand-new one. Pet insurance is legally a property-insurance contract between you and one specific carrier — which is precisely why coverage doesn't follow your pet from one company to the next (the NAIC Pet Insurance Model Act defines the product this way).

So the new company starts from zero. It applies its own waiting periods, its own definition of "pre-existing," and — typically on your first claim — runs its own review of your pet's medical records. Getting approved for a new policy is not the same as preserving coverage for the conditions your old policy already paid on.

The part most people miss: a condition can count as pre-existing without ever being formally diagnosed. Under the model act's definition, documented signs or symptoms are enough — a "mild heart murmur" or "occasional limp" noted by your vet years ago can be traced back and excluded later (PetPlace explains this symptom-level standard clearly).

How the new insurer decides what's "pre-existing" (claim-time underwriting)

Here's the mechanic that explains nearly every switching horror story: most carriers don't underwrite when you enroll — they underwrite when you claim. The new company happily takes your premium on day one without examining your pet. Then, on your first claim, it requests the invoice, the claim form, and your pet's full, vet-stamped medical history, and combs backwards from the condition you're claiming. "They never examined my pet, so I'm covered" is the single most expensive misconception in this whole process.

And it isn't only formal diagnoses that count. A charted symptom — even an offhand owner remark the vet wrote down — can be enough; the standard is symptom-level, not diagnosis-level. Owners describe the fallout vividly: in one widely shared account, a Great Dane's second cruciate surgery was denied as pre-existing because the first knee had been treated under the old insurer — paid only after the surgeon re-attributed the cause — and a single bout of diarrhea can see a whole category of future GI claims excluded.

A few practical tells follow. A chronic condition mid-treatment betrays its own timeline — a heart problem you've been medicating "for a while" can't plausibly be brand-new. If your pet hasn't been examined recently when coverage starts, the insurer may contest your first post-waiting-period claim — paying a clearly fresh injury but disputing anything that could predate coverage, like a lump, early arthritis, or a half-healed strain. And while the policy usually lets the insurer pull every record, how far back they actually review varies by carrier — so never count on a clean cutoff for an older, long-resolved condition.

One caveat: carriers aren't identical. Some do ask health questions at application, and an undisclosed condition can void the policy outright — so always answer honestly.

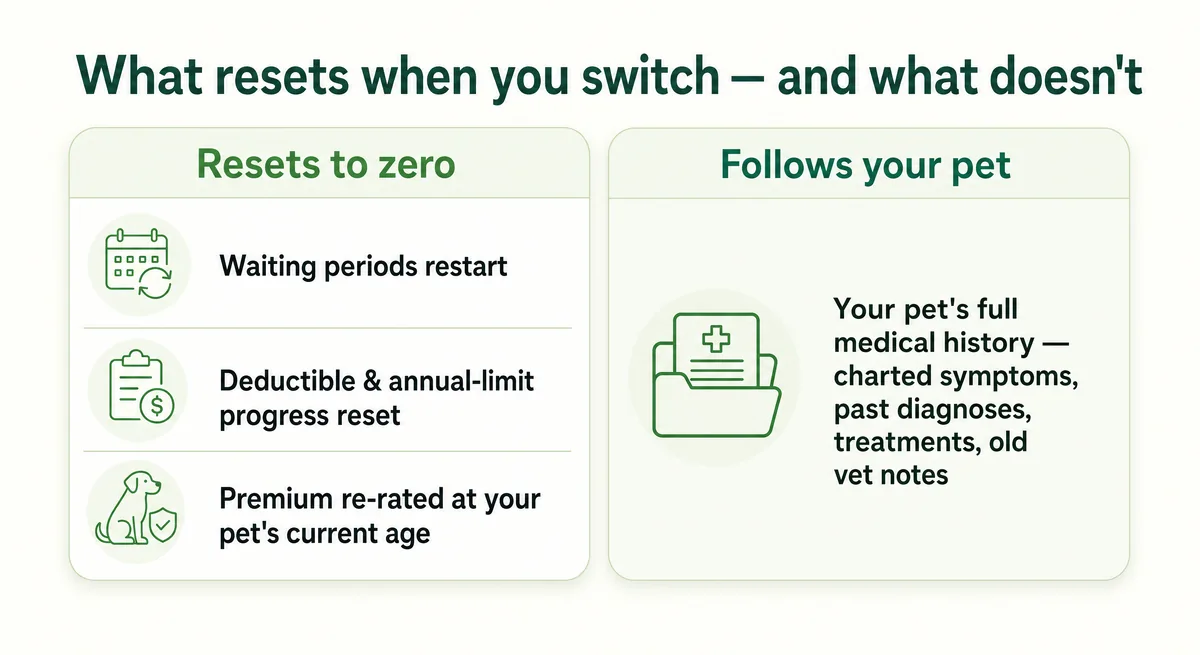

What resets — and what doesn't

When you switch, several clocks and counters drop back to zero. The one thing you'd most want to reset — your pet's history — doesn't.

Waiting periods restart

Because a switch is a new policy, not a renewal, you serve the new insurer's waiting periods from scratch — and there's no universal number. The NAIC model act prohibits accident waiting periods, caps illness and orthopedic waits at 30 days, and calls for a vet-exam waiver provision — but state adoption varies, and market practice often differs. In practice, accidents are usually covered within a few days, illnesses after about 14 days, and orthopedic or cruciate conditions are the real gotcha — commonly around six months, though the exact wait varies widely by state and policy form. Some states cap it: Washington limits illness and orthopedic waiting periods to 30 days and requires an exam-based waiver. That waiver is the escape hatch — some carriers will drop the long orthopedic wait if you submit a recent clean vet exam, so ask and get it in writing.

Deductible and annual-limit progress reset to zero

Whatever you'd paid toward this year's deductible and annual limit with the old insurer doesn't carry over — both counters start fresh. Deductible type matters too: an annual deductible resets once a year, while a per-incident or lifetime deductible works differently, so compare like for like. And a condition that already ate through your old limit is the same active condition to a new insurer — usually now pre-existing.

Your premium re-rates at your pet's current age

The new insurer prices your pet at its age today, not the age you first insured it. Because risk climbs steeply with age — and the model act requires insurers to disclose age-based pricing — a cheaper-looking quote can evaporate once age re-rating and forfeited coverage are counted. New limits or age rules can leave you worse off, not better — a few dollars off the monthly premium mean little against a now-denied chronic condition.

What does not reset: your pet's medical history

This is the one that stings. Every symptom, claim, diagnosis, treatment, and old vet note follows your pet — it's exactly what the new insurer reads at claim time. New policy, same history.

Pre-existing conditions vs waiting periods vs age/breed exclusions

These three get tangled together constantly, but they're not the same — and the difference decides whether coverage is delayed, gone for good, or never offered:

- Waiting period — temporary. A short window before a new policy's coverage activates (a few days for accidents, about two weeks for illness, longer for orthopedic). It clears with time; nothing is permanently excluded.

- Pre-existing exclusion — usually permanent. A condition your pet already showed signs of is carved out of the policy — for a chronic or incurable condition, no amount of waiting undoes it. (A few curable conditions are the narrow exception — see below — and we cover what counts as a pre-existing condition separately.)

- Age cap / breed exclusion — built in. Some insurers won't enroll pets past a certain age, charge older pets more, or exclude breed-linked hereditary conditions. These live in the policy terms, not your pet's history.

Mixing them up is the biggest source of switching confusion — a waiting period feels like a denial, but isn't one.

Before you switch — can you adjust your current policy instead?

Switching is rarely the only lever, and often not the best one. Before you cancel anything, ask your current insurer what you can change in place. You can usually adjust your deductible or reimbursement percentage — and sometimes negotiate — without forfeiting the coverage you've already built. The big advantage: because your existing insurer already knows your pet's history, adjusting an existing policy usually doesn't trigger a fresh waiting period, so the conditions it already covers stay covered (usually — confirm it for your specific change).

The trap to watch for. One kind of "adjustment" can quietly re-underwrite you even at the same company: raising your annual limit or reimbursement level. Owners report that bumping up your coverage can trigger fresh underwriting for the increased portion — potentially treating conditions you're already managing as pre-existing against the higher limit. The rules vary by carrier and policy form, so ask in writing exactly how your specific change affects existing conditions before you make it.

So ask one explicit question before you change anything: "Does this adjustment trigger re-underwriting or a new waiting period?" — and get the answer in writing. If the math still favors leaving, our guide on whether switching is worth it walks through the full decision.

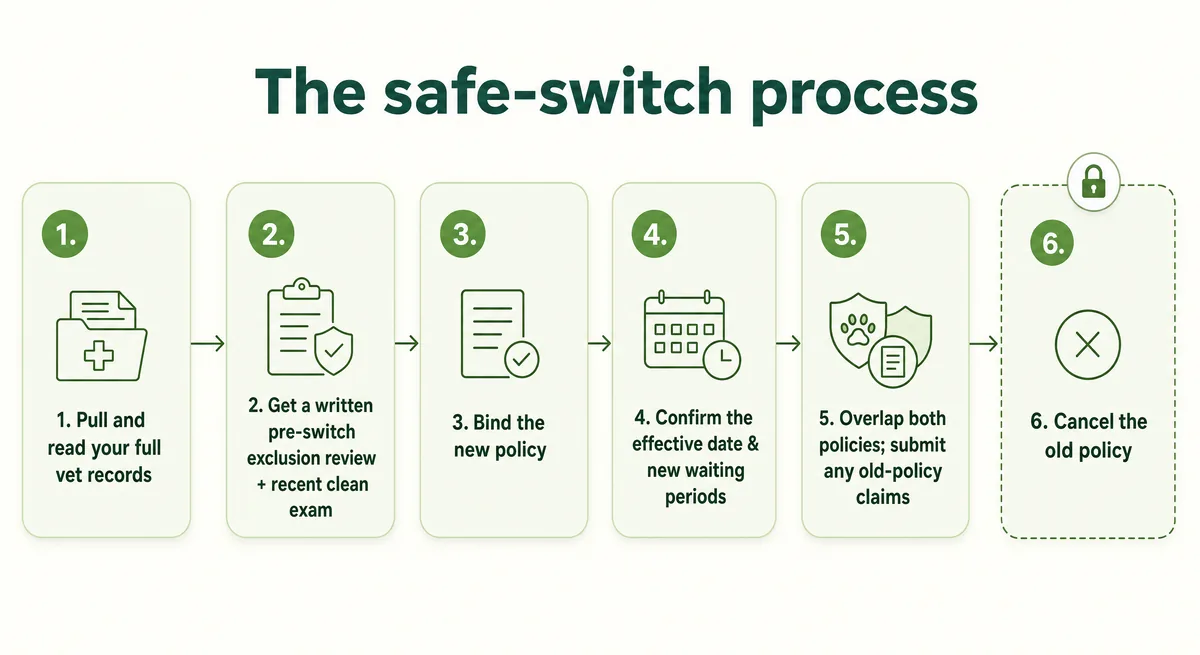

How to switch without losing coverage (step by step)

"Don't cancel first" is the headline, but a safe switch is a full sequence. Work through it in order:

- Pull your pet's full vet records and claim history — then read them the way an adjuster will. Every charted symptom, note, and past treatment is what the new insurer scans at claim time.

- List the active and past conditions you find, including undiagnosed symptoms, so nothing blindsides you later.

- Ask about a medical-record review — and when it happens. Some carriers will assess your pet's records and tell you what they'll treat as pre-existing. Timing varies: Embrace's free Medical History Review, for instance, is requested after you enroll, with a partial-refund cancellation window if the results surprise you. Ask each insurer whether it offers a review, when it happens, and whether the result is binding — and make sure a recent clean exam is on record (some insurers want a healthy exam within the past year).

- Compare quotes — and ask each carrier directly how it handles the claim-time records review and continuous coverage.

- Bind the new policy and get written confirmation of the effective date and the new waiting periods.

- Overlap the two policies. Keep the old one active while the new policy's waiting periods run, and submit any outstanding old-policy claims promptly — including a "straddling" claim for treatment dated while the old policy was still in force. Many insurers require claims within about 90 days of the invoice date, so don't let that window close.

- Cancel or downgrade the old policy only after you have written confirmation the new one is in force and past its waiting periods.

The document checklist (and what each proves)

Gather these before you file your first claim with the new insurer — each one closes a specific gap an adjuster might otherwise question:

| Document | What it proves |

|---|---|

| Prior policy / declarations page | You carried continuous coverage — and what it included |

| Cancellation confirmation | Exactly when the old policy ended (no coverage gap) |

| EOBs (explanations of benefits) | The old carrier actually paid on the specific condition |

| Itemized invoices | The date and nature of each treatment |

| Full medical records + SOAP notes | Symptoms, onset, and history — what the new insurer audits |

| Vet health summary | A concise, current list of your pet's conditions |

Two things to remember: the new insurer will request your pet's full vet-stamped history at the first claim — a health summary won't substitute for the actual notes — and many carriers require claims within about 90 days of the invoice date, so file promptly.

Overlap, two policies, and changing clinics

Briefly running two policies during a switch is legitimate — it's the safe play. Keep the old policy active until the new one is enrolled and past its waiting periods, and some insurers will even let you hold both at once, with one designated as primary. What you can't do is collect from both for the same expense or hide one policy from the other — claiming the same bill twice is double-dipping, and it can be treated as insurance fraud and denied. If you do run two policies, disclose both and follow each insurer's coordination-of-benefits rules.

Two related myths worth killing:

- Switching clinics doesn't hide history. Adjudication follows the condition, not the building — your pet's records travel, and a new vet's first visit only creates more notes the insurer can request.

- A second policy won't make an old condition "new." Any insurer reviewing the records sees the same timeline; a fresh contract can't reset what already happened.

One practical snag: some brands share an underwriter, so you can't hold both active at once (owners flag AKC and Pets Best). Check before you stack coverage.

When switching is safe vs dangerous (per-pet triage)

Whether switching is smart comes down to one pet's record, not a blanket rule. Run yours through this:

Usually safe to switch: a young pet with clean records — no recent symptoms, no chronic medications, no pending diagnostics or surgery, and no past claims tied to a condition likely to recur. With nothing for the new insurer to flag, you're mostly just resetting waiting periods.

Switch with caution — or stay put: any pet in active treatment (switching mid-treatment is the worst case — the stage of care itself reveals the timeline), or with a history of allergies, orthopedic injuries, GI, urinary, or kidney issues, a heart murmur, asthma, dental disease, cancer, or any chronic medication or pending procedure. These are exactly what gets reclassified as pre-existing at a new insurer.

Multi-pet household? Triage each pet on its own record — a clean young dog and a senior cat on daily meds are two entirely different decisions.

One honest caveat: switching horror stories dominate Reddit and Quora partly because burned owners are the ones who post. Plenty of people move a young, healthy pet to a better-value plan cleanly and never look back — if the records are clean, your odds are good.

Limited exceptions that can preserve coverage

A few narrow paths can carry coverage across a switch — but none is true "portability," and every one comes with conditions that change. Treat all of these as verify-in-writing before you rely on them:

- MetLife "No Loss, No Gain." When it's offered (often through an employer or association), MetLife can continue coverage for a pre-existing condition your prior insurer already covered — but only with continuous coverage and no gap, and you submit your policy declarations and EOBs with the first claim. It's typically arranged by phone.

- AKC's ~365-day path. Owners report that AKC can cover pre-existing conditions after 365 days of continuous coverage with the Hereditary+ add-on — subject to an age cap and a 180-day IVDD wait, and owners note AKC shares an underwriter with Pets Best (so you may not be able to hold both). Confirm the current terms and your state's availability with AKC directly.

- Curable-condition windows. Some insurers stop treating a fully resolved condition as pre-existing after a symptom- and treatment-free stretch — commonly anywhere from about 180 days to a full year, depending on carrier (PetPlace explains the curable-vs-chronic split). Document the vet-confirmed resolution date, since these usually require an appeal and a records review.

- Orthopedic-wait waivers. As noted earlier, some carriers will waive the long orthopedic waiting period if you submit a recent clean vet exam — worth asking about if hip or cruciate risk is your main worry.

The common thread: each exception is conditional, carrier-specific, and subject to change. Confirm the exact terms in writing for your pet and your state before you switch on the strength of any one of them.

If your insurer is non-renewing or changing your plan (involuntary switching)

Sometimes the switch isn't your choice. Pet policies are typically annual contracts, so at renewal — subject to your state's rate-approval and notice rules — an insurer may re-rate your premium, change terms, or decline to renew, and when an underwriter changes, owners report being non-renewed or dropped even after years of loyal coverage. It can feel like a punishment for insuring early and paying on time. That reaction is fair.

But an involuntary switch runs on the same mechanics as a voluntary one — a new insurer will still treat your pet's documented conditions as pre-existing — so your response is the same discipline, just on a tighter clock.

If you're pushed onto a replacement plan, ask the carrier one question in writing: is this a renewal of my existing coverage, or a brand-new application? A genuine continuation may keep your covered conditions intact; a new application resets everything. Get that answer before you accept, and line up your records exactly as you would for any switch.

Is switching actually worth it?

Run the honest math: weigh the premium you'd save against the coverage you'd forfeit — the conditions that turn pre-existing, the reset deductible and annual limit, and a premium re-rated at your pet's current age. For a young, healthy pet chasing a better-value plan, switching can genuinely pay off. For a pet with charted conditions, the savings are usually swamped by what you give up.

And if a switch would leave your pet effectively uninsurable, insurance isn't your only tool. A veterinary discount plan (such as Pet Assure) or a deliberate self-insurance fund — money set aside each month for vet bills — can soften costs without the pre-existing wall. Neither replaces comprehensive coverage, so weigh them honestly rather than as equivalents.

For the full cost-benefit breakdown, see our guide on whether switching pet insurance is worth it.

Frequently Asked Questions

Can I switch from one pet insurance company to another?

Yes — but you're not transferring a policy, you're canceling one and buying a new one. The new insurer underwrites your pet from scratch, so waiting periods restart and any condition already in your pet's records is typically treated as pre-existing. Switching is most painless for a young, healthy pet and riskiest for one with charted conditions.

Will pet insurance cover arthritis after I switch?

If your pet's arthritis was diagnosed or already showing signs under your old plan, a new insurer will almost always classify it as a pre-existing condition and exclude it. A new policy only covers conditions that first appear — and clear their waiting period — after it takes effect.

Is diabetes covered if I switch pet insurance?

Generally no, if the diabetes was already diagnosed or symptomatic before the new policy started — it's treated as pre-existing and excluded. As a chronic, lifelong condition, diabetes is one of the clearest cases where switching means losing coverage for it, which is why it pays to confirm what you'd forfeit before you move.

Will pet insurance pay for cataract surgery after switching?

Only if the cataracts (or related eye issues) first appear after your new policy is active and past its waiting period. If cataracts or their symptoms were already noted in your pet's records, the new insurer will treat them as pre-existing and decline the surgery.

What happens to a claim that's in progress when I switch?

Treatment dated while your old policy was still in force is the old insurer's responsibility — so file those in-flight or "straddling" claims with the old company before its post-cancellation submission window closes (often around 90 days). Don't assume the new insurer will pick up a condition that began before its coverage started.

Do I have to notify my old insurer before switching?

No — you don't need their permission. What matters is timing: keep the old policy active until the new one is in force and past its waiting periods, then cancel the old one in writing and confirm the effective end date. Canceling too early opens a coverage gap that can turn a fresh problem into a pre-existing condition.

Is there a best time or age to switch pet insurance?

The safest window is while your pet is young and healthy, with a clean recent vet exam and nothing newly charted. Every additional condition in the record narrows what a new carrier will cover — so the longer you wait, the more you typically stand to lose by switching.

What if my pet gets sick or hurt during the new policy's waiting period?

Anything that arises during a waiting period is generally excluded as pre-existing, even though you're paying premiums. Never ask your vet to backdate or alter records to get around it — that's insurance fraud, and an undisclosed condition can void the entire policy. The honest protection is to overlap policies, so the old one still covers you until the new waiting periods clear.

Sources

- Pet Insurance Model Act (Model #633) — NAIC

- Can I Switch Pet Insurance Providers if My Pet Has Pre-Existing Conditions? — PetPlace

- How do pet insurance companies determine pre-existing conditions? — Quora

- Pre-existing conditions & waiting periods for new insurance — Reddit — r/petinsurancereviews

- Changing insurance and evaluating pre-existing condition possibility — Reddit — r/petinsurancereviews

- Pet Insurance Waiting Periods, Explained — Lemonade

- Timeframe for pre-existing conditions? — Reddit — r/petinsurancereviews

- Pet Insurance Waiting Periods — Progressive

- Made a big insurance mistake as a new pet owner. Is there any way to increase coverage and get pre-existing conditions covered? — Reddit — r/petinsurancereviews

- How To File a Claim With MetLife Pet Insurance — MetLife Pet Insurance

- Can You Switch Pet Insurance Providers? — MetLife Pet Insurance

- Anyone switch pet insurance when premiums go through the roof? — Reddit — r/petinsurancereviews

- Pet Assure — Veterinary Discount Plan — Pet Assure

- RCW 48.205.050: Exclusions—Waiting periods—Requirements — Washington State Legislature

- Pet Insurance Medical History Review — Embrace Pet Insurance