Yes — pet insurance covers surgery, including emergency operations, cancer surgery, and the big orthopedic repairs like a torn cruciate ligament. But "covered" comes with four conditions, and one of them decides most cases: a policy won't pay for the surgery your pet already needs if a symptom is already in the medical record.

That gap — between "can I buy a policy?" (almost always yes) and "will this policy cover this surgery?" (often no) — is where most pet owners get caught, and where most articles on this topic stay vague. We're going to be specific instead.

If you're reading this with an estimate in your hand, start with the timing question just below — the honest answer is in the first sentence. If your pet was just diagnosed, the pre-existing and appeal sections are written for you. And if you have a healthy dog or cat and you're planning ahead, you're in the best spot there is: this is the moment coverage actually works the way it's sold.

Either way, here's what this guide does that the carrier pages won't. We'll show you what "covered" really means, walk a real surgery bill through an actual reimbursement calculation, and decode the fine print that quietly kills surgical claims — pre-existing "signs," the second-knee trap, waiting periods, and benefit caps. Then we'll cover the part almost nobody explains: how you pay the vet before the reimbursement ever arrives.

Table of Contents

- Yes, But "Covered" Has Four Conditions

- Is It Too Late to Insure a Surgery My Pet Already Needs?

- What a Real Surgery Claim Actually Pays: The Math

- Which Surgeries Are (and Aren't) Covered

- Pre-Existing Conditions and the "Signs Of" Trap

- The Second Knee: Bilateral Exclusions Explained

- Waiting Periods and the Timing Decision

- Cancer and Major Bills Across Renewals

- Does It Cover Emergency Surgery and Hospitalization?

- How You Actually Pay: Reimbursement Lag, Direct Pay & Financing

- When a Claim Is Denied: The Appeal Playbook

- Is Pet Insurance Worth It for Surgery?

- Check Your State: The Regulatory Floor

- Frequently Asked Questions

- Sources

Yes, But "Covered" Has Four Conditions

A surgical claim gets paid only when four things are true at once. Miss any one and the "yes" turns into a denial — or a much smaller check than you expected.

- The underlying problem is a covered accident or illness. A broken leg, a swallowed sock, a torn cruciate ligament, a tumor that grew after your policy started — all normally covered. Cosmetic and elective procedures, like a routine spay or an ear crop, are not.

- The first signs appeared after your coverage — and its waiting period — began. This is the condition that catches people. If the problem was already showing up in your pet's records, it's treated as pre-existing, no matter how clearly "medical" the surgery is.

- The specific line items are covered under your plan. The surgery, anesthesia, hospitalization, and follow-up care are standard; the exam fee that triggered the visit often isn't, depending on the carrier.

- You haven't used up your benefit. Most plans cap what they'll pay per policy year. A single big surgery — or a months-long cancer course — can reach that ceiling, and everything past it is on you until the year resets.

The plan type matters here, too. An accident-only policy covers surgery for injuries — the car, the fall, the swallowed object — but not for illness, which is where a lot of the priciest surgeries actually come from: cancer, chronic joint disease, organ problems. For surgical coverage that holds up across your pet's life, you almost always want an accident and illness plan.

Two things "covered" does not mean — and we'll come back to both. It does not mean the insurer pays your vet at checkout; with nearly every carrier you pay first and get reimbursed later. And it does not mean 100% of the bill; your reimbursement is a percentage of the eligible charges after your deductible. Those two facts are where the real number lives.

Is It Too Late to Insure a Surgery My Pet Already Needs?

For the surgery your pet needs right now, the honest answer is almost always no — a new policy won't cover it. You can still buy a policy today (that part is nearly always yes), but it won't pay for a condition your pet already has.

Here's why, and it's the single most important thing to understand about this whole topic. Insurers don't decide "pre-existing" by whether you already have a diagnosis. They decide it by whether a sign or symptom was already in your pet's record before the policy — and its waiting period — began. A limp your vet noted three months ago. A lump they told you to "keep an eye on." A single line that says "recheck." Any of those can make the related surgery pre-existing, even though no one has said the word "surgery" yet.

This is exactly where owners get caught. In pet-insurance forums the same scenario plays out constantly: the vet quotes a surgery for next week, a friend says "sign up for coverage now," the policy gets bought — and the claim comes back denied as pre-existing. Buying in a hurry doesn't beat the record. The record is what the insurer reads.

So if you're holding an estimate today, be clear-eyed: coverage almost certainly won't rescue this bill. For that, skip ahead to how you actually pay — direct-pay options and financing are the realistic levers now. But this is not a dead end. Insurance still protects the unrelated risks that haven't happened yet — a new illness next year, a future accident, and the healthy dog or cat at home who's still fully insurable. (The one thing it usually won't rescue is the matching side of the same problem: if one knee, hip, or eye already has a history, the other is often excluded too — more on that below.) The move is to cover the next risk, not to chase the one already in the chart. And whatever you decide, get the care your pet needs now and keep every record — waiting to see the vet never protects your coverage, it only delays treatment.

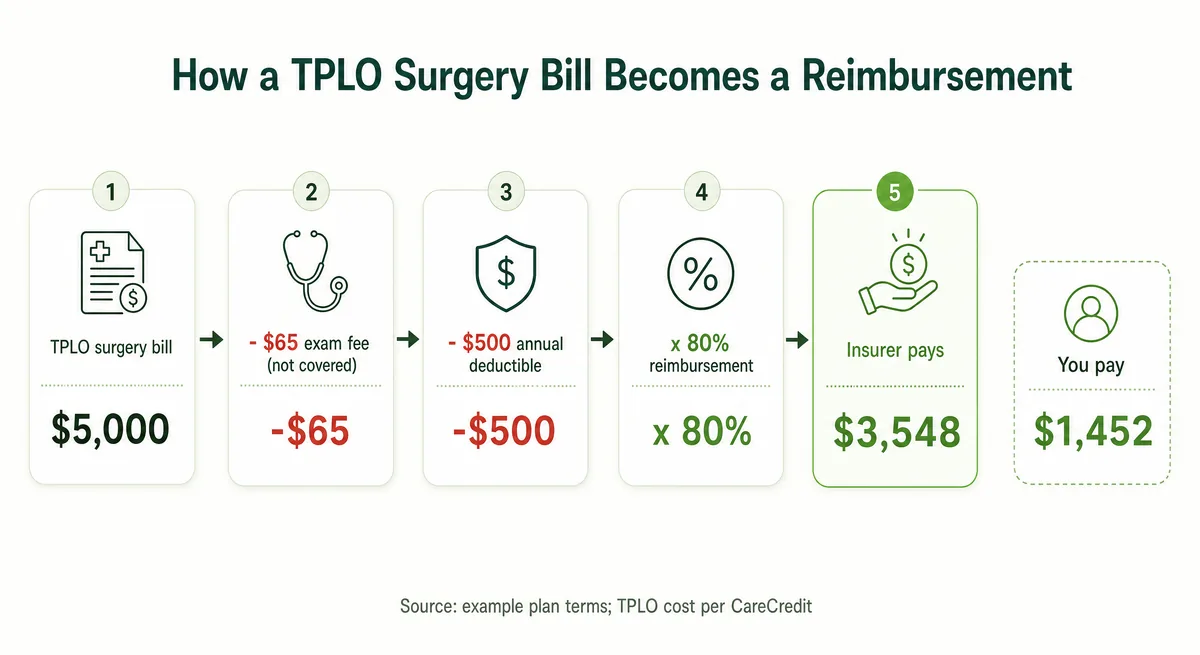

What a Real Surgery Claim Actually Pays: The Math

Here's the number nobody shows you. An "80% plan" does not pay 80% of your surgery estimate. It pays 80% of the eligible charges left after your deductible — and "eligible" quietly drops a line item or two along the way. On a real bill, the gap between what you expect back and what actually lands in your account is often four figures.

Nearly every carrier uses the same formula (the order can vary — more on that below):

(your bill − any line items your plan excludes − your remaining deductible) × your reimbursement percentage = your check — up to whatever is left of your annual limit.

Let's run a torn cruciate ligament, the most common major knee surgery in dogs and one of the priciest. A TPLO repair runs roughly $2,800 to $6,400, averaging about $3,525, according to CareCredit. Say your estimate lands at $5,000, on a common plan: 80% reimbursement, a $500 annual deductible you haven't touched yet, and a $5,000 annual limit.

- $5,000 — the estimate.

- − $65 exam fee. Some carriers don't cover the exam fee that triggered the visit. Eligible charges: $4,935.

- − $500 deductible, subtracted before anything is reimbursed. Now: $4,435.

- × 80% reimbursement — the insurer's share of what's left: $3,548.

You pay $1,452 of a $5,000 surgery, and the insurer sends $3,548 — comfortably under the $5,000 annual cap, so the whole eligible amount counts. Notice it's not 80% of $5,000 (which would be $4,000). It's $3,548, because the deductible and the exam fee came out first.

One detail worth confirming with your carrier: the order of that math. Most insurers subtract the deductible first and then apply the percentage — the calculation above. A few apply the percentage to the full eligible amount and then subtract the deductible, which can shift your check by a hundred dollars or more. Same policy on paper, different payout.

And that annual limit matters more than it looks here. A single $5,000 surgery fits under a $5,000 cap — but a cruciate repair followed by a complication, or a cancer course that runs for months, can blow through it, and everything past the cap is yours until the policy year resets.

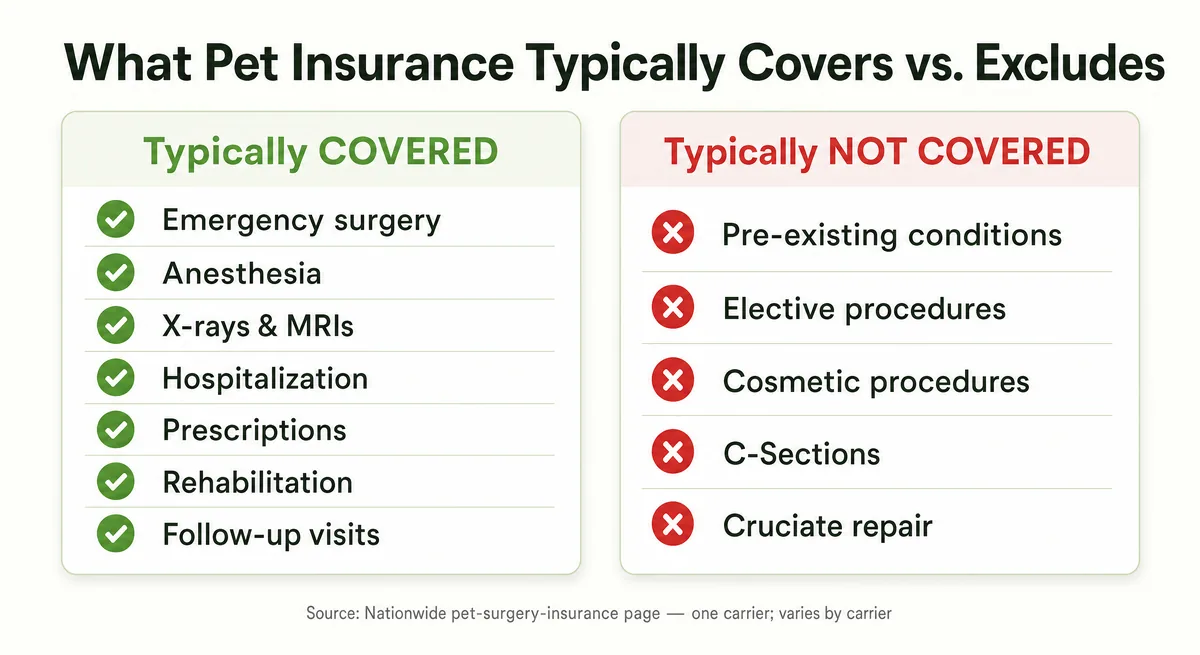

Which Surgeries Are (and Aren't) Covered

On a comprehensive accident and illness plan, most medically necessary surgery is covered — and, importantly, so is everything around it. When a surgical claim pays, it typically includes the operation plus the supporting line items:

- Emergency and trauma surgery — a hit-by-car repair, a swallowed-object removal

- Mass and tumor removal

- Dental surgery tied to a covered accident or illness — though dental coverage varies sharply by plan

- Orthopedic repairs — fractures, and many cruciate and hip procedures (see the catch below)

- Anesthesia, imaging, hospitalization, and follow-up care

What's reliably not covered is narrower but predictable: elective and cosmetic procedures — a routine spay or neuter, an ear crop, a dewclaw removal that isn't medically necessary — and anything tied to a pre-existing condition. Spaying and neutering can sometimes be reimbursed, but only through a separate wellness or routine-care add-on, never the core surgical coverage that pays for the emergencies.

Here's the trap, and it comes straight from a carrier's own page. Nationwide's pet surgery page — from one of the largest and oldest U.S. pet insurers — lists its exclusions plainly: pre-existing conditions, elective procedures, cosmetic procedures, C-sections, and "cruciate repair." Read that last one twice. A cruciate (CCL) repair is the single most common major orthopedic surgery in dogs, and on this particular product it's excluded outright — optional cruciate coverage can be added on some Nationwide plans.

The lesson isn't "avoid Nationwide" — every carrier's exclusion list is different, and other insurers cover cruciate repair as standard. The lesson is that "covers surgery" and "covers your surgery" are two different promises. Before you buy — and especially if your breed is prone to a particular procedure — read the actual exclusions list for the specific plan, not the marketing headline. The surgery your dog or cat is most likely to need someday is exactly the one worth checking for by name in the policy document.

Pre-Existing Conditions and the "Signs Of" Trap

The word that decides more surgical claims than any other is "pre-existing" — and most owners misread it. A pre-existing condition is not "something your vet diagnosed before you bought the policy." It's something that showed signs before your coverage began, diagnosis or not.

Read one carrier's own definition: a pre-existing condition is one that "first occurred or showed clinical signs or symptoms (there doesn't need to be a diagnosis)" before coverage started. That parenthetical is the whole trap. A limp, a lump your vet told you to keep an eye on, a "recheck in two weeks" note — each is a sign, and each can make the surgery that follows pre-existing, even though no one has named a condition yet.

When you file your first claim, the insurer pulls your pet's records — often going back a year or more — and reads them for exactly these signals. That's why the record, not your intent or your memory, is what decides the claim.

There is a narrow exit for some problems. Many carriers treat a curable condition as no longer pre-existing once it stays symptom- and treatment-free for a set stretch — but the stretch varies: about 180 days at some carriers, a full 12 months at others. Chronic and orthopedic conditions — cruciate injuries included — usually don't qualify for that reset at all.

One myth worth correcting: you've probably read that you have to prove a condition wasn't pre-existing. In a growing number of states, that's backwards. Under the NAIC Pet Insurance Model Act, which about fifteen states have adopted, the insurer carries the burden of proving the exclusion applies. Whether that protection covers you depends on your state — more on that below.

The Second Knee: Bilateral Exclusions Explained

This is the exclusion that hands owners their biggest surprise bill, and it has a name: bilateral. For conditions that can strike both sides of the body — cruciate ligaments, hips, cataracts, luxating patellas — if one side showed signs before your coverage began, the other side is usually excluded too, even though it hasn't happened yet.

Cruciate tears are the textbook case. Read Healthy Paws' clause word for word: "If the cruciate ligament on one leg is injured prior to enrollment or during the 15-day waiting period, then the cruciate ligament on the other leg is excluded from coverage." One torn knee on the record, and the second one — the leg most likely to go next — is off the table.

Here's why that stings. A dog that tears one cruciate is, in many vets' experience, likely to tear the other, and a single TPLO repair runs into the thousands. Owners in dog forums describe exactly this trap: a first surgery paid out of pocket, then a denial on the second knee, then an impossible choice between another few thousand dollars and their dog's mobility. It sits behind some of the hardest financial decisions owners ever face.

The wording varies by carrier, which is exactly why it pays to read it before you buy. Some, like MetLife, publish the full list of conditions they treat as bilateral — hip and elbow dysplasia, cruciate injuries, cataracts, luxating patella, glaucoma. Others exclude the second side "regardless of cause," meaning it doesn't matter how the second injury actually happened. And a few fold bilateral logic into their general pre-existing definition instead of spelling it out. The practical takeaway is the same across all of them: if your dog already has any history with one knee, hip, or eye, assume the matching side may not be covered — and confirm it in the policy document, not the brochure.

Waiting Periods and the Timing Decision

A waiting period is the gap between the day your policy starts and the day it will actually pay for a given problem. For surgery, the orthopedic waiting period is the one that matters most — and it varies more than almost any other term in the policy. There is no single answer: across carriers the orthopedic wait runs from nothing at all to six months — and as long as a year for specific conditions like hip dysplasia.

Accident coverage usually starts soonest and illness coverage a little later, but orthopedic conditions like cruciate tears sit in their own, much longer bucket. MetLife applies no separate orthopedic waiting period at all. Figo holds orthopedic conditions for 30 days. And both Pets Best and Embrace make you wait roughly six months — Embrace's is a 180-day wait on cruciate, IVDD, patellar luxation, and hip dysplasia. Same surgery, wildly different clock: a TPLO that clears only a two-week illness wait at one carrier stays excluded for half a year at another.

Several of those carriers let a vet exam shorten the orthopedic wait — but read the trade carefully. In Embrace's own words, an orthopedic exam can drop the wait to 14 days — yet anything the vet flags on that exam becomes pre-existing and is excluded from then on. The waiver isn't free; you're trading waiting-period time for pre-existing exposure. If your pet's joints are sound today, it can be worth doing. If there's any history there, the exam can surface exactly the problem you were hoping to insure.

Cancer and Major Bills Across Renewals

Yes — chemotherapy, radiation, and oncology medications are covered under a standard accident-and-illness policy at most carriers, as long as the cancer isn't pre-existing and the waiting period has passed. The hard part isn't whether cancer is covered; it's that treatment runs for months and collides with your policy's annual boundaries. A course of radiation runs roughly $2,500 to $7,000 at Cornell's teaching hospital, and chemotherapy protocols commonly span three to six months — long enough to straddle a renewal.

Two things reset when your policy year does. First, the payout cap: most plans limit what they pay per year, and unused room doesn't roll over. Hit a $5,000 annual limit mid-treatment and, as MetLife spells out, new expenses are excluded until the policy renews. Second, the deductible: Figo requires a fresh annual deductible for each policy period a treatment spans. The exception on both counts is Trupanion, whose filed policy sets no payout cap and charges its deductible once per condition for the life of your pet rather than every year.

The reassuring part: a cancer diagnosed while your pet is insured stays covered when you renew — Embrace, for one, continues coverage at renewal and won't reclassify an ongoing condition as newly pre-existing. In the states that have adopted the NAIC model act, that renewal protection is written into law (more on that below).

But there's a trap worth knowing before you touch your policy mid-treatment. If you discover your annual cap is too small, raising it is not a simple upgrade. Under Pets Best's policy, increasing your annual limit requires canceling your current policy and issuing a new one with new waiting periods — so a condition already showing signs, like a cancer under treatment, would be treated as pre-existing on the new policy. You cannot simply buy more headroom in the middle of chemo.

None of this is a reason to hesitate on care. What decides coverage is what's already in your pet's records, not the calendar — so never delay the workup to protect a policy. Get the diagnosis and the treatment your vet recommends, then work the coverage around it.

Does It Cover Emergency Surgery and Hospitalization?

Yes. An accident-and-illness policy covers emergency surgery and the hospital stay around it — diagnostics, anesthesia, the procedure itself, and overnight care — as long as the underlying problem isn't pre-existing and your waiting period has already passed. (The ER exam or consultation fee is the common exception — many base plans don't cover it without an add-on.) A dog that swallows a sock on a Tuesday is exactly what this coverage is for.

The catch is that "emergency" doesn't suspend the usual rules. The same pre-existing and waiting-period tests apply to a 2 a.m. crisis as to a scheduled procedure, so a condition your pet was already showing signs of before enrollment can still be denied — even in the ER.

When it is covered, the bills are real. Removing a swallowed foreign object runs anywhere from $1,600 to over $12,000 in Embrace's own claims data, and emergency bloat (GDV) surgery typically runs $3,000 to $6,000.

Here's the part that catches owners off guard: most ER hospitals demand a large deposit at admission — before your insurer pays a cent. With a reimbursement policy, you front that money and wait. That cash-flow gap bites hardest in an emergency, which is why it's worth understanding how you'll actually pay the bill before you're standing at the counter.

How You Actually Pay: Reimbursement Lag, Direct Pay & Financing

Here's the reality no quote page mentions: with almost every carrier, you pay the vet in full first and get reimbursed days to weeks later. On a $5,000 surgery, that means finding $5,000 today and waiting for the check — a wait owners routinely describe as the most stressful part of a claim. Only a handful of carriers change that, and "direct pay" means very different things depending on who's offering it.

| How it works | Carrier | What it means at checkout |

|---|---|---|

| True point-of-sale direct pay | Trupanion (VetDirect Pay) | Pays the hospital in real time at checkout — but only at clinics running its software (about a third of U.S. hospitals). You pay just your share. |

| Fast pay-to-owner | Pumpkin (PumpkinNow) | Pays you in as little as 15 minutes for eligible care over $500, if your bank supports instant payments. |

| Pre-arranged, case by case | Healthy Paws | Can pay the vet directly, but only if it's arranged by phone before treatment and the vet agrees. |

| Post-adjudication routing | Pets Best (Vet Direct Pay) | Sends money to the vet only after the claim is processed — so it won't bridge checkout unless the vet defers billing. |

| Reimbursement (the default) | Most carriers | You pay in full, file a claim, and wait days to weeks for the money. |

The one model that truly removes the gap is point-of-sale direct pay, because it shifts the cash-flow risk from you to the vet — which is precisely why it's still rare.

When you do need to bridge the gap, two financing rails dominate vet counters. CareCredit offers promotional periods with no interest if you clear the full balance in time — but miss the deadline and interest (around 33% APR) is charged retroactively to the original purchase date, which is how a manageable plan quietly becomes an expensive one. Scratchpay works differently: checking your rate is only a soft credit pull, terms run from 0% to 36% APR, and it pays the clinic directly.

The practical takeaway: before you ever need it, find out which system your carrier uses and whether your regular clinic accepts it. In a real emergency, "covered" and "paid at the counter" are two very different promises — and the gap between them is measured in the thousands of dollars you may have to front yourself.

When a Claim Is Denied: The Appeal Playbook

A denial isn't always the end of the road. Many surgical claims are refused for reasons you can challenge — and your insurer is obligated to tell you exactly which policy provision it relied on, in writing. That written reason is the starting point for every appeal.

Most surgery denials trace to one of five causes: the claim was classified as an illness when the owner believes it was an accident (or the reverse); the underlying condition was ruled pre-existing under "signs of" language; a bilateral exclusion applied to a second knee, hip, or eye; the waiting period hadn't fully passed; or the annual benefit cap was already exhausted. The through-line: it's the medical record, not your intent, that decides the claim.

That's exactly what makes the appeal winnable. The playbook that works runs in three steps:

- Get a letter from your vet. A dated note documenting the onset — or, for an accident reclassification, a witnessed trauma event — is the single strongest piece of evidence, because it speaks to the record the adjuster is reading.

- File a formal written appeal before the deadline. Carriers set a window; Pets Best's policy, for instance, lays out a three-level path — an internal appeal within 60 days, then external review by an independent veterinarian, then arbitration.

- Escalate to your state Department of Insurance. If the carrier won't budge, every state's insurance regulator accepts pet-insurance complaints and will ask the insurer to justify its decision.

One reason to read renewal terms before you commit: the coverage you hold today isn't guaranteed forever. In June 2024, Nationwide non-renewed roughly 100,000 pet policies, citing veterinary-cost inflation, and a 2025 federal class action alleges it sold "lifetime" coverage it then dropped. The takeaway isn't to avoid a single carrier — it's to read the renewal and cancellation terms as closely as the coverage ones.

Is Pet Insurance Worth It for Surgery?

Here's the straight answer: for the average pet in the average year, you'll likely pay more in premiums than you get back. That isn't a scam — it's how catastrophe insurance works. You're not buying a rebate; you're buying protection against the surgery you can't predict and can't easily absorb.

Run the math both ways. An accident-and-illness policy for a dog averages about $62 a month — roughly $745 a year. Pay that for three years and a single $4,500 knee repair, reimbursed at 80–90% after your deductible, more than covers every premium you've paid. Go those same three years with only routine care, and you're out of pocket ahead. In a Consumer Reports member survey, only about a third said they'd come out ahead — the honest base rate for a product you hope never to use.

And the premium isn't fixed. It climbs as your pet ages, and entire books get re-rated: California regulators approved an average 33% Trupanion increase in 2025, and thousands of Florida owners saw double-digit hikes. Budget for a cost that grows.

So it comes down to your situation. Insuring a young, healthy pet before any signs appear is where coverage works best — premiums are lowest and nothing's excluded yet. If you're disciplined enough to bank $60–$100 a month untouched and could write a five-figure check tomorrow, self-insuring can win. But for most owners who couldn't absorb a $6,000 bill on short notice, coverage — or at least a financing backstop — is the safer bet. The worst place to be is both uninsured and unfunded.

Check Your State: The Regulatory Floor

Where you live can decide whether a surgical claim is handled fairly, because the protections vary widely by state. The NAIC Pet Insurance Model Act sets a floor that a growing number of states have written into law — and its provisions land squarely on surgery.

In a state that has adopted it, the model act caps illness and orthopedic waiting periods at 30 days — and "orthopedic" is defined to include cruciate ligament rupture, IVDD, and hip, elbow, and patellar conditions, the exact surgeries covered above. It bans waiting periods for accidents, requires that any waiting period be waivable by a vet exam, and — most importantly — puts the burden on the insurer to prove a condition was pre-existing, reversing the usual default. It also locks in renewals: a condition covered one year can't be reclassified as pre-existing the next.

One caveat: this is a procedural floor, not a coverage mandate. Insurers can still exclude hereditary or congenital conditions — they just have to disclose it and prove it. And adoption is uneven. Roughly 15 states have enacted it (Washington, Florida, and Ohio among them); California has only an older, weaker disclosure law with none of those protections; and many large states haven't adopted the model act, so the protections above may not apply where you live. That's why "check your state" isn't filler — confirm what your own state's law provides, or ask your state insurance department, before you assume a protection is there.

Frequently Asked Questions

What happens if your pet needs surgery and you can't afford it?

You have more options than a lump sum out of pocket. Ask the clinic about payment plans or in-house financing first; then look at medical-credit lines like CareCredit or Scratchpay that many vets accept, nonprofit treatment grants, and university veterinary teaching hospitals, which often price major surgery below private specialty clinics. If the condition is already in your pet's records, insurance won't rescue this particular bill — but these bridges can keep care within reach.

What does pet insurance not pay for?

The big exclusions are pre-existing conditions (anything that showed signs before your coverage began or during its waiting period), the matching side of a bilateral condition when the first side was pre-existing, and elective or cosmetic procedures. Exam fees and any costs above your annual cap fall to you as well. Some carriers go further on specific surgeries — Nationwide's own surgery page lists cruciate repair and C-sections as exclusions — which is why reading your policy's exclusions matters more than the marketing.

Does pet insurance cover pancreatitis?

Yes — pancreatitis is treated as an illness and is covered by accident-and-illness plans, as long as it isn't pre-existing and your waiting period has passed. The catch is that pancreatitis tends to recur: if your pet had an earlier episode, or symptoms like vomiting were noted in the record before coverage began, later flare-ups are usually excluded as pre-existing. As with every condition, when the first signs appeared decides more than the diagnosis label.

Which pet insurance covers hip dysplasia?

Most accident-and-illness plans cover hip dysplasia, but it's one of the most restricted conditions. It often carries a longer orthopedic waiting period, and terms vary sharply: Healthy Paws, for example, applies a 12-month wait for hip dysplasia and excludes it entirely for pets enrolled at age 6 or older. If signs appeared before coverage, it's pre-existing anywhere. So how long you've held the policy — and what the record shows — matters more than which carrier's logo is on it.

If I buy a policy today, will this week's surgery be covered?

Almost certainly not. Every policy has a waiting period before benefits start — commonly 14 days for illness and often much longer for orthopedic surgery — and any condition your vet has already diagnosed or noted becomes pre-existing. A surgery already on the schedule is both inside the waiting period and documented in the record, so it won't be covered. Buying now protects your pet against future, unrelated problems — not the one you're already facing.

Do I have to pay the vet upfront?

Usually, yes. With almost every insurer you pay the full bill at checkout and file for reimbursement afterward, which lands in days to weeks. The main exception is Trupanion's VetDirect Pay, which can pay the hospital directly at checkout — but only at clinics running its software. A few others (Pumpkin, Healthy Paws, Pets Best) offer faster or case-by-case versions, so confirm what your carrier and clinic support before an emergency.

Is a pre-approved estimate a guarantee the claim will be paid?

No. A pre-authorization or pre-approved estimate is an indication, not a binding coverage decision — carriers make the final call when you file the claim and see the full records. Healthy Paws, for instance, notes that prior approval "is not a coverage determination." Get any pre-approval in writing, but treat it as a strong signal rather than a promise, and keep your documentation in case you need to appeal.

Does pet insurance cover cancer treatment like chemo and radiation?

Yes. Chemotherapy, radiation, and oncology medications are covered under standard accident-and-illness plans at most carriers, provided the cancer wasn't pre-existing and the waiting period has passed. The harder problem is money over time: because treatment often runs three to six months, it can straddle a policy renewal, resetting your deductible and testing your annual cap. Some carriers confirm coverage continues at renewal, so a cancer diagnosed while insured stays covered.

Sources

- How Much Does Dog ACL/Cruciate (TPLO) Surgery Cost? — CareCredit

- Pet Insurance Coverage and Exclusions — Healthy Paws

- Does Pet Insurance Cover Surgery? — NerdWallet

- Pet Surgery Insurance — Nationwide

- Pet Insurance and Pre-Existing Conditions — ASPCA Pet Health Insurance

- Pre-Existing Conditions — Embrace

- Pet Insurance Model Act (MDL-633) — NAIC

- Bilateral Conditions and Pet Insurance — MetLife Pet Insurance

- Does Pet Insurance Have a Waiting Period? — MetLife Pet Insurance

- Pet Insurance Coverage — Figo Pet Insurance

- Surgery Coverage — Pets Best

- What Is the Waiting Period for Orthopedic Conditions? — Embrace Pet Insurance

- Cancer Management: Frequently Asked Questions — Cornell University College of Veterinary Medicine

- Does Pet Insurance Cover Cancer Treatment? — MetLife Pet Insurance

- Cancer Coverage for Pets — Embrace Pet Insurance

- Trupanion Policy (Maine filed form, Exhibit A-1) — Maine Bureau of Insurance

- Pets Best Policy Booklet (Annual Illness, sample) — Pets Best

- Cost of Surgery to Remove a Swallowed Foreign Object — Embrace Pet Insurance

- Dog Bloat Surgery: Cost and What to Expect — Great Pet Care

- Trupanion Form 10-K (FY2025) — VetDirect Pay — U.S. Securities and Exchange Commission

- PumpkinNow Urgent Pay — Pumpkin Pet Insurance

- Pet Insurance Claims — Healthy Paws Pet Insurance

- Vet Direct Pay — Pets Best

- Deferred Interest vs. APR — CareCredit

- How It Works — Scratchpay

- Nationwide to Drop About 100,000 Pet Insurance Policies — CBS News

- Silberman et al. v. Nationwide Mutual Insurance Company — Class Action Complaint — U.S. District Court (D. Mass.), via ClassAction.org

- State of the Industry 2025 Report Highlights — NAPHIA

- Is Pet Insurance Worth It? — Consumer Reports

- Trupanion California Rate Hike Approved — Insurify

- Nearly 50K Florida Pet Parents Face Double-Digit Premium Hikes — InsuranceNewsNet

- AB 2056 — Pet Insurance — California Legislature

- Pet Insurance Model Act (#633) — State Adoption Page — National Association of Insurance Commissioners (NAIC)

You may be interested...

More published guides that build on this topic.

Conditions

Conditions

Dog ACL Surgery: Costs, Recovery & Whether Insurance Will Pay

What dog ACL/TPLO surgery really costs in 2026, how recovery works, and when pet insurance does (and doesn't) pay — including the second-knee trap.

Conditions

Conditions

My Dog Ate Chocolate: Symptoms, Vet Costs, and What to Do Next (2026)

Plain-English triage if your dog ate chocolate: symptoms by hour, dose by weight and product, real 2026 ER costs, and what pet insurance covers (and doesn't).

Conditions

Conditions

Cat Kidney Failure: Symptoms, Stages, and Real Vet Costs (2026 Guide)

Plain-English guide to cat kidney failure: IRIS stages, real US vet costs, what treatment looks like at home, and what insurance does (and doesn't) cover.