Here's how pet insurance works, start to finish: you pay your vet the full bill, file a claim, and your insurer reimburses a share of the covered cost — after you meet your deductible, at your reimbursement percentage (often 70%, 80%, or 90%), up to your annual limit.

The part that trips up almost every first-timer is this: it's reimbursement, not a copay at the register. Unlike the human health insurance you're probably picturing, you front the whole bill yourself and get money back afterward — most U.S. policies pay on a reimbursement basis rather than paying the clinic directly.

If you've never bought a policy, that's actually the reassuring part: once you see how the handful of pieces fit together, the rest is mostly arithmetic. We'll define every term the first time it appears, so no insurance jargon is left sitting there cold.

This guide walks the whole machine in plain English: what you pay each month, why coverage doesn't start on day one, what actually happens when you're standing at the vet counter, how your deductible, percentage, and limit stack up on a real bill, and what really lands back in your account.

Table of Contents

- How pet insurance works, start to finish

- You pay the vet first - the part that surprises everyone

- The three numbers that decide your payout

- A real claim, worked out

- How it works at the vet + the claim timeline

- When coverage starts: waiting periods & pre-existing

- What's covered vs not: accident-only, accident-and-illness, wellness

- What it costs - and does it work differently for dogs vs cats?

- So, is it worth it?

- Frequently Asked Questions

- Sources

How pet insurance works, start to finish

Every pet insurance policy runs the same basic sequence. Learn this one chain of events and the rest of this guide is just filling in the details:

- You enroll and pick your terms. You choose a plan and set three dials — your deductible, your reimbursement percentage, and your annual limit — and together they decide both your monthly premium and, later, how much you get back.

- You pay a monthly premium. This keeps the policy active whether or not you ever file a claim, the same way your car or home insurance does.

- You wait out the waiting period. Coverage doesn't switch on the moment you sign up. There's a short gap — commonly a few days for accidents and about two weeks for illnesses, longer for some orthopedic conditions — before you can claim.

- Your pet gets sick or hurt. Something happens that isn't a pre-existing condition and isn't excluded by your plan.

- You pay the vet in full at the counter. This is the step that surprises almost everyone: you settle the whole bill yourself first, then get paid back later.

- You file a claim. You send your insurer the itemized invoice and, usually, your pet's recent medical records — with most carriers you can do it from a phone app.

- The insurer does the math. They subtract any deductible you haven't met yet, pay their reimbursement percentage of what's left, and check the result against your remaining annual limit.

- You get reimbursed. The money comes back to you by direct deposit or check, usually within a few days to a few weeks.

The thing to hold onto is that this is reimbursement insurance, not the network model you know from human health plans. There's no card to swipe at the front desk and no small copay at check-in — most U.S. policies pay you back after the fact. Each section below zooms in on one link in this chain: why you pay first, what those three dials actually do, how the math lands on a real bill, and what the whole thing looks like at the vet.

You pay the vet first — the part that surprises everyone

Here's the reality almost no first-timer expects: with nearly every U.S. policy, you pay the vet the full bill yourself, then get reimbursed afterward. It works nothing like the human health insurance you're picturing — there's no card to hand the front desk and no small copay at check-in. The money leaves your account first and comes back to you days to weeks later.

That timing gap is the real thing to plan for. If your dog needs $4,000 of emergency surgery on a Tuesday, you owe the clinic $4,000 that Tuesday, even on an 80% plan — your roughly $3,000 reimbursement only arrives after you file the claim and the insurer processes it. The confusion owners describe is fair: as one put it, "if I had the money to pay for it upfront, I wouldn't need insurance in the first place."

The common workaround is a bridge, not a financing plan: many owners put the bill on a credit card — or a veterinary card like CareCredit with an interest-free promotional window — and pay it off the moment the reimbursement lands. That works, but only if you clear the balance before any deferred interest kicks in. Leaning on it as long-term debt is how a manageable bill turns expensive.

A minority of carriers can skip the wait and pay your vet directly. Trupanion's VetDirect Pay is the leader, settling with participating hospitals right at checkout; it reports most portal claims paid within minutes across roughly 11,500 enabled clinics. A few others — including Pets Best, Healthy Paws, and ASPCA — offer partial or by-arrangement direct pay if you set it up with the clinic ahead of time. But treat direct pay as the exception: unless you've specifically confirmed it, plan on fronting the bill. Knowing that in advance is half the battle — it's the difference between a nasty surprise at the counter and a plan you've already thought through.

The three numbers that decide your payout

When you buy a policy you set three numbers, and together they decide every reimbursement you'll ever get. They're the part beginners most often blur into one vague "how much do they cover" — so here's what each one actually does, and which way it pushes your premium.

1. Your deductible — the part you pay first

The deductible is the amount you cover out of pocket before the insurer pays anything. Most U.S. carriers use an annual deductible: you meet it once per policy year, then it's done no matter how many claims you file. Some use a per-condition deductible instead, which you re-meet for each new problem — Progressive lays out the difference, and Trupanion is the notable outlier, charging its deductible once per condition for the life of the pet. A higher deductible lowers your monthly premium, because you're absorbing more before coverage kicks in.

2. Your reimbursement percentage — your share after that

Once the deductible is met, the insurer pays a set percentage of the remaining covered cost — commonly 70%, 80%, or 90%. The rest is your coinsurance, the slice you keep paying. As ASPCA puts it, "if you select 90%, you'll be responsible for paying 10% of covered expenses." For example, on $1,000 of covered costs after your deductible, a 90% plan returns $900 while an 80% plan returns $800 — the same bill, a $100 difference from the tier alone. A higher percentage means a bigger check but a higher premium.

3. Your annual limit — the ceiling

The annual limit is the most the insurer will reimburse in a single policy year. Only the dollars they actually pay you count against it — not the full bill — and once you hit it, you pay 100% of everything else until the policy renews, when the limit resets. Limits range from a few thousand dollars up to unlimited; a lower cap trims your premium but leaves less protection in a truly catastrophic year.

Here's the point that trips people up: even a "90% plan" almost never pays back 90% of your actual bill. Your deductible comes out first, you still owe your coinsurance share, and some line items (like the exam fee) may not count as "covered" at all — so the real share you get back lands lower. The next section runs a real bill through all three numbers so you can see exactly where the money goes.

A real claim, worked out

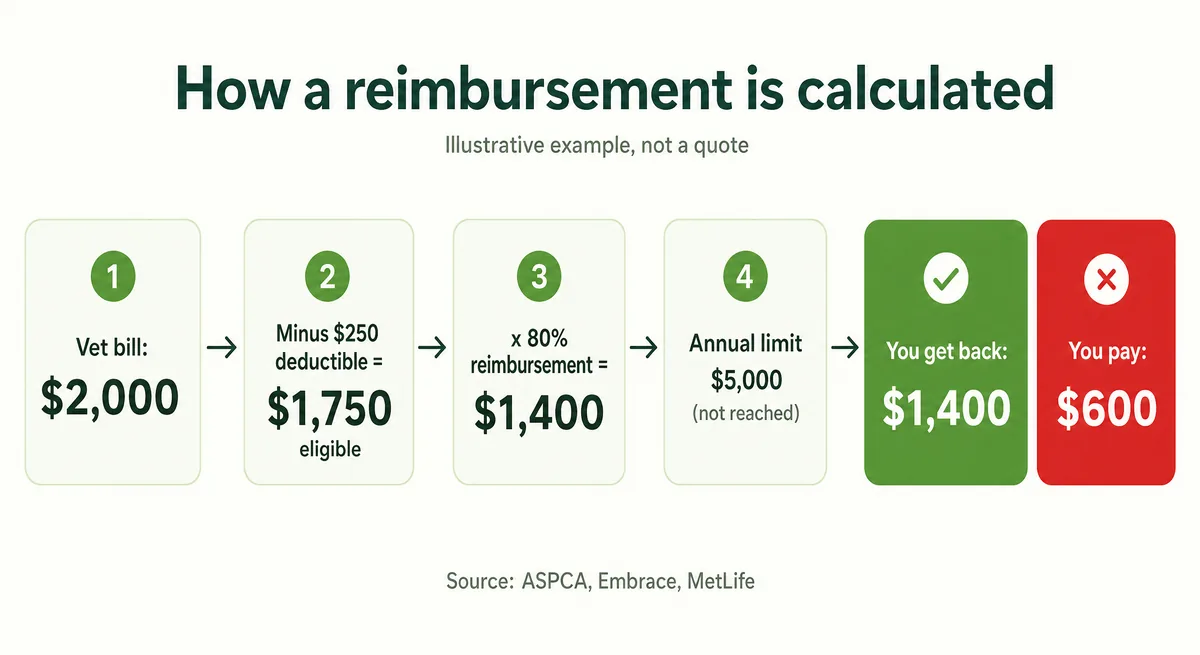

Definitions only get you so far — the real "aha" comes from running an actual bill through all three numbers. Say your dog needs treatment that totals a $2,000 vet bill, and your plan has a $250 annual deductible, 80% reimbursement, and a $5,000 annual limit. (Illustrative figures, not a quote.) Here's how most carriers calculate your check, step by step:

- Start with the covered bill: $2,000.

- Subtract your remaining deductible: $2,000 − $250 = $1,750 in eligible costs.

- Apply your reimbursement percentage: $1,750 × 80% = $1,400.

- Check it against your annual limit: $1,400 is well under $5,000, so it's paid in full — and your remaining limit drops to $3,600 for the rest of the policy year.

You get $1,400 back and pay $600 out of pocket — not the $400 (20% of $2,000) a first-timer might expect, because the deductible comes out before the percentage is applied. That's exactly why the "why didn't I get 80% of my bill?" surprise is so common: here, your effective reimbursement is really 70% of the total ($1,400 of $2,000), and the deductible is the reason the headline percentage and the real one never quite match.

One wrinkle changes the answer: carriers don't all run the steps in the same order. The method above is deductible-first — MetLife, for example, "subtracts your deductible first, and then applies your reimbursement rate," as do ASPCA and Embrace. Others use percentage-first: they multiply by your percentage, then subtract the full deductible — $2,000 × 80% = $1,600, − $250 = $1,350. Same inputs, $50 less, because you absorb the whole deductible yourself. Embrace shows the same split on a $1,200 bill: $800 the deductible-first way versus $760 the percentage-first way. Healthy Paws, Lemonade, and Pets Best are commonly percentage-first, though the exact order can vary by policy form and state.

Two smaller things also trim the check: your covered bill may leave out line items like the exam fee or sales tax, so the number your percentage applies to can be lower than the total you actually paid. None of this is meant to discourage you — it's just the arithmetic, and once you've seen it run once it's easy to do on any quote. Before you enroll, read the actual policy documents — the sample policy, benefit schedule, and exclusions, not just the quote — for two things that shape your payout: which order the carrier uses, and whether exam fees count as covered. Carriers spell out how they calculate reimbursement, so confirm yours before you need it.

How it works at the vet + the claim timeline

At the vet, you're just a regular paying customer — the insurance part happens later, at home. You check in, your pet is treated, and at the counter you hand over your own card and pay the bill in full. Ask for an itemized invoice (the kind that lists each treatment and its individual cost); that's the document you'll file, not the summary receipt.

Filing is usually quick. With most carriers you snap a photo of that itemized invoice in the app and submit it, often along with your pet's recent medical records — MetLife, for one, asks for the last 12 months of records on a first claim. The insurer checks the visit against your policy, applies your deductible, percentage, and limit, and pays you back by direct deposit or check. You also usually have months to file, not days: Healthy Paws gives you 90 days and ASPCA up to 270, so there's no need to panic if you file a few days late.

How long until the money comes back? It depends on the carrier and the claim, so treat any single promise with a little skepticism. Simple claims can move fast — Healthy Paws advertises around two days, and Lemonade settles some straightforward claims almost instantly in its app. But contracts commonly allow up to 30 days, and plenty of owners report the real-world wait lands closer to two to three weeks, especially on a first claim while the insurer pulls and reviews the records. A standard claim still comes down to the same three beats: pay the vet, file, get reimbursed.

Two things speed it up: send a complete itemized invoice plus records the first time — the most common delay is having to go back for missing paperwork — and expect your first claim to be the slowest, because it triggers that one-time records review. After that, reimbursements usually land faster.

When coverage starts: waiting periods & pre-existing

Two rules decide what a brand-new policy will and won't pay for, and both catch first-timers off guard: coverage doesn't begin the day you sign up, and it generally won't cover a condition your pet already has.

Waiting periods: the gap before coverage kicks in

A waiting period is the stretch between when you start paying and when you can actually file a claim — it exists to stop people from buying a policy only after their pet is already sick. The windows vary by carrier and by problem, so don't assume one number covers everything. Typical shapes are a few days for accidents, around two weeks for illnesses, and a much longer wait — often six to twelve months — for orthopedic issues like cruciate ligaments and hip dysplasia. Healthy Paws, for instance, applies a 12-month hip-dysplasia wait for pets enrolled young. Read your own policy's waiting periods before you assume you're covered.

Pre-existing conditions: what "already has" really means

A pre-existing condition is anything your pet showed signs of before coverage started (or during a waiting period) — and here's the part beginners miss: under the NAIC's model definition, a formal diagnosis isn't required. Signs or symptoms your vet noted — a limp, an itch, a stomach upset — can be enough, and the insurer decides at claim time by reviewing your pet's records. A few carriers are more forgiving: some will cover a curable pre-existing condition again after a symptom-free stretch (ASPCA, for example, uses 180 days), though chronic conditions are almost always excluded for good. And in states that have adopted the NAIC model, the insurer — not you — carries the burden of proving a condition was pre-existing; not every state has, so check your own state's rules.

This is exactly why some owners on Reddit swear you should "never tell the vet anything." Please don't. Skipping or hiding care to protect a future claim can hurt your pet and can void a claim outright. The honest approach — and the one that actually holds up — is to get your pet the care it needs, keep good records, and enroll while your pet is young and healthy, before there's anything to exclude. The finer print on exclusions is a bigger subject than this overview; here, the mechanic is the point.

What's covered vs not: accident-only, accident-and-illness, wellness

Before you pick a plan, you pick a tier — and the tier decides what's covered. The industry sorts policies into three, which NAPHIA tracks as accident-only, accident-and-illness, and accident-and-illness with a wellness add-on.

| Tier | What it covers | What it doesn't |

|---|---|---|

| Accident-only | Injuries: swallowed objects, broken bones, bite wounds, cuts | Any illness — infections, cancer, chronic disease |

| Accident & illness (most common) | Everything above plus illnesses: infections, cancer, allergies, diabetes, and other chronic conditions | Routine/preventive care; pre-existing conditions |

| + Wellness add-on | Adds routine care: exams, vaccines, flea/tick, dental cleanings | Still excludes pre-existing conditions |

Most people who say "pet insurance" mean the middle tier, accident and illness — it's the one that catches the big, unpredictable bills. That matters because the conditions pets actually rack up — skin allergies, ear infections, upset stomachs, cancer — are illnesses, not accidents. Accident-only costs less, but it won't touch any of them.

The surprise that trips up nearly every first-timer: routine care isn't included by default. Checkups, vaccines, and dental cleanings are covered only if you add a wellness rider — and even then, that add-on mainly spreads predictable costs across the year rather than protecting you from a big surprise. No tier, meanwhile, covers a pre-existing condition. Every plan also carries its own exclusions and fine print; the full in-and-out list is a subject of its own, but the tier you choose is the first and biggest fork in the road.

What it costs — and does it work differently for dogs vs cats?

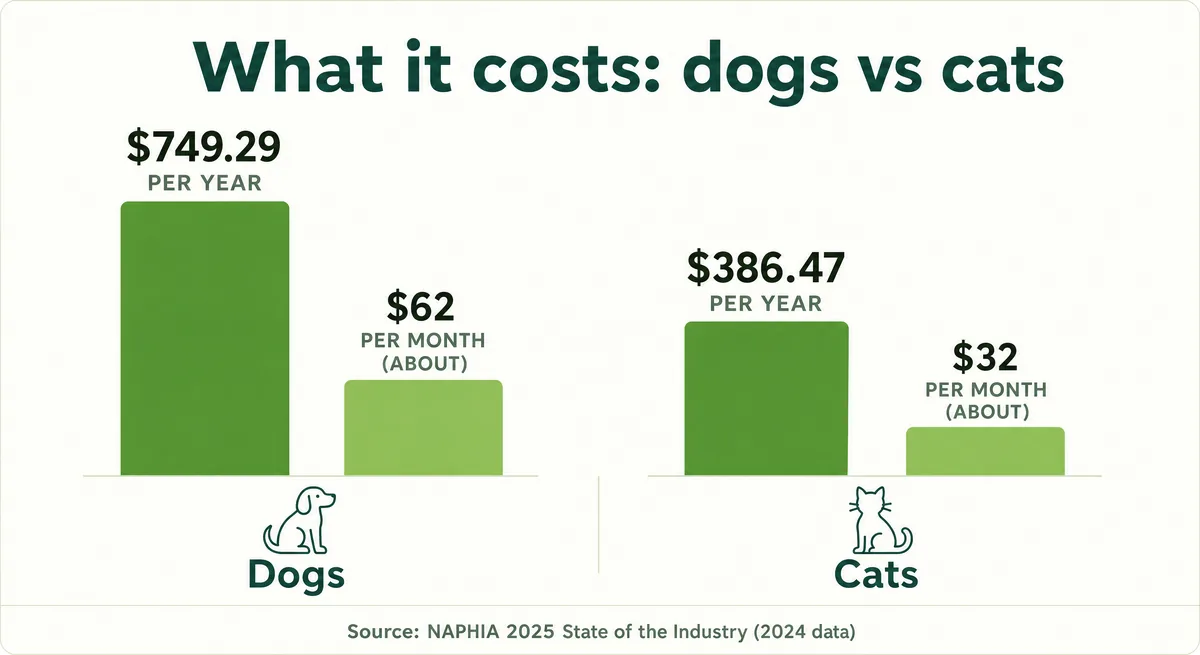

What you'll pay comes down to a handful of factors, and the biggest is the species. On the most common accident-and-illness plans, NAPHIA's 2024 industry data puts the U.S. average at about $749 a year (~$62/month) for dogs and $386 a year (~$32/month) for cats. Treat those as averages, not your quote: real premiums swing widely with your pet's breed and age, your ZIP code, and your plan choices, so your own number can land well below or above them.

So yes, it works a little differently by species: dogs cost roughly twice as much to insure as cats, because they tend to claim more often and their treatments run higher. The mechanics — reimbursement, deductibles, waiting periods — are identical; only the price and the most common conditions differ.

Beyond species, four things move your number:

- Breed. Bigger and higher-risk breeds cost more. On identical terms (Embrace's example prices a young dog in Texas), Embrace quotes a French Bulldog around $36/month versus a Chihuahua around $11 — a 3× spread from breed alone.

- Age at enrollment. Premiums are lowest for a young pet and climb every year as your pet ages — the main reason to enroll early.

- Where you live. Local vet costs feed straight into your premium, so the same pet costs more in a high-cost metro than in a rural ZIP.

- Your three dials. A higher deductible or a lower annual limit trims the premium; a higher reimbursement percentage raises it.

That's the shape of the cost; working out the exact number for your pet — and whether it pencils out — is a bigger exercise than this overview. Here, the takeaway is simple: dogs cost about double cats, you'll pay less the younger you start, and those three dials are yours to tune.

So, is it worth it?

Honest answer: for some pets it clearly is, for others it isn't — and "how does it work" and "is it worth it" are really the same question, so here's the short version before you dig deeper.

The case for it is simple: insurance protects you against the rare, huge bill you can't easily save your way to. Setting aside $100 a month is smart, but it won't cover a single $6,500 surgery in year two or a $10,000 emergency — the kind of bills owners describe over and over. And the money does flow the other way, too: U.S. insurers paid out about $3.07 billion in claims in 2024. Think of it less as a bet you hope to win and more as a budgeting tool that limits your exposure to a big covered bill — though your deductible, reimbursement percentage, annual limit, and any exclusions still shape what you actually pay.

The honest counterweight: premiums rise as your pet ages. A policy that looks cheap for a puppy or kitten gets pricier every year, and by the senior years some owners conclude they'd have come out ahead just saving. That's why insurance is most cost-effective when you start young and healthy — and why the "worth it" verdict depends heavily on your pet's age, breed, and your own tolerance for a surprise bill.

Working that math all the way out — premiums paid versus likely payouts over a lifetime — is its own exercise. Now that you understand how the machine works, the honest next step is the full break-even analysis.

Frequently Asked Questions

How does pet insurance work when I go to the vet?

You pay the vet the full bill yourself, then file a claim to get reimbursed — there's no insurance card to swipe at the front desk. During the visit you're just a normal paying customer. Afterward you send your insurer the itemized invoice (and usually your pet's recent records), and they pay you back a share of the covered cost by direct deposit or check, typically within a few days to a few weeks. A small number of carriers can pay your vet directly, but only if you arrange it in advance.

Do I pay the vet, or does the insurance company pay directly?

With almost every U.S. policy, you pay first and get reimbursed later — it's reimbursement insurance, not the copay-at-the-counter model you know from human health plans. That means you need to be able to front the whole bill, then wait for your money back. A few carriers (Trupanion is the best known) offer direct-to-vet payment at participating clinics, but treat that as the exception, not the rule.

Why didn't I get my full reimbursement percentage back?

Because your deductible comes out before the percentage is applied, and you still owe your coinsurance share. On an 80% plan with a $250 deductible, a $2,000 bill pays back $1,400, not $1,600 — that works out to 70% of the total, not 80%. Some line items, like the exam fee or sales tax, may also not count as “covered,” which trims the check a little more. It's normal, not an error.

What counts as a pre-existing condition?

Any condition your pet showed signs or symptoms of before your coverage started (or during a waiting period) — and a formal diagnosis isn't required. Under the model definition U.S. regulators use, a noted limp, itch, or stomach upset can be enough, and the insurer decides at claim time by reviewing your pet's records. This is why enrolling while your pet is young and healthy matters. Never skip or hide vet care to protect a future claim — get your pet the care it needs.

How soon does coverage start?

Not the day you sign up. Almost every policy has a waiting period — commonly a few days for accidents, about two weeks for illnesses, and often six to twelve months for orthopedic issues like cruciate ligaments, depending on the carrier and your state. Anything that appears during the waiting period is usually treated as pre-existing, so buying a policy after your pet is already sick won't cover that illness. Check your own policy's waiting periods before you assume you're covered.

What are the downsides of pet insurance?

The main ones: you pay the vet upfront and wait for reimbursement, coverage doesn't start immediately, pre-existing conditions are excluded, and premiums rise as your pet ages. Routine care isn't covered unless you add a wellness rider. None of that makes it a bad deal — it's protection against rare, large bills, not a way to save on everyday costs — but it's why insurance is most cost-effective when you enroll a young, healthy pet.

Does pet insurance cover a UTI?

Usually yes, on an accident-and-illness plan — a urinary tract infection is treated as an illness, so it's covered as long as it isn't pre-existing and your illness waiting period has already passed. If your pet had urinary symptoms before coverage began, that specific problem may be excluded as pre-existing. Coverage specifics vary by carrier, so confirm against your own policy.

Does pet insurance cover IVDD surgery?

Often yes, if you have accident-and-illness coverage, the condition isn't pre-existing, and any orthopedic or illness waiting period has passed. Intervertebral disc disease (IVDD) surgery can run into the thousands, which is exactly the kind of bill insurance is designed for — but breeds prone to it, like Dachshunds, make the pre-existing and waiting-period rules especially important to check before you actually need the coverage.

Sources

- Pet Insurance — NAIC — Center for Insurance Policy and Research

- Vet Direct Pay vs. Reimbursement — Trupanion

- Pet Insurance That Pays the Vet Directly — U.S. News & World Report

- Pet Insurance Deductibles — Progressive

- Deductibles — Trupanion

- How Does Pet Insurance Work? — ASPCA Pet Health Insurance

- Annual Reimbursement Limit — MetLife Pet Insurance

- How Pet Insurance Companies Calculate Your Refund — Embrace Pet Insurance

- What Is Reimbursement? — MetLife Pet Insurance

- Filing a Pet Insurance Claim — MetLife Pet Insurance

- Pet Insurance Claims — Healthy Paws Pet Insurance

- How to File a Claim — ASPCA Pet Health Insurance

- Pet Insurance Claims Process — MoneyGeek

- How Do Pet Insurance Waiting Periods Work? — U.S. News & World Report

- Frequently Asked Questions — Healthy Paws Pet Insurance

- Pet Insurance Model Act (MO-633) — National Association of Insurance Commissioners

- Pet Insurance and Pre-Existing Conditions — ASPCA Pet Health Insurance

- State of the Industry Report 2025 (Highlights) — NAPHIA

- Pet Insurance 101 — Progressive

- How Much Does Pet Insurance Cost? — Embrace Pet Insurance

- How Much Does Pet Insurance Cost? — MetLife Pet Insurance

- State of the Industry Report 2025 — NAPHIA

You may be interested...

More published guides that build on this topic.

Pet Insurance Basics

Pet Insurance Basics

How Does Pet Insurance Work If You Switch Providers?

Switching pet insurance starts a new policy, not a transfer. How it works, what resets, how insurers decide what's pre-existing, and when not to switch.

Pet Insurance Basics

Pet Insurance Basics

Is Pet Insurance Worth It in 2026? The Honest Math

We break down the financial reality of pet insurance in 2026 using current BLS, NAPHIA, NAIC, and veterinary sources.