If you've read three "best pet insurance" lists and walked away with three different winners, you're not imagining it. Somewhere around the fourth undated star rating, most shoppers do the same thing: they stop trusting review sites and add "reddit" to the search. That instinct is healthy. Most pet insurance reviews are built to sell you a policy, not to show you evidence.

This page works differently. Our scores come from the binding policy documents each carrier actually issues — not its marketing pages — read alongside regulator data: complaint records, state rate filings, and the new market-conduct data as it becomes public. And every volatile number on this page, from a score to a complaint index to a platform rating, carries the date we last verified it, because a rating without a date is a rating you can't trust.

One more thing before the verdicts. WhiskerCover is a licensed insurance agency — we can help you get your dog or cat covered, which is exactly why you deserve to know how we're paid. We explain that in plain English a short scroll below, before any recommendation, not buried in a footer.

The master ratings table comes first, so if you just need a shortlist, it's one scroll away. If you've been burned before, stay for the parts no review site shows: who really owns which brands, what regulators know that star ratings hide, and why every "best of" list names a different winner.

Table of Contents

- Our ratings at a glance

- What is the most trusted pet insurance?

- How we rate (and how we're paid)

- The reviews behind the reviews: who owns whom

- What regulators know that review sites don't show

- Why every “best pet insurance” list names a different winner

- Carrier-by-carrier verdicts

- Is any pet insurance actually worth it?

- The fine print that decides your claims

- What Reddit actually says (dated and screened for astroturf)

- Frequently Asked Questions

- Sources

Our ratings at a glance

As of July 2026, no major U.S. pet insurer earns better than 3.9 out of 5 on our board — which tells you something about the 4.8s and 4.9s you've seen elsewhere. Every score below comes from our own weighted rubric, built on each carrier's binding policy forms and the regulator record, and every score carries the date we assigned it. The full weights are published in How we rate (and how we're paid), and the clause-level evidence lives in our fine-print index.

One honest note on what's not in this table: we don't print NAIC complaint-index numbers here. For most of these brands, the underwriter writes several lines of insurance, so its complaint index blends pet policies with everything else it sells — quoting it per brand would look rigorous and mean almost nothing. The regulator section explains what the index can and can't tell you, carrier by carrier.

| Carrier | Our score (as of Jul 2026) | Underwritten by (financial strength) | Regulator & renewal record | What owners report (dated) |

|---|---|---|---|---|

| Embrace | 3.9 / 5 | American Modern (Munich Re) — AM Best A+, affirmed Jul 17, 2025 | — | Few fresh reports in our July 2026 capture |

| Spot | 3.7 / 5 | United States Fire (Crum & Forster) — AM Best A+, upgraded Aug 28, 2025 | — | Quiet positive claims stories; low annual caps criticized (Jan 2026) |

| AKC (PetPartners) | 3.7 / 5 | Independence American (IAIC) — AM Best A−, affirmed Dec 17, 2025 | — | Cited as the community's pre-existing escape — the 365-day exception (Jul 2025) |

| Prudent Pet | 3.6 / 5 | Markel Insurance Co. — Markel NA group AM Best A, affirmed Nov 21, 2025 | — | Trustpilot 4.8 (category capture Jan 29, 2026) |

| Trupanion | 3.5 / 5 | American Pet Insurance Co. — Demotech A′ ("Unsurpassed"), affirmed Jun 19, 2026; no AM Best rating exists | CA renewals: +12% (2023), +29% (2024), +33% avg (2025), each CDI-approved | Split verdict: "$54,400 paid across 3 dogs" vs. per-condition-deductible regret (May 2026) |

| Pumpkin | 3.5 / 5 | United States Fire (Crum & Forster) — AM Best A+, upgraded Aug 28, 2025 | — | $150/mo at age 10+, $250 projected next renewal — but $24k paid in final-year claims (May 2026) |

| ASPCA Pet Health Insurance | 3.5 / 5 | United States Fire (Crum & Forster) — AM Best A+, upgraded Aug 28, 2025; IAIC in some states — A−, affirmed Dec 17, 2025 | — | Few fresh reports in our July 2026 capture |

| Pets Best | 3.4 / 5 | APIC — Demotech A′, affirmed Jun 19, 2026 — or Independence American by policy — A−, affirmed Dec 17, 2025; check your declarations page | CA: +45% effective Apr 2, 2025 on APIC-written policies; insurer projected 12,700+ cancellations | Value praised; slow claim processing noted (Jul 2025) |

| Figo | 3.4 / 5 | Independence American (IAIC) — AM Best A−, affirmed Dec 17, 2025 | — | Mixed-to-negative via the Costco channel (Jul 2025) |

| Lemonade | 3.4 / 5 | Lemonade Insurance Co. (self-underwritten) — Demotech A (Exceptional) (current listing) | — | Budget pick; fast on simple claims, complex-claim denial disputes reported (Jan 2026) |

| MetLife Pet | 3.3 / 5 | Metropolitan General Ins. Co. or IAIC by state — no separate AM Best FSR published for Metropolitan General (checked May 2026); IAIC — A−, affirmed Dec 17, 2025 | — | Coverage praised — "grandfathered everything in"; service complaints (Apr 2026) |

| Fetch | 3.1 / 5 | XL Specialty (AXA XL) — AM Best A+, affirmed Oct 2025 | — | On the community avoid-list: rate increases tied to claim history reported (Feb 2026) |

| Healthy Paws | 2.9 / 5 | Chubb underwriters (ACE American et al.) — AM Best A++, affirmed Jan 16, 2026 | 2020 WA order: underwriters repaid $4.7M to ~18,000 policyholders over rating practices on policies sold through Healthy Paws (WA OIC) | Senior renewal exit stories — $240/mo at age 12 on a healthy lab (Mar 2026) |

| Nationwide | 2.6 / 5 | Veterinary Pet Insurance Co. / National Casualty — Nationwide group AM Best A, affirmed Nov 7, 2025 (downgraded from A+ in Dec 2023) | ~100,000 pet policies non-renewed from mid-2024 (CBS News); a class action over it is pending — allegations, not findings | Denial-scope confusion and exit anger (Jun 2026) |

| Physicians Mutual | Not yet scored — policy-form audit pending | Underwriter not yet verified by us | — | The community's anti-private-equity pick (Apr 2026) |

| Odie | Not yet scored — underwriter panel in transition | Multi-carrier panel (Trisura, Accredited, Clear Blue — in flux) | — | "Stay away" warnings (Jan 2026); 155 BBB complaints in 3 years, as of Jul 4, 2026 |

How to read this: a dash means our July 2026 research pass found no state-regulator action or documented mass renewal event for that carrier — it is not a clean bill of health, just an absence of documented record. Scores are ours alone; they deliberately do not echo any other site's ratings. The owner-report column summarizes dated, screened community threads — sentiment evidence, not statistics. And two carriers stay unscored on purpose: we don't rate what we haven't audited.

If you just need a shortlist

- A pet likely to develop a chronic, expensive condition: Trupanion — unlimited payouts and true direct vet pay, if you go in accepting the documented renewal record above.

- A balanced first policy for a young, healthy pet: Embrace — short waiting periods, an orthopedic waiver option, and the strongest overall terms on our board.

- A senior pet other carriers won't enroll: Spot — no upper age limit at enrollment.

- Switching with a medical history: AKC — the only major carrier with a 365-day path to covering pre-existing conditions (not offered in Florida or Washington). Read the switching-trap answer in the FAQ before you move.

- Budget first: Lemonade or Pets Best — cheapest way into real coverage, with the trade-offs listed above in plain view.

Those are conditional calls, not crowns. The rest of this page shows the evidence behind every cell — starting with exactly how we score, and who pays us.

What is the most trusted pet insurance?

The most trusted pet insurance is the one whose underwriter holds a current financial-strength rating, whose complaint record with state regulators runs below average for its size, and whose renewal price increases are documented and moderate. No star average measures any of those three things, so "most trusted" has no single-name answer.

That definition isn't ours by accident — each test rests on evidence regulators actually collect. The table above carries the first and third tests in its columns; the second, the complaint record, gets its own section below.

A rated underwriter. The brand on the ad is not necessarily the company that pays your claim. The NAIC Pet Insurance Model Act requires insurers to disclose when the underwriting company differs from the marketing brand — regulators treat that gap as a consumer-protection issue. So trust starts with knowing who actually stands behind the policy, and whether AM Best or Demotech currently rates them.

A below-average complaint record. The NAIC publishes a complaint index for every insurer: 1.0 means the company drew an average share of complaints for its premium volume; higher means more. It's the closest thing to an objective trust score that exists — with real limits we unpack in the regulator section, because for most pet brands the index blends in the underwriter's other lines of business.

A documented renewal record. Trust isn't tested at signup — it's tested at renewal, when the premium moves. State rate filings are the receipts: California's insurance department tells shoppers outright to ask whether premiums rise with age and claims. A carrier whose increases are on file and moderate has earned something no testimonial can.

Notice what's missing from that test: star ratings. When owners ask "most trusted," what they mean — in their own words — is "did claims actually get paid", and stars don't answer that either. We won't crown one winner, because the trustworthy choice depends on your pet: the carrier you trust with a chronic illness is not the one you trust to stay affordable for a healthy cat. The table above applies all three tests to sixteen carriers, dated.

How we rate (and how we're paid)

Here is the whole machine: the weights we score with, the documents we score from, and the money behind the page. If a review site won't show you all three, you're reading its incentives, not its research.

The scoring weights, in full

| What we score | Weight | What feeds it |

|---|---|---|

| Policy fine print | 30% | The binding policy form: how "pre-existing" is defined and how far back it looks, waiting periods (including orthopedic), deductible structure (annual vs. per-condition), exam-fee treatment, direct vet pay, enrollment age caps |

| Renewal behavior | 25% | Documented premium trajectory: state rate filings, regulator-approved increases, mass non-renewals — plus dated owner-reported renewal quotes as corroboration |

| Claims & service experience | 20% | Dated, astroturf-screened community reports of claims actually paid or fought, processing speed, and support quality |

| Regulator record | 15% | Enforcement actions and restitution orders, complaint data where it's meaningful for the underwriter, and market-conduct filings as they become public |

| Financial strength | 10% | The underwriter's current AM Best or Demotech rating, with its affirmation date |

Two of those weights deserve a word of defense. Renewal behavior gets a quarter of the score because it is the single most documented consumer harm in this market: California's regulator approved single-year increases of 25–45% on some carriers' renewal books in 2025 alone, while veterinary-services inflation ran about 6.5% in 2025 — a gap a shopper only discovers at renewal, unless a review told them first. And fine print gets the largest weight because it decides claims: two policies with identical premiums can treat the same limping dog completely differently, depending on a lookback clause.

What we read (and what we don't)

Every score starts with the carrier's policy form — the contract you'd actually sign — pulled state by state where terms differ. That's where the real answers live: the definitions section, the exclusions list, the deductible mechanics. Marketing pages, press releases, and other review sites' scores are not inputs; when we quote a platform rating or a community thread, it appears as context, dated, never as the basis of a score. The full process, including how often each input is re-verified, is on our methodology page.

What we can't read, we say so: insurers' claim-denial rates are filed confidentially with regulators, so no site — including this one — knows them. Where a cell in our table rests on thinner evidence, the capsule for that carrier says so plainly.

And because carriers change underwriters, ratings get affirmed or pulled, and renewal books get re-filed, every volatile figure here is re-verified on a rolling basis — the page's last-verified date moves only after the whole board has been rechecked. A rating that was true in January and quoted in July isn't a small error in this market; it's how shoppers end up trusting a carrier that no longer exists in the form they read about.

How we're paid, in plain English

WhiskerCover is a licensed insurance agency. If you buy a policy through us, the insurer typically pays us a commission. That is the business model — not banner ads, not selling your data, not charging you.

Three commitments keep that money away from the scores. First, scores come out of the rubric above before any commercial consideration enters the room; nobody re-scores a carrier because of a payout rate. Second, no carrier can pay for placement — the table sorts by score, and several carriers on it pay us nothing at all. Third, when a carrier we can earn commission from scores badly, the score stands; you can check that claim against the table above, where partner and non-partner carriers sit in the same columns with the same dates.

You also won't find the word "independent" anywhere on this page — on purpose. The FTC's Consumer Review Rule, in force since October 21, 2024, treats a company-controlled review site that misrepresents its independence as a violation, and the FTC's own guidance says a disclosure can't cure an express independence claim. We sell insurance and we rate insurers; the honest posture is to show you the rubric and the receipts, and let you judge whether the evidence holds up.

The reviews behind the reviews: who owns whom

The U.S. pet insurance shelf looks like dozens of competing companies. Underneath, it's a handful of underwriters — and, increasingly, one owner. That matters for a simple structural reason: reviews attach to brands, but complaints, rate filings, and solvency attach to underwriters. The NAIC's Pet Insurance Model Act requires insurers to disclose when the underwriting company differs from the marketing brand, because regulators already treat that gap as a consumer-protection issue. A reviews page that doesn't map it can't actually explain what it's rating.

The map: brands, underwriters, owners

| Underwriter (who pays claims) | Brands sold on its paper | Worth knowing |

|---|---|---|

| United States Fire (Crum & Forster) | Spot, Pumpkin, ASPCA Pet Health Insurance / Hartville | The ASPCA doesn't run its brand — it licenses the name for royalties |

| Independence American (IAIC) | Figo, AKC (PetPartners), Pets Best and ASPCA-brand policies in some states, some MetLife Pet policies | IAIC is the Doubtless group's own carrier |

| American Pet Insurance Co. (APIC) | Trupanion, Pets Best (part of the book), Chewy CarePlus in some locations | Pet-only insurer — its record maps ~1:1 to pet policies |

| American Modern (Munich Re) | Embrace, incl. the USAA program | |

| Chubb (ACE American et al.) | Healthy Paws | Chubb bought the Healthy Paws program in 2024 |

| XL Specialty (AXA XL) | Fetch | Not part of the Doubtless group — often misfiled there |

| Lemonade Insurance Co. | Lemonade, Chewy CarePlus in other locations | Self-underwritten public company |

| Metropolitan General / IAIC by state | MetLife Pet | |

| Veterinary Pet Ins. Co. / National Casualty | Nationwide pet | The book shrank by ~100,000 policies from mid-2024 |

| Markel Insurance Co. | Prudent Pet | |

| Rotating panel (Trisura, Accredited, Clear Blue) | Odie | Landing pad for ManyPets' U.S. exit; panel in flux |

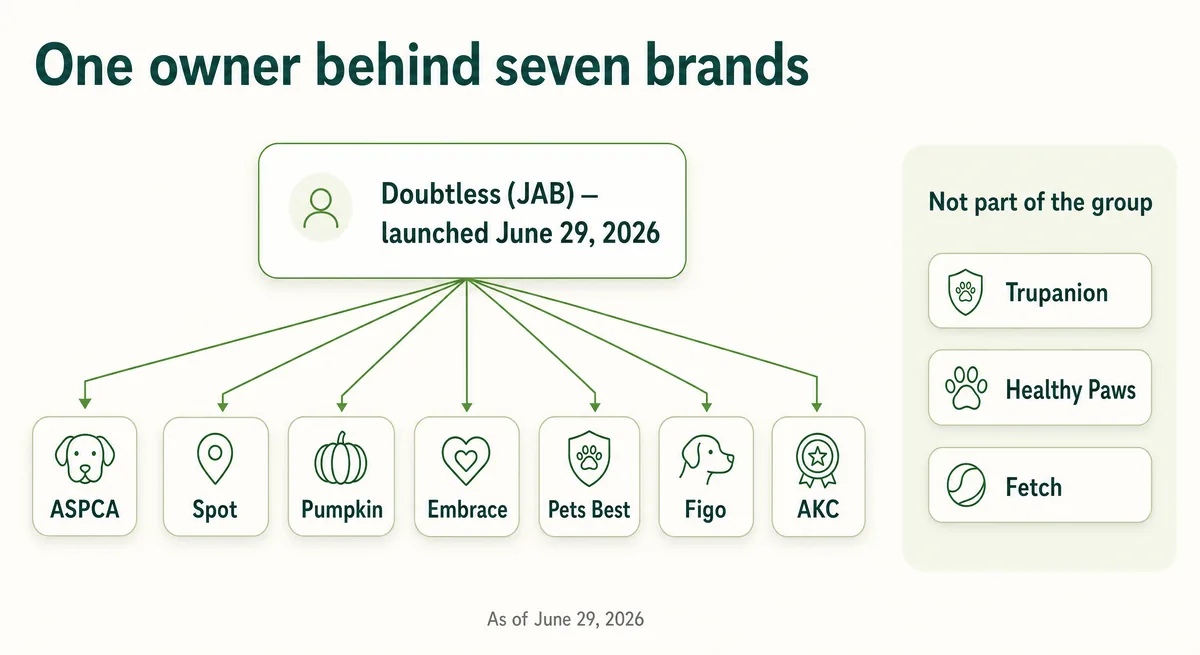

One owner behind seven brands

On June 29, 2026, JAB's pet insurance platform relaunched globally as Doubtless — six million insured pets across ten markets, and one owner standing behind ASPCA Pet Health Insurance, Hartville, Figo, AKC, Pets Best, Pumpkin, Embrace, and Spot, plus the underwriter IAIC. The pieces were bought one by one: Pumpkin in May 2023, Pets Best in early 2024, Spot in June 2024.

So when a best-of list presents ASPCA and Spot as rival winners, it's comparing two storefronts of the same underwriting family. Pet owners have started to notice — a widely upvoted Reddit comment lists the brands under one owner and concludes they're "making a pet insurance monopoly" — though the community's version of the list usually includes Fetch, which is wrong: Fetch rides AXA XL paper and isn't part of the group. That's worth correcting in both directions.

To be equally clear about what consolidation does not mean: shared ownership doesn't make the products identical. Spot and Pumpkin sit on the same underwriter and still differ on caps, cure windows, and price. What consolidation does concentrate is everything upstream of the product — reinsurance, pricing strategy, claims infrastructure — which is why we rate brands but always show you the underwriter.

Financial strength, with dates

Three rating events from the past year show why an undated financial-strength letter is nearly useless.

- Crum & Forster was upgraded to AM Best A+ (Superior) on August 28, 2025 — yet most review pages still print the stale "A" for Spot, Pumpkin, and ASPCA policies. In this case, undated means undersold.

- IAIC spent four months under review. AM Best placed it under review on August 6, 2025 after re-filed 2024 statements showed its pet reinsurance failed risk transfer, and removed the status — affirming A− — on December 17, 2025, after renegotiated reinsurance and a $125 million capital contribution from its parent. A shopper reading an undated "A−" that fall had no idea any of it was happening.

- Trupanion's underwriter has no AM Best rating at all. The "AM Best downgraded APIC to B++" claim that circulates on review sites traces to no AM Best release we could find; APIC's actual rating is Demotech A′ (A Prime, "Unsurpassed"), affirmed June 19, 2026. Repeating the myth makes Trupanion look downgraded; omitting the Demotech rating makes it look unrated. Both errors are live on this SERP right now.

The roster itself also moves: ManyPets left the U.S. market, with renewals handed to Odie from January 1, 2025, and Companion Protect no longer sells direct to consumers (its site redirected to a business-programs page when we checked on July 4, 2026). At least one prominent review aggregator still listed ManyPets as an active choice this summer. Dating the roster isn't pedantry — it's the difference between reviewing the market and reviewing a memory of it.

What regulators know that review sites don't show

Three layers of regulator data exist for pet insurers — a complaint index, a brand-new market-conduct dataset, and an enforcement paper trail — and as of July 2026, no page ranking for "pet insurance reviews" uses more than a sliver of any of them. Here's what each one can tell you, what it can't, and how to pull it yourself.

The NAIC complaint index — powerful, and easy to misread

Every state files consumer complaints into a national database, and the NAIC turns them into a complaint index: 1.0 means a company drew exactly its expected share of complaints for its premium volume; 2.0 means twice its share. It's the closest thing to an objective, cross-company trust score in insurance.

Two things make it misleading if you quote it carelessly — which is exactly how review sites quote it, when they quote it at all. First, the index is computed per legal entity and line of business. Most pet brands ride on underwriters that also sell auto, home, and specialty lines, so the entity's index blends pet complaints with everything else — you cannot read Spot's claim-handling off United States Fire's number. Only a pet-dedicated insurer, like Trupanion's American Pet Insurance Company, maps roughly one-to-one. Second, the values move every year, and the NAIC serves them through an interactive lookup rather than a page you can link — so any index number you read without a retrieval date is a number of unknown age.

To check a carrier yourself, open the NAIC's Consumer Insurance Search, enter the underwriter's NAIC code from our ownership map (Trupanion's APIC is 12190), click the company result, and choose "Go To Complaint Trend Report." Sixty seconds, primary source, current year — better than anything a star rating can tell you.

The new pet MCAS — denial reasons, finally counted

Since the 2024 data year, every insurer writing any U.S. pet premium must file a pet-specific Market Conduct Annual Statement — there's no minimum-premium exemption. The filing instructions show what regulators now count that reviewers never could: claims closed without payment broken out by reason — pre-existing condition exclusion, waiting period, hereditary exclusion, benefit limit, below-deductible — plus company-initiated non-renewals, applications declined for health status, and lawsuits closed with consideration for the consumer.

Here's the honest catch: company-level filings are confidential. What's public is the state-level scorecard dashboard, with 2024 and 2025 data already posted. That means a hard rule you can use against any review site: no public per-carrier claim-denial rate exists for U.S. pet insurance. Any page quoting one — "Carrier X denies 14% of claims" — is quoting something that cannot be sourced. We'd love to print those numbers too. Nobody can.

The enforcement record — history with dates on it

The paper trail is thinner than you'd expect, which is itself information — but what exists is specific, and it clusters exactly where owner complaints cluster: pricing practices.

- 2020, Washington: the state fined two Chubb underwriters $950,000 (with $200,000 suspended) and ordered $4.7 million repaid to roughly 18,000 policyholders over policies sold through Healthy Paws — including raising rates based on pet age when filings said age wouldn't be a factor. Six years old now; we date it and weigh it as history, not headline.

- 2016–2019, Washington: the Trupanion group drew fines totaling $500,000 across three orders — incorrect rates and complaint handling, sales through unlicensed sellers, and gifts to vet clinics. Same caveat: dated history.

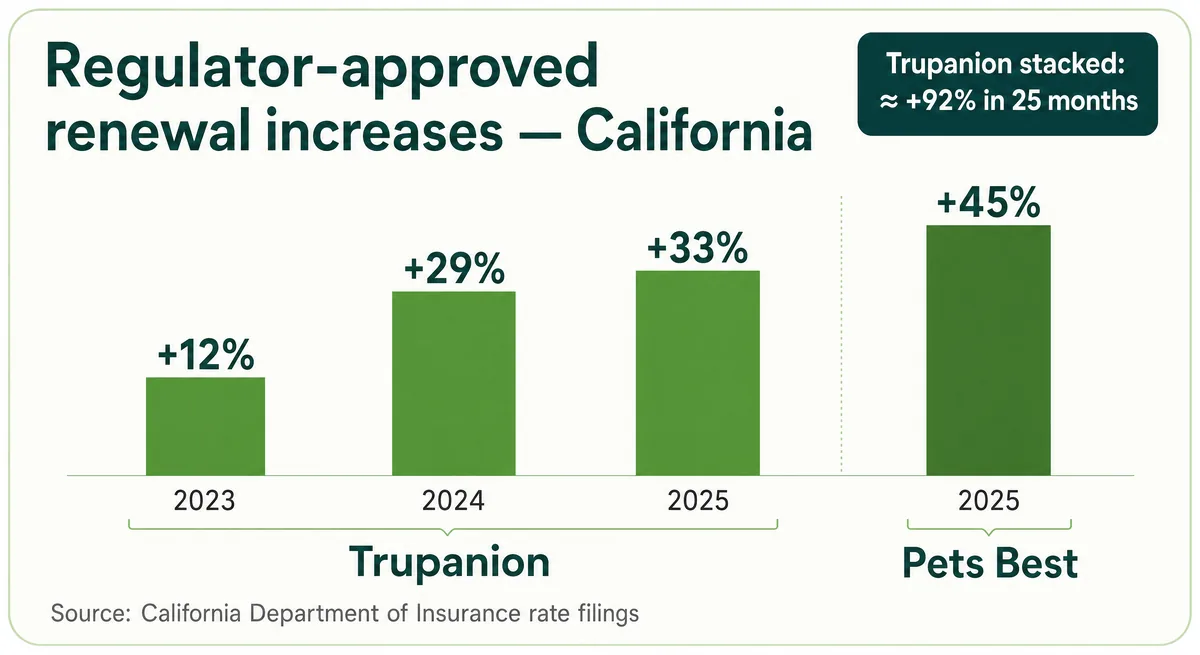

- 2023–2025, California: the current record is rate filings, not fines — the CDI approved the stacked Trupanion increases and the 45% Pets Best increase detailed in the renewal section below, and now maintains a public roster of pet insurers doing business in the state.

- March 2025, Washington: a $30,000 fine and cease-and-desist against a company marketing an unlicensed pet "insurance" club — proof the category is being watched.

Read the pattern: regulators have acted on how pet insurance is priced and sold, almost never on whether individual claims were wrongly denied — that's what MCAS was built to surface next. So when a review page shows you five stars and no filing history, it isn't summarizing this record. It just never looked.

Why every “best pet insurance” list names a different winner

Because "best" is a formula, and every site runs a different one. In our early-July 2026 audit of the pages ranking for pet insurance reviews, the major lists crowned different winners in the same season — not because the carriers changed, but because the scoring recipes did. Once you see the four mechanisms, the disagreement stops being confusing and starts being useful.

1. Weight artifacts. Forbes Advisor's methodology, as captured July 1, 2026, put half its score on cost — plan pricing counted for 50%, more than coverage, satisfaction, and company integrity combined. MoneyGeek ran affordability at 50% too (June 2026 capture). A formula that's half price will reliably crown the cheapest credible carrier — which tells you what's cheap, not what pays claims well at renewal time.

2. Micro-samples presented as findings. U.S. News (May 14, 2026 capture) built 60% of its score on a satisfaction survey of 844 respondents spread across 11 brands — roughly 77 owners per carrier, with per-brand counts undisclosed. Per-brand slices that thin swing on a handful of experiences, yet they're rendered as decimal-point ratings.

3. "Competitors" that share an owner. NerdWallet's list (May 1, 2026 capture) ended in a five-way 5.0 tie: ASPCA, Spot, MetLife, Hartville, and Pumpkin. Four of those five ride the same underwriting family we mapped in the ownership section. A tie between four storefronts of one group isn't a competition — it's a catalog.

4. Monetization sitting next to the ratings. Pet Insurance Review — the aggregator that ranks for this keyword — displayed a "100% Independent" badge in July 2026 with no methodology page anywhere, scores clustering at 4.9 for Embrace, Healthy Paws, Fetch, Trupanion, and Pets Best alike, and disclosed paid-click monetization. Pet Insurance Gurus lists "AM Best rating of the underwriter" among its criteria — and prints no actual rating on the page. We state these as observations from the pages themselves, dated; draw your own conclusion about what a uniform wall of 4.9s can discriminate. Credit where due: Pawlicy Advisor — a licensed agency like us — refuses to print numerical scores at all and names underwriters; but its page hadn't been refreshed since February when we checked in July 2026, and stale honesty still misleads.

Now set all of that against the one rater with no affiliate stake. Consumer Reports, surveying 3,583 members between December 2024 and January 2025, concluded that none of the 14 providers it rated rose above a middling grade — while 53% of insured owners were very or completely satisfied and only 34% said they saved more than they paid in premiums and deductibles. And the review platforms can't even agree with each other: Trustpilot's category page (captured January 29, 2026) had Trupanion and Nationwide at 4.4 while Pet Insurance Review scored the same carriers 4.9. Somebody's instrument is broken, and it isn't the pet owners'.

None of this means the incumbent lists are corrupt — cost-heavy weighting is a defensible choice if you know it's there. It means a "best" verdict is meaningless without its formula. So use any best-of list, including ours, the same way:

- Find the weights first. If you can't find them, you've learned the most important thing already.

- Check the sample. A satisfaction score without an n and a date is decoration.

- Map the winner to its underwriter and owner. Two "rival" winners from one family means the list compared brands, not insurers.

Our formula is published above, weights and all, precisely so you can run this test on us.

Carrier-by-carrier verdicts

Sixteen capsules, ordered by our score, each built the same way: the score with its date, who underwrites the policy, the fine-print clause that most defines it, the dated reputation record, what owners consistently report, and who it actually fits. These are deliberately short — each carrier gets a dedicated full review that goes clause-by-clause; until a carrier's review publishes, its capsule here is our complete verdict.

Embrace — 3.9/5

Score as of July 2026. Underwritten by American Modern (Munich Re), AM Best A+ affirmed July 17, 2025. The fine-print standout is the front end: no waiting period for accidents, 14 days for illness, and the six-month orthopedic wait can be shortened with a vet exam waiver — the trap that catches most new policies, largely defused. No regulator-documented renewal event in our July 2026 pass, and community chatter is quiet, which for a pet insurer is praise. Best for: a young, healthy pet whose owner wants the strongest all-around terms on our board. Full review → our dedicated Embrace review is in production; until then, this is our complete verdict.

Spot — 3.7/5

Score as of July 2026. Underwritten by United States Fire (Crum & Forster), AM Best A+ upgraded August 28, 2025. Two clauses define it: no upper age limit at enrollment — rare, and decisive for senior pets — and a 180-day cure window that lets a curable pre-existing condition come back into coverage, with the standard carve-out: knee and ligament events are excluded from that mercy. Owners report smooth, quick claim payments, with the recurring caution that low annual caps ($5k) are too thin for real emergencies — pick the higher limit. Part of the Doubtless family. Best for: senior pets and owners who want forgiveness on cured conditions. Full review → our dedicated Spot review is in production; until then, this is our complete verdict.

AKC (PetPartners) — 3.7/5

Score as of July 2026. Underwritten by Independence American, AM Best A− affirmed December 17, 2025. One clause earns this ranking: after 365 days of continuous coverage, AKC's plans can cover even incurable pre-existing conditions — the only escape hatch of its kind among major carriers (not offered in Florida or Washington), and the reason the community treats it as the pre-existing workaround. The trade-offs: longer standard waiting periods and a Doubtless-family underwriter that spent late 2025 under ratings review before its affirmation. Best for: switchers and owners of pets with a medical history who can commit to a full year. Full review → our dedicated AKC review is in production; until then, this is our complete verdict.

Prudent Pet — 3.6/5

Score as of July 2026. Underwritten by Markel Insurance Company, Markel NA group AM Best A affirmed November 21, 2025. Our policy-form audit found no standout trap, and its platform reputation runs unusually high — Trustpilot 4.8 at the January 29, 2026 category capture. The honest caveat: the record is thin because the book is smaller and younger than the giants', so there are simply fewer renewals and claims to judge. Independent of the Doubtless group. Best for: owners who want a well-rated independent and accept a shorter track record. Full review → our dedicated Prudent Pet review is in production; until then, this is our complete verdict.

Trupanion — 3.5/5

Score as of July 2026 — and the sharpest split verdict on this page. Underwritten by its own American Pet Insurance Company: no AM Best rating exists (despite what some review sites claim), but Demotech rates it A′, affirmed June 19, 2026. The fine print gives with one hand — no payout caps, true direct vet pay at checkout, per-condition deductibles that go to $0 — and takes with the other: an 18-month lookback that counts even signs of a condition, exam fees never covered, and each "new" condition restarting its own deductible, which owners of repeat-symptom pets experience as a deductible treadmill. The renewal record is regulator-documented: CDI-approved increases of +12%, +29%, and +33% average stacked across 2023–2025 in California — the middle step confirmed in Trupanion's own release on the approval. Owners with chronically ill pets report five-figure payouts and stay; owners of healthy pets watch premiums climb and leave. Both are right. Best for: a pet likely to develop an expensive chronic condition, insured young and held. Full review → our dedicated Trupanion review is in production; until then, this is our complete verdict.

Pumpkin — 3.5/5

Score as of July 2026. Underwritten by United States Fire (Crum & Forster), A+ as above. Fine print sits in the friendly cluster: 180-day cure window with the knee carve-out, 90% reimbursement as the standard shape. The reputation signal to know: owners of older pets report steep late-life pricing — one dated account put a 10-year-old dog at $150/month with $250 projected — while the same policy paid roughly $24,000 in final-year claims. That's the senior-pet bargain in one anecdote: expensive, and it paid. Doubtless family. Best for: owners who want high reimbursement percentages and accept senior-age pricing. Full review → our dedicated Pumpkin review is in production; until then, this is our complete verdict.

ASPCA Pet Health Insurance — 3.5/5

Score as of July 2026. Underwritten by United States Fire (Crum & Forster), A+ as above; IAIC in some states. Know what the name is: the ASPCA licenses its brand for royalties — the charity doesn't run the insurer. The product itself mirrors its Doubtless siblings: 180-day cure window, knee/ligament carve-out, customizable plans. Few fresh owner reports surfaced in our July 2026 capture; its complaint themes historically track the family's shared claims infrastructure. Best for: owners who want the Spot/Pumpkin-style terms from the family's longest-standing storefront — just don't pick it because of the name on the door. Full review → our dedicated ASPCA review is in production; until then, this is our complete verdict.

Pets Best — 3.4/5

Score as of July 2026. Underwriting is split by policy vintage between APIC and Independence American (A−, December 17, 2025) — check your declarations page. The value case is real: consistently among the cheapest credible quotes, plus vet payment after adjudication via release form. The record cuts both ways: California approved a 45% renewal increase effective April 2, 2025 on APIC-written policies — with the insurer itself projecting 12,700+ cancellations — and owners report slower-than-average claim processing alongside genuinely paid large claims. Best for: budget-first buyers who understand the renewal risk they're pricing in. Full review → our dedicated Pets Best review is in production; until then, this is our complete verdict.

Figo — 3.4/5

Score as of July 2026. Underwritten by Independence American (A−, December 17, 2025). Its fine-print distinction is the reimbursement ceiling — plans run up to 100%, which almost nobody else offers (note the pairing rules: the 100% option isn't available with every deductible and annual-limit combination). Reputation is mixed and channel-dependent: the sharpest complaints in our capture came through the Costco-sold version — coverage denials and cancellation friction — and its underwriter spent August–December 2025 under ratings review before affirmation. Doubtless family. Best for: owners chasing a 100% reimbursement structure who buy direct and read the exclusions first. Full review → our dedicated Figo review is in production; until then, this is our complete verdict.

Lemonade — 3.4/5

Score as of July 2026. Self-underwritten by Lemonade Insurance Company, Demotech A (current listing). The budget entry point of the scored field: cheap, instant-feeling, with exam fees sold as an add-on rather than included. The split: simple claims pay fast — often near-instantly — while complex claims can meet the AI underbelly; a January 2026 dispute over a five-figure chronic-kidney claim, denied with reference to a predictive tool, is one owner's account, but it matches the pattern owners describe: great until it's complicated. Best for: young healthy pets on a budget, with the higher limits and the add-ons taken seriously. Full review → our dedicated Lemonade review is in production; until then, this is our complete verdict.

MetLife Pet — 3.3/5

Score as of July 2026. Underwritten by Metropolitan General or Independence American depending on state — and note that Metropolitan General had no separately published AM Best financial-strength rating when we checked in May 2026 (the "A+" quoted on review sites belongs to MetLife's life-insurance companies). Coverage earns real praise: multi-pet handling, and a documented case of a switcher whose conditions were grandfathered in rather than re-excluded. Operations are the complaint: unreachable support and enrollment errors recur in owner reports, and one documented first-year renewal in our capture ran roughly +40%. Best for: multi-pet households that value coverage breadth over service polish. Full review → our dedicated MetLife review is in production; until then, this is our complete verdict.

Fetch — 3.1/5

Score as of July 2026. Underwritten by XL Specialty (AXA XL), AM Best A+ affirmed October 2025 — and not part of the Doubtless group, despite what community lists claim. The terms look generous on paper — sick-visit exam fees are covered as a standard policy item, which most carriers don't do. The reputation problem is renewal behavior: the community's most consistent warning is rate increases tied to claim history, with slow reimbursements in the same threads — and one owner reports that asking whether something was covered was itself counted as a claim (a single account we could not corroborate; we flag it because the chilling effect is the point). Best for: honestly, few situations while the claim-history pricing reports persist — the included exam fees are real value only if renewals stay affordable enough to keep the policy. Full review → our dedicated Fetch review is in production; until then, this is our complete verdict.

Healthy Paws — 2.9/5

Score as of July 2026. Underwritten by Chubb companies, AM Best A++ affirmed January 16, 2026 — the strongest paper on this page, wrapped around its weakest trend line. The fine print is dated where it counts: exam fees never covered, and a 12-month hip-dysplasia wait with permanent exclusion if enrolled at six or older. The record: the 2020 Washington order over age-based rating ($4.7M repaid), a still-unresolved age-escalation lawsuit (allegations, not findings), owner-reported senior premiums like $240/month at age 12, and policyholder-reported notices — unconfirmed by the company — of benefits moving to 70%/$500 in December 2025. Best for: almost no new buyer today; existing policyholders should read our switching-trap answer before leaving. Full review → our dedicated Healthy Paws review is in production; until then, this is our complete verdict.

Nationwide — 2.6/5

Score as of July 2026. Underwritten by Veterinary Pet Insurance Co. / National Casualty; Nationwide group AM Best A affirmed November 7, 2025, a notch below its pre-2023 A+. The score is about commitment: Nationwide non-renewed roughly 100,000 pet policies from mid-2024, and a pending class action — allegations, not findings — quotes its own marketing promise never to drop pets for age. Owner threads add denial letters whose scope owners can't parse. A carrier can pay claims well and still strand you at renewal; that's the specific risk here. Best for: existing members with legacy plans worth keeping — not new money. Full review → our dedicated Nationwide review is in production; until then, this is our complete verdict.

Physicians Mutual — not yet scored

We don't rate what we haven't audited, and as of July 2026 our policy-form audit of Physicians Mutual's pet product is pending — so no number. What we can report, dated: it's a newer entrant to pet insurance, and community sentiment is notably warm for a reason that says everything about this market — owners recommend it as the carrier least likely to be acquired by private equity. That's a trust thesis, not a coverage verdict. Best for: watch this space; we'll score it when the audit completes. Full review → our dedicated Physicians Mutual review is planned; this capsule will carry the score first.

Odie — not yet scored

Unscored on purpose: Odie's underwriting panel is in transition (Trisura, Accredited, and Clear Blue entities appear across its own disclosures), and it absorbed ManyPets' exiting U.S. book from January 1, 2025 — a migration that produced a measurable complaint wave: 155 BBB complaints in three years, 143 of them in the last twelve months, as of July 4, 2026. Community shorthand is blunt avoidance. Scoring a company mid-transition would date instantly; we'll rate it when the panel settles. Best for: ManyPets refugees who should compare their migrated terms against the market before renewing. Full review → our dedicated Odie review is planned; this capsule will carry the score first.

Is any pet insurance actually worth it?

Usually yes — but not as a way to save money, and the industry's own numbers say so. In Consumer Reports' member survey (3,583 respondents, December 2024–January 2025), only 34% of insured owners saved more than they paid in premiums and deductibles — yet about two-thirds still called pet insurance worth it. Both numbers are true, and the gap between them is the honest answer.

The gap closes when you understand what you're buying. Most owners lose a little money on pet insurance most years — that's how insurance works. What they're paying for is the year they don't lose: the emergency where treatment is possible but expensive, and the decision would otherwise be made by their bank balance. Veterinary professionals put this more bluntly than any brochure; the most-upvoted vet answer in our community research says the point isn't saving on vet bills — it's never having to put a pet down for financial reasons.

The math makes the same case. Consumer Reports' surveyed owners paid median premiums of $654 a year for dogs. Set that against a single common orthopedic emergency: TPLO surgery for a torn ACL averages about $3,525, and ranges to $6,417 — one incident that can swallow five-plus years of premiums, and cruciate tears are famously bilateral. Owners who carry coverage know this trade: in a January 2026 U.S. News survey of 1,500 pet owners, 86% of insured owners said they get their money's worth — while 65% of the uninsured said cost is what keeps them out.

And yet the self-insurance argument deserves a straight telling, because it now wins top-comment slots even in threads where a pet died: put the premium into a dedicated savings account and cover emergencies yourself. That's rational — under conditions. So here's the conditional answer, not a crown:

- Young, healthy pet and thin savings: insurance is worth it — you're buying the best odds that a covered $5,000 night at the ER stays a bill, not a goodbye, within your policy's limits and exclusions.

- Substantial liquid savings and a tolerance for tail risk: self-insuring can be defensible — if the account really exists, really grows, and you'd really spend it at 2 a.m.

- Older pet or one with a medical history: run the numbers before assuming either way — enrollment caps and pre-existing exclusions change the math, and the fine print below decides more than the premium does.

We keep a full worked analysis — break-even math by pet age and scenario — in our guide to whether pet insurance is worth it. For this page, the verdict-relevant point is simpler: "worth it" depends far more on which policy and which clauses than on the category — which is why the capsules above rate carriers, not the concept.

The fine print that decides your claims

Star ratings measure how people feel; clauses decide what gets paid. These are the three clause families that generate the most denied claims, the most renewal shock, and the most regret in every thread we screened — with the actual carrier-by-carrier spread, dated.

Does any pet insurance cover hip dysplasia?

Yes — most accident-and-illness policies cover hip dysplasia, but three clauses decide whether yours will: the orthopedic waiting period, the enrollment-age cutoff, and the bilateral exclusion. Miss any one of them and a covered condition becomes a denied claim.

The spread is wide. Embrace runs a six-month orthopedic wait that can be shortened with an orthopedic exam waiver. Healthy Paws applies a 12-month hip dysplasia wait — and excludes hip dysplasia permanently if your pet enrolls at age six or older. And the bilateral exclusion is the quiet one: if one hip (or knee) shows trouble before coverage, many policies exclude the other side too, on the logic that bilateral conditions are one condition. Regulators are tightening this space — the NAIC model act caps waiting periods at 30 days and mandates exam-based waivers in the states that have adopted it, and California went further by statute. But adoption is state-by-state, so read your state's rules, not a national average.

Does pet insurance cover diabetes and other chronic conditions?

Yes — if the policy was in force before the first symptom hit the chart. Enrolled after? Then it depends entirely on how your carrier defines "pre-existing," and that definition varies more than any other clause in pet insurance.

The documented spread: Trupanion applies an 18-month lookback that counts even signs of a condition that was never diagnosed. ASPCA, Spot, Pumpkin, and Hartville run 180-day cure windows — a condition that stays symptom- and treatment-free for 180 days is treated as new again — with knee and ligament conditions carved out of that forgiveness. Healthy Paws uses a 12-month window; AKC stands alone with a 365-day path that can cover even incurable pre-existing conditions. Two protections worth knowing from the model act — in the states that have enacted it, and in policies whose language mirrors it: the burden of proving a condition was pre-existing sits on the insurer, and a carrier can't reclassify a condition it already covered at renewal.

The fights owners actually have are rarely about a diagnosis — they're about classification. A stray "signs of" entry in an old chart becomes the anchor for a pre-existing denial years later; the same mechanics let repeated symptoms be split into separate conditions, each restarting its own per-condition deductible. Two practical defenses from the veterans' playbook: if a denial letter is ambiguous about scope — one condition or the whole pet — make the carrier state it in writing; and appeal with a vet-written relatedness letter, which veterinary staff report succeeding routinely when diagnoses are coded consistently.

One thing we will not tell you: to delay a vet visit so nothing lands in the record. Records affect coverage — that's real — but a chart note costs you a clause fight; a missed diagnosis can cost your pet. Get the care, keep copies of everything, and pick the carrier whose lookback you can live with.

Renewal hikes: what the regulator record shows

Expect pet insurance premiums to rise at renewal — with age, with local vet costs, and sometimes far faster than either. This isn't anecdote; it's on file with state regulators, and it's the single best-documented consumer harm in the category.

California's Department of Insurance approved Trupanion increases of +12% (2023), +29% (2024), and a +33% average for 2025 across 97,153 policies — roughly +92% of stacked base-rate growth in about 25 months, every step approved. It approved a 45% Pets Best increase effective April 2, 2025, on about 64,770 policies — with the insurer itself projecting 12,700+ cancellations. For scale: veterinary-services inflation ran about 6.5% in 2025.

And when a carrier doesn't re-price, it can retreat: Nationwide non-renewed roughly 100,000 pet policies from mid-2024, and the resulting class action — still pending, allegations only — quotes the company's own FAQ promising never to drop a pet for age. The community's renewal stories track the filings almost exactly: the +40%-at-first-renewal threads aren't outliers; they're the approved rate structure, experienced one mailbox at a time. California's SB 1217 now requires insurers to disclose whether premiums rise with age — ask that question in any state, before you buy.

Every clause in this section comes from the policy forms we track in our fine-print index, carrier by carrier — when a capsule above says "read the policy language," that's where it lives.

What Reddit actually says (dated and screened for astroturf)

Shoppers append "reddit" to pet insurance searches for one reason: editorial review pages read like ads, and owners want to know what people who actually filed claims experienced. The instinct is right. The execution needs care — because the community's own space has been partially captured by the same affiliate economics it exists to escape.

Here's the finding no ranking page prints. The original hub, r/petinsurance, is gone. Its successor — the roughly 29,000-member subreddit that Google ranks on page one for this exact keyword — was the subject of an August 2025 community investigation alleging it is partially operated as an affiliate funnel by its own moderators: seeded "what's the best insurance?" posts answered with links to commercial sites, and manufactured "best according to Reddit" threads built to intercept exactly the search you may have just made. We saw the residue in our own July 2026 capture — a product plug here, a bare carrier-URL "recommendation" there, both reading as seeded. Quora's pet insurance feed showed the same monetization pattern when we reviewed it the same week.

So we screen before we cite. Every community claim on this page comes from a thread we read in full, carries its date, drops anything that pattern-matches to seeding, and is treated as sentiment — never as statistics. Unhappy owners write more than happy ones; that's the medium. What survives the screen is genuinely valuable, and it clusters into three durable themes:

- Verdicts split by pet, not by carrier quality. The community's Trupanion argument — five-figure payouts praised in one thread, deductible mechanics resented in the next — isn't noise; it's the accurate shape of the product. Our capsules keep those splits intact instead of averaging them away.

- Renewal stories that match the filings. The +40%-at-renewal threads corroborate, almost number for number, the CDI-approved increases in the fine-print section. When anecdote and regulator record agree, believe both.

- A method, not a carrier. The veterans' checklist repeats across threads: read the policy before the reviews, get a baseline exam at enrollment, don't buy limits under $10k, and understand your deductible structure before the first claim, not after.

The purest artifact of that third theme is a March 2025 post that became community canon: an owner who read the fine print of 16 companies and published the spreadsheet, with the takeaway that you should always read the policy documents yourself. That is the community's answer to review-site distrust — do the primary reading. It's also, not coincidentally, this page's entire method: the same reading, done as a full-time job, with the receipts and the dates shown.

One standing request: if a thread you trust contradicts a capsule above, check the dates first — carrier terms and scores drift, and a 2024 thread can be honestly wrong about a 2026 policy. If the dates hold, we want to know about it.

Frequently Asked Questions

If I switch pet insurers, does everything become pre-existing?

Mostly, yes — that's the switching trap. Anything in your pet's medical record before the new policy starts falls under the new carrier's pre-existing lookback, and every waiting period resets. The exceptions are narrow: AKC's plans can cover even incurable pre-existing conditions after 365 days of continuous coverage, and cure-window carriers re-cover conditions that stay symptom-free long enough. If your pet has a medical history, price the exclusions — not just the premium — before you leave, and never cancel the old policy until the new waiting periods have passed.

Can I still get pet insurance for a senior dog or cat?

Usually you can buy a policy — whether it's worth it depends on what it excludes. Several major carriers cap new enrollment around the early-to-mid teens, while Spot has no upper age limit at all. But buying a policy and covering your pet's existing conditions are two different things: nothing already in the chart comes with you, and senior-age premiums are substantial. For an older pet, compare the enrollment caps in our capsules above, and run the break-even math before assuming either answer.

Does any pet insurance pay the vet directly?

Two carriers meaningfully do. Trupanion can pay participating clinics directly at checkout, so you only cover your share — the feature its reputation is built on. Pets Best can pay your vet after a claim is approved, using a signed release form. Most others work on reimbursement — you pay the full bill, file, and wait — though a few carriers will pay a clinic directly case by case, so ask both your carrier and your vet. If cash flow at the emergency vet is your worry, that difference matters more than a half-star of rating.

Do I have to use a specific vet with pet insurance?

No. U.S. pet insurance is reimbursement-based, not a network product like human health insurance — any licensed veterinarian counts, including emergency hospitals and specialists. The bill gets reimbursed under your policy's terms no matter whose clinic issued it. What varies by carrier is how fast that reimbursement arrives and whether direct payment is possible at all (see the previous answer).

Do pet insurance companies profit by denying claims?

Not the way the fear suggests. Insurers price premiums above expected claims — that's the business — and denials cluster in defined clauses: pre-existing exclusions, waiting periods, and benefit limits, which is why reading the policy protects you better than reading star ratings. Worth knowing: no public per-carrier denial rate exists — insurers' market-conduct filings collect denials by reason, but company-level data is confidential. Any site quoting a specific denial percentage is quoting something that cannot be sourced.

What happened to ManyPets, Nationwide, and other brands I've seen reviewed?

The roster moved — which is exactly why undated reviews mislead. ManyPets left the U.S. market, with renewals handled by Odie since January 1, 2025. Nationwide non-renewed roughly 100,000 pet policies starting mid-2024. Companion Protect no longer sells directly to consumers. Nationwide, to be clear, still sells pet policies — it shrank its book, which is a different fact. If a review site hasn't caught any of this, check its dates before trusting anything else on the page.

Is Chewy CarePlus the same as Trupanion or Lemonade?

Related, not identical. CarePlus is Chewy's marketplace brand, underwritten by Trupanion's insurer or Lemonade depending on your location — but the plan terms are not carbon copies of those carriers' direct products, and owners report differences in deductible structure and exam-fee handling. Treat it as its own policy: read the CarePlus documents, not the underwriter's reviews, before buying.

What's a good NAIC complaint index score for a pet insurer?

Below 1.0 — that means the company drew fewer complaints than expected for its premium volume; above 1.0 means more. Two cautions before you compare: the index is calculated per legal underwriting entity and line of business, so for brands on multi-line underwriters it blends pet with auto and home; and values change yearly, so note the date you looked. Look any carrier up in about a minute via the NAIC's Consumer Insurance Search using the underwriter from our ownership map.

Why is my new-policy quote so much cheaper than the renewal stories on this page?

Because you're seeing the entry price, and renewals are where pet insurance gets expensive. Premiums recalibrate upward with your pet's age and local veterinary costs — and regulator-approved single-year increases of 25–45% have hit some carriers' renewal books, far above vet-cost inflation. That's why our scores weight renewal behavior at a quarter of the total: the carrier that's cheapest at signup and the carrier that's livable at year five are often different companies.

Sources

- American Pet Insurance Company — FSR A′ (A Prime) — Demotech

- Lemonade Insurance Company — FSR A (Exceptional) — Demotech

- AM Best Affirms Credit Ratings of Munich Re and Its Subsidiaries (American Modern) — Business Wire

- Crum & Forster Upgraded to A+ (Superior) Financial Strength Rating by AM Best — PR Newswire

- AM Best Removes From Under Review, Affirms Independence American Insurance Co. — Insurance Journal

- AM Best Affirms Credit Ratings of AXA XL's Subsidiaries — AM Best

- AM Best Affirms Credit Ratings of Chubb Limited and Its Subsidiaries — AM Best

- AM Best Affirms Credit Ratings of Nationwide Mutual Insurance Company — AM Best (press release PDF)

- AM Best Affirms Credit Ratings of Markel Group Inc. and Its Subsidiaries — Business Wire

- Prudent Pet — Underwriting Disclosure — Prudent Pet

- Trupanion policyholders face 33% rate hike for pet insurance in California — Insurify (WFMZ syndication)

- 45% rate hike on the way for Pets Best policyholders in California — Insurify (WFMZ syndication)

- Nationwide to drop about 100,000 pet insurance policies — CBS News

- Kreidler orders two pet insurers to repay $4.7 million to consumers — Washington State OIC (Wayback capture)

- Pet Insurance Company category ratings — Trustpilot

- Odie Pet Insurance Marketing, Inc. — Complaints — Better Business Bureau

- Odie — Licensing Disclosures — Odie Pet Insurance

- I've had it with Trupanion — cancelling (r/petinsurancereviews) — Reddit

- My experience with Spot so far (r/petinsurancereviews) — Reddit

- Are there any good pet insurance companies left? (r/petinsurancereviews) — Reddit

- Pet insurance increased by 40% (r/Pets) — Reddit

- Lemonade pet claim denial dispute (r/Insurance) — Reddit

- MetLife price increase & switching carriers? (r/petinsurancereviews) — Reddit

- Why I chose Fetch — top comment warnings (r/petinsurancereviews) — Reddit

- Best pet insurance, for dogs specifically? (r/petinsurancereviews) — Reddit

- Insurance denying claims — how do I appeal? (r/Frenchbulldogs) — Reddit

- Vet bill scared me into getting pet insurance (r/petinsurancereviews) — Reddit

- Overwhelmed with picking the BEST (r/petinsurancereviews) — Reddit

- NAIC Pet Insurance Model Act (Model #633) — NAIC

- How to file a complaint and research complaints against insurance carriers — NAIC

- Pet Insurance Questions and Answers — California Department of Insurance

- 16 CFR Part 465 — Rule on the Use of Consumer Reviews and Testimonials — eCFR / Federal Trade Commission

- Consumer Reviews and Testimonials Rule: Questions and Answers — Federal Trade Commission

- Veterinarian services price inflation (BLS CPI series) — BLS CPI aggregation (in2013dollars)

- Doubtless Pet Care Launches to Provide Peace of Mind to Pet Parents — Business Wire

- JAB acquires majority stake in Pumpkin Insurance Services — Business Wire

- IPH Enters Strategic Partnership with Synchrony and Completes Acquisition of Pets Best — PR Newswire

- Independence Pet Holdings Acquires Spot Pet Insurance — Business Wire

- AM Best Places Credit Ratings of Independence American Insurance Company Under Review — Business Wire

- ManyPets exits US market to focus on UK operations — InsurTech Insights

- Embrace Pet Insurance — Underwriting — Embrace Pet Insurance

- Healthy Paws — Legal / Underwriting — Healthy Paws

- Chewy CarePlus Pet Insurance Review — NerdWallet

- Consumer Insurance Search — NAIC

- Market Conduct Annual Statement — 2024 (pet insurance line) — NAIC

- MCAS Instructions — Pet insurance, 2024 data year — NAIC

- MCAS Data Dashboard — NAIC

- Pet Insurers Doing Business in California — California Department of Insurance

- Washington Fines Petcube, Orders It to Stop Marketing Unauthorized Pet Insurance — Insurance Journal

- Best Pet Insurance Companies Of 2026 — Forbes Advisor

- Best Pet Insurance Companies — MoneyGeek

- Best Pet Insurance Companies of 2026 — U.S. News & World Report

- Best Pet Insurance Companies for 2026 — NerdWallet

- Pet Insurance Review — ratings hub — PetInsuranceReview.com

- Pet Insurance Gurus — best pet insurance rankings — PetInsuranceGurus.com

- Best Pet Insurance Companies (member survey, Dec 2024–Jan 2025) — Consumer Reports

- Best Pet Insurance — comparison guide — Pawlicy Advisor

- Trupanion Pet Insurance Review — U.S. News & World Report

- Pet Insurance for Pre-Existing Conditions — NerdWallet

- Embrace Pet Insurance — Waiting Periods — Embrace Pet Insurance

- Benanav v. Healthy Paws Pet Insurance LLC — docket — CourtListener

- Healthy Paws Pet Insurance — consumer reviews — ConsumerAffairs

- Wanting a vet's honest opinion about pet insurance (r/AskVet) — Reddit

- Pet Owner Cost Survey (January 2026, n=1,500) — U.S. News & World Report

- California Insurance Code §12880.7 (SB 1217 disclosures and waiting-period limits) — Justia

- Silberman et al. v. Nationwide Mutual Insurance Company — complaint — ClassAction.org

- r/petinsurancereviews run as affiliate spam ring by its own mods — investigation (r/TheseFuckingAccounts) — Reddit

- I read the fine print of 16 companies and made a spreadsheet (r/petinsurancereviews) — Reddit

- Best Age to Get Pet Insurance: When to Enroll Your Dog or Cat — Spot Pet Insurance

- Pet Insurance Plans and FAQs — Figo Pet Insurance

- Does Fetch Pet Insurance cover exam fees? — Fetch Pet Insurance

- Pre-Existing Conditions Coverage for Pets — AKC Pet Insurance

- Trupanion Comments on Rate Filing Approval in California — GlobeNewswire (Trupanion release)