Here's the honest answer up front: Nationwide is a large, financially strong, long-established pet insurer with unusually broad coverage — but whether it's worth it in 2026 depends almost entirely on which plan you buy and on whether you still trust the company after it canceled a large block of existing policies.

Nationwide has been doing this longer than anyone. It issued the first pet insurance policy in the United States, back in 1982, it remains one of the biggest carriers on the shelf, and it's one of the very few that will insure a bird, a reptile, or a rabbit. That pedigree is real. It's also not the same thing as being right for your pet.

Two things trip up almost every Nationwide shopper, and most reviews skate past both.

The first is how Nationwide actually pays you back. Most of its plans reimburse a percentage of your real vet bill; one pays on a fixed benefit schedule — a set dollar cap per condition, no matter what your vet charges. Buy the wrong one and a covered surgery can still leave you thousands short.

The second is the 2024–2025 cancellations: Nationwide moved to non-renew roughly 100,000 policies and got sued over it. We'll tell that story straight — what happened, and, just as important, what a policy bought today actually gets you.

We've read the plan documents, the benefit schedules, and the court filing so you don't have to. Here's the verdict, decoded — plan by plan.

Table of Contents

- The Verdict: Who Nationwide Is (and Isn't) For

- Nationwide's Plans, Decoded

- Benefit Schedule vs. Percentage of the Bill

- What Happened in 2024–2025: The Non-Renewals & the Lawsuit

- Coverage, Exclusions & Waiting Periods

- What Nationwide Pet Insurance Costs

- Exotic & Avian Coverage

- Financial Strength & Complaint Record

- What Real Owners Say (Reddit & Yelp)

- Nationwide vs. the Alternatives

- If You Were Non-Renewed: What to Do Next

- Frequently Asked Questions

- Sources

The Verdict: Who Nationwide Is (and Isn't) For

Nationwide is a legitimately strong carrier that's a poor fit for a real slice of the people who search for it. There's no blanket "good" or "bad" here — the right call depends on which pet you have and, above all, which plan you'd actually buy.

Nationwide makes sense if you:

- want a large, financially stable insurer — its underwriters carry an AM Best "A" (Excellent) financial-strength rating, so the company standing behind your claim isn't going anywhere;

- have an exotic pet — a bird, reptile, rabbit, or ferret — because Nationwide is one of the very few U.S. carriers that will insure it at all;

- want routine-care (wellness) coverage bundled in, and you've read the fine print on how your specific plan reimburses.

Look harder elsewhere if you:

- have a senior pet — new illness coverage is sold only to dogs and cats 8 and under (9 for the Major Medical plan), so older pets have far fewer options;

- would be blindsided by a benefit-schedule plan that caps each payout at a fixed dollar amount no matter what your vet charges — one Nationwide plan works exactly this way, and we decode it next;

- need certainty your policy will renew at a predictable price, because the 2024–2025 cancellations shook a lot of long-time customers, and that trust question is a fair one to sit with.

The rest of this review earns that verdict rather than asserting it: how each plan actually pays, what the cancellations did and didn't mean, and what a policy bought today gets you. The two sections that follow are where most Nationwide regret starts — read them before you decide.

Nationwide's Plans, Decoded

"Nationwide pet insurance" isn't one product — it's a small family of plans that cover and, crucially, pay very differently. Buying the wrong one is the most common Nationwide mistake, so here's the current lineup in plain terms.

| Plan | How it reimburses | Reimbursement | Annual deductible | Annual limit |

|---|---|---|---|---|

| Whole Pet | % of your actual vet bill | 50% or 70% | $250 | $10,000 |

| Modular | % of your actual vet bill | 50%–80% | $100–$1,000 | up to $5,000 per category |

| Major Medical | Benefit schedule — a fixed cap per condition | set dollar amount per condition | $250 | per-condition caps |

| My Pet Protection Choice | % of your actual vet bill | 50%–80% | $250 | $5,000 per category |

Terms per Nationwide's own plan pages; the exact options you're offered vary by state and pet.

Two things to notice. First, three of the four plans pay you back a percentage of what you actually spent — the model most people picture when they think "pet insurance." Major Medical is the exception. It pays a fixed dollar allowance per condition, and that single difference is where the biggest payout surprises live — so it gets its own section next.

Second, My Pet Protection Choice is largely an employer or association benefit rather than an off-the-street retail plan; existing members typically can only enroll or switch into it at renewal. If you want routine-care coverage, check whether it's a separate wellness add-on rather than part of the core medical plan — that changes the price you're actually comparing. And whichever plan you're quoted, confirm the reimbursement basis, the deductible, and the annual cap in writing before you sign: those three numbers, not the brand name, decide what you actually get back.

Benefit Schedule vs. Percentage of the Bill

This is the fine print that decides whether a covered surgery leaves you roughly whole or thousands short — and it's the single thing most Nationwide reviews skip. A Nationwide plan can pay you back in two completely different ways, and they are not interchangeable.

A percentage of the actual bill. Whole Pet, Modular, and My Pet Protection Choice work the way most people expect: after your deductible, they reimburse a set percentage of what you actually paid — 50% to 80%, depending on the plan and the level you choose. Bigger bill, bigger check.

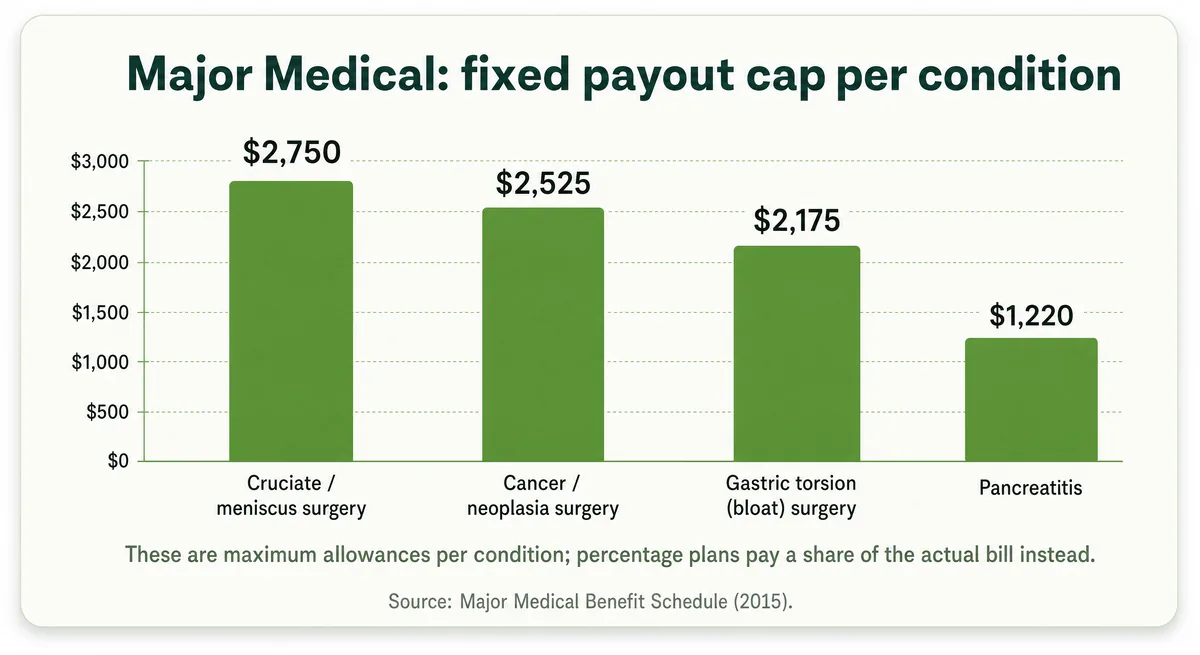

A benefit schedule. The Major Medical plan is the exception. It pays on a benefit schedule — a list of fixed dollar caps, one per condition. Whatever your vet charges, the plan pays up to that condition's set allowance and not a dollar more.

Here's why that gap matters. On Nationwide's own Major Medical benefit schedule, cruciate (knee) surgery is capped at $2,750. A string of other big-ticket conditions — cancer surgeries, a kidney transplant, cataract surgery — top out at $2,525 each; bloat surgery at $2,175.

Say your dog tears a cruciate ligament and the repair runs $5,000 (a common four-figure surgery). On a percentage plan reimbursing 80%, you'd get back roughly ($5,000 − $250 deductible) × 80% = $3,800. On Major Medical, the cruciate benefit is capped at $2,750 regardless of the bill — so you'd receive up to about that and cover the remaining ~$2,000-plus yourself.

One caveat worth stating plainly: the sample schedule those figures come from is a 2015-dated form (version VS-G-3-a). Vet prices have risen sharply since then, so if anything those fixed caps understate today's gap — always confirm the current schedule for your state before you buy. The takeaway: on a benefit-schedule plan, the number that decides your payout isn't your reimbursement percentage — it's the cap for the exact condition your pet happens to develop, which you can't predict in advance.

What Happened in 2024–2025: The Non-Renewals & the Lawsuit

If you've seen the angry threads, here's the sober version. In June 2024, Nationwide announced it would non-renew about 100,000 pet insurance policies — its own figure — with cancellations rolling out through the summer of 2025. It was the largest move of its kind by the country's oldest pet insurer, and it's the reason a lot of long-time customers now distrust the brand.

The cuts centered on a comprehensive legacy plan, Whole Pet with Wellness. Nationwide's stated reason was cost: "inflation in the cost of veterinary care and other factors," it said, forced "underwriting changes and the withdrawal of some products in some states." It also said the non-renewals had "no association with age, breed or prior claims," and that it would honor coverage through the end of each customer's current term.

Affected owners saw it differently, and it's now in court. In June 2025, three Massachusetts policyholders filed a class action — Silberman v. Nationwide (U.S. District Court, District of Massachusetts, No. 1:25-cv-11619). The complaint alleges Nationwide marketed a promise never to drop a pet because of age, then cancelled anyway; it pleads that roughly 100,000 to 300,000 Whole Pet with Wellness policies were cancelled over about a year. That wider range is the plaintiffs' allegation, not an established count — the ~100,000 figure is Nationwide's own.

Two honest caveats before you write Nationwide off. First, this was the withdrawal of specific legacy products, not the company leaving pet insurance — it still sells new policies today. Second, the plans a new customer buys now are the ones covered above, not the discontinued Whole Pet with Wellness. What the episode fairly costs Nationwide is trust: buy today, and you're betting the plan you pick won't be the next one repriced or retired. That's a reasonable worry — and it's the biggest reason to weigh Nationwide against a carrier with a steadier renewal track record, which is what the rest of this review is here to help you do.

Coverage, Exclusions & Waiting Periods

Nationwide's core coverage is broad — accidents, illnesses, surgery, diagnostics — but a handful of fine-print rules decide whether a specific claim gets paid. These are the ones worth knowing before you buy.

The cruciate trap. Nationwide won't cover a torn cruciate (knee) ligament in the first 12 months of a policy — a full year, where many insurers use 14 days to six months. On the Modular plan, cruciate coverage is an optional rider you can only add after your first year. If knee trouble is a real risk for your dog, that timeline matters.

Other waiting periods are more standard: 14 days for accidents and illnesses, 90 days for spay/neuter and dental. In a number of states — California, Florida, and Washington among them — Nationwide shortens these waits, dropping the accident wait to zero and the cruciate wait to 30 days.

Pre-existing conditions aren't covered on any Nationwide plan, which is the industry norm. Keep two different questions separate here: can you buy a policy? (almost always yes) and will this condition be covered? If a symptom is already in your pet's records, that condition is excluded even though the policy still sells. Nationwide does allow a "curable" exception — a condition that's stayed symptom-free and treatment-free for at least six months can become eligible again. For the full mechanics, see our guide to pre-existing conditions.

A few more to weigh: hereditary conditions are only limitedly covered, and only on the Major Medical plan; and Nationwide's reimbursement tops out at 80% in most states, a notch below the 90% several rivals offer. One genuine point in Nationwide's favor: it covers the vet exam fee on covered visits, which some competitors exclude. And recall the age gate — new illness coverage stops at age 8 (age 9 on Major Medical), so the earlier you enroll, the more options you keep.

What Nationwide Pet Insurance Costs

The first thing to know about Nationwide's pricing is that there isn't a published price. Nationwide's own site lists no premiums — it routes you to a quote tool or a phone number — so any "starts at $X" figure you see elsewhere is a third-party quote, not an official rate.

To give you a feel, one sample quote set from NerdWallet — a 2-year-old pet in Katy, Texas with a $250 deductible, $5,000 annual limit, and 80% reimbursement — came back roughly like this per month:

- Mixed-breed dog: about $43

- Golden Retriever or German Shepherd: about $50–$51

- French Bulldog: about $82

- Cats: from about $19

Those are illustrations, not your quote — real premiums swing hard with breed, age, and ZIP code. Age changes the picture too: by around age 8, new coverage is often accident-only, which looks cheap (roughly $18–$23/month for dogs) but leaves out illness entirely.

To judge whatever number you're quoted, anchor it to the market. Across all U.S. carriers, NAPHIA's 2024 data puts the average accident-and-illness premium near $62/month for dogs and $32/month for cats. If a Nationwide quote lands well above that, it's the plan design (limits, deductible, reimbursement rate) and your pet's profile driving it — so ask what changes when you adjust those dials before you decide it's too expensive.

Exotic & Avian Coverage

This is Nationwide's genuine standout. If your pet is a bird, reptile, rabbit, ferret, or other small mammal, Nationwide is one of the very few U.S. insurers that will cover it at all — a niche most carriers simply won't touch.

The Avian & Exotic plan reimburses 50% or 70% of eligible vet bills, with one $250 annual deductible (not per incident) and a $7,500 annual limit. Eligible animals run a long list — birds, rabbits, ferrets, guinea pigs, chinchillas, hamsters, rats, and many reptiles and amphibians. It won't cover venomous or endangered species, animals that need a state or federal permit, or flock birds like chickens and pigeons.

One correction to a claim you'll still see repeated: Nationwide is no longer the only U.S. insurer here. As of 2026, MetLife also covers exotic pets across multiple species — though its exotic coverage is limited to a set of states. So Nationwide is one of very few, not the sole option. For an exotic-pet owner, "very few" is still reason enough to give it a serious look.

Financial Strength & Complaint Record

On the one question a balance sheet answers — can Nationwide pay the claims it owes? — the answer is a clear yes. It's one of the financially strongest carriers in the category. The concern we keep flagging in this review isn't solvency; it's renewal and coverage risk.

The ratings bear that out. In November 2025, AM Best affirmed Nationwide's property-casualty group at Financial Strength Rating A (Excellent), an "a+" issuer credit rating, and a stable outlook — that's an FSR of A and an ICR of a+, not an "A+" grade. Nationwide's disclosures add S&P at A+ and Moody's at A2, and pet underwriter National Casualty holds AM Best's top Financial Size Category XV (surplus of $2 billion or more).

Who underwrites your policy matters — it's the entity you'd name in a state complaint. Per Nationwide's underwriting disclosure, pet policies are written by Veterinary Pet Insurance Company in California (NAIC 42285) and by National Casualty Company in every other state (NAIC 11991), both Nationwide Mutual subsidiaries. Those codes unlock each one's public record.

For complaints, skip the star-rating aggregators and go to the regulator. The NAIC now publishes a pet-specific scorecard tracking complaints per 1,000 policies, non-renewals, and claims closed without payment, and you can look up National Casualty by code in the NAIC Consumer Information Source. We won't quote a complaint number here — it moves, so read it live. One caveat on the "A+ from the BBB" line: that BBB profile is company-wide, not pet-specific. The takeaway: this is a financially sound insurer, so the real question isn't whether it can pay — it's whether the plan you buy stays as sold, which is what the rest of this review weighs (and how we assess a carrier).

What Real Owners Say (Reddit & Yelp)

Read the forums today and the mood is clearly negative — but read closely and it's a specific kind of negative. Treat everything here as sentiment, not verified fact: venting posts and non-renewal anger dominate these threads, while quietly satisfied owners rarely bother to write in. With that selection bias flagged, here's the honest consensus.

The anger is real, and it's about repricing — not claim denials. On r/petinsurancereviews, one owner's cat premium jumped from about $600 to $1,450 a year after their plan was discontinued; another reported a healthy 6-year-old pug going from $39.80 to $128.11 a month — more than triple — with no warning. The recurring grievance isn't "Nationwide won't pay a claim." It's "Nationwide dropped or repriced the plan I'd relied on for years." The same theme runs heavy on Nationwide's Yelp listing, where the reviews skew hard toward cancellation and claims complaints.

The counterweight is just as real. Owners who got in early — say a 90% / $7,500 plan — report genuine value, with Nationwide reimbursing broad, vet-recommended care: supplements, Adequan, prescription food, physical therapy. The common historical refrain is that Nationwide paid well. So the trust problem is about what happens at renewal, not how a routine claim gets handled.

Many "scam" complaints are really coverage-tier confusion. The loudest "complete scam" posts often turn out to be someone who bought an accident-only or wellness plan, then had an illness or ER claim denied — and the crowd itself corrects them: read the policy, wellness isn't illness coverage. On Quora, a self-described 40-year agency owner uses a $303-reimbursed-on-$1,000-in-premiums story to indict the whole category, not Nationwide specifically. That low-reimbursement feeling usually traces to the deductible, coinsurance, and per-condition caps we decoded earlier — not to a rigged game.

Our read: the net sentiment is a trust reset triggered by the 2024–2025 cancellations. Weigh it as exactly that — a fair warning about renewal risk, not evidence that Nationwide mishandles the claims it agrees to pay.

Nationwide vs. the Alternatives

If you're cross-shopping, the carrier Nationwide is most often measured against is Trupanion — and the difference that matters isn't the sticker price, it's the plumbing: how each one reimburses, and how its deductible works.

| Nationwide | Trupanion | |

|---|---|---|

| Reimburses | A percentage of the bill — or a fixed benefit schedule on Major Medical | A percentage of the actual bill (no benefit schedule) |

| Deductible | Annual — resets every policy year | Per condition, for the pet's lifetime — paid once per condition |

| Reputation | Broad coverage (incl. exotics); recent renewal-trust hit | Owner-praised for fast, rarely-denied payouts; usually pricier |

That deductible contrast is the one owners on Quora say finally made it click: most carriers, Nationwide included, charge an annual deductible, while Trupanion charges a per-condition lifetime deductible — better if your pet develops one expensive chronic condition, worse if it racks up many small unrelated ones. Tellingly, a self-described Nationwide agent in that same thread said he picked Trupanion for his own dog for exactly that reason (labeled sentiment, not a verdict).

Trupanion also recurs as the Reddit and Quora favorite for paying claims quickly and rarely denying them — but expect to pay more for it. This is deliberately a short compare; for a fuller head-to-head across carriers, see our comparison hub.

If You Were Non-Renewed: What to Do Next

If Nationwide non-renewed or repriced you, the single most important move is to act quickly and avoid a gap in coverage. Any condition already in your pet's records can be treated as pre-existing by a new carrier, gap or no gap — but a lapse only makes things worse, and some insurers will consider honoring your prior coverage only if there's no break. So line up the new policy before the old one ends, rather than cancelling first and shopping later. And keep taking your pet to the vet through the switch; the goal is continuous coverage, never skipped care.

Keep two questions separate, because the gap between them is what trips people up: can you buy a new policy? (almost always yes) and will your pet's existing condition be covered? (often no). No honest source can promise a specific pre-existing condition will be covered — so treat every carrier's pre-existing rules as something to confirm in writing for your pet's exact history.

With that caveat, dropped owners on Reddit consistently point to a few options worth pricing:

- MetLife — a carrier dropped owners commonly move to; ask directly whether it will honor your prior continuous coverage, and get the answer in writing before you switch.

- AKC (PetPartners) — the community go-to for enrolling seniors or pets other insurers turn away.

- Trupanion — prices on your pet's age at enrollment and holds that basis, so the earlier you switch, the better it ages.

You're not stuck. Shop the carriers that fit your situation, read each one's pre-existing definition closely, and buy before the current policy lapses.

Frequently Asked Questions

Is Nationwide a good insurance company for pets?

It's a strong choice for some owners and a cautious one for others. Nationwide is financially solid — AM Best rates it A, with an “a+” issuer credit rating — and offers unusually broad coverage, including exotics and vet exam fees. Be more careful if you need certainty your plan won't be repriced or dropped at renewal, would be caught off guard by the Major Medical benefit schedule, or have a senior pet (new illness enrollment stops at age 8, age 9 on Major Medical).

Do all vets accept Nationwide Pet Insurance?

Effectively yes — you can use any licensed veterinarian in the U.S. Nationwide isn't a network plan: you pay your vet directly and Nationwide reimburses you afterward, so there's no list of “accepted” clinics to check. That also means your regular vet, a specialist, or an emergency hospital all work the same way — the only question is whether the specific treatment is covered by your plan.

Why did Nationwide cancel pet insurance?

In June 2024, Nationwide announced it would non-renew about 100,000 pet policies, concentrated on its legacy Whole Pet with Wellness plan, citing rising veterinary costs. Importantly, it did not leave pet insurance — it still sells new policies today. Affected owners dispute the company's “no association with age” framing in a class-action suit, Silberman v. Nationwide, which alleges the cancellations fell hardest on older and chronically ill pets.

What is the most reputable pet insurance?

There's no single “most reputable” insurer — it depends on what you weigh most. For fast, rarely-denied payouts, owners on Reddit and Quora repeatedly name Trupanion; for enrolling seniors or pets with prior conditions, AKC comes up most often; Nationwide remains one of the most financially secure and offers the widest species coverage. A genuinely reputable carrier is financially sound, transparent about its exclusions, and consistent at renewal — judge any name against those three things, not a star score alone.

What's the difference between accident-only, illness, and wellness coverage?

They cover different things, and mixing them up is the most common avoidable complaint about Nationwide. Accident-only pays for injuries — broken bones, swallowed objects, bite wounds. Illness coverage adds sicknesses like cancer, infections, and chronic disease. Wellness (or routine) coverage handles preventive care — exams, vaccines, dental cleanings. An accident-only plan won't pay illness claims (though it covers emergencies caused by a covered accident), and a wellness plan won't pay illness or injury claims — so confirm exactly which tier you're buying before a claim proves it the hard way.

Does Nationwide cover pre-existing conditions?

No — like nearly every U.S. pet insurer, Nationwide excludes pre-existing conditions on all of its plans. There is one opening: a condition that has been cured and stayed symptom-free and treatment-free for at least six months may become eligible again. Keep two questions separate — you can almost always buy a policy, but whether a condition already in your pet's records will be covered is a different matter, and often the answer is no.

Is Nationwide pet insurance worth it?

It can be — but be honest about the math: in most years you'll pay more in premiums than you get back, because insurance buys protection against a rare four- or five-figure bill, not a routine rebate. Whether Nationwide specifically is worth it comes down to which plan you pick — a percentage-of-the-bill plan or the fixed benefit schedule — and how much renewal risk you can stomach after the 2024–2025 cancellations. For an exotic pet, its rare species coverage tilts the answer toward yes.

Sources

- Nationwide Celebrates 40 Years of Pet Insurance History — Nationwide

- Nationwide dropping about 100,000 pet insurance policies — CBS News

- AM Best Affirms Credit Ratings of Nationwide Mutual Insurance Company and Its Key Operating Subsidiaries — AM Best

- Nationwide Pet Insurance Overview for 2026 — U.S. News & World Report

- Nationwide Pet Insurance — All Products — Nationwide

- Nationwide Pet Insurance Review 2026: Pros and Cons — NerdWallet

- Nationwide Major Medical Plan Benefit Schedule (form VS-G-3-a, 2015) — Nationwide

- Silberman et al. v. Nationwide Mutual Insurance Company et al. — Class Action Complaint (D. Mass., No. 1:25-cv-11619) — ClassAction.org

- Nationwide Pet Insurance — Plan Restrictions — Nationwide

- Nationwide Pet Insurance — What's Not Covered — Nationwide

- Nationwide Pet Health Insurance — Nationwide

- Average Premiums (industry data) — NAPHIA

- Nationwide Avian & Exotic Pet Plan (official flyer) — Nationwide

- Exotic Pet Insurance: Cost & Coverage — MoneyGeek

- Nationwide Company Ratings (AM Best, S&P, Moody's) — Nationwide

- National Casualty Company — AM Best Rating Disclosure (FSC XV) — AM Best

- Who Underwrites Nationwide Pet Insurance — Nationwide

- Veterinary Pet Insurance Company — Company Profile (NAIC 42285) — California Department of Insurance

- National Casualty Company — Company Profile (NAIC 11991) — California Department of Insurance

- Pet Insurance MCAS Scorecard Ratios — NAIC

- Consumer Information Source (company complaint lookup) — NAIC

- Nationwide — BBB Business Profile & Complaints — Better Business Bureau

- Nationwide Review (owner report, r/petinsurancereviews) — Reddit

- Nationwide Major price increase (owner report) — Reddit

- Nationwide plan discontinued / repriced (owner report) — Reddit

- 'Nationwide is a complete scam' thread (tier-confusion correction) — Reddit

- Does Nationwide dropping policies foreshadow a trend? (category-skepticism) — Quora

- Figo or Nationwide? — Nationwide agent's deductible decode & Trupanion pick — Quora

- Best/most economical pet insurance — Trupanion pays quickly, rarely denies — Quora

- Need new policy — Nationwide ending my policy, switching & pre-existing risk — Reddit

- Nationwide Pet Insurance FAQ (any licensed vet) — Nationwide

- Nationwide Pet Insurance — Yelp reviews — Yelp