Trupanion is a premium-priced U.S. pet insurer built around one unusual idea: a per-condition, lifetime deductible you pay once per illness or injury — not every year — paired with a flat 90% reimbursement and no payout caps, plus the option to pay your vet directly at checkout. Our short verdict: it's worth the higher price for some pets and overpriced for others.

That "once per condition" deductible is the whole ballgame, and it's the part most reviews gloss over. For a pet that develops a chronic, lifelong condition, meeting the deductible a single time can save you thousands. For a healthy pet with a string of unrelated one-off problems, an ordinary annual deductible can work out cheaper.

So it tends to fit owners of chronic-illness-prone or large, predisposed breeds, anyone who wants uncapped coverage without fronting a five-figure bill, and people enrolling a young, healthy pet before problems become "pre-existing." It's a weaker fit for budget shoppers, low-risk pets, and anyone who wants routine-care or exam-fee coverage — Trupanion covers neither.

We're a licensed agency, not a review farm, and we've read Trupanion's policy so you don't have to. Below: what it really costs, what the fine print excludes, and whether it's right for your pet. Here's how we review.

Table of Contents

- Our Verdict at a Glance

- How the Per-Condition Deductible Works

- What Trupanion Really Costs (and Why Premiums Rise)

- Coverage, Reimbursement & VetDirect Pay

- What Trupanion Doesn't Cover

- Is Trupanion Legit? Financial Strength & Complaints

- Trupanion vs. Lemonade

- What Real Owners Say

- Who Should (and Shouldn't) Choose Trupanion

- Frequently Asked Questions

- Sources

Our Verdict at a Glance

We rate Trupanion 3.8 out of 5. It's one of the most complete pet insurance policies you can buy — and one of the most expensive. Whether that trade is worth it comes down to your pet's health risk and your budget, not a one-size verdict. Our rating rewards the uncapped coverage and direct-to-vet payment, and marks it down for the price and the fine print (see how we review).

Pros

- No annual, per-incident, or lifetime payout caps, with a flat 90% reimbursement.

- A per-condition deductible that can save thousands on a chronic, lifelong illness — you pay it once, not every year.

- At participating clinics, VetDirect Pay can settle approved charges with your vet at checkout, so you don't front a five-figure bill and wait for a refund.

- Covers hereditary and congenital conditions and reimburses your actual vet bill, not a capped fee schedule.

Cons

- Among the highest sample premiums of any major carrier.

- Cohort-based renewal increases can be steep — double-digit, and sometimes far more.

- No wellness plan and no coverage for exam fees or routine care.

- That per-condition deductible works against you if your pet has many small, unrelated problems.

Best for: owners of chronic-illness-prone or large, predisposed breeds who enroll before any symptoms appear; anyone who wants uncapped catastrophic protection; and owners who couldn't easily float a five-figure emergency bill out of pocket.

Not ideal for: budget shoppers comfortable with a payout cap, pets that mostly generate small one-off issues, owners who want routine or exam-fee coverage, and anyone likely to cancel after a few price hikes — you have to keep the policy to bank the deductible advantage.

How the Per-Condition Deductible Works

Trupanion's deductible is charged per condition, not per year: you meet it once for each new illness or injury, and it never resets as long as your coverage stays continuously active. That single design choice is the biggest reason Trupanion can be a bargain for one pet and a poor deal for another, and it's the part most reviews skate past.

You choose a deductible from $0 to $1,000. With an ordinary annual deductible, the meter resets every policy year. With Trupanion, once you've paid the deductible for, say, allergies, you never pay it again for allergies for the rest of your pet's life.

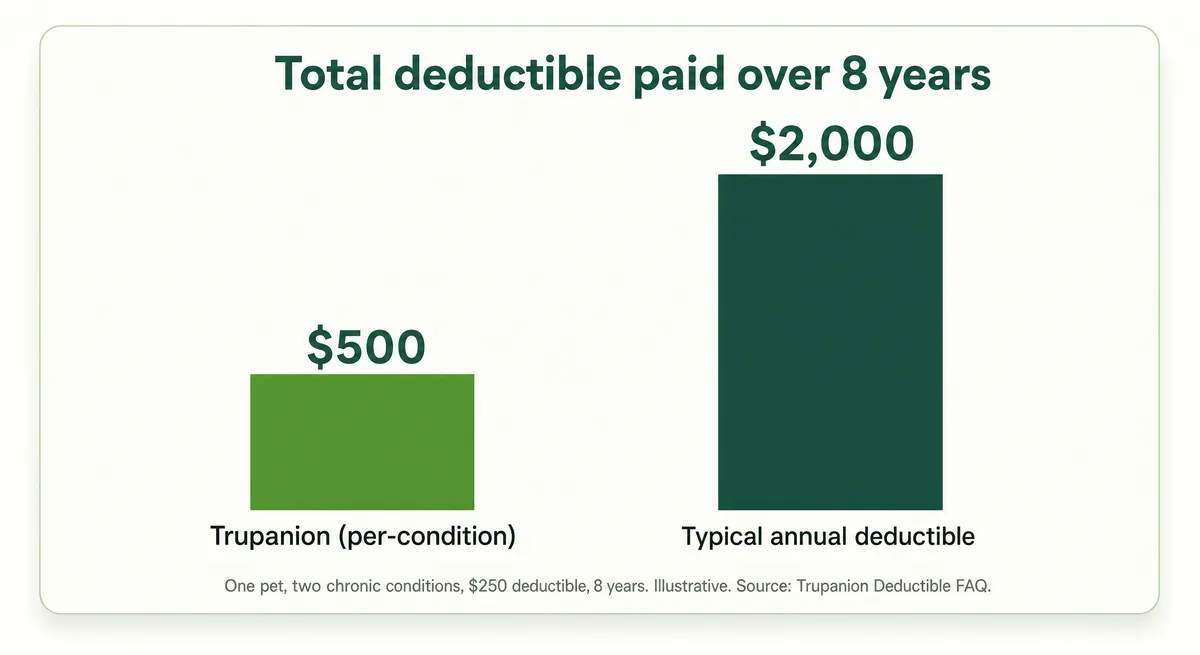

Where it saves you money

Say your dog develops two chronic conditions — allergies and diabetes — on a $250 deductible, over eight years of treatment. With Trupanion you pay $250 once for each: $500 total. A carrier with a $250 annual deductible would charge it every year: $250 × 8 = $2,000. That's roughly $1,500 less over your pet's life, and the gap only widens the longer a lifelong condition is treated (Trupanion's own worked example).

Where it costs you more

Now flip it. A healthy pet with a run of unrelated one-off problems — a swallowed sock one month, an ear infection the next, a torn nail after that — can trigger a fresh deductible each time. Four separate conditions in a year could mean four $250 deductibles ($1,000) with Trupanion versus a single $250 with an annual-deductible carrier (NerdWallet). And whether recurring symptoms count as one condition or several is Trupanion's call, which owners sometimes dispute.

One more wrinkle: Trupanion applies your 90% reimbursement before subtracting the remaining deductible, which nets slightly less than carriers that subtract the deductible first. The gap is 10% of your remaining deductible — about $20 on a $200 deductible (NerdWallet).

The catch most reviews skip

That "never resets" promise only holds while the policy stays continuously active — let it lapse and re-enroll, and conditions you'd built up coverage for can be treated as pre-existing. You can also only lower your deductible within the first 30 days; after that you can raise it but not reduce it. If any of this is load-bearing for your budget, confirm the current terms in your state's sample policy before you buy.

What Trupanion Really Costs (and Why Premiums Rise)

Trupanion is among the most expensive pet insurers, and there's no single price — what you pay swings with your pet's breed, age at signup, and ZIP code. In one national sample from mid-2026, Trupanion averaged about $165 a month for a dog and $83 for a cat — roughly $100 more per month for the dog than the industry average.

Because location and breed drive so much, real quotes range widely. NerdWallet's 2026 sample quotes for pets in Katy, Texas ran from about $168 a month for a medium mixed-breed dog to $371 for a French bulldog at age 2, and climb further in high-cost metros. Trupanion prices on age at enrollment, breed, ZIP code, and your chosen deductible, so always pull a real quote — a "starts at" figure won't reflect your pet.

"No birthday pricing" vs. real increases (can you negotiate?)

Trupanion's "Pricing Promise" is true as far as it goes: your premium won't rise just because your pet had a birthday (Trupanion, How We Price). But that's not a frozen price. Trupanion raises rates by cohort — groups of similar pets by breed, enrollment age, and location — as regional vet costs climb. So your bill can still jump sharply, just not because of your pet's age.

How sharply? California regulators approved Trupanion increases of roughly 12%, then 29%, then 33% in about two years, with the largest effective for mid-2025 renewals. One California owner reported their monthly premium climbing from $128 to $251 over three years (an owner account, not a typical figure). Cohort increases have hit owners in other states too.

Can you push back? Not really — pet insurance rates are filed with and overseen by state insurance regulators (the exact rules vary by state), so there's no haggling a renewal down. What you can do is change your coverage: raising your deductible (or lowering your reimbursement percentage where your state allows it) trims the premium. Just weigh that against the long-term deductible math above.

Coverage, Reimbursement & VetDirect Pay

Trupanion sells one comprehensive accident-and-illness plan that reimburses 90% of your actual vet bill with no payout caps, and it can pay your vet directly at checkout. There's no accident-only tier and no wellness plan.

The plan covers hospitalization and surgery, diagnostics, hereditary and congenital conditions, cancer, prescription medications, and some prescription food and supplements. Two features set it apart:

- No payout limits. No per-incident, annual, or lifetime cap — which matters when a cancer or complex-surgery case runs into five figures.

- Actual-cost reimbursement. Trupanion pays a percentage of your real invoice, not a "reasonable and customary" fee schedule that can leave you owing the difference at a pricey specialty or emergency hospital.

Reimbursement is a flat 90% in most states (a few offer lower coinsurance options), so once you've met a condition's deductible you pay just 10% of covered costs. One important exception: exam fees and taxes are never reimbursed — more on that next.

VetDirect Pay: the standout feature (and its limit)

VetDirect Pay is Trupanion's signature perk. At a participating clinic, the hospital submits your invoice and Trupanion sends its share straight to the vet, so you cover only your deductible, your 10%, and any excluded items — no fronting a big bill and waiting weeks for a refund. One owner described a roughly $988 bill where Trupanion paid about $719 within about four minutes at checkout (an owner account).

The catch: it only works at clinics running Trupanion's software. Many primary vets and some ER and specialty hospitals participate, but plenty don't — call ahead to confirm, especially for your nearest emergency hospital. Where direct pay isn't available you pay up front and file for reimbursement, which Trupanion says it processes for most claims within 24 hours.

What Trupanion Doesn't Cover

Trupanion covers accidents and illnesses generously, but it never pays exam fees or sales tax, offers no routine or wellness care, and won't touch pre-existing conditions — and one clause, the bilateral exclusion, catches owners off guard.

Exam fees and taxes. Nearly every vet visit for a sick pet carries an exam or office-visit fee, and Trupanion excludes it — you pay it out of pocket even on an otherwise-covered claim. It also excludes sales tax and all routine and preventive care: vaccines, spay/neuter, flea and tick control, and dental cleanings.

Pre-existing conditions. Anything your pet showed signs or evidence of in the 18 months before your policy's effective date — or during the waiting period — is excluded, even if it was never formally diagnosed. (The policy form can reach back further than 18 months, so check your state's sample policy.) This is why enrolling a young, healthy pet matters: buying a policy is easy, but getting a specific condition covered is a separate question.

The bilateral exclusion (the knee trap)

This is the fine print that surprises people most. For a set of conditions that tend to strike both sides of the body, if your pet showed signs on one side before coverage began (or during the waiting period), the other side is excluded too — even years later. So if your dog had a minor luxating patella in the left knee before enrolling, a later luxating patella needing surgery on the right knee can be denied under the bilateral clause, even though the right side was healthy at signup. State policy forms vary, so confirm the exact list.

The listed bilateral conditions include cruciate ligament injuries, luxating patella, hip and elbow dysplasia, cataracts, cherry eye, glaucoma, and entropion/ectropion. If your pet has any history on one side, ask Trupanion in writing how it will treat the other side before you count on that coverage.

One bright spot: Trupanion's waiting periods are short — 5 days for accidents and 30 days for illnesses — with no extra-long wait for cruciate or orthopedic conditions that some competitors impose.

Is Trupanion Legit? Financial Strength & Complaints

Yes — Trupanion is a legitimate, state-regulated insurer, not a scam. Its U.S. policies are underwritten by the American Pet Insurance Company (APIC), a licensed carrier wholly owned by Trupanion, Inc. (Nasdaq: TRUP). The honest nuance is in its ratings and its complaint record.

Financial strength. APIC carries a Demotech Financial Stability Rating of A″ ("A Double Prime"). It isn't currently rated by A.M. Best, so disregard any older "B++" you may see quoted. On capital, Trupanion's insurance arm held a capital cushion of roughly $140 million above its regulatory minimum at the end of 2024 — a sign of financial strength, though, like any insurer, payouts still depend on its solvency and your policy's terms.

What the complaint record actually shows

Here's where reviews split. On the Better Business Bureau, the Trupanion brand is BBB-accredited with an A+ rating, yet its customer-review average sits near 1 out of 5 across a couple hundred reviews. On Trustpilot it scores about 4.4 stars — but that's a paid, company-managed profile that actively invites customers to review, so it skews positive. Neither number alone tells the story.

Read together, a pattern emerges: many positive reviews credit Trupanion with paying claims quickly, while the negative reviews cluster around two themes — pre-existing and bilateral denials, and premium increases. As one of the largest pet insurers, Trupanion also generates a high raw volume of complaints simply because it has so many policyholders; the fairer measure is the complaint ratio relative to its size, which regulators track through the NAIC complaint index — worth checking for any carrier you're weighing.

Regulators have historically fined Trupanion for licensing and marketing lapses — a 2016 Washington action over unapproved rates and advertising, for instance — but those are housekeeping issues, not findings of bad-faith claim denial.

Trupanion vs. Lemonade

Trupanion and Lemonade sit at opposite ends of the pet-insurance spectrum. Trupanion is the premium, no-limits, pay-your-vet-directly option; Lemonade is the budget, app-first alternative with an annual deductible and a payout cap. Here's the head-to-head.

| Feature | Trupanion | Lemonade |

|---|---|---|

| Deductible | Per-condition, lifetime ($0–$1,000) | Annual, resets yearly ($100–$750) |

| Reimbursement | Flat 90% | 70%, 80%, or 90% |

| Payout limit | Unlimited | Annual cap ($5,000–$100,000) |

| Pay the vet directly? | Yes (VetDirect Pay) | No — reimburses you via app |

| Starting price | Highest among majors | Low; bundling discounts available |

| Wellness/routine care | Not offered | Optional add-on |

| Availability | All 50 states + DC | ~42 states + DC |

The deepest difference is the deductible: Lemonade's resets every year, while Trupanion's is paid once per condition and then never again for that condition — so the two designs quietly reward very different pets and spending patterns.

Which should you pick? If you have a young, low-risk pet and a tight budget — and you're comfortable with a payout cap and paying up front — the lower starting price and optional wellness coverage of this app-based plan make it the easier yes. If your pet is a chronic-illness-prone or large breed, or you value uncapped coverage and never fronting a big emergency bill, Trupanion's per-condition deductible and direct pay are worth the premium.

One catch cuts both ways: Lemonade uses attained-age pricing, so its premiums climb as your pet gets older, while Trupanion's rise by cohort instead — neither stays cheap forever. For the full breakdown, including how each handles pre-existing conditions and claims, see our side-by-side comparisons.

What Real Owners Say

Across Reddit and Quora, the crowd consensus is consistent: Trupanion pays claims reliably and the direct pay is a genuine lifesaver — but the rising price is the near-universal gripe. (These are owner opinions, not verified facts, and forums skew toward people with something to vent about.)

The loudest complaint is renewal increases. On r/petinsurancereviews, rate-hike threads outnumber everything else. Owners describe premiums climbing steeply over a few years, especially in California and other high-cost areas, and several feel "trapped" — unable to afford the new price yet unable to switch without their pet's conditions becoming pre-existing somewhere else.

The biggest surprise is the per-condition deductible. Newcomers repeatedly realize it applies per condition, not per year — and that a pet with recurring, separate issues can trigger a fresh deductible each time.

What owners praise. Two themes hold up even among critics. First, Trupanion actually pays: some owners report five-figure and even ~$80,000 lifetime payouts on chronically ill pets. Second, VetDirect Pay is the number-one reason people stay, because they never have to front a huge bill. On Quora, a licensed insurance agent framed it simply: pet insurance is peace of mind you're glad to have when the emergency arrives.

The net verdict from the crowd: if you understand the deductible and can stomach the price curve, Trupanion is a trusted, generous insurer — just go in with eyes open about where the cost is headed.

Who Should (and Shouldn't) Choose Trupanion

Trupanion earns its premium for pets with real catastrophic or chronic risk, and it's a poor deal for low-risk pets whose owners shop on price first. Here's how that breaks down by situation.

Choose Trupanion if…

- You're insuring a young, healthy puppy or kitten — enroll early, before anything can be called pre-existing, and you get the most from the lifetime deductible.

- Your pet is a breed prone to chronic or hereditary conditions (allergies, diabetes, hip or elbow problems, cancer), where the per-condition deductible and uncapped payouts earn their keep.

- You'd struggle to front a $5,000–$10,000 emergency bill and want VetDirect Pay to settle it at the counter.

Look elsewhere if…

- You have a low-risk pet and a tight budget, and a cheaper annual-deductible plan — with a payout cap you can live with — makes more sense.

- You want wellness or exam-fee coverage: Trupanion offers neither, and there's no multi-pet discount.

- You're on a fixed income and worried a cohort rate hike could price you out in a few years — a real risk for pets enrolled later in life.

Whichever way you lean, if you go with Trupanion, enroll before symptoms appear — and know that switching away later can be hard, because ongoing or chronic conditions are likely to count as pre-existing at a new carrier (rules for long-cured conditions vary). To pressure-test the price against alternatives, weigh it in our side-by-side comparisons and run your own numbers with our cost guide.

Frequently Asked Questions

Is Trupanion pet insurance worth it?

It depends on your pet and your budget. Trupanion is worth its higher price for pets with real chronic or catastrophic risk — its per-condition deductible and uncapped payouts shine on lifelong conditions, and VetDirect Pay means you don't front a big bill. It's a weaker value for young, low-risk pets on a tight budget, who often do better with a cheaper annual-deductible plan that has a payout cap they can accept.

Does Trupanion raise your rates when you file a claim?

No. Trupanion doesn't raise your premium because of the claims you file, or because your pet had a birthday. Instead it adjusts rates by cohort — groups of similar pets by breed, age at enrollment, and location — as veterinary costs climb in your area (Trupanion). So your bill can still rise sharply over time, just not as a penalty for using your coverage.

What isn't covered by Trupanion?

Trupanion doesn't cover exam or office-visit fees, sales tax, or any routine and wellness care (vaccines, spay/neuter, dental cleanings, flea and tick control). It also excludes pre-existing conditions and applies a bilateral clause — a prior issue on one knee, hip, or eye can permanently exclude the other side (Trupanion). Always read your state's sample policy for the full list.

Does Trupanion pay the vet directly?

Yes — at participating clinics. Trupanion's VetDirect Pay lets the hospital bill Trupanion at checkout, so you pay only your deductible, your 10% coinsurance, and any excluded items instead of fronting the whole invoice. It only works where the clinic runs Trupanion's software, so confirm with your regular vet and your nearest emergency hospital before you count on it.

How much does Trupanion cost per month?

There's no single price — it depends on your pet's breed, age at enrollment, ZIP code, and deductible. As a rough gauge, one 2026 national sample put Trupanion near $165 a month for a dog and $83 for a cat, among the highest of the major carriers (U.S. News). Large or high-risk breeds in expensive metros can run well over $200. Always pull a real quote.

Which pet insurer has the fewest complaints?

There's no clean “fewest complaints” winner, because larger insurers naturally rack up more raw complaints than small ones. The fairer measure is the NAIC complaint index, which weighs complaints against a company's size. Trupanion draws a high volume simply because it's one of the biggest, but its complaints cluster around price increases and pre-existing denials rather than refusing to pay valid claims. Check the NAIC index for any carrier you're comparing.

Trupanion or Lemonade — which is better?

Neither is universally better; they suit different pets. Trupanion fits chronic-illness-prone or large breeds and owners who want uncapped coverage and direct-to-vet payment. Lemonade fits budget-minded owners of young, low-risk pets who are fine with an annual deductible, a payout cap, and paying up front. See our side-by-side comparisons to weigh them for your own pet.

Sources

- Deductibles — how Trupanion's per-condition deductible works — Trupanion

- No payout limits — Trupanion

- Trupanion Pet Insurance Review 2026 — U.S. News & World Report

- What isn't covered by a Trupanion policy — Trupanion

- Trupanion Pet Insurance Review 2026: Pros and Cons — NerdWallet

- How We Price (Policy Basics flyer) — Trupanion

- Trupanion hits California pet owners with another rate hike — Insurify

- Trupanion 33.69% price increase in 2026 (owner report) — Reddit — r/petinsurancereviews

- Pet insurance coverage — Trupanion

- Vet direct pay vs. reimbursement — Trupanion

- Data point for Trupanion direct pay to vet (owner report) — Reddit — r/petinsurancereviews

- Pre-existing conditions, and how they're determined — Trupanion

- American Pet Insurance Company sample policy form (Maine filing) — Maine Bureau of Insurance

- When does my coverage begin (waiting periods) — Trupanion

- Report on Examination of American Pet Insurance Company — New York Department of Financial Services

- American Pet Insurance Company — Financial Stability Rating — Demotech, Inc.

- Trupanion, Inc. FY2024 Form 10-K — U.S. Securities and Exchange Commission

- Trupanion — BBB profile & customer reviews — Better Business Bureau

- Trupanion reviews — Trustpilot

- Seattle pet insurer fined $150,000 for many violations — The Seattle Times

- Lemonade pet insurance FAQ (deductible, reimbursement, limits, add-ons) — Lemonade

- Just want to share my experiences with Trupanion (owner reports incl. ~$80k payout) — Reddit — r/petinsurancereviews

- Is Trupanion pet insurance a scam? (owner and agent answers) — Quora