If you're pricing pet insurance in Illinois, here's the short version: expect to pay roughly $30–$60 a month for a dog and $15–$40 for a cat, depending on your city, your pet's age and breed, and how much coverage you choose. Quotes vary a lot between carriers, so it pays to compare a few. And there's no Illinois-only pet insurer — you buy a nationwide carrier that's available to Illinois residents and file claims from wherever you live, Chicago to Carbondale.

If you just want a pick, here's the use-case shortlist this guide builds toward (the cheapest is usually Pumpkin):

- Best overall: ASPCA

- Cheapest: Pumpkin

- Best on a budget: Embrace

- Best for paying the vet directly: Trupanion

- Best digital experience: Lemonade

- Most comprehensive: Fetch

- 100% reimbursement option: Figo

One piece of timely news: Illinois just passed its first pet-insurance law (HB 3595), which takes effect July 1, 2026 and adds real consumer protections — a cap on illness waiting periods, a 30-day free look, and clear disclosure of what's excluded. As you'll see, though, it stops well short of forcing insurers to cover pre-existing conditions, and it doesn't cap premiums.

Below, we get specific: what coverage actually costs across Illinois, why a single Chicago vet bill can dwarf a year of premiums (and how to find an affordable, non-corporate clinic), why a clinic "wellness membership" isn't insurance, exactly what the new law guarantees, and which carrier fits your situation.

Table of Contents

- How much does pet insurance cost in Illinois?

- Why Chicago vet care costs so much — and how to manage it

- Wellness membership vs pet insurance — don't confuse them

- How paying the vet works in Illinois — don't get surprised at the counter

- Illinois pet insurance laws: what HB 3595 guarantees you

- Best pet insurance in Illinois: use-case picks

- Illinois-specific risks worth insuring against

- Already have a diagnosis? Read this before buying

- Frequently Asked Questions

- Sources

How much does pet insurance cost in Illinois?

In Illinois, expect to pay roughly $30–$60 a month for a dog and $15–$40 for a cat, with the statewide average around $57/mo for dogs and $27/mo for cats. What you actually pay turns on your pet's age and breed, your ZIP code, and the deductible, reimbursement rate, and annual limit you choose.

Those are accident-and-illness premiums — Embrace, for instance, pegs typical Illinois coverage at $25–$50 a month in 2025. Because there's no Illinois-only insurer, your rate comes from a nationwide carrier's pricing for your specific pet and address.

Average cost by city

Where you live matters — Chicago is the priciest metro and the suburbs run lower. Lemonade's 2025 sample premiums for a representative dog show the spread (your quote will vary by pet, age, breed, and coverage level):

| City | Sample monthly premium (Lemonade dog, 2025) |

|---|---|

| Chicago | $50–$55 |

| Aurora | $40–$45 |

| Naperville | $40–$45 |

| Joliet | $35–$40 |

The gap tracks local vet prices — a Chicago clinic simply charges more than one in Joliet — so the same pet costs more to insure downtown than in the suburbs or downstate.

Cost by pet, breed, and age

Age is the single biggest lever — premiums roughly double from puppy to senior. Here's WSJ's Illinois sample for dogs:

| Carrier | Puppy | Age 2 | Senior |

|---|---|---|---|

| Pumpkin | $34.11 | $34.11 | $63.70 |

| Spot | $36.39 | $36.39 | $67.95 |

| ASPCA | $38.46 | $38.46 | $71.82 |

| Pets Best | $46.39 | $41.62 | $79.33 |

Breed and your deductible choice swing it too. In one widely-cited example (general, not Illinois-specific), a property-casualty professional priced a German shepherd enrolled at 16 weeks at about $63/mo with a $400 deductible, or $35/mo with a $1,000 deductible — same dog, very different premium.

Why Illinois premiums vary so much — shop around

Quotes for the same coverage can land miles apart. In one Reddit discussion, owners comparing quotes saw most insurers around $60–$90 a month, Trupanion at $200–$278 (one was quoted $500), and Pumpkin near $51 — a single anecdote, but a common kind of experience. That's not a glitch — carriers weight age, breed, and ZIP differently, and some (Trupanion especially) price for unlimited payouts and paying the vet directly. Raising your deductible or lowering your reimbursement percentage is the quickest way to pull a quote down. The fix: pull three or four quotes for the exact same deductible, reimbursement percentage, and annual limit before you judge any carrier on price.

Why Chicago vet care costs so much — and how to manage it

This is the real reason to insure a pet in Illinois: Chicago vet bills are steep, and one bad day can dwarf a whole year of premiums. Here's what Chicago owners actually report paying — real bills, not statewide averages:

- A routine senior-dog checkup — exam, vaccines, a urine test — ran about $750.

- ER hospitalization quoted at roughly $2,000 a night.

- A neuter quoted near $1,000 at a corporate clinic.

- Dental at a VCA hospital quoted $2,000–$3,000 — a comparable cleaning ran under $1,100 at UIC's Medical District Veterinary Clinic.

A lot of the local anger points at one thing: private-equity and corporate consolidation. Chicago owners say chains like VCA and Banfield (both Mars-owned) and Thrive have been buying up neighborhood hospitals and pushing prices up — one owner reported costs running "400% higher" after a buyout. To be fair, vets are genuinely underpaid and short-staffed, so not every increase is greed — but the jumps are real, and you can route around them.

How to find an affordable, non-corporate vet

Chicago owners trade names of independent clinics they trust — among those they point to are Ravenswood Animal Hospital, the Medical District Veterinary Clinic at UIC, Burnham Park, Forest Glen, and Oz. A smart local tactic: look up a clinic's business license to see who actually owns it before assuming it's independent. For low-cost spay/neuter, Spay Illinois serves the suburbs, and Dutch, an online vet service, may help with some minor, non-emergency issues where it's available. Prices also vary widely across the state, so suburban and downstate clinics often beat Chicago rates for the same procedure.

All of this feeds one insurance decision: your annual limit. A $5,000 cap looks fine until a single specialty surgery — a TPLO knee repair or a swallowed-object removal — blows right through it. In a city where one claim can run into five figures, an unlimited or high annual limit is usually worth the few extra dollars a month — it's the difference between a five-figure specialty bill wrecking your month and paying just your deductible and coinsurance.

Wellness membership vs pet insurance — don't confuse them

Plenty of Illinois owners think they have pet insurance when they actually have a wellness membership. Some literally call their Banfield plan "my pet insurance" — understandable, since Banfield's clinics sit inside PetSmart stores all over the state. But the two products do completely different jobs.

A wellness membership is prepaid preventive care — exams, vaccines, a dental cleaning, parasite prevention. It has no accident, illness, or catastrophic coverage: if your dog swallows a sock or tears a knee, a wellness plan pays nothing toward it. Accident-and-illness insurance is the reverse — it covers the big, unexpected bills, not routine checkups (unless you bolt on a wellness rider). Here's the split:

Chicago clinics offer plenty of these memberships — GoodVets' "GoodPet+" ran about $120/mo (recently discontinued), Banfield's Active Care Plus around $63/mo, and Forest Glen's "Happy Healthy Pets" about $50/mo. They're fine for predictable care — but a plan only pays off if you'd actually use every service it includes, and there are two catches: a clinic can discontinue its plan (as GoodVets did, leaving members scrambling), and a membership ties you to one provider.

For most Illinois owners the smartest combination is simple: self-fund the routine stuff (or use a cheap wellness plan if the math truly works for you), and buy accident-and-illness insurance for the catastrophic bills a Chicago ER can hand you. The membership smooths small, expected costs; insurance is the backstop for the ones that could otherwise force a heartbreaking choice.

How paying the vet works in Illinois — don't get surprised at the counter

Before you pick a carrier, understand how you'll actually pay — in a city where one visit can run into the thousands, the mechanics matter. With almost every pet insurer, coverage is reimbursement-first: you pay the vet in full, file a claim, and get reimbursed often within days, though it can take a couple of weeks depending on the insurer and the claim. You front the money first.

That's the rub for big Chicago bills. Owners say fronting a $2,000 ER night or a five-figure surgery and waiting on reimbursement is a real hardship — which is why some choose a carrier that pays the clinic directly.

The main option is Trupanion's VetDirect Pay, which can settle with the hospital at checkout instead of reimbursing you later — but only if your clinic is enrolled, so ask your Chicago-area vet whether they participate before you count on it. (More on Trupanion's trade-offs in the picks below.)

Without direct pay, a financing bridge can cover the gap: a veterinary credit line like CareCredit, or an online vet such as Dutch for minor issues. Just watch the deferred-interest fine print on those cards, and treat financing as a stopgap, not coverage. For a planned procedure, ask whether your insurer offers pre-authorization or a coverage review, and get any answer in writing — final payment still depends on your pet's records and the policy's terms.

One reality even insured owners hit: you still owe your deductible, your share of the coinsurance, and anything the policy doesn't cover — and you owe the entire bill if a claim is denied. So keep a small cushion or a financing option ready even after you're covered.

Illinois pet insurance laws: what HB 3595 guarantees you

As of July 1, 2026, Illinois has its first pet-insurance law. House Bill 3595 adds a dedicated Pet Insurance article (Article XLVIII) to the Illinois Insurance Code — the state's first real rulebook for the product. It won't make coverage cheaper or force anyone to cover more, but it gives Illinois buyers concrete protections worth knowing. Here's the short version:

| What HB 3595 guarantees | What it does not do |

|---|---|

| Illness and orthopedic waiting periods capped at 30 days; no waiting period for accidents | It does not force insurers to cover pre-existing conditions |

| A 30-day "free look" — return the policy for a full refund if you haven't filed a claim | It does not cap what insurers can charge |

| Mandatory up-front disclosure of exclusions, limits, and waiting periods (including pre-existing, hereditary, congenital, and chronic exclusions) | It does not guarantee that any given claim gets paid |

That 30-day cap is a genuinely big deal. At many carriers, orthopedic conditions like cruciate-ligament tears carry six-to-twelve-month waits; under the new law, Illinois limits them to 30 days for the policies it governs. And the disclosure rule forces a carrier to spell out, before you buy, exactly what it won't cover. Illinois joins a small but growing group of states with pet-specific insurance statutes modeled on the national (NAIC) template.

How to file a complaint with the Illinois Department of Insurance

If a carrier mishandles a claim, you're not stuck with its decision. The Illinois Department of Insurance (IDOI) takes consumer complaints and will take your dispute up with the insurer — a free, state-backed channel most owners don't realize they have. File through the IDOI consumer portal, and keep your policy documents, the claim, and the insurer's denial letter on hand to support your case.

Best pet insurance in Illinois: use-case picks

There's no single "best" pet insurer in Illinois — the right one depends on what you're optimizing for. Every option below is a nationwide carrier available to Illinois residents; match the pick to your situation rather than chasing a one-size winner. Sample Illinois quotes are included where owners have shared them:

- Best overall — ASPCA. The consensus all-around pick, with broad coverage including behavioral and alternative therapies.

- Cheapest — Pumpkin. Routinely the lowest-priced in head-to-heads; one Illinois owner was quoted about $51/mo.

- Best on a budget — Embrace. Chicago owners report roughly $62/mo for a $1,000 deductible, 90% reimbursement, and an unlimited annual limit.

- Best for paying the vet directly — Trupanion. No payout limits, no "birthday" price hikes, and its VetDirect Pay program — but pricier (owners report $200–$278/mo).

- Best digital experience — Lemonade: fast app-based claims (reimbursement-only).

- Most comprehensive — Fetch; 100% reimbursement option — Figo (where available — deductibles, limits, and exclusions still apply).

A fair word on Trupanion: vets praise its VetDirect Pay program because it solves the front-the-Chicago-bill problem — but some owners report frustrating claims experiences with it. Weigh the direct-pay convenience against the higher price, and read recent claim reviews before committing. Choose on the dimensions that matter in Illinois — direct-pay availability, annual limits, and claim handling — not marketing copy.

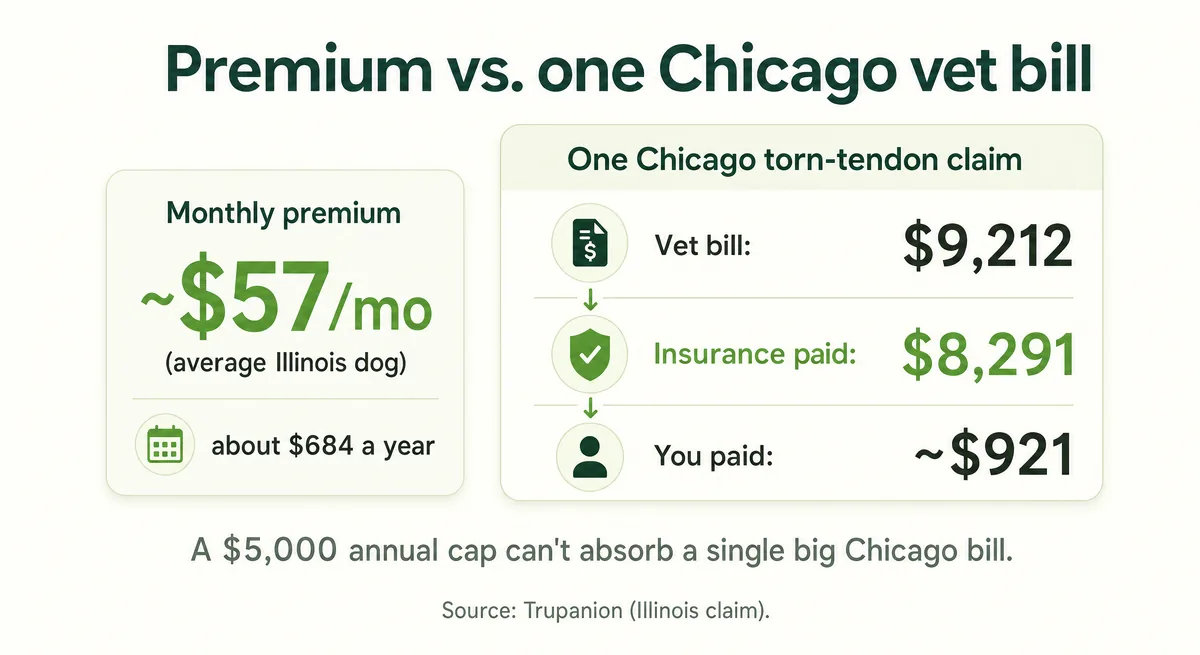

Is it worth it? Two real Illinois claims: ASPCA paid $5,625 of a $6,794 torn-ACL bill, and Trupanion paid $8,291 of a $9,212 Chicago torn-tendon claim for a dog named Crosby. Against a $50–$60 monthly premium, a single orthopedic surgery — see our guide to dog ACL surgery — can return more than years of premiums in one claim.

Tie it back to your lane: a clean, young pet can chase the cheapest solid plan; a household that dreads fronting a big Chicago bill should weigh direct pay; and anyone insuring against a five-figure specialty surgery should prioritize a high or unlimited annual limit over a few dollars of monthly savings. Whichever you lean toward, pull a current quote for the exact deductible and limit you want, and — if direct pay matters to you — confirm your own Chicago-area clinic actually participates before you decide.

Illinois-specific risks worth insuring against

Illinois's climate and geography create a handful of region-specific health threats — and they're exactly the kind of accident-and-illness events insurance exists for (a wellness plan won't touch them). A few worth knowing:

- Leptospirosis — a bacterial infection spread through Illinois soil and standing water, and transmissible to humans; serious cases mean days of hospitalization.

- Lyme and other tick-borne disease — notable across Illinois; ask your vet about tick prevention and the Lyme vaccine.

- Blue-green algae poisoning — thrives in Illinois fresh water in warm weather and can be rapidly fatal; never let a pet drink or swim where there's bluish-green surface scum.

- Heatstroke and toxic plants such as hydrangeas, among the common warm-weather hazards for Illinois pets.

- Venomous snakes — downstate Illinois is home to the cottonmouth, copperhead, and timber rattlesnake; a serious bite can mean a four-figure emergency.

- Winter hazards — road salt on paws, plus cold-weather slips and injuries.

None of this should scare you off a hike or a swim — it's simply why a solid accident-and-illness policy (not a routine-care membership) is the right backstop for an Illinois pet.

Already have a diagnosis? Read this before buying

Here's the catch that surprises Illinois owners most: the very vet visit that scared you into buying insurance can itself become a pre-existing exclusion. If your dog just had foreign-body surgery or your cat was diagnosed with a chronic condition, a policy you buy today will almost certainly exclude that condition — and sometimes the matching body part too (a left-knee cruciate tear can get the right knee excluded as well). The single best move is to enroll before symptoms start, while your pet's record is clean.

Two red flags to watch when you read the fine print:

- Renewal terms. Read how a policy treats an ongoing condition at renewal, along with any per-condition or annual limits — the fine print is where coverage can quietly narrow over time.

- Upper age limits. A few policies only enroll new pets up to about age 8 — a problem if you wait too long with a senior pet.

It isn't always hopeless: some carriers reinstate a curable condition after a symptom-free window, and changing carriers has its own rules. For the full mechanics, see our guides to pre-existing conditions and switching pet insurance. But the Illinois takeaway is simple: the cheapest coverage to get is the policy you buy before your pet needs it.

Frequently Asked Questions

How much does pet insurance cost in Illinois?

Pet insurance in Illinois runs roughly $30–$60 a month for a dog and $15–$40 for a cat, with the statewide average around $57/mo for dogs and $27 for cats. Your actual rate depends on your city (Chicago is priciest), your pet's age and breed, and the deductible, reimbursement rate, and annual limit you choose.

Which company has the cheapest pet insurance in Illinois?

Pumpkin is usually the cheapest in head-to-head comparisons — one Illinois owner was quoted about $51/mo. But cheapest isn't automatically best: a low premium can hide a higher deductible or lower reimbursement, so compare the full structure (deductible, reimbursement %, and annual limit) before deciding on price alone.

Is it really worth it to get pet insurance?

For most Illinois owners, yes — because the bills it offsets are large. A Chicago ER night can run about $2,000 and a specialty surgery into five figures, while premiums are roughly $50–$60/mo. Real Illinois claims show the math: ASPCA paid $5,625 of a $6,794 torn-ACL bill and Trupanion paid $8,291 of a $9,212 claim. It's least useful for routine care and most useful as a catastrophic backstop.

Does pet insurance cover diabetes?

Only if it isn't pre-existing. If your pet is diagnosed with diabetes before your coverage starts (or during the waiting period), every insurer will exclude it — and because diabetes is a chronic condition, that exclusion generally sticks. Enroll before any symptoms appear and the condition can be covered if it develops later.

Will pet insurance cover heart murmurs?

It depends on timing. A murmur — or related symptoms — noted in your pet's records before coverage begins (or during the waiting period) will usually be treated as pre-existing and excluded. A murmur first detected after your waiting periods are over is generally covered, though coverage for congenital and hereditary conditions varies by carrier, so check that exclusion before buying.

Is pet insurance cheaper downstate than in Chicago?

Generally yes. Chicago is the most expensive metro in the state — premiums run about $50–$55/mo there versus $35–$40 in Joliet — because rates track local vet costs. Suburban and downstate owners usually pay less for the same coverage.

Is Banfield's Optimum Wellness Plan the same as pet insurance?

No. Banfield's Optimum Wellness Plan is a prepaid preventive-care membership — exams, vaccines, dental cleaning — with no accident or illness coverage. It won't pay for an emergency surgery or a new diagnosis. It's fine for routine care, but it is not a substitute for accident-and-illness insurance.

Should I add a wellness plan?

Only if you'd actually use everything it includes. A clinic wellness membership prepays or discounts routine services, while an insurance wellness rider reimburses eligible preventive costs up to set limits — either way, it pays off mainly for owners who use all those services. For most people the cheaper approach is to self-fund predictable routine costs and put your premium dollars toward accident-and-illness coverage instead.

Sources

- Best Pet Insurance in Illinois — U.S. News & World Report

- Best Pet Insurance in Illinois — WSJ Buy Side

- Insuring Your Pet in Illinois — Embrace Pet Insurance

- Illinois Pet Insurance Guide — Lemonade

- What Is the Average Cost of Pet Insurance? — Quora

- Vet bill scared me into getting pet insurance — what do people actually use? — Reddit (r/petinsurancereviews)

- What Is Your Vet Bill Like? (r/chicago) — Reddit (r/chicago)

- Are there any non-private-equity-owned vets/clinics in Chicago? — Reddit (r/AskChicago)

- Optimum Wellness Plans — Banfield Pet Hospital

- What Chicago vet clinics offer monthly wellness plans (not insurance)? — Reddit (r/AskChicago)

- If you have a dog or cat, do you have pet insurance? Why or why not? — Quora

- Who are the leading companies in the pet insurance space? — Quora

- Is there a real pet insurance (USA) that's not a scam? — Quora

- HB3595 — Pet Insurance (215 ILCS 5, Art. XLVIII) — Illinois General Assembly

- Pet Insurance — Consumer Information — Illinois Department of Insurance

- ASPCA Pet Health Insurance — ASPCA Pet Health Insurance

- Pet Insurance in Illinois — Trupanion

- What's Covered: Illinois Pet Insurance — Nationwide Pet Insurance

- What is a good pet insurance company that serves [my state]? — Quora