Is Embrace pet insurance worth it? For the right pet and the right owner, yes — but "the right owner" is doing a lot of work in that sentence, and the star ratings won't help you sort it out. The same company earns warm, five-star praise on one review platform and a near–one-star average on another. That split isn't random, and a big part of this review is explaining it.

We're a licensed insurance agency, and our job here is to decode the fine print, not to bolt a rating onto a sales page. So we read Embrace's actual plan documents — the deductible math, the waiting periods, the pre-existing rules, the claim form — so you don't have to. Then we set that fine print against what real owners report and against the hard numbers behind the company: who actually underwrites the policy, how financially sound they are, and how its renewal mechanics work.

Here's the short version. Embrace is a broad-coverage choice if you enroll a young, healthy pet and value coverage depth — and a weaker fit if you need the lowest matched quote or are trying to insure an older pet with a medical history. Price can only be compared on identical quote inputs. The rest of this page shows the work.

Table of Contents

- The verdict: who Embrace is (and isn't) for

- Who underwrites Embrace (and is it trustworthy)?

- What Embrace costs — and why your renewal will rise

- How Embrace pays: deductible, reimbursement & the Healthy Pet Deductible

- Waiting periods & pre-existing conditions

- What's covered, what's not, and the rider surprises

- How to file an Embrace claim (and how fast you get paid)

- Embrace vs Lemonade: which should you pick?

- Is USAA pet insurance the same as Embrace?

- What real customers say

- Frequently Asked Questions

- Sources

The verdict: who Embrace is (and isn't) for

Embrace is a strong fit if you enroll a young, healthy dog or cat and care about breadth of coverage. Its accident-and-illness plan is genuinely comprehensive — it folds in dental illness and hereditary and congenital conditions that some competitors treat as add-ons, and you can bolt on a flat-allowance wellness plan for routine care. Enroll early, before anything shows up in the medical records, and you get the most out of it. Put plainly, it's built for the owner who wants deep coverage in place well before they ever need to use it — and who can absorb renewal repricing.

Embrace works against you in three situations. First, if you're shopping on price alone: only matched quotes for the same pet, ZIP code, limit, deductible, reimbursement, and add-ons can establish whether Embrace or a competitor is lower. Second, if you're insuring an older pet or one with a medical history: the pre-existing rules and attained-age pricing can make switching late unattractive. Third, if cash flow at the vet is the deciding factor, ordinary Embrace claims use reimbursement, but an expected bill over $1,000 can be pre-certified and paid directly to an agreeing veterinary hospital. That is an optional advance arrangement, not routine real-time checkout adjudication.

One honest caveat colors the whole verdict: renewal increases. Embrace, like many carriers, can reprice as a pet ages and underlying veterinary costs and approved rates change; individual owners report a wide range of renewal increases. Budget for a bill that grows, not a flat one. If that's a dealbreaker, the fine print below shows exactly where Embrace earns its keep and where it doesn't.

Who underwrites Embrace (and is it trustworthy)?

Short answer: the company on the marketing isn't the company holding the money. Embrace is the agency that administers your policy; the insurer that actually carries the risk and pays claims is American Modern Home Insurance Company (in Florida, American Southern Home Insurance Company, a company in the same American Modern group). That distinction matters, because a policy is only as reliable as the balance sheet behind it.

On that score, the news is good. The two disclosed issuing companies sit in American Modern Insurance Group. The cited AM Best disclosure for that group lists an A+ (Superior) Financial Strength Rating, affirmed in July 2025. The declaration-page insurer controls; a group rating should not be relabeled as a rating of the Embrace agency itself. This is arguably the single most reassuring fact about Embrace, and it's the one most star-rating reviews skip entirely.

Ownership is worth knowing too. In late 2023, the Embrace brand was acquired by JAB Holding Company for about $1.5 billion. As of June 29, 2026, it is part of JAB’s Doubtless pet-care platform, the successor branding for the shared portfolio that includes Pets Best, Figo, and Spot. Shared ownership does not make the products or issuing entities identical. The underwriting paper remains the declaration-page American Modern entity; the owner of the brand is not the insurer holding the policy risk.

What Embrace costs — and why your renewal will rise

There's no single "Embrace price." Your premium is built from your pet's species, breed, age, and ZIP code, plus the deductible, reimbursement rate, and annual limit you pick. Embrace's own guidance puts most dog owners at $20 to $70 a month and cat owners at $10 to $30, and those ranges are not a matched market comparison. In one third-party 2026 sample, a medium mixed-breed dog on a $250 deductible / 80% / $5,000 plan ran about $39 a month at age 2 and $69 by age 8; a domestic shorthair cat ran roughly $19 to $35.

How does that stack up? The latest industry benchmark from NAPHIA puts the average U.S. accident-and-illness premium at about $69.67 a month for dogs and $32 for cats (2025 data). That national figure is a context benchmark, not evidence that Embrace sits above or below another carrier for a particular pet.

Here's the part the sales page doesn't lead with: your premium won't hold. Embrace can change rates as your pet ages and as veterinary costs and approved rates change — and owners on Reddit report jumps of 33%, 65%, even 84% at a single renewal, sometimes with no claims filed. You can soften the blow by raising your deductible, lowering your reimbursement rate, insuring multiple pets, or staying claim-free to earn the Healthy Pet discount — but plan for a bill that grows, not one that stays put.

How Embrace pays: deductible, reimbursement & the Healthy Pet Deductible

This is where Embrace is worth decoding, because two of its mechanics work differently from carriers you may have used before. Three choices set your plan, and you pick all three at enrollment:

| Your choice | Options Embrace offers |

|---|---|

| Annual deductible | $200 to $1,000 |

| Reimbursement rate | 70%, 80%, or 90% |

| Annual payout limit | $2,000 up to unlimited |

The detail that matters most: Embrace's deductible is annual, not per-incident — you meet it once per policy year, no matter how many times your pet sees the vet. Say you pick a $500 deductible and your dog tears a knee in March, then needs an unrelated stomach surgery in September; you satisfy that $500 once for the whole year. On a per-incident plan, each new condition can reset the deductible from scratch — the trap that burns a lot of switchers. After the deductible is met, Embrace reimburses your chosen 70%, 80%, or 90% of covered costs, up to your annual limit. (Deductible and limit options live on Embrace's dog and cat plan pages.)

The Healthy Pet Deductible: real perk, real small print

Embrace's signature twist is the Healthy Pet Deductible: for every policy year you don't receive a claim reimbursement, your annual deductible drops by $50, at no extra charge, until it can reach $0. A $500 deductible falls to $450 after one claim-free year and, in principle, to $0 after ten. But read the catch: it rewards exactly one thing — staying claim-free — so it helps the young and the lucky far more than the pet who actually uses the policy, and a $50 reduction is easily swallowed by a renewal increase that adds far more than that.

One moving piece to confirm: Embrace is shifting this benefit to a Healthy Pet Premium Discount — roughly 5% off in your first qualifying low-claim year and 10% in the second — and rolling it out state by state. So whether a brand-new policy gives you the shrinking deductible or the premium discount depends on where you live. Check which one applies to you before you count on the $50-a-year math.

Waiting periods & pre-existing conditions

Waiting periods are the gap between when your policy starts and when coverage actually kicks in. Embrace's are competitive: accident coverage begins on the policy effective date with no additional accident wait in current published materials, while illness has a 14-day wait. Ignore any older review that cites a "48-hour" accident wait — that figure is outdated. Orthopedic timing is state-specific: for dogs, listed conditions such as cruciate-ligament tears, hip dysplasia, and IVDD can carry a 180-day exclusion period in common dog forms, but timing varies by state. Where the applicable state form permits it, you may be able to reduce the period to as few as 14 days by having your vet complete Embrace's Orthopedic Report Card exam within your first two weeks — but only if the exam turns up no orthopedic signs, since any abnormality found can still be treated as pre-existing. Some states and policy versions do not offer the reduction, so use the issued form and written confirmation rather than a national shorthand.

Pre-existing conditions: what "curable" actually buys you

Here's the distinction that trips up switchers: Embrace will sell a policy for almost any pet, but it won't cover a condition that showed signs or got treatment before your coverage (or waiting periods) began. Embrace reviews your pet's medical records from the 12 months before enrollment to draw that line.

Where Embrace is more generous than many carriers is curable conditions. If a one-off problem — an ear infection, a bout of diarrhea — stays symptom-free and treatment-free for 12 straight months, Embrace may cover it if it comes back. Incurable conditions (cancer, diabetes, allergies, most orthopedic issues) stay excluded for good. And watch the bilateral rule: if one knee or hip was affected before coverage, the other side is treated as pre-existing too. None of this is a reason to delay a vet visit — get your pet the care they need; just know that what ends up in the records shapes what's covered.

What's covered, what's not, and the rider surprises

Embrace's accident-and-illness plan is broad — but two everyday costs sit outside the base plan, and that's where new customers get blindsided. Vet exam fees (the "office visit" charge) and prescription medications are optional add-ons, not automatic. Skip them, and a claim that includes the exam fee comes back partly denied — a common, avoidable surprise. Decide up front whether you want them.

On the plus side, the base plan covers more than many rivals: dental illness such as gum disease and extractions (up to a $1,000 annual sub-limit; routine cleanings aren't covered), plus hereditary and congenital conditions — hip dysplasia, IVDD, and the like — as long as they aren't pre-existing.

Wellness Rewards is Embrace's routine-care add-on, and it's worth understanding for what it is: not insurance, but a flat annual allowance you spend down on vaccines, exams, dental cleanings, and flea and tick prevention. You pick a $300, $500, or $700 tier (plus a $25 bonus) and get reimbursed against receipts, with no deductible. The honest math: the yearly cost lands close to the allowance itself, so it roughly breaks even — it pays off only if you reliably use the whole budget each year. (It's also not offered in Rhode Island.)

One enrollment note: a pet can be newly enrolled in full accident-and-illness coverage up to age 14; a pet first signed up at 15 or older is limited to the accident-only plan. A pet already covered before 15 keeps its accident-and-illness policy at renewal.

How to file an Embrace claim (and how fast you get paid)

The switcher's real question isn't "can I file a claim?" — it's "will I actually get paid, and how fast?" Here's how it works. The easiest route needs no paperwork at all: you submit through your online MyEmbrace account or the mobile app, uploading an itemized invoice from your vet. If you'd rather use the Embrace pet insurance claim form, you'll find it inside your account and attach it when you submit by email, fax, or mail instead.

Two things to know before your first claim. First, ordinary claims reimburse you after payment. For a likely bill over $1,000, Embrace offers optional pre-certification and may pay the veterinary hospital directly when the hospital agrees beforehand; the company says pre-certification typically takes five business days or less. This is not a general or real-time direct-pay network. Second, your first claim triggers a medical-history review: Embrace pulls your pet's records from the 12 months before enrollment to confirm nothing was pre-existing, which is why the first claim takes longer than the ones after it.

On speed, Embrace says most claims are handled in about 10 to 15 business days, with reimbursement by direct deposit (a few business days) or a mailed check. Reality varies: some owners on Reddit report a first claim paid the same day, while others describe weeks of back-and-forth over records. The pattern is consistent — clean, complete documentation and a finished medical-history review are what turn a slow claim into a fast one.

Embrace vs Lemonade: which should you pick?

Embrace and Lemonade are the two carriers first-time buyers most often weigh against each other, and they're built differently: Embrace is a traditional, coverage-deep plan on a strong underwriter; Lemonade is an app-first insurtech with a different configuration and claims flow. Here's how they line up (the Embrace figures are detailed in the sections above):

| Feature | Embrace | Lemonade |

|---|---|---|

| Reimbursement | 70%, 80%, 90% | 70%, 80%, 90% |

| Annual deductible | $200–$1,000 | $100–$750 (caps at $750) |

| Annual payout limit | $2,000 to unlimited | $5,000–$100,000 (no unlimited) |

| Waiting periods | 0-day accident after effectiveness; 14-day illness; state-specific dog orthopedic timing and waiver eligibility | 0-day accident, 14-day illness, 30-day orthopedic |

| Claims | Reimbursement, ~10–15 business days | AI app, many claims paid in minutes to days |

| Enroll up to | Age 14 (then accident-only) | ~Age 14 |

| Price comparison | Matched quote required | Matched quote required |

What the differences mean depends on your pet. If you're insuring a clean-record young pet and price is the priority, run matched quotes; neither carrier has a defensible universal price or claims-speed advantage for every profile. If you have a large-breed dog, watch the orthopedic gap — Lemonade currently publishes a 30-day orthopedic wait, while Embrace timing and exam-reduction eligibility vary by state; compare issued forms rather than treating six months as national. If you're a switcher chasing a lower renewal, know that both carriers can reprice at renewal — an app-first sales and claims interface is not proof of a universally cheaper entry price or faster result on every claim. And if you want the deepest coverage — an unlimited annual limit, dental illness in the base plan, the applicable Healthy Pet discount or legacy deductible program — Embrace offers a different benefit mix, backed by an A+ underwriter. For a fuller side-by-side across more carriers, see our pet insurance comparison hub.

Is USAA pet insurance the same as Embrace?

USAA offers members an Embrace-administered pet-insurance program; Embrace’s current disclosure identifies American Modern Home Insurance Company, or American Southern Home Insurance Company in Florida, as the possible issuing entities. The declaration page controls. That establishes the administrator and possible insurer, not universal term-for-term equivalence with every direct Embrace policy. Compare the USAA quote, sample form, benefit options, discounts, and issued declarations with the direct channel before assuming they match.

The one real difference is a member discount. USAA members typically get a percentage off the base Embrace premium — but how much varies by state and can change: California members, for example, reported on Reddit their discount cut sharply at a recent renewal. So treat any quoted discount as something to confirm at the point of sale, not a fixed number. The practical takeaway: if you're a USAA member, you're considering an Embrace-administered program — judge the issued terms on their own merits, and confirm the member discount before you commit.

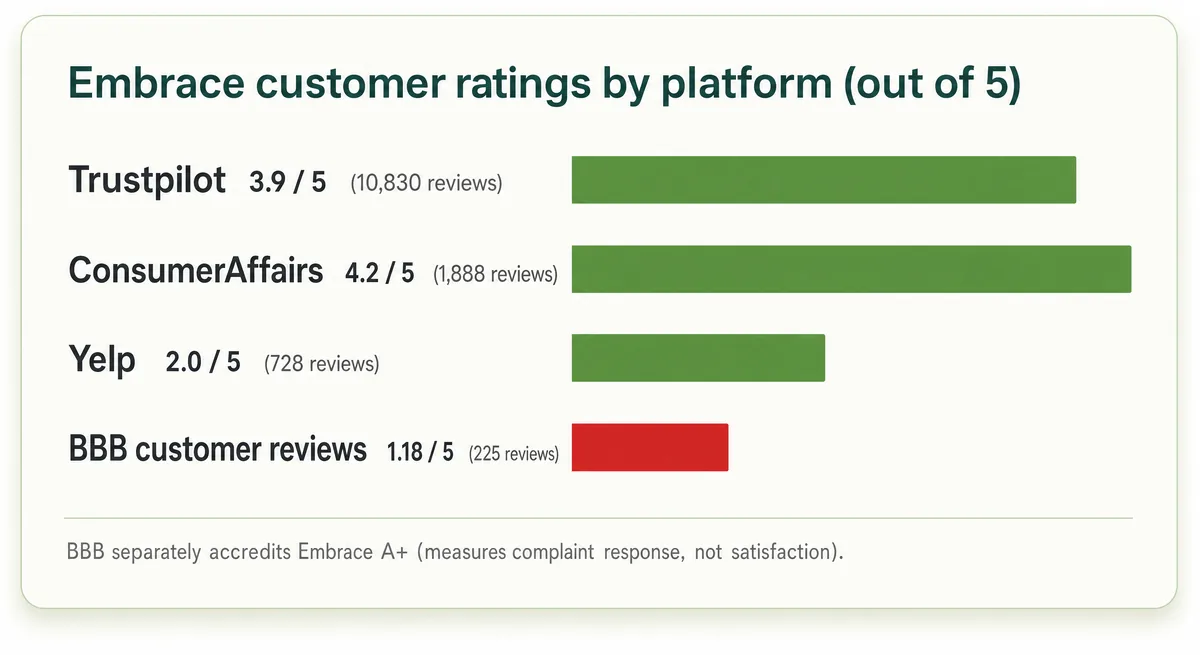

What real customers say

Embrace's reviews come with a genuine puzzle: the same company scores wildly differently depending on where you look. It holds a 3.9 out of 5 on Trustpilot across more than 10,000 reviews and 4.2 on ConsumerAffairs, yet just 2.0 on Yelp and a striking 1.18 out of 5 on the Better Business Bureau — where, confusingly, Embrace is also accredited with an A+.

That A+ isn't a satisfaction score. The BBB letter grade measures whether a business responds to complaints, not whether customers are happy — which is how it can sit right beside a 1.18 average. Read the platforms together and a consistent pattern emerges.

What owners praise (on Trustpilot and Reddit): fast, denial-free payouts when they enrolled a pet early — several describe cancer or major-surgery claims reimbursed by direct deposit within days — plus the 24/7 PawSupport vet line.

What owners complain about (on the BBB, Yelp, and Reddit): renewal rate increases, by a wide margin the loudest grievance; claims denied over pre-existing conditions; and long phone hold times. The through-line is that Embrace tends to satisfy owners who got in early and stay claim-light, and frustrate those hit by a big renewal jump or a pre-existing dispute. Treat all of this as aggregated sentiment, not a verdict on how your specific claim will go.

Frequently Asked Questions

Is Embrace Pet Insurance any good?

Yes, for the right owner. Embrace's current underwriting disclosure identifies American Modern Home Insurance Company, or American Southern Home Insurance Company in Florida; the American Modern group AM Best disclosure lists A+ (Superior); declarations control. Embrace offers broad issued benefits for eligible conditions, but claim outcomes still depend on the records and contract. It's a weaker fit if you're shopping purely on price or insuring an older pet with a medical history, and renewal repricing is a recurring complaint in the cited owner reports.

Do most vets accept Embrace Pet Insurance?

Any licensed vet works. Embrace has no provider network, so you can see any licensed U.S. veterinarian, pay the bill, and submit for reimbursement afterward. Your vet doesn't need any relationship with Embrace, and there's no in-network or out-of-network distinction. Ordinary claims reimburse you after payment. Optional pre-certification for an expected bill over $1,000 may let Embrace pay an agreeing hospital directly when arranged beforehand; it is not real-time checkout adjudication.

What does Embrace not cover?

Pre-existing conditions are the big exclusion. Embrace also won't cover elective or cosmetic procedures, breeding and pregnancy, or routine and preventive care unless you add the Wellness Rewards plan. Vet exam fees and prescription medications aren't in the base plan either — they're optional riders you have to select. Incurable pre-existing conditions stay excluded for life, though some curable ones can regain coverage.

Which is better, Embrace or Trupanion?

It depends on what you value. Trupanion can pay your vet directly at checkout and uses a per-condition deductible, which suits owners of a pet with one big chronic condition. Embrace uses an annual deductible, includes dental illness in the base plan, and offers an optional wellness allowance. Its ordinary claims reimburse after payment, while optional pre-certification can support direct hospital payment for an expected bill over $1,000 if the hospital agrees. Trupanion has the broader real-time participating-clinic mechanism; compare forms and clinic participation. Our Trupanion review has the full picture.

How long does Embrace take to pay a claim?

Usually about 10 to 15 business days. Embrace processes most claims in that window, with reimbursement by direct deposit or mailed check. Your very first claim takes longer because Embrace reviews your pet's medical history to check for pre-existing conditions. Owners report a wide range in practice — some paid the same day, others waiting weeks — and complete documentation is what speeds it up.

Does Embrace cover pre-existing conditions?

Not incurable ones, but curable conditions can come back into coverage. Embrace permanently excludes chronic or incurable pre-existing conditions like cancer, diabetes, and most orthopedic issues. A curable condition — say an ear infection — may become eligible again if your pet stays symptom-free and treatment-free for 12 consecutive months. Embrace uses your pet's medical records to decide what counts as pre-existing.

Is Embrace's Healthy Pet Deductible still available?

It depends on your state. The Healthy Pet Deductible — which drops your deductible $50 for each claim-free year — is being replaced by a Healthy Pet Premium Discount, rolled out state by state. Depending on where you live, a new policy may give you the shrinking deductible or the premium discount instead. Confirm which one applies before you count on the $50-a-year benefit.

Sources

- Coverage FAQ — Embrace Pet Insurance

- What does Embrace offer in terms of dental illness coverage? — Embrace Pet Insurance

- Wellness Rewards — Embrace Pet Insurance

- Pet Insurance Deductible, Explained — Lemonade

- Demystifying Pet Insurance Coverages — Lemonade

- Pet Insurance Waiting Periods — Lemonade

- USAA Pet Insurance — U.S. News & World Report

- Anyone with Embrace through USAA based in California? (r/petinsurancereviews) — Reddit

- Embrace Pet Insurance Reviews — Trustpilot

- Embrace Pet Insurance Reviews — ConsumerAffairs

- Embrace Pet Insurance — Yelp

- Embrace Pet Insurance — BBB Customer Reviews — Better Business Bureau

- Dog Insurance — Embrace Pet Insurance

- What is the Healthy Pet Deductible? — Embrace Pet Insurance

- Waiting Periods — Embrace Pet Insurance

- What is the waiting period for orthopedic conditions? — Embrace Pet Insurance

- Pre-existing Conditions — Embrace Pet Insurance

- What is the reimbursement process for Embrace claims? — Embrace Pet Insurance

- Claims — Embrace Pet Insurance

- My First Embrace Claim (r/petinsurancereviews) — Reddit

- Why did my premium change? — Embrace Pet Insurance

- How much does pet insurance cost? — Embrace Pet Insurance

- Embrace Pet Insurance Review 2026 — NerdWallet

- State of the Industry Report 2025 (2024 data) — NAPHIA

- My Embrace Pet Insurance renewal is increasing by 84%? (r/petinsurancereviews) — Reddit

- Underwriting — Embrace Pet Insurance

- American Modern Home Insurance Company — Credit Rating Disclosure (AMB #003031) — AM Best

- JAB acquires Embrace Pet Insurance for $1.5 billion — Coverager

- Doubtless Pet Care launches as JAB’s renamed pet-care platform — Business Wire

- State of the Industry Report 2026 Highlights (2025 data) — NAPHIA

- Optional pre-certification and direct hospital payment — Embrace Pet Insurance