Figo is one of the cheaper pet insurance quotes you'll see, and it dangles something most insurers won't: a 100% reimbursement option that wipes out co-insurance entirely. So is it the smart-value pick, or is it cheap for a reason? A licensed insurance agent's answer is that it depends on your pet and your paperwork.

For a young dog or cat with a clean medical record — an owner who wants full reimbursement and values a free 24/7 vet chat line — Figo is a genuinely strong-value plan. For the owner of a cancer- or orthopedic-prone breed who could blow through a low annual cap, or anyone with gaps in their vet records, it can be the wrong call.

We read Figo's actual policy booklets — for more than one state — so you don't have to, and two things jumped out that a spec-sheet review won't tell you. First, the cheapest Figo plan's low annual limit can run out in a single bad year, so "cheap" quietly caps your protection. Second, the fine print that matters most — your accident wait, whether a torn knee ligament is covered early, the bilateral rule — depends on which policy form your state uses, not on one nationwide Figo rule. Below is the whole honest tour: the plans and the 100% catch, the state-by-state waiting periods, why claims get denied on an avoidable mechanism, and exactly who should skip it.

Table of Contents

- Verdict: Who Figo Fits, and Who Should Skip It

- Figo at a Glance: Plans, Dials & Price

- Waiting Periods & the Fine Print That Depends on Your State

- Why Figo Claims Get Denied (and How to Avoid It)

- What Figo Really Costs Over Time (the Cheap-but-Capped Trap)

- Who Underwrites Figo, and Is It Stable?

- Figo Through Costco

- Figo vs. the Competition

- How We Reviewed Figo

- Frequently Asked Questions

- Sources

Verdict: Who Figo Fits, and Who Should Skip It

There's no single star score that fits every reader, so here's the honest version: Figo is a strong-value plan for the right pet and a quietly risky one for the wrong pet. Which one you are comes down to three things — how much of a big vet bill you can front, how prone your breed is to expensive conditions, and how clean your pet's medical records are.

Figo is a good fit if:

- You have a young dog or cat with a clean vet history and want to lock in coverage before anything can be called "pre-existing."

- You want to eliminate co-insurance — Figo is one of the few insurers offering a 100% reimbursement option, so a covered claim reimburses 100% of your eligible costs after the deductible, instead of leaving you a 10–30% co-insurance share.

- You'd actually use a free, unlimited 24/7 telehealth line for the 2 a.m. "is this an emergency?" moments.

- You can comfortably front a large bill and wait to be paid back — Figo reimburses you, not the vet directly.

Think twice, or skip Figo, if:

- You own a cancer- or orthopedic-prone breed — a Golden Retriever, German Shepherd, or other large dog — and would buy the cheapest tier, whose $5,000 annual cap can be swallowed by a single cancer or two-knee year, leaving the rest on you.

- Your pet's records have gaps or unexplained symptoms — Figo reviews two years of vet notes at your first claim, and anything that reads as pre-existing gets excluded.

- You need the insurer to pay your vet directly at checkout; Figo is reimbursement-only.

None of this makes Figo a scam or a slam dunk. It's a genuinely cheap, tech-forward plan whose value depends entirely on matching the right tier to your pet — and the rest of this review shows you exactly how to do that.

Figo at a Glance: Plans, Dials & Price

Figo sells a single accident-and-illness plan, and you shape it with three dials: your annual deductible, your reimbursement rate, and your annual payout limit. Set those three for your pet and budget and you've essentially built your policy.

The payout limit comes in three tiers — Figo brands them Essential, Preferred, and Ultimate:

| Plan tier | Annual payout limit | Who it tends to suit |

|---|---|---|

| Essential | $5,000 | Lowest premium; young, lower-risk pets |

| Preferred | $10,000 | A middle ground for most owners |

| Ultimate | Unlimited | Expensive or large breeds with real catastrophe risk |

On top of the tier you pick a deductible from $100 to $750 (older pets may only see higher $1,000–$1,500 options) and a reimbursement rate of 70%, 80%, 90%, or 100%. A lower deductible and a higher reimbursement rate both push the premium up — the usual insurance trade-off.

What does that cost? In NerdWallet's May 2026 quote test — a $250 deductible, 80% reimbursement, and the $5,000 limit, priced in Katy, Texas — a Golden Retriever ran about $39 a month at age 2 and $92 by age 8; a French Bulldog ran roughly $61 rising to $144 over the same span. Treat these as dated examples, not a quote — your real price turns on your pet's age, breed, ZIP code, and the dials above.

The 100% Reimbursement Option (and Its Catch)

Most insurers cap reimbursement at 90%, leaving you a "co-insurance" share of every covered bill — on an $8,000 surgery at 80%, that's $1,600 out of pocket even after your deductible is met. Figo is one of the few carriers offering 100% reimbursement, which erases that share entirely. It's a genuine draw for anyone who wants a covered claim to pay back the whole bill.

The catch: 100% reimbursement is available only with a $500 or $750 deductible and, per independent comparisons, can't be combined with the Unlimited limit — it pairs only with the $5,000 or $10,000 caps. Figo doesn't spell this rule out on its plan page, so confirm the exact combinations on your own quote. If it holds, the owner who most wants unlimited protection can't also have zero co-insurance — you pick one or the other.

Live Vet & Powerups

Every Figo policy includes Live Vet — free, unlimited 24/7 telehealth through the Pet Cloud app, a real perk for the late-night "is this an emergency?" question. One honest caveat: Figo staffs it with "veterinary professionals" who cannot prescribe medication, so treat it as triage, not a substitute for a clinic visit.

Two things buyers often assume are built in but aren't. Vet exam fees — the office-visit charge on an accident or illness visit — require a paid "Veterinary Exam Fees" Powerup, and routine or wellness care needs a separate Wellness Powerup. Figo's own site lists exam fees inside its coverage section, which can read as included — confirm the add-on is on your quote before you count on it.

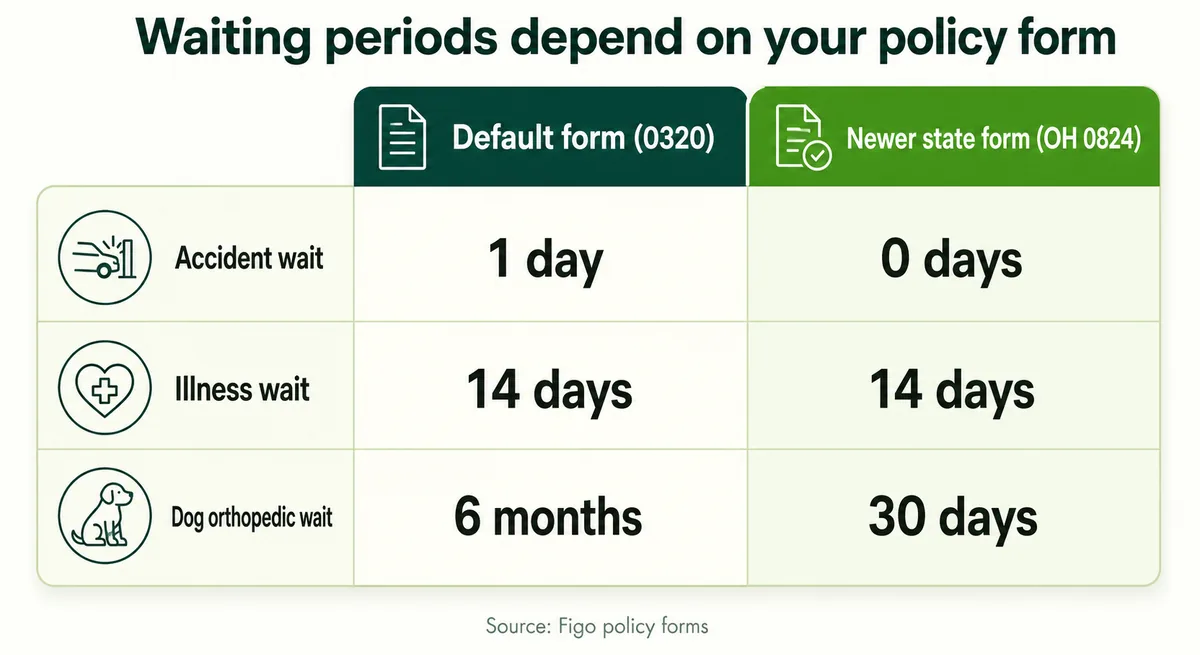

Waiting Periods & the Fine Print That Depends on Your State

Here's the single most important thing no spec-sheet review tells you: Figo doesn't have one nationwide waiting period. Your accident wait, your dog's orthopedic wait, and whether a torn knee ligament is covered early all depend on which policy form your state uses — and you can tell which one governs by the form number printed on your declarations page.

Figo runs two form generations. The older default form (IAIC FPI POL 0320) is still the current sample in states that haven't reformed. Newer state forms — confirmed in Ohio, Nebraska, and Washington — soften several of the waits. Don't infer your terms from the state on the form, though: read the actual waiting-period section of your own declarations page and policy booklet, since only these three are confirmed here.

| Provision | Default form (IAIC FPI POL 0320) | Newer state forms (e.g. OH 0824) |

|---|---|---|

| Accident (injury) wait | 1 day | 0 days |

| Illness wait | 14 days | 14 days |

| Dog orthopedic wait | 6 months | 30 days |

| Torn cruciate (CCL) | Routed into the 6-month orthopedic wait | Treated as a 30-day orthopedic illness |

That last row is the trap. On the default form a cruciate tear is technically an "accident," but Figo routes orthopedic accidents into the 6-month wait — so a dog who blows a knee in month one is denied even though the 1-day accident wait cleared long ago. On a newer state form the same tear clears in 30 days. Cats face no special orthopedic wait on either form.

Figo also offers an Orthopedic Waiver Form that can waive the illness and orthopedic waits if your vet examines your pet and files the form within a short, form-specific deadline after your start date — check the exact window in your own policy, because missing it by a day forfeits the waiver. The catch: it screens for a 20-item list of disqualifying conditions — IVDD, ligament and knee issues, arthritis, cancer, and more — and anything flagged becomes a permanent exclusion. It helps a spotless pet and can quietly hurt a charted one.

Two more form-dependent rules matter for knees. The bilateral rule — where a problem in one knee makes the other side pre-existing — is only defined on the default form but made automatic "regardless of cause" on the newer ones. And the curable pre-existing window (the symptom-free stretch that can re-cover a healed condition) runs 12 months on the default form and 365 days on newer ones, but never applies to ligament and knee conditions on either. The takeaway is simple: pull your declarations page, read the form number, and match it to the table above before you assume anything about your waits.

Why Figo Claims Get Denied (and How to Avoid It)

The Figo complaints you'll read about usually trace to two knowable things: a paperwork gate you can clear, and a pre-existing review you can prepare for. Neither is random bad faith, and understanding both helps you sidestep the problems that fill the review sites.

Start with the paperwork. Figo is reimbursement-only — it pays you back, never your vet directly — and before it will process a claim it requires a paid invoice showing a $0 balance. Miss that and an approval can look like a denial: in one widely shared Reddit thread, $2,422 in claims came back "approved" for $9.20 over a missing zero-balance invoice — then paid out about $1,900 once the owner and vet fixed the documentation.

The bigger issue is pre-existing conditions. At your first claim — not at enrollment — Figo pulls roughly two years of your pet's medical records "including notes" and reads them for any sign or symptom that pre-dates your start date. Because the clause is symptom-based, something your vet merely jotted down before your coverage started — worms treated six months before the policy, say — can be read as pre-existing and excluded. Worth knowing: Figo's marketing FAQ mentions a 12-month records request while its policy forms can require 24 months, so gather your pet's full history rather than counting on the shorter figure.

None of this means Figo won't pay. It publishes a cancer case reimbursed over $25,000, and owners frequently report that a stuck claim gets resolved after they and their vet push back. If a claim is denied, your policy sets an appeal window — commonly 90 days — so act on the deadline printed in your denial notice. The honest move is records discipline, done early: before you file, ask your vet for a copy of your pet's full history, pre-load it into the Pet Cloud app, and confirm every invoice is marked paid. And never delay care to protect a claim — complete, current records are what get you reimbursed, not what sink you.

What Figo Really Costs Over Time (the Cheap-but-Capped Trap)

Figo often quotes below the industry average — and that cheapness is exactly what you have to watch, because the lowest tier caps what the policy will ever pay in a year. For reference, the 2024 NAPHIA benchmark put the average accident-and-illness dog policy at about $749 a year ($62 a month) and the average cat at $386 ($32 a month). A young, common-breed dog on Figo's $5,000 tier usually prices under that — but price climbs steeply with age: in NerdWallet's quote test, a Figo quote for an 8-year-old ran about 136% higher than for a 2-year-old. That's a snapshot of new-business pricing, not a guaranteed renewal path, but it shows the direction your premium heads.

Here's where "cheap" bites. A serious dog-cancer year — surgery, chemotherapy, and radiation — realistically runs $10,000 to $25,000. On Figo's $5,000 Essential tier, the payout is hard-capped at $5,000 for the year no matter whether you chose 80% or 90% reimbursement. So a $15,000 bill that would reimburse $12,000 at 80% is cut to $5,000 — leaving about $10,000 on you. A plan with no annual limit would pay roughly $12,000 to $13,500 on that same bill.

Two smaller mechanics compound it. Figo charges a fresh deductible each policy period, so treatment that straddles your renewal — a chemo course that runs into a new plan year — triggers a second deductible. A diminishing deductible can trim $50 a year off that, but only while you stay claim-free; one paid claim resets it.

The honest steer: if you own a cancer- or orthopedic-prone breed, don't buy the cheapest cap. Step up your annual limit — the $10,000 tier sharply cuts the risk, and only the Unlimited tier removes the annual ceiling altogether (worth knowing, since the worst cancer years above can top $10,000 too). Just remember that Unlimited is the one limit that can't be paired with Figo's 100% reimbursement option: you choose maximum payout or zero co-insurance, not both.

Who Underwrites Figo, and Is It Stable?

The name on your declarations page isn't really "Figo." Figo is the brand and administrator — a managing general agent — while your actual insurer is Independence American Insurance Company (IAIC), which carries an A- (Excellent) rating from AM Best. IAIC sits inside Independence Pet Holdings, the JAB-backed group that also owns Pets Best, Embrace, ASPCA, and Pumpkin, among others; Figo itself joined the group when JAB acquired it in 2021.

That private-equity ownership is the thing owners flag most. On Reddit, "figo is private equity, avoid it" is a common refrain, driven by fear of renewal-price gouging as a pet ages. It's a fair worry to name — though in practice premium increases track your pet's age and the insurer's whole book, not ownership alone.

On financial strength, 2025 brought a genuine wobble worth knowing. In August, AM Best placed IAIC under review after its pet reinsurance failed a risk-transfer test; in December it affirmed the A- once the parent injected $125 million of fresh capital and the reinsurance was restructured. Translation: currently sound, but recently tested.

One thing we won't do is publish a single complaint-index number for Figo. The underwriting entity is shared across several sibling brands, so any figure at that level blends all of them and tells you little about Figo specifically. Judge its service on dated, brand-level reviews instead.

Figo Through Costco

If you've seen Costco Pet Insurance and wondered whether it's a different, weaker product, it isn't: Costco Pet Insurance is Figo-administered and underwritten by the same insurer, IAIC. You get Figo coverage from the same underwriter and administrator, so expect the same waiting periods and fine print rather than a stricter policy — though it's still worth comparing your actual quote and issued terms. The material difference is price.

Costco members get about 15% off the premium, and Executive members also have the first month and the $15 enrollment fee waived. It's a genuine discount on the exact same coverage, not a cheaper-but-stricter version.

Two caveats. The discount doesn't change Figo's age-based repricing — premiums still climb as your pet ages, and dogs 8 and older (cats 10 and older) can face geriatric-screening requirements at enrollment. And you'll need a Costco membership to qualify. Otherwise, if you were going to buy Figo anyway, the Costco route simply costs less — so it's worth pulling a quote both ways and taking whichever price is lower for your pet.

Figo vs. the Competition

Figo is almost never shopped alone — owners line it up against a short list of rivals, usually for a new puppy. The deciding factors come down to three: price, whether you want an unlimited annual limit, and whether Figo's 100% reimbursement option matters to you. Here's the quick read on the three names that come up most.

| Rival | How it stacks up against Figo | Leans better when… |

|---|---|---|

| Lemonade | Publicly traded (not private-equity owned), app-first, and tends to cap its annual limits rather than offer a true unlimited tier; often a lower headline price | You want a low price and a slick app, and don't need unlimited coverage |

| Pets Best | Frequently cheaper than Figo — and, like Figo, an Independence Pet Holdings sibling | You want Figo-style coverage at a lower price from the same group |

| ASPCA | Also an IPH sibling; a familiar-name, annual-limit product | You value a well-known brand with straightforward annual-limit plans |

One thing worth knowing: two of those "competitors" — Pets Best and ASPCA — sit under the same Independence Pet Holdings parent as Figo, so switching between them won't escape the private-equity ownership concern some owners raise. The genuine differentiators stay Figo's own: the 100% reimbursement option and the state-by-state fine print covered above. For side-by-side numbers on any of these match-ups, see our pet insurance comparisons, or browse the full lineup of single-brand pet insurance reviews.

How We Reviewed Figo

This review leans on primary documents wherever the stakes are highest. We read Figo's actual binding policy forms — both the default edition and newer state forms — along with the underwriter's AM Best rating filings and NAPHIA's industry cost benchmarks, and we cross-checked pricing and plan features against third-party reviews. Every price, waiting period, and rule above is dated and linked to its source.

For real-world experience, we synthesized labelled voice-of-customer from the BBB, Trustpilot, the app stores, and Reddit — treating it as sentiment, not incidence data, since owners with a claim story tend to post more often than those without one. Where a figure couldn't be verified against a primary source, we left it out. You can read more about how we evaluate insurers on our methodology page.

Frequently Asked Questions

Is Figo pet insurance good, and is it worth it?

For the right pet, yes. Figo is a strong-value plan if you have a young, healthy dog or cat and want full (100%) reimbursement plus a free 24/7 telehealth line. It's a weaker fit if you'd buy the cheapest $5,000-capped tier for a cancer- or orthopedic-prone breed, or if your pet's vet records have gaps. It's above-average on technology and price — not a scam, but not flawless either.

Does Figo pay my vet directly, or do I get reimbursed?

Figo is reimbursement-only — you pay the clinic, then submit a paid invoice showing a $0 balance and Figo pays you back, typically within 30 days of complete documentation. There's no direct-to-vet payment, so you'll need to front the bill and wait to be reimbursed.

How long is Figo's waiting period?

It depends on your state's policy form. On the older default form, accidents have a 1-day wait and dog orthopedic conditions a 6-month wait; on newer state forms, accidents have no wait and orthopedic conditions a 30-day wait. Illness is 14 days either way. Check the form number on your declarations page.

Does Figo cover cruciate (CCL) ligament surgery?

Yes, though the timing depends on your form. On the default form a torn cruciate is called an "accident" but routed into the 6-month orthopedic wait, so a month-one tear is denied; newer state forms handle it as a 30-day orthopedic illness. Newer forms also treat both knees as one bilateral condition, so a problem in one can make the other pre-existing.

Is Figo cheaper through Costco?

Yes. Costco Pet Insurance is the same Figo product, underwritten by the same insurer, at about 15% off for members — Executive members also get the first month and the $15 enrollment fee waived. It's a discount on identical coverage, not a stricter policy, though you'll need a Costco membership to buy it.

Figo vs. Lemonade — which is better?

It depends on what you value. Lemonade is often a little cheaper, app-first, and publicly traded rather than private-equity owned — but it tends to cap its annual limits, while Figo offers a true Unlimited tier and a 100% reimbursement option Lemonade doesn't. Pick Lemonade for price and simplicity, Figo for a higher payout ceiling.

Is Figo the same as ASPCA pet insurance?

Not the same, but closely related: both Figo and ASPCA sit under the same parent, Independence Pet Holdings, so the ownership-and-renewal concerns some owners raise apply to both. ASPCA is a familiar, annual-limit brand; Figo stands out with its 100% reimbursement option and free Live Vet line. Compare a quote from each before deciding.

Can I enroll a senior pet — is there an upper age limit?

Figo doesn't set a hard upper age limit, so you can enroll an older pet. But dogs 8 and older and cats 10 and older may need a veterinary exam or geriatric screening to enroll, and premiums for senior pets run meaningfully higher. Enrolling before any signs or symptoms appear reduces the pre-existing-condition risk, though waiting periods and the usual policy terms still apply.

Sources

- Dog Insurance Plans (100% reimbursement option, limits) — Figo Pet Insurance

- Pet Cloud & Live Vet (free 24/7 telehealth) — Figo Pet Insurance

- Figo Pet Insurance Review (plan tiers, quote grid, Powerups) — NerdWallet

- Figo Pet Insurance (100% reimbursement restriction) — PetInsuranceQuotes

- Figo Sample Policy (Dog), default form IAIC FPI POL 0320 — Figo Pet Insurance / IAIC

- Figo Ohio Policy, form IAIC FPI POL OH 0824 (eff. 08/01/2024) — Figo Pet Insurance / IAIC

- Figo Nebraska Insurer Disclosure of Important Policy Provisions — Figo Pet Insurance / IAIC

- Figo Washington Insurer Disclosure of Important Policy Provisions — Figo Pet Insurance / IAIC

- Figo Waiting Period Waiver Form (IAIC FPI WP-WAIVER) — Figo Pet Insurance / IAIC

- Figo's Ultimate Guide to Claims (reimbursement-only, paid invoice, appeals) — Figo Pet Insurance

- "FIGO IS A SCAM" — zero-balance-invoice denial, ~$1,900 paid after appeal (VOC) — Reddit r/petinsurancereviews

- Figo Medical Records FAQ (records look-back) — Figo Pet Insurance

- Support Through a Pet Cancer Diagnosis (large claim reimbursed, Figo-published VOC) — Figo Pet Insurance

- State of the Industry 2025 (2024 average premiums) — NAPHIA

- Dog Chemotherapy Cost: How Much Is Dog Cancer Treatment — Embrace Pet Insurance

- Pet Insurance Coverage & Exclusions (no-annual-payout-limit plan) — Healthy Paws

- Carrier / Underwriter Information (Figo is an MGA; IAIC underwrites) — Figo Pet Insurance

- AM Best affirms IAIC A- (Excellent), $125M capital contribution (2025-12-17) — AM Best

- AM Best places IAIC under review with developing implications (2025-08-06) — AM Best / Business Wire (via Morningstar)

- Independence Pet Holdings (parent group & sibling brands) — Independence Pet Holdings

- "Stuck between choosing Figo and Lemonade" — private-equity ownership distrust (VOC) — Reddit r/petinsurancereviews

- Costco Pet Insurance Review (Figo-administered, IAIC-underwritten) — U.S. News

- Costco Pet Insurance (Figo, 15% member discount, age screening) — Pawlicy Advisor