The American Kennel Club doesn't insure your pet. "AKC Pet Insurance" is a brand name the club licenses to a company called PetPartners; the insurer whose name actually appears on your policy is Independence American Insurance Company, or its sister carrier, Independence Pet Insurance Company. That distinction matters more than any star rating, because it decides who reads and pays your claims — and it's the first thing most reviews skip right past.

If you landed here, you probably own a purebred or a registered dog, you trust the AKC name, and you want one honest answer: will this plan actually cover the hip dysplasia, heart condition, or other inherited problem your breed is prone to? That is the question we built this review around, because for this brand's audience it's the one that counts.

We read AKC's actual policy documents so you don't have to — the waiting periods, the pre-existing rules, the fine print on hereditary conditions, and the add-ons that quietly cost extra. Below you'll get the verdict up front (who this fits and who should skip it), the truth about who underwrites it, exactly what's covered versus what's a paid rider, real 2026 pricing against the national average, and a straight read on whether AKC actually pays.

Table of Contents

- The Verdict: Who AKC Pet Insurance Fits — and Who Should Skip It

- Who Actually Underwrites AKC Pet Insurance?

- Plans, Riders, and What's Actually Covered

- Does AKC Cover Your Purebred's Hereditary Conditions?

- Waiting Periods and the 365-Day Pre-Existing Rule

- Cost: Real Quotes vs. the National Average

- Does It Pay? Claims and Complaints

- The 30-Day Free Trial and the Breeder Channel

- AKC vs. the Main Alternatives

- Frequently Asked Questions

- Sources

The Verdict: Who AKC Pet Insurance Fits — and Who Should Skip It

AKC Pet Insurance is a legitimate, financially solid plan — but whether it's a good buy comes down to two decisions you make at enrollment, not the AKC badge itself. Get them right and it's a strong pick for a purebred owner. Get them wrong and it's an ordinary plan wearing a familiar name.

It's a good fit if:

- You own a purebred or registered dog, you're enrolling while it's under two years old, and you'll add the HereditaryPlus rider — the only way this plan covers the inherited conditions most people buy the brand for.

- Your pet already has a health issue and you can keep coverage in force for a full year. AKC is one of the few carriers where a pre-existing condition may become eligible after 365 days of continuous coverage.

- You're a breeder who wants the registration perks and the optional breeding coverage.

Look elsewhere if:

- Your dog is already two or older and you need hereditary coverage — the rider is usually off the table by then, and the exact cutoff varies by state.

- You'd choose the cheapest "Basic" tier, whose $500 lifetime per-incident cap makes it nearly useless for anything serious or recurring.

- You just want the simplest, lowest-price plan. The headline price is competitive, but the coverage that matters here lives in paid add-ons.

Every one of those calls hinges on the plan and riders you pick, not the AKC name. The rest of this review shows you exactly how to make them.

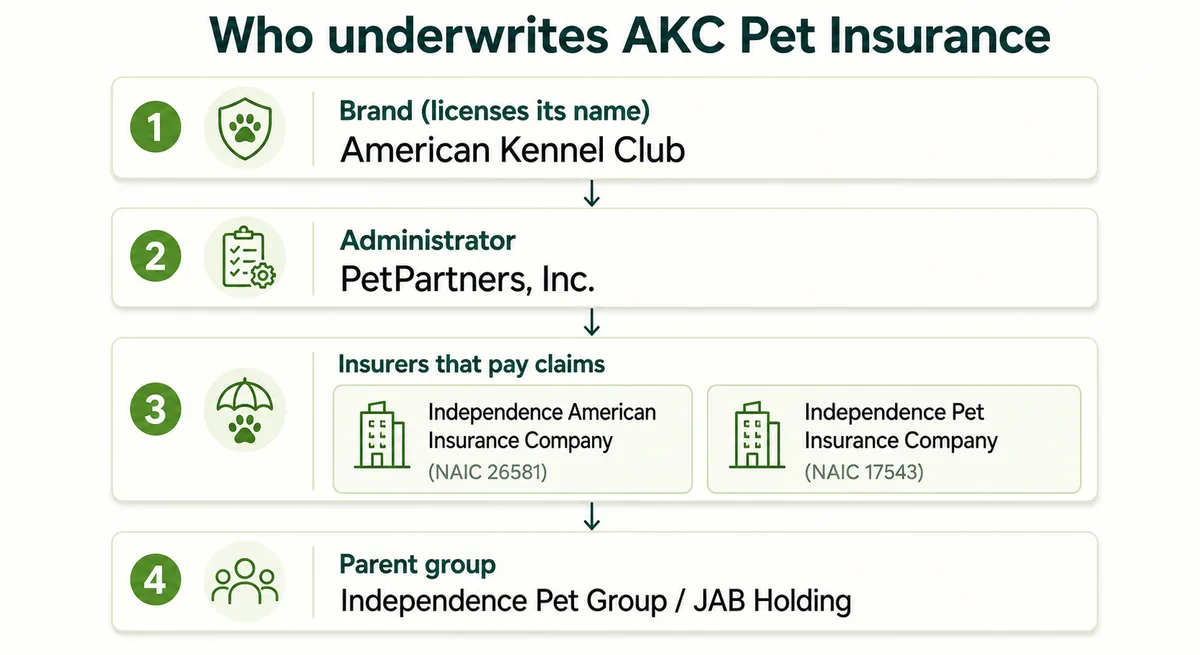

Who Actually Underwrites AKC Pet Insurance?

The American Kennel Club does not underwrite, sell, or pay claims on AKC Pet Insurance — it licenses its name for a royalty. Three separate companies actually run the product, and knowing which is which tells you who you're really trusting with a claim:

- The brand (licensor): the American Kennel Club. It lends its name and its reach to registered-dog owners — and nothing more.

- The administrator: PetPartners, Inc. (National Producer Number #7612549), based in Raleigh, North Carolina. This is the agency that sells your policy and services your account.

- The insurer that actually pays: Independence American Insurance Company (NAIC #26581), or its sister carrier, Independence Pet Insurance Company (NAIC #17543). One of these — not the AKC — is the risk-bearing company named on your policy.

Both carriers sit under Independence Pet Group, ultimately controlled by the private-equity firm JAB Holding — a large pet-insurance group, not a standalone kennel-club operation. And since the policy can be issued by either of the two carriers above, it's worth checking which one is named on your own declarations page.

Financial strength and the 2025 rating event

On paper the carrier is solid: Independence American holds an AM Best rating of A- (Excellent) with a stable outlook. But there's a wrinkle most reviews skip. In August 2025, AM Best placed the carrier "under review with developing implications" over a reinsurance and annual-statement issue, then reaffirmed the A- in December 2025 — only after its parent added a $125 million capital contribution. It resolved well, but a lifetime commitment deserves that context.

One more caveat: that A- belongs to Independence American specifically. Its sister carrier, Independence Pet Insurance Company, doesn't share that published rating — so if that entity is the one named on your policy, don't assume the same grade.

Plans, Riders, and What's Actually Covered

AKC's headline price buys a fairly narrow base plan. A lot of what owners assume is "covered" is actually a paid add-on — so the smart move is to know exactly where the line sits before you enroll.

You start with one of two base plans:

- CompanionCare — the accident-and-illness plan. You set the dials: a deductible from $100 to $1,000, reimbursement of 70%, 80%, or 90%, and an annual limit from $2,500 up to unlimited.

- AccidentCare — an accident-only plan. Once a pet is over nine, it's the only coverage AKC will sell, and it pays nothing toward illnesses.

Then come the riders — and this is where the real coverage lives. The base plan excludes more than most people expect until you pay extra:

| Coverage | In the base plan? |

|---|---|

| Accidents & illnesses, surgery, diagnostics, hospitalization | Yes |

| Vet exam / office-visit fees | No — needs the ExamPlus rider |

| Wellness & routine care (vaccines, dental cleaning) | No — needs Defender / DefenderPlus |

| Hereditary & congenital conditions | No — needs HereditaryPlus |

| Behavioral & alternative therapies | No — needs AlternativePlus |

| End-of-life costs; breeding complications | No — needs SupportPlus / Breeding |

The trap to watch is the cheapest "Basic" configuration. It advertises an unlimited annual limit, but pairs it with a $500 per-incident limit that lasts your pet's entire life. For a one-time injury, fine. For a serious or recurring problem, that cap is reached fast — and then you're paying the rest yourself. If you want AKC to function as real coverage, build a custom plan and skip the Basic tier.

Does AKC Cover Your Purebred's Hereditary Conditions?

Not in the standard plan — and for a product built around the American Kennel Club's name, that's the single most important thing to understand. Hip and elbow dysplasia, luxating patella, heart disease, eye disorders, and other inherited problems are excluded from the base plan. You get them only by buying the optional HereditaryPlus rider.

And there's a window. You can generally add HereditaryPlus only while your pet is under two years old (the exact cutoff can vary by state). Miss it, and the coverage most purebred owners came for is closed to you for good.

Even when you add it in time, the fine print bites. The rider carries a 30-day waiting period, and the orthopedic problems big breeds worry about most — cruciate-ligament injuries and disc disease (IVDD) — each carry their own 180-day waits. If your dog shows symptoms of one of those during its waiting period, the condition can be treated as pre-existing — the exact outcome the coverage was meant to prevent.

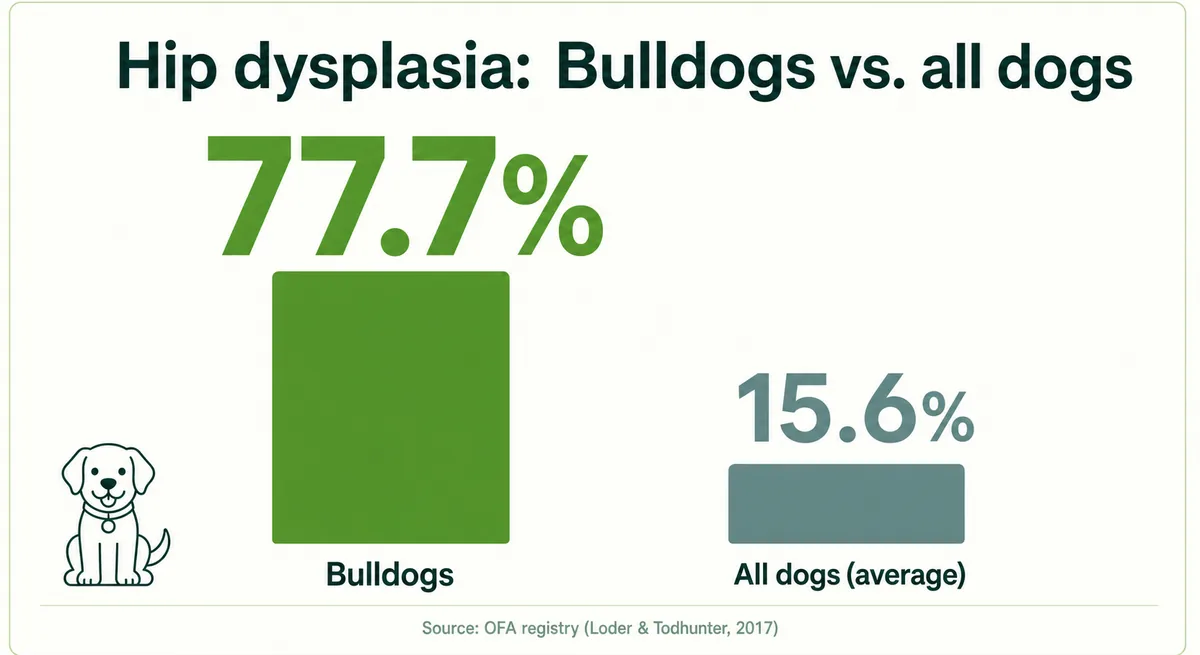

Why does this matter so much here? Because the AKC name draws purebred and breeder owners — precisely the dogs with the highest inherited-disease risk. In the Orthopedic Foundation for Animals registry, canine hip dysplasia affects about 15.6% of dogs overall — and as many as 77.7% of Bulldogs. Many of the large, popular breeds AKC's audience owns sit well above that average.

These are also the conditions with the biggest bills. A single IVDD (slipped-disc) surgery can run $10,000 to $15,000 all-in at a specialty hospital, and hip-replacement or luxating-patella surgery commonly climbs into the low thousands per joint. That's exactly the kind of bill insurance is supposed to absorb.

So the honest verdict for a purebred owner is narrow: HereditaryPlus isn't optional — it's the whole reason to choose AKC, and you have to add it while your dog is young. Do that, and the plan finally fits the audience it's marketed to. If your dog is already two or older, AKC most likely can't give you the coverage you came for, and a carrier that builds hereditary conditions into its base plan is the better bet.

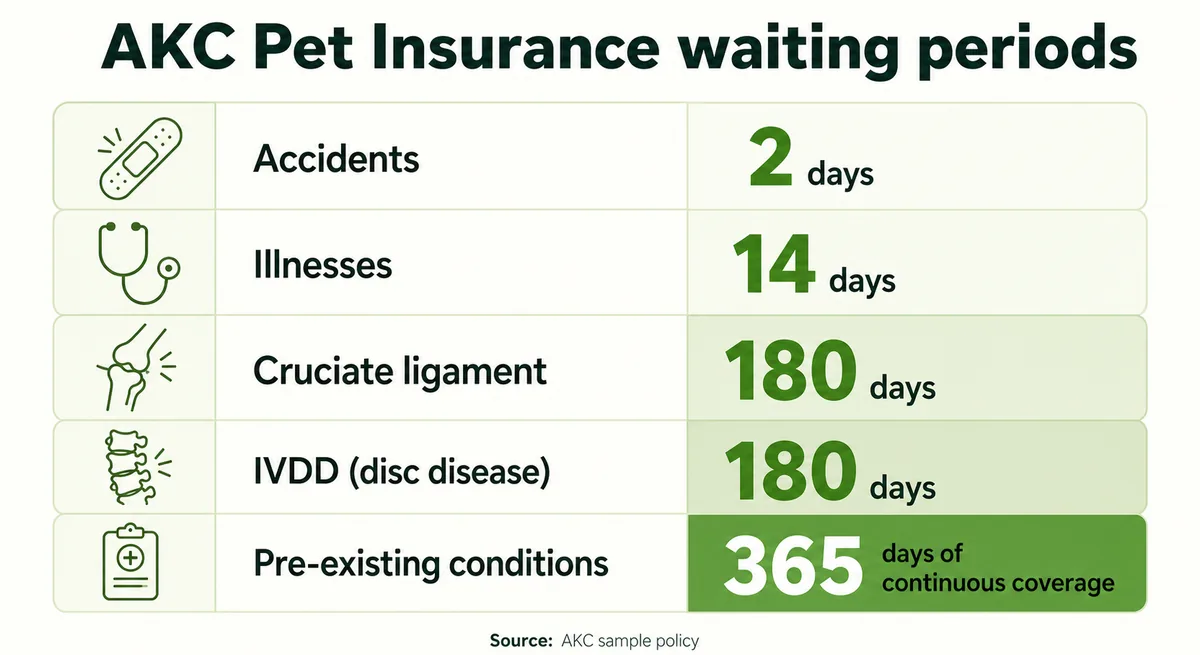

Waiting Periods and the 365-Day Pre-Existing Rule

AKC's waiting periods are quick on accidents and long on the expensive orthopedic stuff — a common industry shape, but worth knowing before you assume you're covered on day one. Here's how long each takes to kick in, per AKC's policy disclosures:

- Accidents: 2 days

- Illnesses: 14 days

- Cruciate ligament injuries: 180 days

- IVDD (disc disease): 180 days

- Pre-existing conditions: 365 days of continuous coverage

(Some third-party sites still list a "5-day accident wait"; AKC's current disclosure says two days.)

The pre-existing rules are where the fine print earns its keep. AKC defines a pre-existing condition broadly: anything that showed symptoms before your coverage started counts, whether or not a vet ever formally diagnosed it. A bilateral clause then extends that logic across the body — if one knee's cruciate ligament showed symptoms before coverage, a later tear in the other knee is also treated as pre-existing and excluded.

The headline feature, though, is genuinely unusual: after 365 days of continuous coverage, AKC begins covering conditions that were pre-existing when you enrolled — something most carriers never do. The word continuous is load-bearing, though: let the policy lapse even briefly and that year-long clock starts over. And read the rest of the strings attached. It applies only to conditions the policy would otherwise cover, so a hereditary problem still needs the HereditaryPlus rider added in time. And on the Basic tier, that $500 per-incident cap can leave the "coverage" nearly worthless for a serious illness.

One bright spot most reviews miss: in many states AKC offers a Waiting Period Waiver. A prompt vet exam shortly after you enroll can shorten or remove some waits when your pet shows no sign of those conditions. The exact exam window, which waits qualify, and the eligible states all vary, so ask AKC before you count on it.

Cost: Real Quotes vs. the National Average

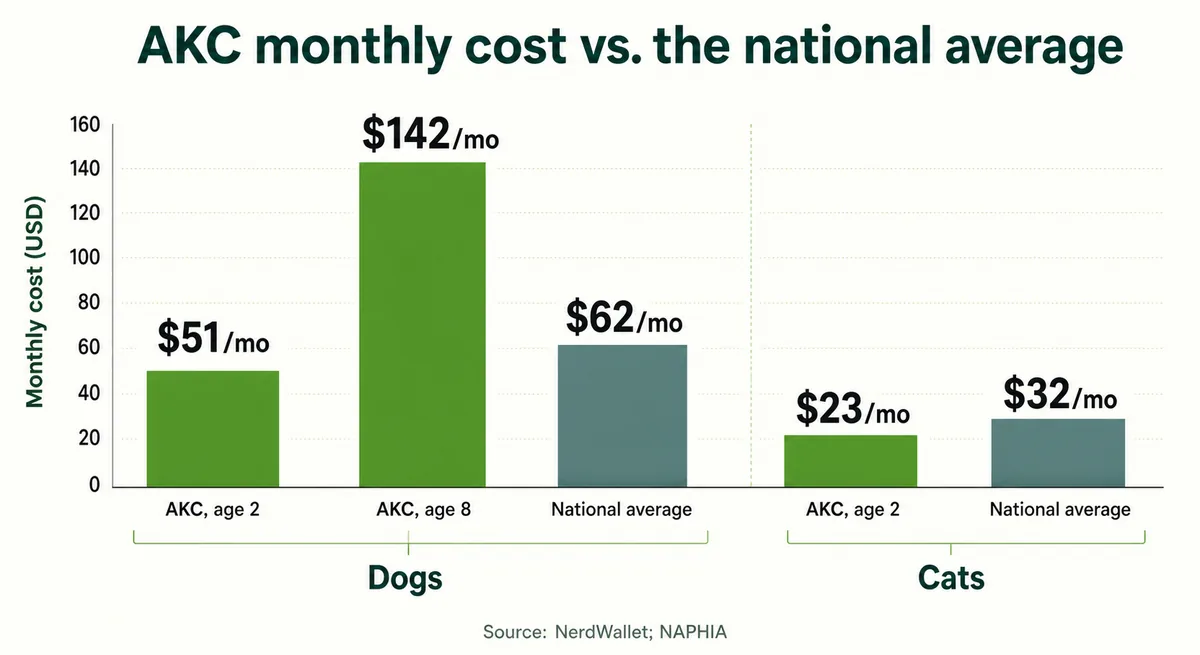

AKC's prices are competitive for a young pet and climb steeply with age — the same pattern as every pet insurer. In one 2026 sample (a $5,000 annual limit, $250 deductible, and 80% reimbursement), NerdWallet quoted a 2-year-old Labrador at about $51 a month, rising to roughly $142 by age 8; a domestic shorthair cat started near $23. Treat those as dated examples, not a promise — your real quote depends on your pet, your ZIP code, and the dials you choose.

The age curve is the story owners underestimate: a dog's premium roughly triples between ages 2 and 8. That's not unique to AKC, but it's the number that stings at renewal.

How does that stack up nationally? The North American Pet Health Insurance Association puts the 2024 average accident-and-illness premium at about $62 a month for dogs and $32 for cats. So a young AKC dog sits below the national average, while an older one lands well above it.

Don't over-read "below average," though. AKC's sample quote assumes one specific configuration, while the national figure blends every plan, age, and deductible — so a low headline number isn't proof AKC is cheaper like-for-like.

A few discounts can trim the bill: AKC offers a 5% multi-pet discount and a 10% discount for qualifying AKC breeders, capped at 15% total. But the honest "true cost" for the purebred owner this brand targets is the base premium plus HereditaryPlus (and often a wellness rider) — which quietly erases much of that headline advantage.

Does It Pay? Claims and Complaints

Honestly, it's mixed — some owners report large claims paid smoothly, while others describe denials that left them feeling misled. There's no public claims-payout statistic for AKC, so treat what follows as voice-of-customer signal, not a denial rate. Going in with clear expectations, and good records, is your best protection.

The mechanics are standard: you pay your vet first and file for reimbursement — there's no guaranteed direct-to-vet payment. You have 180 days to file, straightforward claims are paid quickly by check or deposit, and anything requiring extra vet records can take up to 30 days.

On the positive side, the payouts can be real. One long-term policyholder reported that AKC's administrator paid out more than $30,000 over two years on a chronically ill cat once past the 365-day mark. Balanced against that, the most common complaint is exactly what the fine print sets up: owners describe the pre-existing language as "purposely vague," and denials tend to cluster around pre-existing and bilateral-condition technicalities.

The review scores need context, because they attach to shared corporate entities, not the AKC brand alone. The administrator, PetPartners, holds an A+ rating from the Better Business Bureau. AKC's own Trustpilot page shows about 4.4 out of 5, but it collects invited reviews, which inflates the figure; an independent Yahoo Finance review scored it just 1.9. The Pet Cloud claims app, by contrast, is genuinely well-liked at 4.8 stars on the App Store. Read all of these as directional, not gospel.

One regulatory footnote worth knowing: in 2022, Vermont regulators fined the underwriter $163,050 for adjusting pet claims with unlicensed adjusters. It's dated and was resolved — but it's the kind of detail a careful shopper should have.

The practical takeaway isn't to fear denials; it's records discipline. Keep a complete vet history, get a baseline exam on file, and document every claim fully — in the complaints owners share, the denials usually trace to a specific exclusion clause (pre-existing or bilateral), not to randomness.

The 30-Day Free Trial and the Breeder Channel

A lot of owners first meet AKC insurance through its free trial — often handed to them by a breeder or through the registration process. It's a genuine perk, but it helps to know exactly what it is.

Register an eligible dog and you get 30 days of accident-and-illness coverage at no cost, which you activate within about 28 days. As a low-risk on-ramp while you shop, it's useful.

The catch is that "free" doesn't mean a clean slate. The standard waiting periods still apply during the trial — so IVDD, cruciate injuries, and pre-existing conditions are excluded just as they would be on a paid policy. Think of it as a test drive, not a substitute for a full policy, and read the enrollment terms before you decide to continue.

Because breeders routinely steer new owners into this trial, many purebred buyers arrive already enrolled. That's actually a reason to act quickly: it puts you in a perfect position to add the HereditaryPlus rider while your dog is still under two — the window that decides whether your breed's inherited risks are ever covered. Just don't confuse the insurance with AKC Reunite, which is a separate microchip and pet-recovery service.

AKC vs. the Main Alternatives

How AKC stacks up depends entirely on your situation, and the honest picture is split down the middle:

- Where it wins: its 365-day pre-existing coverage is genuinely rare — most carriers won't cover pre-existing conditions at all (see how Healthy Paws and Lemonade handle them). If your pet has a manageable existing condition and you can wait out the year, AKC is one of the few real options.

- Where it loses: the hereditary base-exclusion. Carriers like Embrace and Pets Best fold hereditary conditions into the standard plan, so a purebred owner never has to chase a rider before age two.

It's also worth remembering that AKC's carriers sit inside one of the industry's largest pet-insurance groups. Some brands you weigh it against may share the same corporate back-end — another reason to judge each plan on its actual coverage terms, not its logo, and to read each carrier's own review before you choose.

The right pick still comes down to your pet's age, breed, and health today: lean toward AKC for the pre-existing edge if you'll actually add the riders, and toward a base-hereditary carrier if your purebred is already past the age-two window. For a true head-to-head across carriers, deductibles, and payout limits, use our full pet insurance comparison.

Frequently Asked Questions

Is AKC Pet Insurance legit?

Yes. It's a real, licensed product — not a scam. The American Kennel Club simply licenses its name to PetPartners, and the coverage is underwritten by Independence American Insurance Company, which holds an A- (Excellent) rating from AM Best. The catch isn't legitimacy; it's the fine print — hereditary conditions and exam fees are paid add-ons, and pre-existing coverage only begins after a year.

Who actually underwrites AKC Pet Insurance?

The insurer on your policy is Independence American Insurance Company (NAIC #26581) or Independence Pet Insurance Company (#17543), both under Independence Pet Group. PetPartners, Inc. administers the plan, and the American Kennel Club only licenses its brand name — it doesn't sell or pay claims. Which carrier appears on your policy can vary by state.

Does AKC Pet Insurance cover hereditary conditions?

Only if you add the optional HereditaryPlus rider — and you can generally add it only while your dog is under two years old. The base plan excludes hip and elbow dysplasia, luxating patella, heart disease, and similar inherited problems. For the purebred owners this brand attracts, adding that rider early is the single most important step.

Does AKC Pet Insurance cover pre-existing conditions?

Unusually, it can — but only after 365 days of continuous coverage, and only for conditions the policy would otherwise cover. Most carriers won't cover pre-existing conditions at all, so this is a genuine differentiator. Two caveats: a hereditary pre-existing condition still needs the HereditaryPlus rider, and if you let coverage lapse, the year-long clock restarts.

What are AKC Pet Insurance's waiting periods?

Per AKC's policy disclosures, they're 2 days for accidents, 14 days for illnesses, and 180 days for cruciate-ligament injuries and IVDD; pre-existing conditions require 365 days of continuous coverage. A clean vet exam within about seven days of your start date can waive some of these waits, though availability varies by state.

How much does AKC Pet Insurance cost?

It depends on your pet, location, and coverage settings, and it rises steeply with age. In one 2026 sample, NerdWallet quoted a 2-year-old Labrador near $51 a month, climbing to about $142 by age 8. That's below the roughly $62-a-month national average for dogs when young — though that's not an apples-to-apples comparison, and the honest cost includes any riders you add.

Is the AKC 30-day free trial really free?

Yes — newly AKC-registered dogs get 30 days of accident-and-illness coverage at no cost, activated within about 28 days. Just know the standard waiting periods still apply during the trial, so it isn't a clean slate for existing conditions — treat it as a trial, and read the enrollment terms before you continue to a paid plan.

Can I get AKC Pet Insurance for a senior dog?

Only partly. A pet over nine can get only the accident-only AccidentCare plan, which won't cover illnesses. If you enroll a dog while it's younger, coverage continues as it ages — so to get illness protection for an older pet, enroll before it's past nine.

Sources

- AKC Pet Insurance — Underwriting & Legal Disclosures — AKC Pet Insurance (PetPartners, Inc.)

- AKC Pet Insurance — Coverage FAQ (hereditary rider, age limits) — AKC Pet Insurance (PetPartners, Inc.)

- AKC Pet Insurance — Pre-Existing Conditions Coverage — AKC Pet Insurance (PetPartners, Inc.)

- AKC Pet Insurance Review 2026: Pros and Cons — NerdWallet

- AM Best Removes From Under Review, Affirms A- Rating of Independence American Insurance Company — AM Best

- AM Best Affirms Independence American Insurance Co. Ratings After $125M Capital Contribution — Insurance Journal

- AKC Pet Insurance — Hereditary & Congenital Condition Coverage (HereditaryPlus) — AKC Pet Insurance (PetPartners, Inc.)

- Demographics of hip dysplasia and other orthopedic diseases in dogs (OFA registry data) — Loder & Todhunter, PMC / NCBI

- How Much Does IVDD Surgery Cost? — Southeast Veterinary Neurology

- AKC Pet Insurance — California Insurer Disclosure (waiting periods, pre-existing, bilateral clause) — AKC Pet Insurance (PetPartners, Inc.)

- AKC Pet Insurance — State Documents & Sample Policies (Waiting Period Waiver Form) — AKC Pet Insurance (PetPartners, Inc.)

- NAPHIA State of the Industry 2025 Report (2024 average premiums) — North American Pet Health Insurance Association (NAPHIA)

- AKC Pet Insurance — Breeder & Multi-Pet Discounts — AKC Pet Insurance (PetPartners, Inc.)

- AKC Pet Insurance — How to File a Claim — AKC Pet Insurance (PetPartners, Inc.)

- r/petinsurancereviews — AKC pre-existing feedback (owner-reported payout) — Reddit

- PetPartners, Inc. (dba AKC Pet Insurance) — BBB Profile — Better Business Bureau

- AKC Pet Insurance Review (ratings roundup) — Insurify

- AKC Pet Insurance Review 2026 (editorial rating) — Yahoo Finance

- Pet Cloud — Apple App Store listing — Apple App Store (Figo Pet Insurance LLC)

- Stipulation & Consent Order — Independence American Insurance Company (Docket 22-018-I) — Vermont Department of Financial Regulation

- AKC Pet Insurance — 30-Day Free Coverage Offer — AKC Pet Insurance (PetPartners, Inc.)

- Organizational Examination of Independence Pet Insurance Company (ownership chain: JAB Holding / Independence Pet Group) — Delaware Department of Insurance

- AKC Pet Insurance — Breeder Discounts (10% breeder discount; 15% maximum) — AKC Pet Insurance (PetPartners, Inc.)