ASPCA Pet Health Insurance is a real, financially backed policy — not a scam. But here's the twist most reviews skip: the ASPCA doesn't actually run it. America's best-known animal-welfare charity licenses its name; a for-profit agency administers the plan, and a separate, rated insurer collects your premium and pays — or denies — your claims.

We read ASPCA's policy documents so you don't have to, and the honest verdict is that it's a solid middle-of-the-road choice for a welfare-minded adopter — not the standout the trusted badge implies. The plan gets real things right: a short 14-day waiting period, exam fees built into the base plan, and a genuinely rare path to cover some "curable" pre-existing conditions. It also hides traps worth knowing before you buy — a knee-and-ligament exclusion that quietly undercuts that short wait, and a "true" monthly cost that only appears once you add the optional Preventive Care rider.

So below we answer the two questions the ASPCA name raises but a spec sheet dodges: does buying this actually help shelter animals, and will your pet's condition really be covered? We name who underwrites it, what it costs as your pet ages, and exactly who should buy it — or skip it.

Table of Contents

- Does the ASPCA Actually Run This — and Who Underwrites It?

- What ASPCA Pet Insurance Costs — the Honest Monthly Total

- Coverage, Plans, and the Fine Print That Bites

- Claims, Renewals, and Complaints — What Owners Actually Report

- Financial Strength and Trust Data

- Who ASPCA Is Best For — and Who Should Skip It

- Frequently Asked Questions

- Sources

Does the ASPCA Actually Run This — and Who Underwrites It?

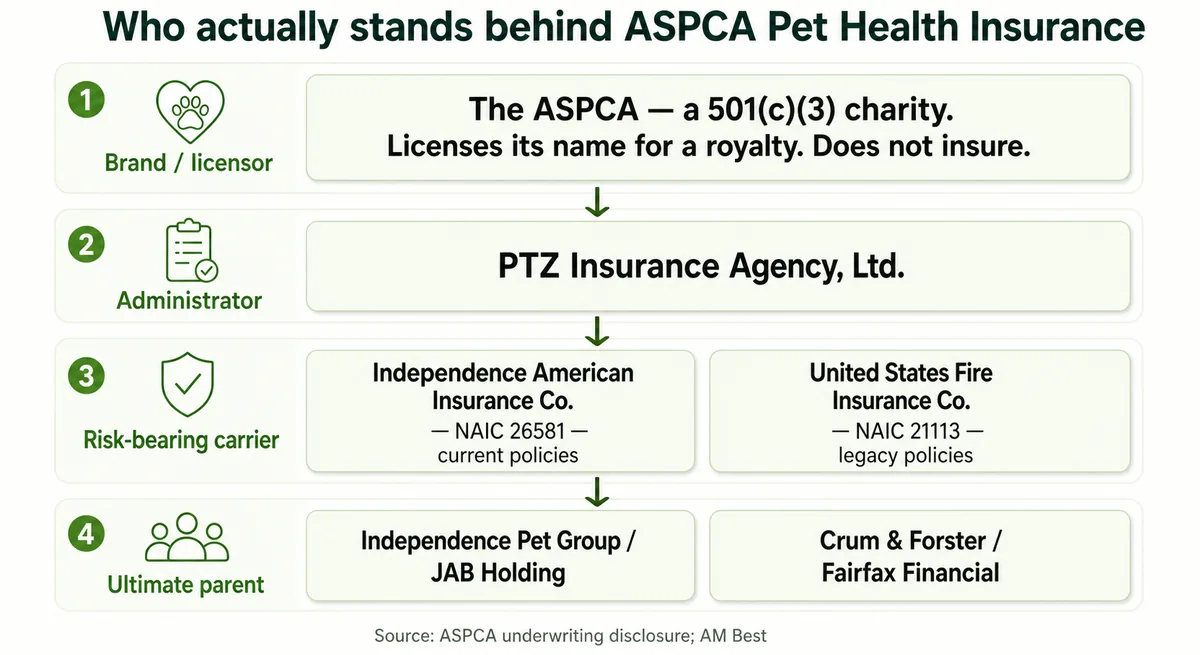

No — and this is the fact the warm badge quietly relies on. The ASPCA is a 501(c)(3) animal-welfare charity that licenses its name to this program. It doesn't sell the policy or pay your claims, and it says so directly: it "is not an insurer," and the arrangement is a name-licensing royalty, not a charitable contribution. So buying an ASPCA policy is not a donation to shelter animals — if supporting the charity is your goal, give to the ASPCA directly and shop the insurance on its own merits.

Four separate companies stand behind "ASPCA Pet Health Insurance." Keeping their roles straight is the whole game:

| Layer | Who it is | What they do |

|---|---|---|

| Brand / licensor | The ASPCA (a 501(c)(3) charity) | Lends its name for a royalty; doesn't sell policies or pay claims |

| Producer / administrator | PTZ Insurance Agency, Ltd. | Builds, markets, and services the plan |

| Risk-bearing insurer | Independence American Insurance Co. (NAIC #26581) — or United States Fire Insurance Co. (#21113) on older policies | Collects your premium and pays — or denies — claims |

| Ultimate parent | Independence Pet Group / JAB Holding, or Fairfax Financial | Owns the risk-bearing carrier |

Here's the wrinkle almost no review mentions: the insurer on your policy — and its owner — depends on your state and when you enrolled. Current accident-and-illness policies are underwritten by Independence American Insurance Company, which sits under Independence Pet Group and, ultimately, JAB Holding Company — the same parent as AKC Pet Insurance, Figo, Spot, and Pumpkin. Older policies ride on United States Fire Insurance Company, which stayed with Crum & Forster and its parent Fairfax Financial when the pet program was sold in 2022.

That has a real consequence for shoppers: two "different" brands you're weighing against each other may quietly share one owner, so cross-shopping ASPCA, Spot, and Pumpkin can be closer to comparing three doors on the same house than three separate insurers. Both carriers are financially solid — we cover the ratings later — but the practical move is simple: read your own declarations page. It names the insurer, and that entity, not the charity on the logo, is the one legally on the hook for your claim.

What ASPCA Pet Insurance Costs — the Honest Monthly Total

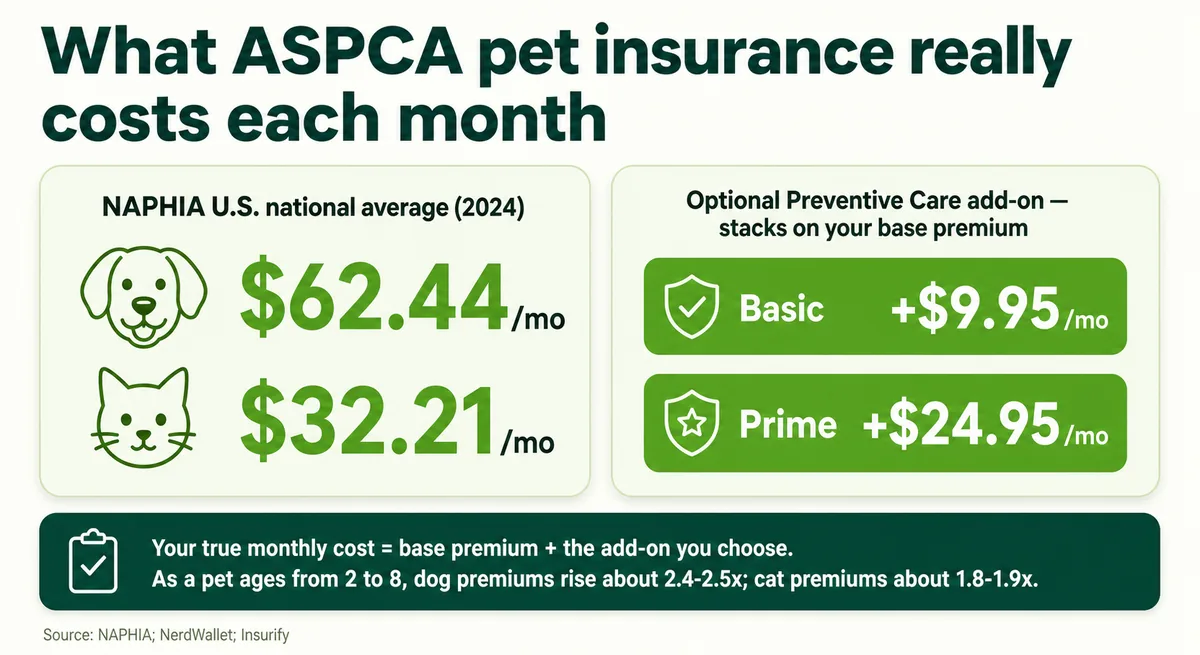

ASPCA prices in the middle of the market for a young pet and climbs steeply as your pet ages — and the number you'll actually pay is higher than the headline quote once you add the optional wellness rider. Every figure below is a dated sample tied to a specific configuration, not a guaranteed premium; ASPCA's own site doesn't publish sample prices, so these come from third-party quotes.

Representative NerdWallet quotes for the Complete Coverage plan (Katy, TX; $250 deductible, $5,000 annual limit, 80% reimbursement), at age 2 versus age 8:

| Pet | Age 2 | Age 8 |

|---|---|---|

| Labrador Retriever | $55/mo | $137/mo |

| French Bulldog | $78/mo | $194/mo |

| Medium mixed-breed dog | $39/mo | $98/mo |

| Domestic Shorthair cat | $19/mo | $35/mo |

Notice the split: dog premiums climb about 2.4–2.5× from age 2 to age 8, but cats rise more gently — closer to 1.8–1.9×. A young dog often lands below the NAPHIA national average of roughly $62/month for dogs (and $32 for cats) — a blended average across all plans and configurations, so read it as rough context, not a like-for-like match — then blows past it with age, the "cheap at 2, pricey at 8" reality behind what pet insurance actually costs over a lifetime. Cats stay comparatively affordable across the whole age band, which makes ASPCA an easier long-term yes for a cat household than for the owner of a large, aging dog.

Two levers move the real number. Discounts help a little: a 10% multi-pet discount, plus up to 10% for veterinary staff, some association members, and certain employer programs. But if you want wellness coverage, your all-in figure is the base premium plus the optional Preventive Care add-on — about $9.95/month for Basic or $24.95/month for Prime. On a $40 base plan, adding Prime pushes the total to roughly $65/month — worth counting before the headline quote wins you over.

Coverage, Plans, and the Fine Print That Bites

ASPCA sells two base plans plus one optional add-on. Complete Coverage is the accident-and-illness plan most buyers want; Accident-Only is a cheaper plan that pays for injuries but not illnesses — the mismatch behind a lot of angry "they denied my claim" stories, because a sick pet on an accident-only plan simply isn't covered. And "Complete" is a plan name, not a promise that everything is bundled: routine wellness, vaccines, and dental cleanings are not in it — those live in the separate Preventive Care rider below.

You tune Complete Coverage with three dials: an annual deductible of $100, $250, or $500; reimbursement of 70%, 80%, or 90%; and an annual limit from $2,500 up to unlimited. Two genuine strengths stand out: exam and office-visit fees are built into the base plan (many carriers charge extra for those), and there's no vet-network restriction — any licensed U.S. vet works.

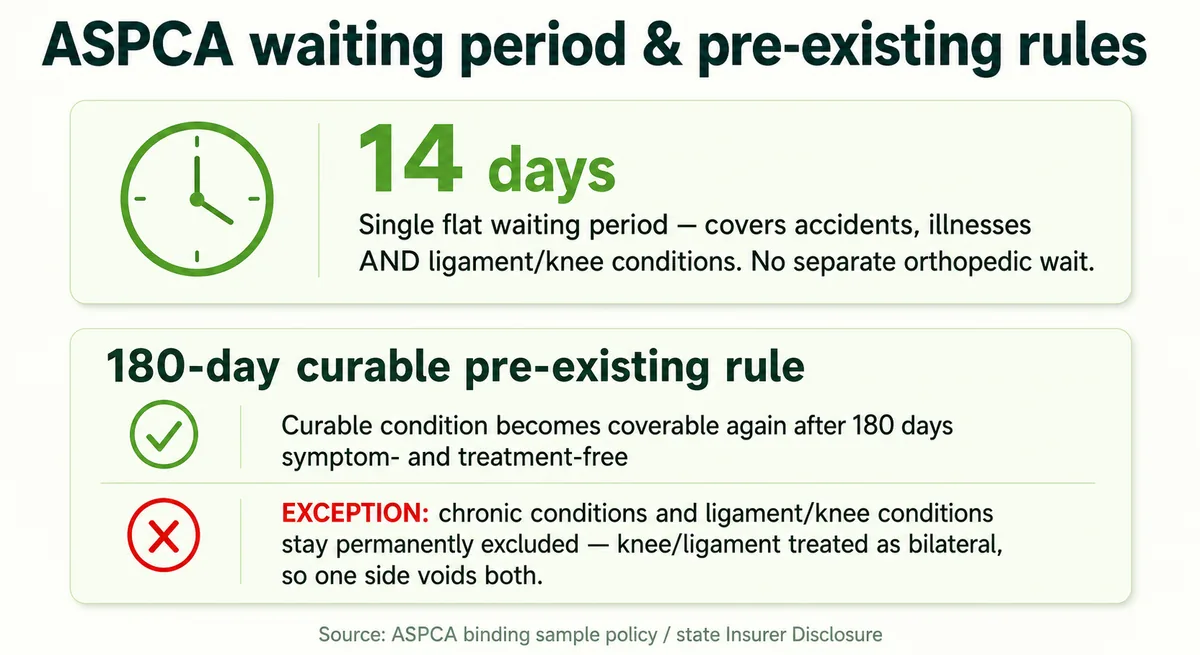

Waiting periods are short and, unusually, flat: a single 14-day wait covers accidents, illnesses, and even cruciate/knee injuries — there's no separate six-month orthopedic wait like some competitors impose. You can even shorten it: a clean Waiting Period Health Assessment exam, done from 3 days before to 7 days after your start date, can waive the wait (it does not, however, erase a pre-existing condition). These waiting-period terms come from ASPCA's sample policy and state disclosures — your own policy form and state set the exact wording, so read your declarations page.

Now the part that bites. ASPCA's pre-existing rule is symptom-based: anything your pet showed signs of before coverage — diagnosed or not — is excluded. ASPCA does offer a rare escape hatch: a curable pre-existing condition can be covered again after 180 days symptom- and treatment-free. But read the carve-out — it "does not apply to chronic conditions or ligament and knee conditions." And here's the trap: knee and ligament problems are treated as bilateral, so if one knee was pre-existing, ASPCA can permanently exclude the other one too, "regardless of cause." Since cruciate-ligament tears are a common four-figure orthopedic claim in dogs — and often strike both knees over a lifetime — that single clause quietly cancels much of the value of the short 14-day wait.

The Preventive Care add-on: forced budgeting, not insurance

Preventive Care isn't real insurance — it's a fixed cash-back schedule with no deductible: a set dollar cap per service (a wellness exam reimburses up to $50; a dental cleaning up to $100 on Basic). Because the annual cap is fixed — $250 on Basic, $450 on Prime — and the rider runs about $120 to $300 a year, it only pays for itself if you actually use the services: on Basic, a wellness exam ($50) plus one dental cleaning ($100) already clears its roughly $120 price, but use less than that and you're just pre-paying for routine care. Either way it's budgeting for predictable costs, not insuring against surprises.

Claims, Renewals, and Complaints — What Owners Actually Report

ASPCA runs on the standard model: you pay the vet, then file for reimbursement. You get a generous 270 days to submit a claim, and the company aims to process clean claims in "30 days or less," paying by direct deposit or check. Direct-to-vet payment exists but is opt-in per claim — you and your vet have to request it, unlike carriers such as Trupanion that pay the clinic directly by default. One weak spot: the mobile app rates about 2.1 out of 5, with owners reporting the claim flow freezing partway through.

The loudest complaints aren't about whether ASPCA pays — they're about renewals. Like most pet insurers, ASPCA prices by your pet's age, so premiums generally rise as it gets older — sometimes sharply. Owners on Reddit describe premiums running from $30 to $45 to $72 a month across renewals, and a 45% jump after a claim — dated, individual examples rather than a guaranteed schedule, but a consistent enough theme to plan for. Watch for the quieter version, too: some owners report their deductible being raised at renewal while the monthly premium held flat — an unverified individual account, but the kind of quiet change worth checking your own renewal notice for.

This bites because of the age-out trap: once your pet has developed a health condition, any new insurer will treat it as pre-existing and exclude it, so walking away from a pricey renewal often isn't a real option. ASPCA's policy disclosures do say it won't raise your premium because of your claims history — true on paper, but read it alongside the reality that age-based pricing pushes the price up as your pet gets older regardless.

It isn't all grim. A meaningful share of owners report fast, full reimbursements — and ASPCA is one of the few brands that also insures horses. As with most carriers, the experience is bimodal: smooth when the records are clean, painful when a claim turns on a pre-existing determination. The practical defense is the same either way — keep your pet's vet records complete and current, file promptly, and never skip needed care to protect a future claim.

Financial Strength and Trust Data

Financial-strength ratings attach to the carrier on your policy — not to the ASPCA charity, which bears no risk — so check the one that actually insures you. Legacy policies underwritten by United States Fire Insurance Company carry an AM Best rating of A+ (Superior), AM Best's second-highest tier, upgraded from A in August 2025. Current accident-and-illness policies underwritten by Independence American Insurance Company hold an A- (Excellent) — still firmly "secure," but a notch lower, and with a recent wrinkle worth knowing: AM Best placed IAIC under review in August 2025 after its pet reinsurance failed a risk-transfer test, then affirmed the A- as stable that December — but only after its parent contributed $125 million and renegotiated that reinsurance. Both carriers are financially sound; IAIC's is simply the more eventful recent story.

For market context, U.S. pet insurers wrote roughly $4.66 billion in premiums in 2024 at a 71.6% loss ratio — the first year regulators tracked pet insurance as its own reporting line. One honest caveat: no complaint index is cleanly published per brand here, because each carrier writes many other lines — so treat any single "ASPCA complaint rate" quoted elsewhere with skepticism.

Who ASPCA Is Best For — and Who Should Skip It

There's no universal "best" here — the right answer depends on your situation. ASPCA is a genuinely good fit for a specific kind of owner, and a mediocre one for others.

ASPCA is a strong pick if you're…

- a welfare-minded adopter or mixed-breed owner who likes that the brand's mission aligns with your values — just remember the ASPCA only earns a licensing royalty for its name here, so your premium isn't a donation to shelters;

- enrolling a young, healthy pet now, before any symptom can be labeled pre-existing;

- someone who specifically values exam fees built into the base plan, the short 14-day waiting period, and the rare chance to re-cover a curable pre-existing condition after 180 symptom-free days.

Think twice — and shop around — if you…

- want your insurer to reliably pay the vet directly at checkout: Trupanion is built for that; ASPCA offers direct-to-vet payment only as an opt-in request and otherwise reimburses you after you've paid;

- prioritize the fastest, most automated claims: app-first carriers like Lemonade tend to turn around straightforward claims quicker;

- are buying for a knee- or ligament-prone breed that already has a history on one side — the bilateral exclusion can then void the other knee too;

- are insuring an older pet and worry about renewal creep, since premiums age-band upward every year.

None of these are dealbreakers so much as trade-offs worth weighing before you buy. The smart move is to put ASPCA side by side with the alternatives: our pet insurance comparison hub runs the head-to-head duels, and you can read our full carrier reviews for the names mentioned above.

Frequently Asked Questions

Does the ASPCA actually run this pet insurance?

No. The American Society for the Prevention of Cruelty to Animals is a charity that licenses its name to the program for a royalty — it doesn't sell the policy or pay your claims. The plan is administered by PTZ Insurance Agency and underwritten by Independence American Insurance Company (or United States Fire Insurance Company on older policies). Because that fee is a licensing royalty, buying a policy is not a charitable donation to shelter animals.

Is ASPCA pet insurance legit and reliable?

Yes — it's a real, financially backed policy, not a scam. The program has operated for over two decades and is underwritten by rated insurers: United States Fire Insurance Company carries an AM Best A+ (Superior) rating and Independence American Insurance Company an A- (Excellent). Owner experiences are genuinely mixed — mostly around claim outcomes — but the coverage itself is legitimate and claims do get paid.

Do vets accept ASPCA pet insurance? Is there a network?

There's no network — you can use any licensed veterinarian in the United States, including specialists and emergency hospitals. ASPCA works on reimbursement: you pay your vet at the time of service and then file a claim to be paid back (the company aims for 30 days or less), so the clinic doesn't need to "accept" the insurance directly.

Does ASPCA cover chronic conditions like Addison's disease?

Yes — ongoing and chronic illnesses such as Addison's disease, diabetes, or allergies are covered under the Complete Coverage plan, provided the condition wasn't pre-existing (it didn't show symptoms before your coverage started or during the waiting period). Two limits matter: claims count against your annual limit each policy year, and chronic conditions are specifically excluded from the 180-day "curable" cure-back rule — so a chronic condition that was pre-existing stays excluded.

Does ASPCA cover pre-existing conditions?

Not in the usual sense. ASPCA's definition is symptom-based: anything your pet showed signs of before coverage — diagnosed or not — is excluded. There is one uncommon exception: a curable condition can become eligible again after 180 days symptom- and treatment-free. That exception does not apply to chronic conditions, or to knee and ligament conditions.

What is the ASPCA pet insurance waiting period?

ASPCA uses a single, short 14-day waiting period that covers accidents, illnesses, and even knee and ligament conditions — there's no separate, longer orthopedic wait like some competitors impose. You can even waive it: a clean Waiting Period Health Assessment exam (completed from 3 days before to 7 days after your start date) removes the wait, though it does not erase a pre-existing condition.

How much does ASPCA pet insurance cost?

It varies by pet, age, and location. Representative Complete Coverage quotes run roughly $19–$35 a month for a cat and $39–$194 a month for a dog between ages 2 and 8 (a young mixed-breed at the low end, an older French Bulldog at the high end). The figure to plan around is the "true" cost: your base premium plus the optional Preventive Care add-on, which runs about $9.95 a month (Basic) or $24.95 a month (Prime) if you add wellness coverage.

Is ASPCA pet insurance worth it?

It depends on your situation. ASPCA is a solid middle-of-the-road choice — strongest for a young, healthy pet whose owner values exam fees built into the base plan, the short 14-day wait, and the curable-pre-existing path. It's a weaker fit if you need your insurer to pay the vet directly, want the fastest automated claims, or have a breed prone to knee and ligament injuries that the bilateral exclusion can undercut. There's no single "most highly rated" pet insurer — satisfaction splits sharply on whether you ever hit a denied claim.

How do I cancel ASPCA pet insurance?

You cancel by contacting ASPCA's customer service — through the online Member Center or by phone. Ask about the exact steps and any refund of unused premium, since those depend on your state and your policy's terms. Some owners have reported, in dated reviews, that cancellation may need a phone call rather than a fully online process, so allow a little time for it.

Sources

- ASPCA Pet Health Insurance underwriting disclosure — ASPCA Pet Health Insurance

- Pet Insurance and Pre-Existing Conditions — ASPCA Pet Health Insurance

- ASPCA Pet Health Insurance strategic cause partnership — ASPCA

- Independence Pet Group Completes Acquisition of Fairfax's Crum & Forster Pet Insurance Group and Pethealth — Insurance Journal

- United States Fire Insurance Company — AM Best rating & ultimate parent — AM Best

- ASPCA Pet Insurance Review 2026: Pros and Cons — NerdWallet

- State of the Industry Report 2025 — NAPHIA

- ASPCA Pet Health Insurance plans — ASPCA Pet Health Insurance

- ASPCA Pet Insurance Reviews: How It Stacks Up (2026) — Insurify

- How does pet insurance work? (deductible, reimbursement, annual limit) — ASPCA Pet Health Insurance

- What's covered by ASPCA pet insurance — ASPCA Pet Health Insurance

- Sample policy pages — Florida accident & illness (Form V47) — ASPCA Pet Health Insurance / Independence American Insurance Company

- Delaware Insurer Disclosure of Important Policy Provisions (APHI) — ASPCA Pet Health Insurance / Independence American Insurance Company

- Preventive Care coverage — ASPCA Pet Health Insurance

- ASPCA Pet Health Insurance — top customer questions (claims, filing window, reimbursement) — ASPCA Pet Health Insurance

- ASPCA Pet Health Insurance mobile app — App Store ratings — Apple App Store

- Reddit: Anyone use ASPCA? (r/petinsurancereviews) — Reddit

- Reddit: ASPCA pet insurance (r/petinsurancereviews) — Reddit

- Crum & Forster upgraded to A+ (Superior) by AM Best (US Fire carrier group) — PR Newswire / Crum & Forster

- AM Best places Independence American Insurance Company under review (pet reinsurance risk-transfer) — AM Best

- AM Best affirms Independence American Insurance Company A- (stable) after $125M parent contribution — Insurance Journal

- NAIC 2024 Market Share Report — pet insurance broken out as its own line ($4.66B DPW, 71.62% loss ratio) — National Association of Insurance Commissioners