Short answer: Spot is a legitimate, broadly-featured pet insurance brand that does pay real claims — but whether it's worth it for your pet comes down to two things most reviews skip: who actually stands behind the policy, and which of your pet's conditions the fine print will really cover.

Here's what almost no "spot pet insurance reviews" page tells you: Spot doesn't underwrite its own policies. Spot is a brand and licensed agency; the company that collects your premium and approves or denies your claim is a separate licensed insurer named on your policy — and Spot uses more than one, depending on your state (Spot's own underwriting disclosure).

We read Spot's actual sample policy and its underwriters' financial-strength ratings so you don't have to. This review settles the questions a marketing page dodges: how long Spot's waiting period really is (and the knee-clause catch buried inside it), what Spot costs once the wellness add-on is layered on, whether Spot and Pumpkin are quietly the same company, and — the one that matters most when you're stressed at the vet's counter — who you're actually up against if you ever have to fight a claim.

You'll get a verdict here, but a conditional one. Spot is a strong fit for some pets and the wrong call for others, and we'll tell you which is which before you spend a dollar.

Table of Contents

- The Verdict: Who Spot Fits and Who Should Look Elsewhere

- Who Really Underwrites and Owns Spot (Is It the Same as Pumpkin and ASPCA?)

- What Spot Covers — and the Exam-Fee Truth

- Spot's Waiting Periods — and the Cruciate/Bilateral Trap

- Pre-Existing Conditions and the 180-Day Curable Window

- What Spot Really Costs — Base Plan Plus the Wellness Add-On

- Does Spot Pay? Claims, App, and Real Customer Reputation

- Spot vs. Pumpkin: Two Brands, One Roof

- How to Cancel Spot Pet Insurance

- Frequently Asked Questions

- Sources

The Verdict: Who Spot Fits and Who Should Look Elsewhere

Spot is a genuinely strong accident-and-illness plan on paper — but it isn't the right pick for every pet, and the difference usually comes down to your pet's history, not the brochure.

Spot is a strong fit if:

- You want vet exam fees covered in the base plan — a real perk that only a handful of insurers include without an add-on.

- You're insuring an older or newly-adopted pet: Spot sets no upper age limit to enroll and offers a true unlimited annual-payout tier for owners who don't want a ceiling (CNBC Select).

- You value a short, flat waiting period — Spot applies one 14-day wait to accidents, illnesses, and knee/ligament conditions alike, with no separate months-long orthopedic wait, per its stated waiting-period guidance (Spot) and the sample policy (Spot sample policy). Your own declarations page and state can vary the details.

Look elsewhere if:

- Your pet already has a knee or ligament issue, or any chronic condition. If a knee or ligament problem showed up before coverage started or during the waiting period, Spot's bilateral clause can permanently exclude the second knee too, and its curable-condition "cure-back" window doesn't apply to chronic or knee/ligament problems — we quote the exact wording further down.

- You're shopping purely on price. Because Spot shares its underwriters and its parent group with Pumpkin (and the ASPCA-branded plan), you should quote them side by side for the same coverage before assuming Spot is the cheapest.

- You were counting on a waivable orthopedic wait — Spot offers no vet-exam route to shorten it.

One honest caveat colors everything below: being approved for a Spot policy is not the same as having your pet's condition covered. Spot's marketing leans on broad-coverage language, and much of it holds up — but only once you read the fine print we walk through next, starting with the question that matters most when a claim is on the line: who actually pays it, and how financially solid are they?

Who Really Underwrites and Owns Spot (Is It the Same as Pumpkin and ASPCA?)

Buy a "Spot" policy and four different companies are actually involved — and knowing which is which matters the day you file a claim, because the "Spot" on your welcome email is not the company that pays it.

- The brand and producer is Spot Pet Insurance Services, LLC — a licensed agency that markets and sells the plan and holds no claims reserves (Spot's underwriting disclosure).

- The administrator running Spot's back office — underwriting operations, customer service, and claims handling — is Independence Pet Holdings, which took a majority stake in Spot in 2024 (Insurance Journal). It administers the plan; it is not itself the risk-bearing insurer.

- The risk-bearing insurer — the company that actually pays or denies your claim — is named on your policy form, and Spot uses two: Independence American Insurance Company (NAIC #26581) or United States Fire Insurance Company (NAIC #21113), depending on your state. Spot's own guidance is to "refer to your policy forms" to see which is yours.

- The ultimate parent is where it gets interesting.

Here's the split most reviews miss: those two insurers roll up to two different corporate families. United States Fire is a Crum & Forster company, ultimately owned by Fairfax Financial. Independence American rolls up through Independence Pet Holdings to JAB Holding Company. So depending on which form your state puts you on, your policy sits inside either the Fairfax or the JAB corporate group — but it's the named insurer on your declarations page, not its ultimate parent, that is legally obligated to pay your claim. A parent's size is reassuring context, not a guarantee you can bill; the group matters mainly because it shapes the carrier's own financial strength.

That shared Independence Pet platform is also why Spot and Pumpkin feel so alike — they name the same two underwriters and run on the same administrator (Pumpkin's underwriting disclosure). The ASPCA-branded pet plan sits in the same Independence Pet group of brands. If you're cross-shopping them, treat it as a useful heads-up to quote each one, not a scandal.

What actually deserves your attention is the financial strength of your insurer, not the Spot name. United States Fire carries an AM Best rating of A+ (Superior). Independence American carries A- (Excellent) — two notches lower on AM Best's scale (A+ → A → A-) — and had a busier year: AM Best placed it under review in 2025 over a reinsurance quota-share accounting issue, then removed that review and affirmed the A- in December 2025 after its parent contributed an additional $125 million in capital (Insurance Journal). Both are financially sound — but it's worth knowing which one is behind your policy.

One last thing worth right-sizing: Spot's marketing has leaned on a celebrity dog-trainer association. A famous name can make a brand feel trustworthy, but it isn't a coverage term and it buys you nothing on a claim. Judge Spot on its policy and its carrier, not its endorsement.

What Spot Covers — and the Exam-Fee Truth

Spot sells one main accident-and-illness plan with genuinely flexible settings, plus an optional wellness add-on — but a couple of its headline perks come with an asterisk worth reading before you buy.

The dials you actually choose

Spot's accident-and-illness plan gives you three levers: an annual deductible of $100, $250, $500, $750, or $1,000; a reimbursement rate of 70%, 80%, or 90%; and an annual payout limit that runs from $2,500 up to unlimited (Spot's deductible guide, Spot's annual-limit guide). The deductible comes out first, then Spot reimburses your chosen percentage of the rest. Unlike some rivals, there is no per-incident or per-condition cap — the annual limit is the only ceiling, and it resets each year rather than rolling over (Spot sample policy).

Exam fees: covered — but mind the fine print

Here's the perk that trips people up. Spot does include the vet exam or office-visit fee for a covered accident or illness in its base plan — a genuine advantage, since relatively few insurers do (Spot). But the routine annual wellness exam is a different animal: it's excluded from the base plan and only reimbursed if you add the paid Preventive Care rider. "Exam fees covered" is true for the sick visit — not the yearly checkup.

The rest of Spot's base coverage is broad but conditional. Microchip implantation is included; behavioral therapy is covered only through a vet or a written referral to a credentialed behaviorist; and alternative treatments like acupuncture or hydrotherapy are covered when a vet performs or supervises them — while CBD, supplements, and prescription food for general maintenance are excluded (Spot sample policy). And Spot sets no upper age limit to enroll an older pet (CNBC Select) — just remember that enrolling a senior pet does not undo the pre-existing rules we cover next.

Spot's Waiting Periods — and the Cruciate/Bilateral Trap

Spot's waiting period is refreshingly short: a single 14-day wait covers accidents, illnesses, and knee/ligament conditions alike, with no separate months-long orthopedic wait. In Spot's own policy language, "there is a 14 day waiting period for: diagnosis, treatment or surgery related to accidents, illnesses and ligament and knee conditions" (Spot sample policy).

That matters, because a separate, longer waiting period for cruciate and other orthopedic conditions is common elsewhere in the market — several competitors impose one. If you searched "spot pet insurance waiting period" while worried about a big dog's knees, Spot's flat 14 days is a genuine advantage — and in select states, accident coverage can even begin the next day (Spot).

The Knee Trap: where a short wait quietly gives back

Here's the catch a 14-day headline hides. Spot treats knee and ligament problems as bilateral — an issue on one leg is deemed related to the other. The policy defines "Ligament and Knee Conditions" this way:

…considered bilateral conditions and related, regardless of cause; meaning an occurrence on one side of the body affects both sides of the body.

So if your dog ever showed a knee or ligament problem in one leg before coverage began — or during those first 14 days — the other knee can be treated as pre-existing too, and permanently excluded. A torn cruciate is the most common orthopedic claim in dogs, which makes this the clause most worth checking.

It gets sharper alongside Spot's curable-condition rule. Spot will re-cover a curable pre-existing condition after 180 symptom- and treatment-free days — but that grace window "does not apply to chronic conditions or ligament and knee conditions" (Spot sample policy). A knee problem that counts as pre-existing never earns its way back in.

None of this is a reason to skip a vet visit to keep a condition "off the record." Your pet's health comes first, and hiding a symptom won't change what a vet would document anyway. The practical move is simpler: enroll before problems appear if you can, and go in knowing exactly what Spot's fine print treats as related.

Pre-Existing Conditions and the 180-Day Curable Window

Like nearly every U.S. pet insurer, Spot won't cover pre-existing conditions — but what counts as "pre-existing" is broader than most first-time buyers expect, and pre-existing exclusions are among the most common reasons any pet-insurance claim gets denied.

Spot's definition is symptom-based, not diagnosis-based. A condition is pre-existing if it showed signs before your coverage started or during the waiting period — even if no vet ever named it. That includes anything "recorded in your pet's medical record" or that "would have been detectable by a routine physical veterinary exam" (Spot sample policy). A cough your vet noted last year, or a limp you mentioned in passing, can be enough.

The no-records trap

This is where owners get blindsided. Spot's policy sets the clock on a condition from the moment its signs were "first… observed by any individual, recorded in your pet's medical record, or would have been detectable by a routine physical veterinary exam" (Spot sample policy). In plain terms, a problem your pet was already showing — even one no vet had formally named — can be treated as pre-existing when you file. The practical move is to enroll before symptoms appear and to keep up annual exams so your records establish a clean baseline, never to skip vet visits.

Now the good news, with a limit. Spot offers a curable-condition "cure-back": if a pre-existing condition is curable and stays symptom- and treatment-free for 180 days, Spot will treat it as a new condition and cover it again (Spot sample policy). That's more generous than carriers that exclude every pre-existing condition for life.

But read the exclusion in the same breath: the 180-day window "does not apply to chronic conditions or ligament and knee conditions." A curable ear or urinary infection can earn its way back into coverage; diabetes, allergies, or a torn cruciate cannot.

The honest takeaway for a nervous shopper: buying a Spot policy is not the same as getting a condition covered. If your pet is already showing signs of something, a new policy generally won't cover that condition — the narrow exception being the curable cure-back above, once the symptom-free window is met. And none of this is a reason to put off care your pet needs; get the treatment, then shop insurance for whatever comes next.

What Spot Really Costs — Base Plan Plus the Wellness Add-On

Spot's advertised low starting price is a floor, not a forecast. What you'll actually pay depends on your pet's species, breed, age, and ZIP code — and, if you add wellness, on a second monthly charge most quotes bury.

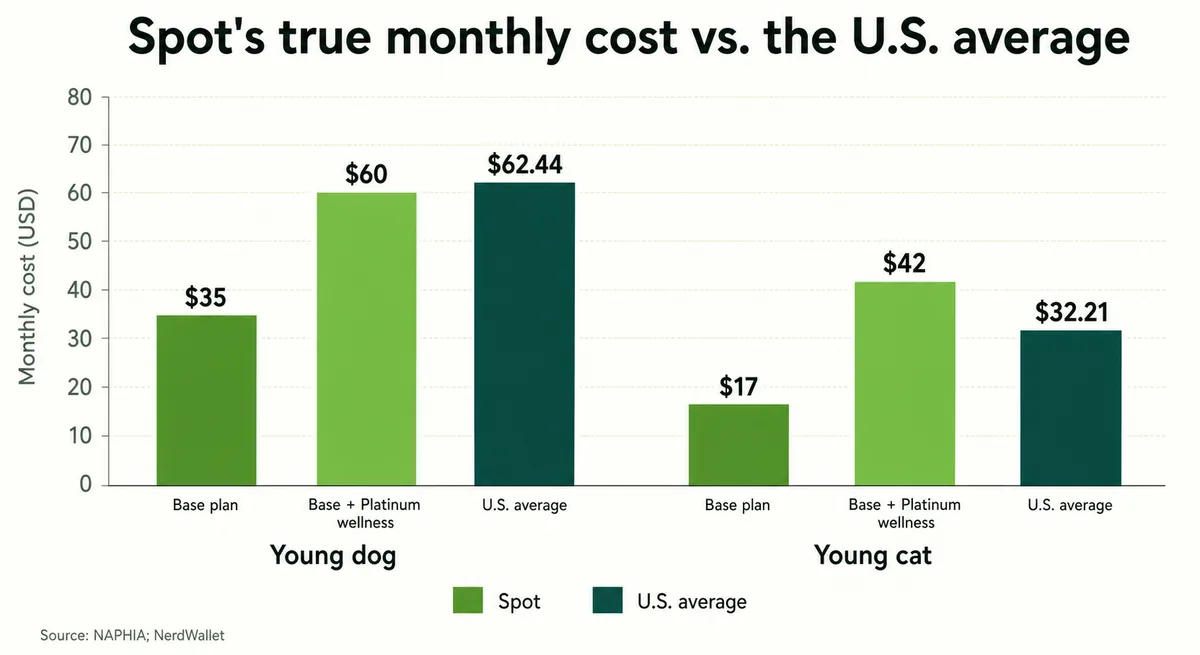

For a concrete anchor: in one 2026 sample set (Katy, Texas; $250 deductible, $5,000 annual limit, 80% reimbursement), Spot quoted a 2-year-old medium mixed-breed dog about $35/month and a 2-year-old domestic shorthair cat about $17/month — but a 2-year-old French Bulldog ran $70, and by age 8 those same dogs climbed to $88–$174 (NerdWallet). Those young-pet figures land under the NAPHIA U.S. average accident-and-illness premium (2024 data) of $62.44/month for dogs and $32.21/month for cats (NAPHIA) — but that average is a blended, sales-weighted number, so a cheaper quote for a young pet isn't proof Spot is cheaper like-for-like.

Now the part the teaser price hides. Spot's optional Preventive Care add-on comes in two tiers: Gold at about $9.95/month (up to $250/year in benefits) and Platinum at about $24.95/month (up to $450/year) (Mercer/Belk, CNBC Select). It's structured as an optional endorsement on the insurance policy, but unlike the base accident-and-illness plan it reimburses a fixed schedule of routine costs rather than a percentage of the bill — closer to budgeting than to risk-transfer coverage. Layer Platinum onto that $35 young dog and the honest all-in is closer to $60/month; onto the $17 cat, about $42/month. Keep the comparison apples-to-apples, though: it's Spot's $17 base insurance quote that belongs next to the $32.21 cat insurance benchmark (comfortably under it), with the preventive package an optional non-insurance extra layered on top — not part of the premium being benchmarked.

Two cost realities to plan for. First, premiums rise as your pet ages: Spot rates on age, breed, and location rather than your claim history, and its policy states that coverage and rates are subject to change at each 12-month renewal (Spot sample policy). NerdWallet's own sample quotes show the scale of that climb — the same medium mixed-breed dog quoted about $35/month at age 2 is quoted roughly $88/month by age 8 (NerdWallet). Second, there's a 10% multi-pet discount if you insure more than one. Budget for the pet you'll have at eight, not just the quote you see at two.

Does Spot Pay? Claims, App, and Real Customer Reputation

Yes — Spot does pay claims, and the process itself is straightforward — but its public reputation is genuinely split, and it's worth understanding why the star ratings disagree so sharply.

Mechanically, Spot is reimbursement-only: you pay your vet, then file. You get a generous 270 days from the date of service to submit a claim (Spot), and reimbursement arrives by direct deposit or check. Spot markets "most claims processed in 48 hours," but treat that as a marketing figure rather than a guaranteed timeline. There is no direct-to-vet payment option — you front the bill and wait to be repaid.

Why the ratings disagree

Here's the puzzle. On Trustpilot, Spot scores a glowing 4.7 out of 5 across thousands of reviews — but that's a company-claimed profile, which tends to surface happier customers. The Better Business Bureau, where Spot is an accredited "A+" business, shows a customer-review average of just 2.94 out of 5, and Spot's app sits near 2.7 stars on Google Play. The truth lives in that gap: plenty of owners are genuinely happy, and a vocal minority feel burned.

The happy stories are real: in owner communities you'll find plenty of accounts of Spot reimbursing accident and illness bills smoothly and paying quickly. The complaints cluster exactly where the fine print predicts — pre-existing and bilateral-knee denials, sticker-shock renewal increases, and friction when cancelling. Individual payout amounts resist a tidy number — what gets reimbursed depends on your deductible, reimbursement rate, limit, and whether the condition is covered at all — so the signal worth trusting isn't any one anonymous claim story but the consistent pattern of who ends up satisfied and who ends up frustrated.

Two caveats keep this honest. First, we're deliberately not quoting a single NAIC complaint index for Spot — its underwriters write many insurance lines well beyond Spot's pet book, so any per-company complaint number reflects that whole business, not Spot specifically. Second, because Spot shares its claims back office with sibling brands like Pumpkin and ASPCA, some of what you'll read about "Spot's" service really belongs to the shared platform.

Spot vs. Pumpkin: Two Brands, One Roof

The most surprising thing about "Spot vs. Pumpkin" is that it's barely a rivalry. Both brands sit under the same parent, Independence Pet Holdings, and draw on the same two underwriters (Spot, Pumpkin). You're not really comparing two companies — you're comparing two plan designs built on one chassis.

So the basics line up: both use annual deductibles, both apply a 14-day waiting period with no separate cruciate wait, and both include vet exam fees in the base plan. Where they diverge is in the dials and the wellness add-on.

| Feature | Spot | Pumpkin |

|---|---|---|

| Reimbursement options | 70%, 80%, or 90% | 80% or 90% |

| Deductible options | $100 / $250 / $500 / $750 / $1,000 | $100 / $250 / $500 / $1,000 |

| Annual limits | $2,500 up to unlimited (lowest option $2,500) | $5,000 up to unlimited (lowest option $5,000) |

| Waiting period | 14 days; no separate cruciate wait | 14 days; no separate cruciate wait |

| Exam fees in base plan | Yes | Yes |

| Wellness add-on | Preventive Care rider (Gold/Platinum), reimburses to a cap | Preventive Essentials — a non-insurance routine-care package |

Table sources: each brand's own plan and underwriting pages (Pumpkin FAQs). The sharpest difference is wellness: Spot's Preventive Care is a tiered rider on the insurance policy, while Pumpkin's Preventive Essentials is explicitly not insurance — a separate refund package for routine care (Pumpkin).

So which wins? It depends on your situation:

- Want the lowest entry price, or a low deductible-and-limit combo? Spot's $2,500 annual-limit floor and 70% reimbursement option let you build a lower-premium plan than Pumpkin's structure allows. Because the two share carriers and a platform, neither is reliably cheaper for a given pet — so quote both for identical coverage rather than assuming.

- Want a higher minimum annual limit? Pumpkin's lowest annual-limit option is $5,000, where Spot lets you go as low as $2,500 — so some owners prefer Pumpkin's higher entry point rather than risk bumping into a small cap. Just keep in mind an annual limit is the ceiling on what a plan reimburses in a year, not a guaranteed payout; the deductible, reimbursement rate, and exclusions still apply.

Because they share a chassis, the honest move is to quote both for identical coverage and choose on price and the wellness structure you'll actually use. For the full side-by-side across every carrier pairing, see our pet insurance comparison hub.

How to Cancel Spot Pet Insurance

Spot has no one-click cancel button in its member portal — the most common gripe we saw about leaving — so plan to reach a person. To cancel, contact Spot's service team by email at service@customer.spotpetins.com or by phone at the customer-service number in your policy documents, and ask them to confirm the cancellation in writing (Spot).

A few practical notes on timing and refunds. You can cancel by email, phone, or in writing, and Spot's policy says it refunds any premium already paid for coverage periods after your cancellation takes effect — and a cancellation in the first 30 days is fully refundable as long as no covered expenses have been applied to your deductible or reimbursed (Spot sample policy). Because premiums are billed as monthly installments, time it before the next payment date and keep the confirmation email. And remember the switching rule: putting a new policy in force before you cancel avoids a lapse in coverage dates, but the new plan's own waiting periods mean its coverage for accidents or illnesses may not start right away — and it does not erase a condition's pre-existing status. The next insurer can still treat an already-recorded condition as pre-existing, so check the new plan's exclusions and waiting periods before you drop Spot.

Frequently Asked Questions

Is Spot Pet Insurance legit and reliable?

Yes. Spot is a legitimate program whose policies are issued by licensed, financially sound insurers — United States Fire Insurance Company (AM Best A+, effective 2025) or Independence American Insurance Company (AM Best A-, affirmed December 2025), depending on your state (AM Best, Insurance Journal). Spot itself is the brand and selling agency, not the risk-bearer, so the company that actually pays your claim is one of those two carriers. It does pay real claims, though public reviews are split — glowing on Trustpilot, more critical on the BBB.

Who underwrites Spot Pet Insurance?

Spot policies are underwritten by either Independence American Insurance Company (NAIC #26581) or United States Fire Insurance Company (NAIC #21113), depending on your state — Spot tells you to check your policy forms to see which one is yours (Spot). The two carriers roll up to different parents: Independence American to Independence Pet Holdings (JAB), and United States Fire to Crum & Forster (Fairfax Financial).

Do vets accept Spot Pet Insurance?

Effectively any licensed U.S. vet works with Spot, because Spot is a reimbursement plan, not a network. You pay your vet directly, then file a claim and Spot reimburses you by direct deposit or check — there's no vet-side billing or approved-provider list. You have up to 270 days from the date of service to submit a claim.

How long is Spot's waiting period?

Spot's standard waiting period is 14 days for accidents, illnesses, and knee/ligament conditions, with no separate months-long orthopedic wait (Spot sample policy) — though in select states accident coverage can start the next day (Spot). The catch: a knee or ligament problem that appears before or during that wait can be excluded as pre-existing, and Spot treats the two knees as related.

Does Spot cover pre-existing conditions?

Not the ones your pet already has — like most U.S. pet insurers, Spot excludes conditions that are pre-existing under your policy. But it does offer a 180-day "cure-back": a curable condition that stays symptom- and treatment-free for 180 days can be covered again as new (Spot sample policy). That grace window does not apply to chronic conditions or to knee and ligament conditions, which stay excluded.

What does Spot not cover?

Spot doesn't cover pre-existing conditions, the second knee when the first knee's problem was pre-existing (it appeared before coverage or during the waiting period), routine or wellness care unless you buy the Preventive Care add-on, or things like breeding, cosmetic procedures, and most non-therapeutic prescription food. It's the standard accident-and-illness exclusion set — with the bilateral knee rule being the one that surprises owners most.

How much does Spot Pet Insurance cost?

In 2026 sample quotes, a young dog ran roughly $35–$70 a month and a young cat about $17, rising steeply with age — a senior dog can top $170 (NerdWallet). Add the optional Preventive Care wellness rider — about $9.95 (Gold) or $24.95 (Platinum) a month — and your true cost climbs accordingly. Expect renewal increases as your pet ages, since Spot rates on age and breed, not your claim history.

Is Spot the same company as Pumpkin or ASPCA?

Not the same brand, but the same corporate family. Spot and Pumpkin name the same two underwriters and share a parent, Independence Pet Holdings (Pumpkin), and the ASPCA-branded pet plan is part of that same Independence Pet group — which is why the plans look so alike. They still differ in plan design and price, so if you're weighing them, get a quote from each for identical coverage and compare before you buy.

Sources

- Insurance Underwriting Information — Spot Pet Insurance

- Underwriting Information — Pumpkin Pet Insurance

- Pumpkin Pet Insurance FAQs (plan terms) — Pumpkin Pet Insurance

- Pumpkin Preventive Essentials (non-insurance wellness) — Pumpkin Pet Insurance

- Does Pet Insurance Cover Exam Fees? — Spot Pet Insurance

- Spot Pet Insurance Review — CNBC Select

- Spot Pet Insurance Review (sample premiums, multi-pet discount) — NerdWallet

- State of the Industry Report 2025 (U.S. average premiums) — NAPHIA

- Spot Pet Insurance — Preventive Care tiers (Gold/Platinum benefit caps) — Mercer / Belk Benefits

- Spot Accident & Illness Sample Policy (form PET-P-20000-1024) — Spot Pet Insurance / Independence American Insurance Company

- What Is the Waiting Period in Pet Insurance? — Spot Pet Insurance

- What Is a Deductible in Pet Insurance? — Spot Pet Insurance

- What Is an Annual Limit in Pet Insurance? — Spot Pet Insurance

- Independence Pet Holdings Acquires Spot Pet Insurance — Insurance Journal

- United States Fire Insurance Company — AM Best Rating (A+, ultimate parent Fairfax Financial) — AM Best

- AM Best Affirms Independence American Insurance Company Ratings (A-, $125M parent contribution) — Insurance Journal

- Submitting a Claim (270-day filing window; service contact) — Spot Pet Insurance

- Spot Pet Insurance Reviews (4.7/5) — Trustpilot

- Spot Pet Insurance Services, LLC — Customer Reviews (A+ accredited, 2.94/5) — Better Business Bureau

- Spot Pet Insurance app (Google Play rating) — Google Play