"Wagmo" isn't one product — it's a brand covering two very different things, and knowing which one you have changes everything. Wagmo Wellness is a routine-care membership that reimburses preventive costs like exams and vaccines; its own membership agreement states plainly that it "is not an insurance product." Wagmo Insurance is a separate accident-and-illness policy, sold on its own and carried by an outside underwriter.

That split is where most reviews — and most buyers — go wrong, especially anyone who got Wagmo through their employer. If that's you, you almost certainly have the wellness membership, not insurance.

Then there's the part nearly every ranking page missed: in 2026 Wagmo's insurance moved to a new underwriter, which quietly dates much of the advice you'll find elsewhere.

This is an honest, licensed-agent review — no hype, no "starting at" teaser pricing. We'll help you figure out which Wagmo you actually have, who stands behind it now, what it really costs, how claims pay out, and whether it's worth it for your pet and your situation.

Table of Contents

- Wagmo at a Glance: Verdict, Pros & Cons

- Which Wagmo Do You Actually Have? Wellness Membership vs. Insurance

- Who Underwrites Wagmo, and What Changed in 2026

- Wagmo Wellness: What It Covers and Whether It's Worth It

- Wagmo Insurance: Coverage, Exclusions & Waiting Periods

- What Wagmo Really Costs

- Filing a Claim (and Why Claims Get Denied)

- What Real Customers Say (Reddit, Trustpilot, BBB)

- Who Wagmo Is (and Isn't) Right For

- Frequently Asked Questions

- Sources

Wagmo at a Glance: Verdict, Pros & Cons

Whether Wagmo is "worth it" depends on which of its two products you mean — and who you are. There isn't one answer, so here's ours, split by the reader we think you are.

- Buying Wagmo Wellness (routine care): Worth it only if you'll use enough preventive care to clear your tier's capped annual reimbursement — and you pay annually, because the monthly plan can bill you back when you cancel.

- Buying Wagmo Insurance (accidents & illness): A legitimate mid-market policy, now backed by an underwriter with an A- (Excellent) rating from AM Best — but not the bargain the "starting at $13" ads suggest. Compare it on price before you commit.

- You got Wagmo through work: You almost certainly have the wellness membership, not insurance. Accident-and-illness coverage is a separate purchase.

- You were just non-renewed in the 2026 switch: Read the underwriter section below first — the pre-existing waiver does not carry knee and ligament conditions across the change.

What we like: wellness claims that pay unusually fast — often about 24 hours; an A-rated carrier now standing behind the insurance; and useful extras like vet telehealth and a multi-pet discount.

What gives us pause: the two-product confusion is the single biggest reason buyers feel misled; on a like-for-like configuration Wagmo isn't cheap — its average premiums sit around the U.S. average, not below it; and claims are documentation-strict with no pre-approval, against a small and currently unhappy public review record. We unpack each below.

Which Wagmo Do You Actually Have? Wellness Membership vs. Insurance

Before you judge Wagmo, figure out which product is yours — because "Wagmo" sells two, and they run on completely different contracts. Here's the 30-second version.

- You have Wagmo Wellness if your plan reimburses routine care — exams, vaccines, routine bloodwork, dental cleanings, flea/tick/heartworm prevention — usually for a flat monthly fee with no deductible.

- You have Wagmo Insurance if you chose a deductible, a reimbursement percentage, and an annual limit, and the plan pays toward accidents and illnesses.

- Got it through your employer or a benefits portal? It's almost always the wellness membership, not insurance — but confirm which product you actually enrolled in. Wagmo's own member FAQ describes pet insurance as a separate add-on you activate in the app, not something bundled into the employer benefit.

The distinction isn't marketing — it's legal. Wagmo's membership agreement states outright that Wagmo Wellness "is not an insurance product," and it excludes any diagnostics or treatment for an accident, illness, or emergency. So if your dog swallows a sock, the wellness membership won't help — that's what the insurance policy is for.

| Wagmo Wellness | Wagmo Insurance | |

|---|---|---|

| What it is | A routine-care reimbursement membership | An accident & illness insurance policy |

| Is it insurance? | No — a membership, not a policy | Yes — a regulated policy |

| What it pays for | Exams, vaccines, routine bloodwork, dental cleaning, parasite prevention | Accidents, injuries, illnesses, surgery, and the diagnostics behind them |

| Who stands behind it | Wagmo (it administers the membership) | An outside insurance carrier — not Wagmo itself (see the next section) |

| How you got it | Direct sign-up or an employer benefit | A separate direct purchase |

One more trap: Wagmo is not Wag! Wag! (wagwalking.com) is a separate dog-walking company that also sells a "not insurance" wellness plan, so reviews and complaints for one get mistaken for the other. Make sure whatever you're reading is actually about Wagmo (wagmo.io).

Who Underwrites Wagmo, and What Changed in 2026

Wagmo doesn't carry the insurance risk itself — it's the brand and administrator, while a licensed insurance company actually backs your policy and pays claims. As of 2026, that carrier is Independence American Insurance Company (IAIC), administered by PTZ Insurance Agency, with United States Fire Insurance Company standing in for policies in New York and Washington. That's a change: older Wagmo policies were underwritten by National Specialty Insurance Company through Boost.

For anyone asking "is Wagmo legit," the company now behind the insurance is financially sound: IAIC holds an A- (Excellent) rating from AM Best, the agency that grades an insurer's ability to pay claims.

If you already hold a Wagmo policy, this affects you. Legacy policies are being non-renewed and moved onto the new IAIC form, and Wagmo has asked members to opt in to the replacement rather than roll over automatically. So if you're a current customer, don't assume you're still covered on the old terms — confirm your new policy is active and check whether you're on the IAIC or U.S. Fire form for your state.

One thing to check closely: when you're moved to the new policy, the terms around your pet's existing conditions can change. A replacement offer may include a waiver that carries some prior conditions over, but exactly which conditions are covered — and any exceptions or eligibility rules — depends on the specific offer you're given. Before you re-enroll or switch, read your own transfer paperwork so you know what's carried over and what isn't.

This is also why so much Wagmo advice online is quietly out of date: major review sites still name the old underwriter, which means the deadlines, waiting periods, and exclusions they quote may describe a policy form you can no longer buy. When the details matter, your own declarations page is the source that wins.

Wagmo Wellness: What It Covers and Whether It's Worth It

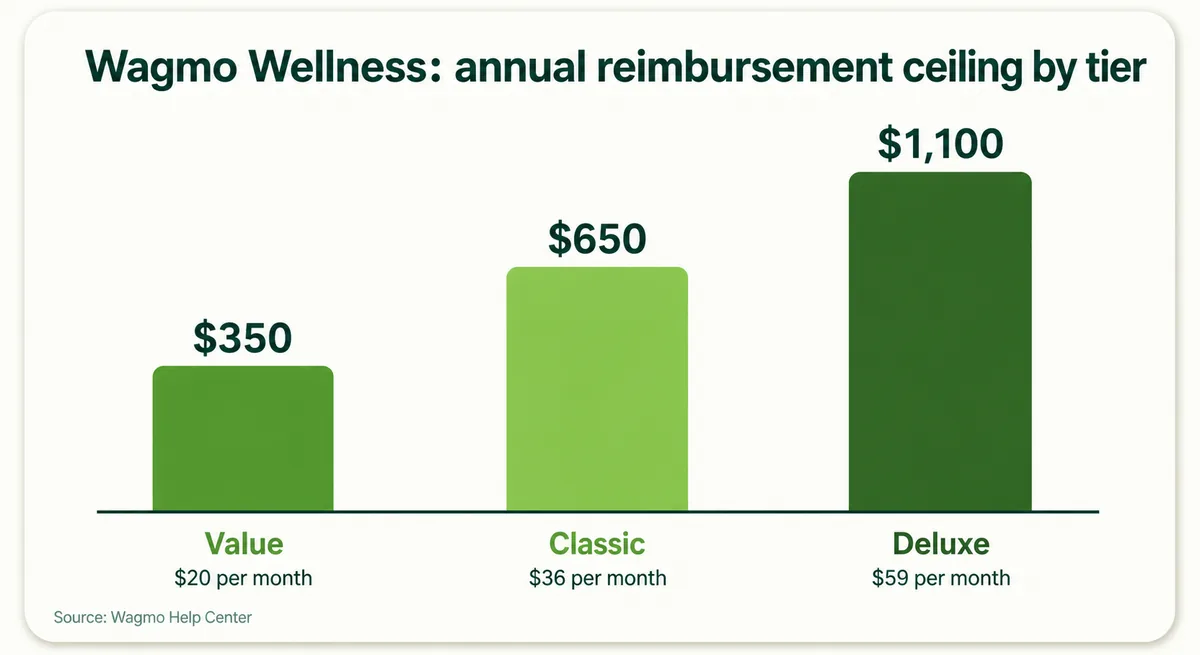

Whether the wellness membership is worth it comes down to arithmetic: you pre-pay a monthly fee and get reimbursed for routine care up to a fixed annual ceiling, so it pays off only if you'll actually claim more than you put in. Wagmo sells it in three tiers.

Per Wagmo's plan details, they run roughly Value (about $20/month, up to ~$350 back a year), Classic (about $36/month, up to ~$650), and Deluxe (about $59/month, up to ~$1,100). Treat those ceilings as the best case, not the expected case.

Here's the catch: every benefit is capped by a dollar amount or a number of visits, whichever runs out first — and the per-category caps (think roughly $100 toward an exam, $100 toward routine bloodwork, $50 toward a fecal test) often sit at or below what a clinic actually charges. To reach the headline ceiling you'd have to use nearly every category to the max. On the Classic tier, for instance, you're paying about $432 a year, so you only come out ahead if you genuinely claim more than that in covered routine care.

One more thing worth knowing: if you take your pet in because something seems wrong, that visit — and the bloodwork to diagnose it — isn't a wellness claim; the membership excludes symptom-driven care. Those costs are covered only if you separately hold Wagmo Insurance and the visit qualifies under that policy. So the membership handles healthy-pet maintenance, not the "is my dog okay?" visits.

The Cancellation Clawback (What Leaving Can Cost)

This is the counterintuitive part, and it only bites monthly members. Under Wagmo's membership agreement, if you cancel a monthly plan mid-year after Wagmo has reimbursed you more than you've paid in, you can be billed the difference back — at full retail, with any membership discounts reversed. In other words, using the plan heavily and then leaving can leave you owing Wagmo money. Annual plans cancelled after claims are paid don't carry that clawback fee, so if you expect to use the plan heavily, paying annually sidesteps that particular risk — just weigh it against prepaying a full year up front, and confirm the refund and cancellation terms for your plan. (New members get a short 24-hour free-look window, and a failed payment triggers a small reprocessing fee.)

Wagmo Insurance: Coverage, Exclusions & Waiting Periods

Wagmo Insurance is a fairly standard accident-and-illness policy: after you meet a deductible, it reimburses a percentage of the covered vet bill up to an annual limit. Wagmo's current plans let you choose from these options, per NerdWallet's recent Wagmo quotes (exact availability can vary by state):

| Choice | Options |

|---|---|

| Annual deductible | $250, $500, or $1,000 |

| Reimbursement rate | 70%, 80%, or 90% |

| Annual payout limit | $5,000, $10,000, $20,000 (or unlimited, by phone) |

Here's how that plays out: say your dog needs $4,000 of covered treatment, and you chose the $250 deductible with 80% reimbursement. Wagmo would pay 80% of the $3,750 left after the deductible — about $3,000 — as long as you're under your annual limit. A higher reimbursement rate or lower deductible pays more but costs more each month, which is the trade-off every plan asks you to make.

Wagmo lists a waiting period of about 14 days in most states for accidents and illnesses, and some conditions can carry a longer wait; the exact windows vary by state and policy form, so check your own policy. As with every pet insurer, pre-existing conditions aren't covered. Some insurers treat certain conditions as "curable" and cover them again after a symptom-free period, but whether Wagmo's current policy does that — and on what terms — is something to confirm in your own policy documents.

One practical limitation: Wagmo can't pre-approve a claim. You won't know the exact payout until after you've paid the vet and filed, which matters most before a big, planned procedure.

Watch the date on older reviews. Some still describe a 50% penalty on prescription medications and a six-figure lifetime cap — those come from the older National Specialty form, not necessarily the policy you'd buy today. Don't assume those legacy figures apply; confirm the prescription terms, any sub-limits, and whether your ceiling is an annual or lifetime maximum against your own current policy. If a figure you're reading doesn't match the options above, it may be describing a plan Wagmo no longer sells.

What Wagmo Really Costs

The low "starting at" price in Wagmo's ads is a marketing floor, not what most people pay. Look at a real, configured quote and Wagmo lands around the national average — not below it.

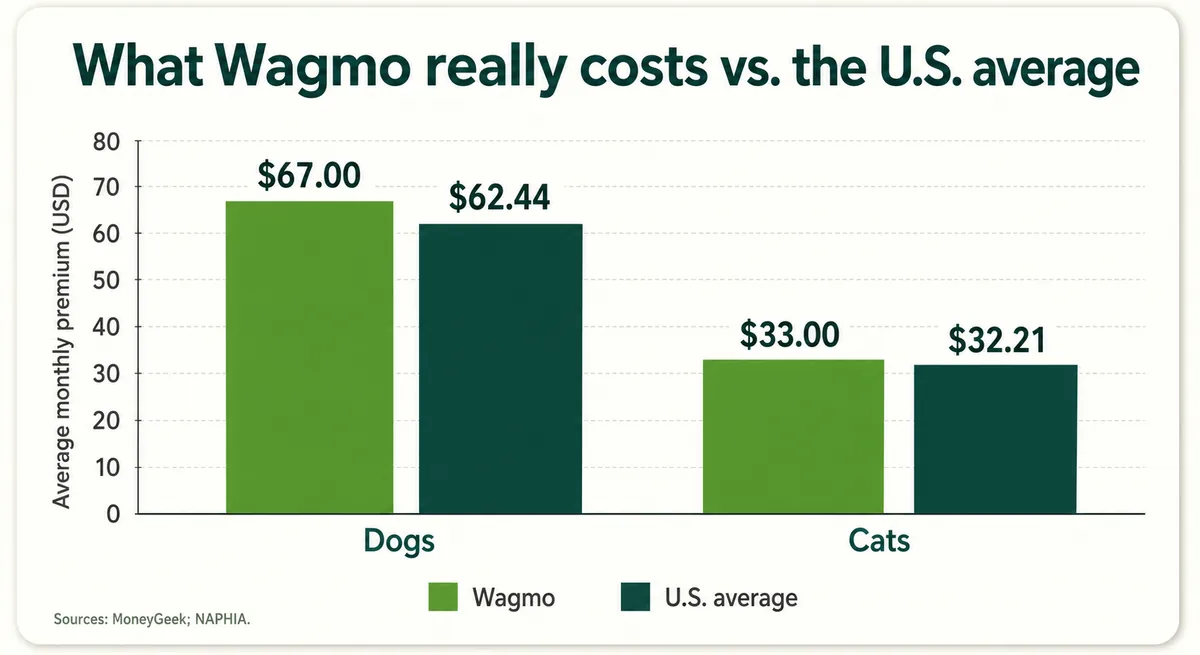

Start with that headline. Wagmo markets a low teaser price, but the pet, age, and coverage settings behind any "starting at" figure aren't disclosed — so treat it as a best case, not a typical bill. A configured quote tells a different story: for a two-year-old pet at a $250 deductible, $5,000 annual limit, and 80% reimbursement, NerdWallet's Wagmo quote came to about $39/month for a dog and $19 for a cat. Wagmo's average premiums, meanwhile, run about $67/month for dogs and $33 for cats — roughly in line with the U.S. accident-and-illness averages of $62.44 for dogs and $32.21 for cats (the two are measured on different samples, but it's a useful benchmark).

So the honest takeaway: once you compare like for like, Wagmo isn't a discount insurer. That doesn't make it a bad buy — it makes "cheap" the wrong reason to choose it. You'll also see different Wagmo prices quoted in different reviews, because each uses a different deductible, limit, and reimbursement mix; that's exactly why the configuration matters more than the sticker. Price Wagmo against a couple of competitors at the same settings, then judge it on coverage and service. (For how those levers move your premium, see our guide to what pet insurance costs.)

Filing a Claim (and Why Claims Get Denied)

With Wagmo you generally pay the vet first and file for reimbursement afterward — there's no pre-approval, so whether you get paid comes down to documentation and timing.

The standard route is owner-reimbursement: you submit a fully itemized invoice — the clinic's details, your pet's name, and line-item charges — plus proof that you paid it in full, per Wagmo's help center. That's where claims tend to fall apart: a handwritten or non-letterhead invoice, or a receipt without an itemized breakdown, can be bounced. A related and common trap is reclassification — if you bring your pet in because something seems wrong, that symptom-driven visit isn't a "wellness" claim, so the membership won't pay it (it's covered only if you separately hold insurance and the visit qualifies).

Deadlines matter, and there isn't one universal number — the filing window varies by policy form and state, and older Wagmo policies used tighter deadlines than newer ones. Don't rely on a figure you read in a review: the deadline that governs you lives in your own policy's claim-notice or proof-of-loss terms (plus any state notices), so confirm it there — or ask Wagmo in writing — before you assume you have months.

One nuance worth asking about: some policies can send the reimbursement to your treating vet "as designated by you" rather than to you, though there's still no direct vet-portal submission — your vet just supplies the records. Whether that option is available, and whether it changes the pay-first requirement, depends on your policy, so confirm it in advance if it matters to you.

What Real Customers Say (Reddit, Trustpilot, BBB)

Treat Wagmo's public reviews as sentiment, not a scorecard — the samples are small and self-selected, so they tell you what frustrates (and delights) people, not how often it happens. With that caveat, a few themes come through clearly.

The loudest, by mid-2026, is the carrier transition itself. On Reddit and the review sites you'll find owners calling the switch a "money grab," saying service "got worse after the first year," or that their plan was being discontinued. Read in context, that's transition friction — the 2026 non-renewal covered above — more than random bad luck. The second recurring theme is wellness-versus-insurance confusion: people who thought they'd bought insurance and later realized they held a wellness membership. The third is claim friction: denials and delays tied to documentation.

It isn't all negative. The most consistent praise is speed — wellness reimbursements that land in a day or two are a genuinely popular feature, and the reason some members stay.

On the scores, watch the dates. Older aggregator snapshots still circulate weaker numbers — MoneyGeek, for example, lists a D+ BBB grade and a 3.4 Trustpilot score — but those lag the live profiles. As of mid-2026, Wagmo's live Trustpilot page sits closer to 2.6 out of 5 across only about a dozen reviews, while its BBB profile actually shows a stronger letter grade despite the company not being BBB-accredited. Either way the raw counts are tiny — a reason to weigh the themes above the star rating. (We found no meaningful Wagmo discussion on Quora, so nothing here leans on it.)

Who Wagmo Is (and Isn't) Right For

There's no single verdict on Wagmo — it fits some situations well and others poorly. Here's our honest read by who you are.

- Routine-care buyers (the wellness membership): Worth it only if you'll use enough preventive care to beat your tier's capped ceiling — and you pay annually to sidestep the cancellation clawback. If your pet sees the vet lightly, you'll probably pay in more than you get back.

- Accident-and-illness buyers (the insurance): A legitimate, A-rated mid-market policy — just don't buy it expecting a discount. Get quotes from a couple of competitors at the same deductible, limit, and reimbursement rate, then choose on coverage and service.

- Employer-plan holders: You have a wellness membership, not insurance. That's fine for routine costs, but if you want protection against a big accident or illness, you'll need to add real insurance separately.

- Senior-pet or pre-existing-condition owners: Read the fine print hardest. Pre-existing conditions won't be covered, and if you're crossing the 2026 carrier switch, the waiver may not carry knee and ligament problems — exactly the pricey, recurring issues you'd most want protected.

Whichever bucket you're in, the smart next step is the same: compare. Put Wagmo beside a couple of other carriers at identical settings and judge it on the merits, not the "starting at" price. And if you found this page because you were just non-renewed, focus on switching cleanly — with your pet's records in order — rather than reflexively re-enrolling into whatever's offered.

Frequently Asked Questions

Is Wagmo a good pet insurance?

It can be, but the honest answer depends on which Wagmo product you mean and what you compare it to. Wagmo's accident-and-illness insurance is a legitimate, mid-market policy now backed by an A-rated carrier — but once you normalize the coverage settings, it isn't the bargain its “starting at $13” ads suggest. Judge it against a couple of competitors at the same deductible, limit, and reimbursement rate rather than on the sticker price.

How much does Wagmo pet insurance cost per month?

Wagmo markets a low “starting at” teaser price, but it hides the coverage settings behind it. A configured quote — a two-year-old pet at a $250 deductible, $5,000 limit, and 80% reimbursement — runs closer to $39/month for a dog and $19 for a cat, and Wagmo's average premiums land around the U.S. average, not below it. The wellness membership is priced separately, by tier.

Does Wagmo cover surgery?

Yes — Wagmo's insurance covers surgery when it stems from a covered accident or illness (a torn ligament, a swallowed object, cancer), subject to your deductible, reimbursement rate, waiting periods, and any exclusions. What it won't cover is surgery tied to a pre-existing condition, or anything billed to the wellness membership, which is for routine care only. The exact terms live on your policy's declarations page, so check yours before a planned procedure.

What is the most highly rated pet insurance?

There's no single “most highly rated” pet insurer — ratings shift by source and methodology, and the right pick depends on your pet's age, breed, and budget. Editorial scorecards, customer-review sites, and financial-strength grades often disagree, so treat any “best” list as a starting point, not a verdict. We'd rather you compare a shortlist on coverage, exclusions, and price for your own situation; our carrier reviews lay each one out the same way.

Is Wagmo worth it for a senior pet?

Often only partially. Any pre-existing conditions your older pet already has won't be covered by Wagmo's insurance — and if you're moving across the 2026 carrier change, the pre-existing waiver may not carry knee and ligament issues. The wellness membership can still defray routine senior care like bloodwork and dental cleanings, if you'll use enough of it to beat the cap. For a senior pet with existing issues, price the realistic coverage before you enroll.

Is a Wagmo plan through my employer the same as pet insurance?

No. A Wagmo plan offered through your employer is almost always the wellness membership, which reimburses routine care and is contractually not insurance. It won't pay for an accident or a serious illness. If you want that protection, you add a separate Wagmo insurance policy (or buy insurance elsewhere). It's worth confirming which one you have before you need it, because the two run on completely different contracts.

Is Wagmo legit?

Yes. Wagmo is a real company, and its current insurance is underwritten by Independence American Insurance Company in most states (and United States Fire Insurance Company in New York and Washington), with IAIC carrying an A- (Excellent) financial-strength rating. Much of the recent negative buzz traces to its 2026 carrier transition — non-renewals and re-enrollment — rather than to any fraud. The fair criticisms are about price-versus-value and claims documentation, not legitimacy. Just be sure you know whether you hold the wellness membership or the insurance policy.

Sources

- Wagmo Wellness Universal Membership Agreement — Wagmo

- Wagmo — Updates (2026 insurance underwriting change) — Wagmo

- Independence American Insurance Company — Independence American Insurance Company

- Wagmo Wellness Member FAQ — Wagmo

- Wagmo Pet Insurance Review — MoneyGeek

- AM Best — Independence American Insurance Company rating action (A- affirmed) — AM Best

- Wagmo — Legacy Sample Policy (National Specialty / Boost) — Wagmo

- What's included in each Wagmo Wellness plan (Value/Classic/Deluxe) — Wagmo Help Center

- Wagmo Pet Insurance Review — NerdWallet

- Wagmo Pet Insurance Plans — Wagmo

- State of the Industry Report 2025 (U.S. average premiums) — NAPHIA

- Wagmo Help Center (claims and coverage) — Wagmo

- Wagmo reviews — Trustpilot