If you're weighing MetLife pet insurance in 2026, you probably have two questions at once: is it actually any good? and who really stands behind it? That second question matters more than most reviews let on — because "MetLife" here is a brand, not a single insurer. We read MetLife's own policy, its underwriters' financial-strength ratings, and what real owners report at claim time, so you don't have to.

The short answers first. Yes, it's a real, widely-used pet insurer — MetLife sells accident-and-illness coverage for dogs and cats in all 50 states and reimburses a percentage of your eligible vet bill — after your deductible and up to your annual limit — at reimbursement rates of 50%, 70%, 80%, or 90%. And no, MetLife doesn't underwrite the policy itself: your coverage is issued by one of two carriers — Metropolitan General or Independence American, depending on your state and policy form — and administered by the company MetLife bought in 2019, the former PetFirst.

So this is a "should you — and which MetLife do you actually have" decision, not a simple star score. Below, we give a conditional verdict for the two readers who usually land here: someone shopping MetLife on their own, and the many who are offered it as a benefit at work and just want to know whether to take it.

Table of Contents

- The Verdict: Is MetLife Worth It (and Who's It For)?

- Who Actually Underwrites MetLife (MetGen vs. IAIC)?

- What MetLife Covers (and the Current Plan Menus)

- Waiting Periods, Pre-Existing & the Fine Print

- What MetLife Costs — Now and as Your Pet Ages

- The Family Plan: Shared Deductible vs. Shared Limit

- MetLife Through Your Employer (and the Portability Catch)

- Claims, Appeals & the Reimbursement-First Reality

- MetLife vs. the Alternatives

- Frequently Asked Questions

- Sources

The Verdict: Is MetLife Worth It (and Who's It For)?

Here's the short version most MetLife reviews bury: yes, it's a legitimate, often good-value policy — the real decision is which MetLife you're getting and whether its fine print fits your situation. MetLife's pitch is breadth and flexibility: one accident-and-illness plan you can dial from a 50% to a 90% reimbursement rate, annual limits from $500 to unlimited, exam fees and dental-illness and alternative therapy built in, and a genuine multi-pet Family Plan. The trade-offs are the reimbursement-first cash flow, a symptom-based pre-existing rule that catches people off guard, and premiums that climb steeply as your pet ages.

MetLife is a reasonable pick if you:

- are offered it at work — the 10% employer discount and a narrow pre-existing "portability" perk make the workplace version the strongest;

- are insuring a younger, healthy pet and want to customize the deductible, reimbursement rate, and annual limit rather than take a one-size plan;

- value breadth — exam fees, hereditary and chronic conditions, holistic care — over the rock-bottom premium.

Look elsewhere if you:

- can't comfortably float a big vet bill up front — MetLife reimburses you, it doesn't pay the clinic directly;

- have a pet with a problem that already shows up in its records — MetLife's symptom-based pre-existing rules will likely exclude it;

- are shopping purely on price — several rivals quote lower for the same pet, and MetLife's "starts at" figure isn't what most buyers actually pay.

The rest of this review settles what should actually decide it: who underwrites your policy, what the current fine print really does, what it costs over time, and what that employer-benefit version really gets you.

Who Actually Underwrites MetLife (MetGen vs. IAIC)?

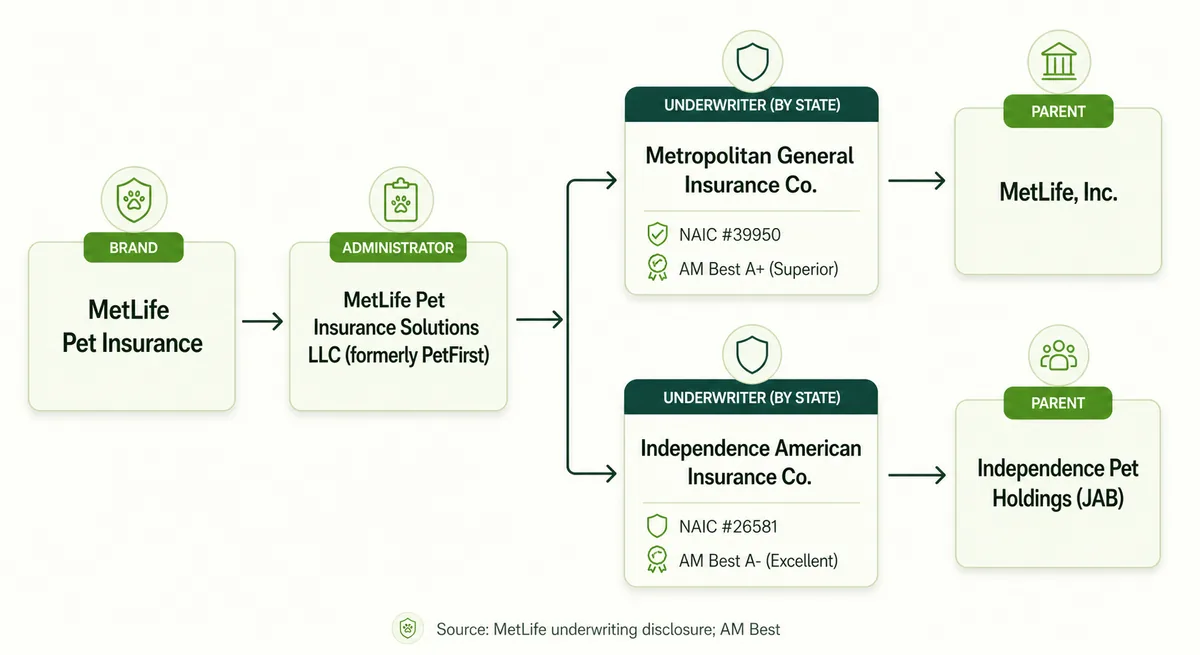

Here's what nearly every MetLife review skips: MetLife isn't the company that pays your claim. "MetLife Pet Insurance" is a brand, administered by MetLife Pet Insurance Solutions LLC — the former PetFirst Healthcare, the pet-insurance business MetLife acquired in 2019. The carrier that actually holds the risk is named on your policy, and it's one of two.

Per MetLife's own policy disclosures, your coverage is underwritten by either Metropolitan General Insurance Company ("MetGen") or Independence American Insurance Company ("IAIC"), depending on your state and policy form — and the two aren't identical. MetGen (NAIC #39950, a Rhode Island company) is a MetLife subsidiary, and AM Best rates it A+ (Superior) — the same top tier as MetLife's life-insurance companies. IAIC (NAIC #26581, a Delaware company) belongs to a different corporate family — Independence Pet Holdings, backed by JAB — and AM Best rates it two rungs lower, at A- (Excellent), a grade it had reaffirmed in December 2025 after its parent added $125 million in capital. Both are financially sound; just read the rating against the carrier on your policy, not the "MetLife" name.

That split isn't just trivia. Which carrier you land on can change the actual terms — the cruciate-ligament waiting period and the way the wellness add-on works differ between the MetGen and IAIC forms, as the next sections show. And here's the catch: MetLife won't publish a state-by-state map of which carrier you'll get. Its disclosure simply points you to your policy documents — so the only reliable way to know who stands behind your coverage is to read your own declarations page.

What MetLife Covers (and the Current Plan Menus)

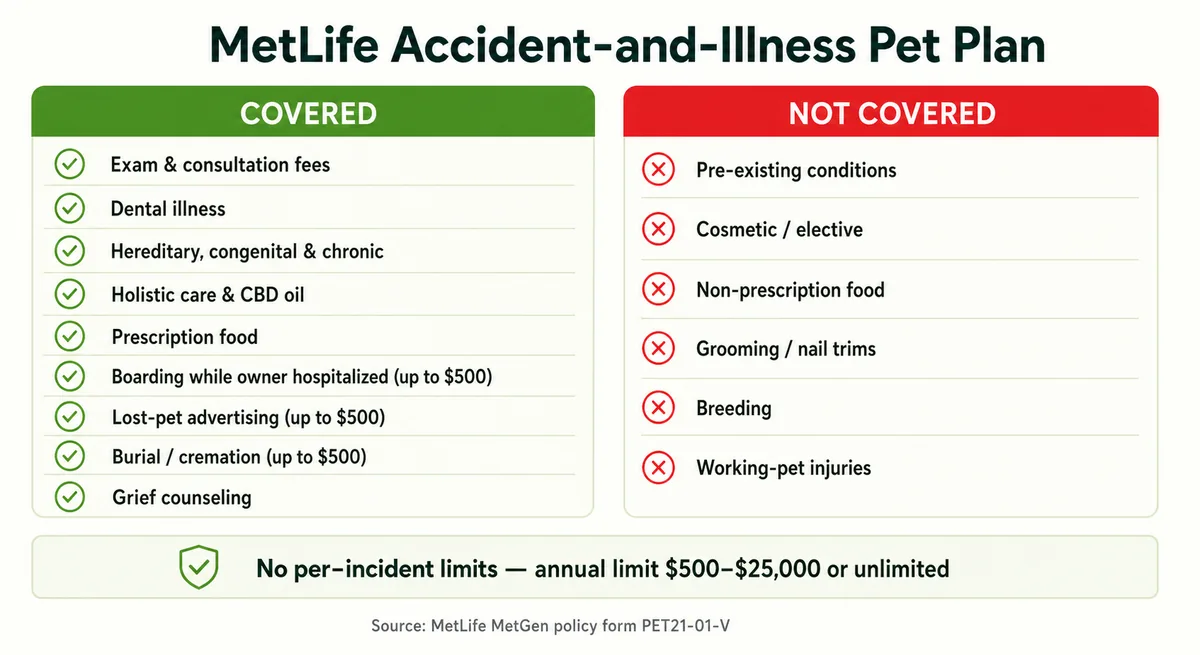

MetLife sells a single accident-and-illness plan — there's no separate accident-only product on the current lineup, despite what some older reviews still list. You set the dials yourself: a reimbursement rate of 50%, 70%, 80%, or 90%, an annual deductible anywhere from $0 to $2,500, and an annual limit from $500 all the way to unlimited — and, notably, no per-incident limits, so one catastrophic claim isn't capped below your annual number. If you've read that MetLife tops out at $10,000, that's stale: the higher limit tiers are real (some are call-in), and the menu is far wider than most review pages show.

The base plan is genuinely broad. It covers exam and consultation fees, dental illness, hereditary and congenital conditions, cancer treatment, and vet-prescribed alternative care (acupuncture, hydrotherapy, even CBD oil). It also folds in benefits comparison grids often miss: boarding if you're hospitalized (up to $500), lost-pet advertising (up to $500), a burial/cremation benefit (up to $500), and free grief counseling. There are no breed exclusions and no upper age limit to enroll.

What it won't cover is the usual list: pre-existing conditions, cosmetic and elective procedures, grooming and non-prescription food, breeding, and injuries from working or commercial use. And routine care isn't in the base plan — MetLife's optional Preventive Care add-on pays a fixed dollar amount per service (a $50–$75 exam, vaccines, a spay/neuter or a dental cleaning) from a set schedule, not a percentage. Treat it as budgeting for wellness, not real protection against a big bill.

Waiting Periods, Pre-Existing & the Fine Print

MetLife's waiting periods on the current form are genuinely short: accident coverage starts the day after you enroll, illness coverage begins after 14 days, and — importantly — there's no separate months-long wait for cruciate-ligament or orthopedic issues on the newer Metropolitan General policy form. If you've seen a "6-month cruciate wait" quoted, that's the older Independence American form — one more reason to check which carrier you're actually on.

The part that catches people out is how MetLife defines a pre-existing condition. It's symptom-based, not diagnosis-based: a condition counts as pre-existing if, before your coverage (or during a waiting period), your pet showed "signs or symptoms consistent with" it — even if no vet ever named the disease. A casual note about occasional vomiting, a symptom your vet jotted at a wellness visit, or a pre-adoption shelter record can all give MetLife grounds to call a later condition pre-existing — if it decides those earlier signs were "consistent with" it. Owners on Reddit describe exactly this: an allergy claim denied off a casual note about food sensitivity, or a newly adopted pet's illness ruled pre-existing because a symptom appeared inside the 14-day window.

A couple of things soften it. MetLife says a curable condition may be covered again once your pet has been symptom- and treatment-free for a while — though it doesn't publish a specific number of days, so don't count on a fixed timeline. And bilateral conditions (like cruciate tears or hip dysplasia) are judged per side. One protection worth knowing: under the NAIC's pet-insurance model law, the burden of proving a condition is pre-existing falls on the insurer, not you — but that protection is only binding in the growing number of states that have actually adopted the provision, so check whether yours has. Either way, a documented written appeal is worth filing. As always, the exact rules live on your declarations page and your state's form.

What MetLife Costs — Now and as Your Pet Ages

There's no single "MetLife price" — what you pay depends on the reimbursement rate, deductible, and annual limit you choose, plus your pet's species, breed, age, and ZIP code. MetLife advertises coverage starting at about $16 a month for a dog and $7 for a cat — but treat that as a marketing floor, not a budget. MetLife's own stated 2026 average is closer to $52 a month for dogs and $28 for cats, and the industry accident-and-illness average from NAPHIA runs about $62 and $32. A policy with real coverage usually costs three to four times that "starts at" number. For a wider view of what pet insurance costs across the market, the drivers are the same everywhere.

The part that stings: renewals

One of the loudest complaints about MetLife isn't denials — it's renewal increases, which tend to hit hardest as a pet ages. One owner on Reddit documented a senior dog's premium climbing from about $163 to $331 a month in roughly two years, with MetLife also trimming the reimbursement rate from 90% to 80% along the way (owner-reported figures, not MetLife's published rates). Vet prices are part of it — the government's vet-services index was up about 5% over the past year — but age is the dominant driver. A couple of things push the other way: a 10% discount if you enroll through an employer, and a "healthy pet" incentive that shaves $50 off your deductible for each claim-free year. Still, go in budgeting for the cost to climb; that, not the intro price, is the real "is it worth it" math.

The Family Plan: Shared Deductible vs. Shared Limit

MetLife is one of the few insurers that lets you cover up to three pets on a single policy — dogs, cats, or a mix. It's genuinely convenient, but it's a trade-off, not a discount, and it cuts both ways.

The upside is the shared deductible: instead of a separate deductible per pet, your whole household works toward one, so you hit it faster and start getting reimbursed sooner. The healthy-pet incentive that trims your deductible for each claim-free year applies to that single shared number, too.

The catch is the shared annual limit. A Family Plan pools one limit across all the pets with no per-pet sub-limits — so if one pet has a catastrophic year (or two need major care in the same policy year), that single household limit can be drawn down or exhausted, leaving the others with less coverage until it resets. Three separate policies would each carry their own full limit. And here's the part MetLife's marketing doesn't lead with: the multi-pet discount you'd earn by buying separate policies (5% for the second, 10% for each additional) isn't available on a Family Plan. So treat it as buying simplicity and one shared deductible — not a cheaper rate. For two healthy pets with modest expected claims it's often the easier call; for a household with one chronically expensive pet, separate policies may actually protect the others better.

MetLife Through Your Employer (and the Portability Catch)

Here's something the star ratings miss: most MetLife pet policies are sold as a workplace voluntary benefit — enrolled during open enrollment and paid straight out of your paycheck. If that's how you're being offered it, two things make the employer version genuinely the strongest — and one of them is easy to overstate.

First, the money: enrolling through an employer usually gets you a 10% discount on your premium (it's not available in Tennessee, and Minnesota calls it by another name). Second, and more valuable, is a narrow pre-existing-condition "portability" perk. Normally MetLife — like every insurer — won't cover a condition your pet already has. But it can carry over previously covered pre-existing conditions when you switch into a MetLife group policy without a gap in coverage, reimbursed at your new rate.

The catch is exactly who qualifies. In MetLife's own words, that pre-existing coverage is "only available to individuals with active pet insurance coverage that have purchased MetLife Pet Insurance as part of an employer group benefit offering." In plain English: you must already have active coverage (from any insurer), switch with no gap, and buy through your employer's group plan. A retail buyer walking in off the street gets none of it. And it's worth asking your benefits team what happens if you leave the job — the discount and this portability are tied to that employer offering, so confirm whether your policy simply continues before you count on it.

Claims, Appeals & the Reimbursement-First Reality

Filing a MetLife claim is straightforward — through the app or member portal, generally within 90 days of treatment — and when it goes smoothly, owners describe fast payouts by check or direct deposit. But there are two things to plan for. First, MetLife is reimbursement-first: you pay the vet in full at the counter and get paid back afterward, so you need the cash or credit up front — there's no paying the clinic directly. Second, your first claim triggers a records request: MetLife wants the last 12 months of your pet's medical records — specifically the vet's SOAP/chart notes, not just the invoice — to screen for pre-existing conditions (a recently adopted pet can submit an adoption contract instead). It's the single most common reason a first claim stalls.

The ratings are where MetLife gets confusing, because two very different pictures coexist. On Trustpilot, MetLife scores about 4.7 out of 5 across thousands of reviews — but that pool is dominated by reviews solicited at enrollment (easy signup, quick quote). Meanwhile the Better Business Bureau profile for the underlying company — MetLife Pet Insurance Solutions LLC, the former PetFirst — sits near 1.1 out of 5, with hundreds of complaints over three years. That gap isn't a contradiction; it's the story: enrollment is smooth, and the friction shows up at claim time, where owners report denials and appeals that get misrouted. Read the pattern, dated, rather than a single score — and if you're contesting a denial, put your appeal in writing.

MetLife vs. the Alternatives

MetLife rarely wins on price alone — its real edge is the employer channel and how much you can customize the plan. So the honest way to cross-shop is by what matters most to you:

- You're offered it at work. Between payroll deduction, the 10% group discount, and that narrow pre-existing portability, MetLife is genuinely hard to beat. Its closest employer-benefit rival is Nationwide, which also offers an unlimited-payout option.

- You want the lowest price for a young pet. App-first Lemonade is frequently cheaper for a healthy puppy or kitten, though it bundles in fewer of the supportive extras MetLife builds into the base plan.

- You hate fronting a big bill. MetLife is reimbursement-first — you pay the vet in full, then wait to be repaid. Trupanion can pay some clinics directly, which solves exactly that liquidity problem.

- You want a simple, high or unlimited limit. Healthy Paws strips its plan down to one uncapped limit; ASPCA, meanwhile, shares MetLife's willingness to re-cover a condition once it has cured.

The toughest case is the priced-out senior owner. Because any new insurer treats an existing condition as pre-existing, switching late is rarely clean — our guide to switching pet insurance walks through when a move pays off and when staying put wins.

Frequently Asked Questions

Who underwrites MetLife pet insurance?

One of two carriers, assigned by your state and policy form: Metropolitan General Insurance Company ("MetGen," NAIC #39950, Rhode Island, AM Best A+) or Independence American Insurance Company ("IAIC," NAIC #26581, Delaware, AM Best A-). Both are administered by MetLife Pet Insurance Solutions LLC. Which one backs your policy — and its exact terms — depends on where you live.

Is MetLife pet insurance the same as PetFirst?

Effectively, yes. MetLife acquired PetFirst Healthcare in 2019–2020 and renamed it MetLife Pet Insurance Solutions LLC, which administers the plans today. That lineage matters when you read reviews: the Better Business Bureau profile still lists the company under its former PetFirst name.

How does MetLife pet insurance pay out?

It's reimbursement-first: you pay your vet in full, file a claim, and MetLife pays you back — 50%, 70%, 80%, or 90% after your deductible — by check or direct deposit. There is no direct-to-vet payment, so you need the funds up front. MetLife says most claims are processed in about 5–10 days.

Does MetLife cover pre-existing conditions?

No — like every insurer, MetLife excludes pre-existing conditions, and its definition is symptom-based: a condition your pet merely showed signs of before coverage can be excluded even without a formal diagnosis. A curable condition may be re-covered after a symptom-free period. The one exception is a narrow portability perk available only when you buy through an employer group plan with no gap in prior coverage.

Do most vets take MetLife pet insurance?

Any of them. Because MetLife reimburses you rather than paying the clinic, there is no network — you can use any licensed veterinarian in the U.S., including specialists and emergency hospitals. The trade-off is that you settle the bill yourself and claim the reimbursement afterward.

How much does MetLife pet insurance cost?

MetLife advertises coverage starting around $16 a month for a dog and $7 for a cat, but treat that as a floor. MetLife's own stated 2026 average is about $52 for dogs and $28 for cats, and a policy with real coverage usually runs three to four times the "starts-at" price. Expect it to rise at each renewal as your pet ages.

Is MetLife pet insurance worth it through my employer?

Often, yes. Enrolling through work usually adds a 10% discount, comes out of your paycheck automatically, and unlocks a pre-existing-condition portability perk you can't get buying retail. The caveat: that discount and portability are tied to the employer offering, so ask your benefits team what happens to the policy if you leave the job.

Is MetLife a good pet insurance plan?

On its current MetGen form, it's genuinely strong — wide customization (50–90% reimbursement, annual limits up to unlimited), no per-incident limits, short waiting periods, and no breed exclusions. The friction points to weigh are its reimbursement-first structure, steep renewal increases as pets age, and a strict symptom-based pre-existing definition. It fits customization-minded and employer-benefit buyers best.

Why did my MetLife premium go up?

The dominant driver is your pet simply getting older, compounded by veterinary-cost inflation — the government's vet-services index rose about 5% over the past year. Two features push the other way: a "healthy pet" incentive that trims your deductible for each claim-free year, and the 10% employer discount. Even so, budget for the cost to climb over time.

Sources

- MetLife Pet Insurance — FAQs (issuer disclosure; reimbursement, deductible & annual-limit menus) — MetLife Pet Insurance

- MetLife Pet Insurance — Optional Preventive Care Coverage (scheduled wellness benefits) — MetLife Pet Insurance

- MetLife — Corporate Ratings (AM Best financial-strength ratings for MetLife's insurance companies) — MetLife, Inc.

- AM Best affirms Independence American Insurance Company A- after $125M parent contribution — Insurance Journal

- MetLife Pet Insurance — Pre-Existing Conditions (symptom-based definition; curable; bilateral) — MetLife Pet Insurance

- NAIC Pet Insurance Model Act #633 (insurer burden of proof; 30-day waiting-period cap) — National Association of Insurance Commissioners

- DO NOT get pet insurance through MetLife (owner reports a symptom-based pre-existing denial) — Reddit — r/puppy101

- MetLife Pet Insurance — How Much Does Pet Insurance Cost? (starts-at floor; 2026 averages) — MetLife Pet Insurance

- State of the Industry Report 2025 — US accident-and-illness average premiums (dogs $749/yr, cats $386/yr) — NAPHIA

- CPI — Veterinarian services (12-month change) — U.S. Bureau of Labor Statistics

- MetLife premium increasing by $147 (owner-reported senior-pet renewal escalation) — Reddit — r/petinsurancereviews

- MetLife Pet Insurance from Employers (voluntary-benefit channel; 10% discount; pre-existing portability footnote) — MetLife Pet Insurance

- MetLife Pet Insurance — Trustpilot (≈4.7/5 across 10,000+ reviews, solicited-at-enrollment) — Trustpilot

- MetLife Pet Insurance Solutions LLC (formerly PetFirst) — BBB profile (~1.1/5; hundreds of complaints) — Better Business Bureau

- MetLife MetGen Pet Insurance Policy (sample form PET21-01-V) — MetLife