If you're weighing Fetch pet insurance in 2026, you probably have two questions at once: is it actually any good? and who really stands behind it? That second question matters more than most reviews admit — because "Fetch" is a brand and a managing general underwriter, not the company that actually pays your claim. We read Fetch's policy, its underwriters' financial-strength ratings, and what real owners report at claim time, so you don't have to.

The short answers first. Yes, it's a legitimate, widely-used insurer with unusually broad coverage — sick-visit exam fees, dental for every adult tooth, behavioral therapy, and virtual vet visits — and it reimburses a percentage of your actual vet bill rather than a fixed benefit schedule. And no, Fetch doesn't underwrite the policy itself: your coverage is issued by one of two carriers — XL Specialty or AXIS Insurance Company, depending on your state — and administered by the company that used to be called Petplan.

So this is a "should you — and which Fetch do you actually have" decision, not a star score. Below, we settle it for the three readers who usually land here: someone comparison-shopping Fetch, an owner burned by a denial or a renewal hike, and a new adopter drawn by Fetch's day-one coverage.

Table of Contents

- The Verdict: Is Fetch Worth It (and Who's It For)?

- Who Actually Underwrites Fetch (XL Specialty vs. AXIS)?

- Is Fetch the Same as Petplan? The 'by The Dodo' Lineage

- What Fetch Covers (and the Current Plan Menus)

- Waiting Periods, Pre-Existing & the Fine Print

- The Adopted-Pet Advantage: 7 Pre-Existing Conditions, Day One

- What Fetch Costs — Now and as Your Pet Ages

- Claims & the Reimbursement-First Reality

- Trustpilot 4.6 & App Store 4.8 vs. BBB 1.13: What the Split Means

- Fetch vs. the Alternatives

- Frequently Asked Questions

- Sources

The Verdict: Is Fetch Worth It (and Who's It For)?

Here's the short version most Fetch reviews bury under a star score: it's a legitimate, genuinely broad policy — the real decision is whether that breadth is worth a top-of-market price that climbs as your pet ages. Fetch's pitch is coverage depth: it pays a percentage of your actual vet bill for sick-visit exam fees, disease in every adult tooth, behavioral therapy, virtual vet visits, and prescriptions, with a customizable 70/80/90% reimbursement rate and no per-incident caps. Its standout perks are a one-year "curable" pre-existing reinstatement and day-one coverage of seven conditions for newly adopted pets. The trade-offs are the reimbursement-first cash flow (you pay the vet, then wait), premiums that reprice steeply at renewal, and a symptom-based pre-existing rule that catches people off guard.

Fetch is a reasonable pick if you:

- are insuring a younger, healthy pet and will actually use the breadth — exam fees, dental, behavioral, tele-vet — rather than chase the lowest premium;

- can comfortably float a large vet bill up front and wait to be paid back;

- just adopted, and want the rare day-one coverage of common shelter conditions.

Look elsewhere if you:

- are shopping on price — Fetch sits at the high end of the market, and renewals climb faster than inflation as your pet ages;

- need the insurer to pay your vet directly — Fetch reimburses you, not the clinic;

- have a pet with a problem already in its records — Fetch's symptom-based pre-existing rules will likely exclude it.

The rest of this review settles what should actually decide it: who underwrites your policy, what the current fine print really does, what it costs over time, and why Fetch's glowing star ratings and its complaint record tell such different stories.

Who Actually Underwrites Fetch (XL Specialty vs. AXIS)?

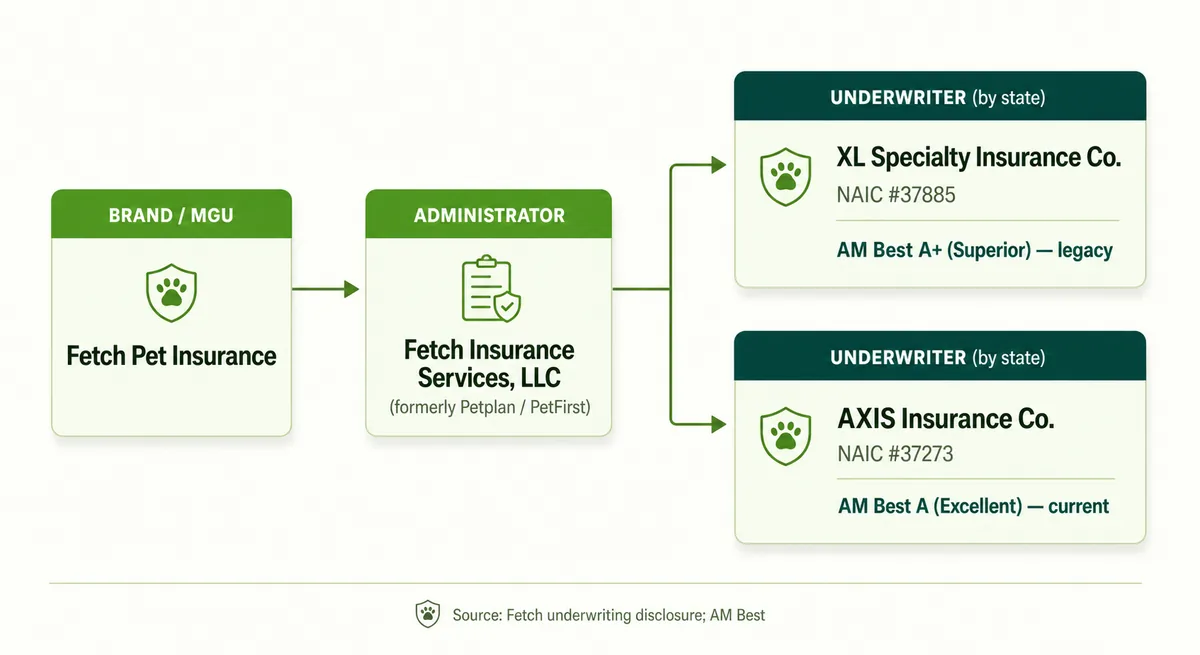

Nearly every Fetch review skips the thing that matters most: Fetch isn't the company that pays your claim. "Fetch" is a brand and a managing general underwriter — the policies are administered by Fetch Insurance Services, LLC (the business that used to be Petplan, then "Fetch by The Dodo"), but the carrier that actually holds the risk is named in your policy, and it's one of two.

Per Fetch's own underwriting disclosure, your coverage is issued by one of two carriers — XL Specialty Insurance Company or AXIS Insurance Company — and the two aren't the same. XL Specialty (NAIC #37885, a Delaware company in the AXA XL group) is the longtime Petplan-era carrier, rated A+ (Superior) by AM Best. AXIS Insurance Company (NAIC #37273, an Illinois company) was added as a Petplan/Fetch underwriter in November 2021, and AM Best rates it A (Excellent) — one tier below XL Specialty's A+, but still a financially strong carrier. Either way, the company standing behind your policy is sound; the point is that it isn't "Fetch."

Why does this matter beyond trivia? Because your actual contract — the waiting periods, the exclusions, the exact caps — is the state-approved form filed by whichever carrier underwrites your policy, not the national marketing copy on Fetch's website. And the catch: Fetch doesn't publish a map of which of its two carriers underwrites which policies. So the only reliable way to know who backs your coverage — and to read the terms that truly apply — is your own declarations page.

Is Fetch the Same as Petplan? The "by The Dodo" Lineage

If you've seen Fetch called "Petplan" or "Fetch by The Dodo," you're not confused — the same US company has worn all three names. It launched in 2003 and operated under the licensed Petplan brand for nearly two decades; in October 2020 it announced a partnership with the animal-media brand The Dodo and rebranded to "Fetch by The Dodo" in March 2022; then in January 2023 it dropped "by The Dodo" to become simply Fetch. (AXIS was added as an underwriter along the way, in November 2021.)

Two things to take from this. First, the US Fetch is not the still-separate UK Petplan — it only licensed that name until early 2022, so don't apply UK reviews or pricing here. Second, and more useful: a lot of "Fetch" reviews are stale. Some still rank under the retired "Fetch by The Dodo" name, and others describe plan terms from the Petplan era. When you read a Fetch review, check its date against this timeline — the product, its price, and even its underwriter have shifted underneath it.

What Fetch Covers (and the Current Plan Menus)

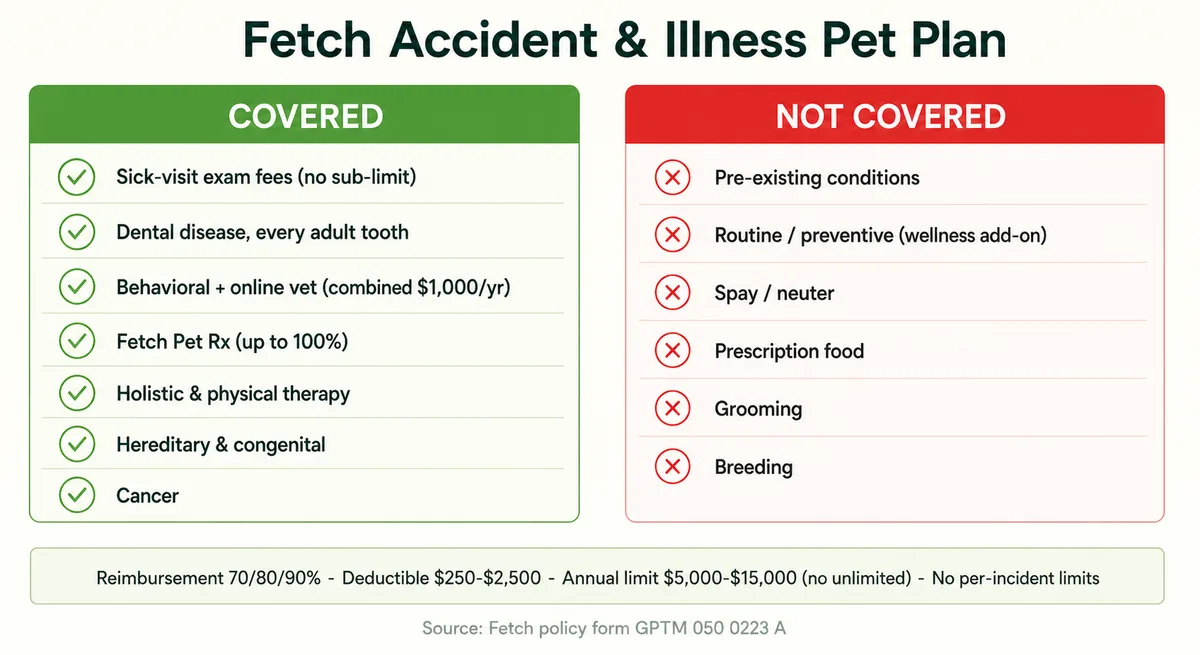

Fetch sells a single accident-and-illness plan, and you set the dials yourself: a reimbursement rate of 70%, 80%, or 90%, an annual deductible from $250 to $2,500, and an annual payout limit of $5,000, $10,000, or $15,000. If you've read that Fetch offers an unlimited annual limit, that's outdated — the current quote flow tops out at $15,000 (more is available only by phone). Two structural points work in your favor: there are no per-incident or per-condition limits — only that single annual cap — and the deductible is annual, so you meet it once per policy year, not once per illness.

The coverage itself is genuinely broad. Fetch reimburses a percentage of your actual vet bill for sick-visit exam fees (no separate sub-limit), disease in every adult tooth (no dental sub-limit), hereditary and congenital conditions, cancer, and vet-administered holistic and physical therapy — and its own Fetch Pet Rx pharmacy reimburses qualifying medications up to 100%, versus your normal 70–90% rate on meds bought elsewhere. What it won't cover is the usual list: pre-existing conditions, routine and preventive care (vaccines and dental cleanings are a separate wellness add-on), spay/neuter, prescription food, and grooming.

Here's the fine-print catch worth knowing before you buy. Fetch markets "behavioral therapy up to $1,000 a year" and "online vet visits up to $1,000 a year" as if they were two separate benefits. But Fetch's published sample policy form (GPTM 050 0223 A) folds both under a single combined $1,000 annual sub-limit — so the two together, not each, are capped at $1,000. Your state-filed contract controls the exact terms, so confirm it on your own policy, but it's exactly the kind of catch the star ratings never surface and the landing page never spells out.

Waiting Periods, Pre-Existing & the Fine Print

Fetch's waiting periods are middle-of-the-road: coverage starts the day after you enroll, with a wait of up to 15 days for both accidents and illnesses and a longer six-month wait for orthopedic conditions (cruciate tears, hip dysplasia, luxating patella). That orthopedic wait is the one to plan around — but Fetch waives it for the knees if a vet documents healthy knees in a baseline exam soon after you enroll. Fetch's current FAQ allows up to 180 days for that exam, though its sample policy form sets a tighter 30-day window — so if your breed is prone to knee trouble, book the exam early and confirm the exact deadline on your own declarations page.

The part that catches people out is how Fetch defines a pre-existing condition. It's symptom-based: a condition counts as pre-existing if your pet showed signs of it before coverage — even during that 15-day window, and even if no vet ever named the disease. Two clauses sharpen the teeth. First, a "first exam" rule: if your pet hasn't seen a vet in the six months before you enroll, any condition recorded at the first post-enrollment visit can be treated as pre-existing. Second, the policy links any new claim to the "same diagnostic classification" as an earlier note — so a single line in old records can echo forward into a denial.

There's genuine relief built in, though. Fetch will re-cover a curable condition if your pet goes a full year symptom-free, with a second-year second chance if it flares once; only if it returns during that second year is it excluded for life. And your state can shorten the waits: under California's SB 1217 (in force since January 2025), the illness and orthopedic waits can't exceed 30 days and accident waits are banned outright — because the state-approved form, not the national FAQ, is what your policy actually runs on.

The Adopted-Pet Advantage: 7 Pre-Existing Conditions, Day One

This is one place Fetch genuinely leads the field. Most insurers exclude every pre-existing condition, full stop — but Fetch covers seven common conditions from day one for newly adopted pets, with no waiting period and no separate charge (your plan's usual deductible and reimbursement rate still apply to treating them). The list targets exactly what shelters tend to send home: upper respiratory infection, ear mites, kennel cough, feline herpes, conjunctivitis, ringworm, and puppy pyoderma (a skin infection).

If you're insuring a pet you just brought home from a shelter or rescue, that's a real, rare perk — those are precisely the ailments that would otherwise get flagged as pre-existing at the first vet visit and denied. Just don't over-read it: it's seven specific conditions, not a blanket pre-existing waiver, and it applies to newly adopted pets. But for the right buyer, it's a genuine reason to put Fetch on the shortlist.

What Fetch Costs — Now and as Your Pet Ages

There's no single "Fetch price" — it turns on your reimbursement rate, deductible, and limit, plus your pet's species, breed, age, and ZIP code. Fetch's own stated average is about $35 a month for a dog and $22 for a cat — but treat that as a starting point, not a budget. For comparable coverage, Fetch prices toward the high end of the market: MoneyGeek, one of the few reviewers that scores on price rather than affiliate enthusiasm, ranks it near the bottom for affordability — 13th for dogs — and gives it just 2.70 out of 5 for dogs and 2.95 for cats. For a wider view of what pet insurance costs across the market, the drivers are the same everywhere — Fetch just prices toward the top of them.

The part that stings: renewals

Fetch's most consistent complaint isn't denials — it's renewal increases, and they hit hardest as a pet ages. Fetch, like most insurers, uses "birthday pricing," so premiums climb each year. One owner on Reddit reported a senior Golden's premium jumping about $1,700 in a single year, to over $4,000 (owner-reported figures, not Fetch's published rates). Vet-cost inflation is part of it — the government's vet-services index was up about 5% over the past year — but age is the dominant driver, and owners describe a lock-in trap: once a condition is on file, a new insurer will likely treat it as pre-existing and exclude it, so switching rarely comes clean and you end up absorbing the increase. For context, the industry accident-and-illness average from NAPHIA runs about $62 a month for dogs and $32 for cats. If you want routine care covered too, Fetch's optional Wellness rider adds roughly $15 to $38 a month for $315 to $735 in scheduled annual benefits. Budget for the cost to climb — that, not the intro price, is the real "is it worth it" math.

Claims & the Reimbursement-First Reality

Fetch is a reimbursement insurer: you pay your vet in full at the counter, then file a claim and get back your chosen 70%, 80%, or 90% after the deductible. There's no paying the clinic directly, so you need the cash or credit up front — the part that catches people off guard with any large emergency bill. Filing is done through the app or member portal, and you have 90 days from the date of treatment (not the invoice date) to submit — miss that window and the claim can be denied.

How fast you're paid is where owner experiences split. When a claim is clean and well-documented, people report smooth payouts: one long-tenured owner on Reddit had a roughly $3,000 tumor surgery approved in about two weeks, with the deposit landing within days. But others describe reimbursements dragging past a month, often because Fetch requests additional medical records — especially on a first claim, when it screens your pet's history for pre-existing conditions. The practical takeaways: keep every invoice and record, submit promptly, and be ready to float the bill. Fetch does pay out on legitimate claims — it just doesn't pay the vet, and it doesn't always pay fast.

Trustpilot 4.6 & App Store 4.8 vs. BBB 1.13: What the Split Means

Fetch's ratings look like two different companies. As of 2026, on Trustpilot it scores about 4.6 out of 5 across thousands of reviews, and its app rates 4.8 across some 27,000 ratings. Yet the Better Business Bureau shows about 1.13 out of 5 across its customer reviews, with 179 complaints closed in three years — even though the BBB's own letter grade is an A+ (that grade measures how responsively a business handles complaints, not how satisfied its customers are).

That gap isn't a contradiction; it's the story. The 4.6-and-4.8 pools lean heavily toward the enrollment and app experience — easy signup, a slick interface, a helpful quote agent — which is genuinely good. The complaint-driven venues (BBB, Reddit) cluster at the other end of the customer lifecycle: claim denials, pre-existing disputes, and renewal increases. Same company, sampled at two very different moments. Read the star scores as "Fetch is easy to buy," not "Fetch is easy to claim on." One thing will sharpen this picture over time: the NAIC added pet insurance as a Market Conduct Annual Statement line for the 2024 data year, so from 2025 regulators began collecting standardized complaint and claims-handling data on pet insurers — a step toward the first apples-to-apples comparisons on the part that actually matters.

Fetch vs. the Alternatives

Fetch's real edge is coverage breadth; its weaknesses are the reimbursement-first cash flow and the renewal climb. So the honest way to cross-shop is by what you care about most:

- You hate fronting a big bill. Fetch reimburses you after the fact. Trupanion can pay participating clinics directly, which erases exactly that liquidity problem.

- You want the simplest possible high limit. Healthy Paws strips its plan down to one uncapped annual limit — less breadth than Fetch, but no menus to overthink and often a lower price on a young pet.

- You're shopping mainly on price for a young pet. App-first Lemonade frequently quotes lower, though it bundles in fewer of the extras Fetch includes; Pets Best is another value-leaning option with solid limits.

The toughest case is the priced-out or denied owner. Because any new insurer treats an existing condition as pre-existing, switching late is rarely clean — our guide to switching pet insurance walks through when a move pays off and when staying put wins. If Fetch's breadth genuinely fits your pet and you can float the bills, it earns its place; if not, one of these will fit better.

Frequently Asked Questions

Who underwrites Fetch pet insurance?

Fetch is a managing general underwriter: policies are administered by Fetch Insurance Services, LLC and underwritten by one of two carriers, by state — XL Specialty Insurance Company (AM Best A+, the legacy Petplan carrier) or AXIS Insurance Company (AM Best A, for newer policies). Your declarations page names which one covers you.

Is Fetch pet insurance worth it?

Fetch is worth it if you're insuring a younger, healthy pet that will use its broad coverage (exam fees, dental, behavioral therapy, Fetch Pet Rx) and you can pay vet bills up front and wait for reimbursement. It's a weaker fit if you're shopping mainly on price — Fetch sits at the top of the market and reprices steeply as pets age.

Is Fetch the same as Petplan or "Fetch by The Dodo"?

Yes — it's the same US company. It operated under the licensed Petplan name until it rebranded to "Fetch by The Dodo" in 2022 and then to simply Fetch in January 2023. It is not the same as the still-separate UK Petplan, so don't apply UK reviews or pricing to it.

Does Fetch cover pre-existing conditions?

No — like most insurers, Fetch excludes pre-existing conditions, and its definition is symptom-based (a condition your pet showed signs of before coverage). But a curable condition can be re-covered after your pet is symptom-free for a full year, and Fetch covers seven named pre-existing conditions from day one for newly adopted pets.

Do all vets accept Fetch pet insurance?

Effectively, yes. Because Fetch reimburses you rather than paying the clinic, there's no network — you can use any licensed veterinarian in the U.S., including specialists and emergency hospitals. You pay the bill and file a claim afterward.

Does Fetch cover exam fees and dental?

Yes. Fetch covers sick-visit exam fees with no separate sub-limit, and dental disease in every adult tooth with no dental sub-limit. Note that routine dental cleanings and other preventive care aren't in the base plan — they require the optional Fetch Wellness add-on.

How much is Fetch pet insurance?

Fetch's own stated average is about $35 a month for a dog and $22 for a cat, but it sits at the high end of the market and your real quote depends on your pet's age, breed, and ZIP code plus the limit, deductible, and reimbursement rate you choose. Budget for it to climb at renewal as your pet ages.

How fast does Fetch pay claims?

Fetch is reimbursement-first: you pay the vet, file within 90 days of the date of treatment, and get 70–90% back. Owners report that clean, well-documented claims can be paid in about two weeks, while some reimbursements take over a month — especially a first claim, which triggers a medical-records review.

Which is better, Trupanion or Fetch?

It depends on what you value. Trupanion can pay participating vets directly and uses a per-condition deductible — better if you can't front large bills. Fetch offers broader coverage (exam fees, dental, behavioral therapy, Fetch Pet Rx) but is reimbursement-first. Match the model to your cash flow and coverage priorities.

Why did my Fetch premium go up?

Mostly your pet simply getting older — Fetch, like most insurers, prices by age, so premiums rise each year — compounded by veterinary-cost inflation, which ran about 5% over the past year. Owners also report that filing claims can nudge renewals higher. And because a logged condition tends to become pre-existing elsewhere, many owners feel locked in, so budget for the climb.

Sources

- Fetch Pet Insurance Coverage — Fetch

- Fetch Pet Insurance underwriting disclosure — Fetch / IMG

- AXA XL Financial Strength Ratings (XL Specialty Insurance Company) — AXA XL

- AM Best Rating — AXIS Insurance Company (AMB #013034) — AM Best

- 'Fetch by The Dodo' Pet Insurance, Formerly Petplan, Launches — PR Newswire

- Fetch Refreshes Company Name, Makes Fetch Happen — PR Newswire

- Can I customize my pet insurance plan? (reimbursement 70/80/90%) — Fetch

- What is a pet insurance deductible? ($250–$2,500) — Fetch

- Annual coverage limit ($5k/$10k/$15k) — Fetch

- Fetch dental coverage (every adult tooth, no sub-limit) — Fetch

- Fetch sample policy form GPTM 050 0223 A (combined $1,000 behavioral/telehealth sub-limit; no per-incident limits; 30-day knee-waiver window) — Fetch

- Fetch waiting periods (0-day accident, ≤15-day illness, 6-month orthopedic, 30-day knee waiver) — Fetch

- Fetch pre-existing conditions (symptom-based; 1-year curable reinstatement) — Fetch

- California SB 1217 (30-day waiting-period cap; accident-wait ban; eff. 2025-01-01) — California Legislature

- Fetch adopted-pet pre-existing conditions (7 covered day one) — Fetch

- How much does Fetch pet insurance cost ($35 dog / $22 cat avg) — Fetch

- Fetch insurance increasing by almost 2k (senior Golden renewal, owner-reported) — Reddit r/goldenretrievers

- BLS Veterinarian services CPI (+5.1% YoY, June 2026) — U.S. Bureau of Labor Statistics

- NAPHIA 2025 State of the Industry Highlights (A&I averages $749 dog / $386 cat) — NAPHIA

- Fetch Wellness rider tiers ($315/$520/$735) — Fetch

- When to file a Fetch claim (within 90 days of treatment) — Fetch

- Fetch owner claims experiences (payout speed; diligent-claimant praise) — Reddit r/dogs

- Trustpilot — Fetch Pet Insurance (4.6/5) — Trustpilot

- Apple App Store — Fetch Pet Insurance (4.8/5, 27K ratings) — Apple

- BBB — Fetch Pet Insurance (1.13/5, 179 complaints/3yr, A+ accredited) — Better Business Bureau

- NAIC MCAS 2024 (pet insurance first-ever MCAS line) — NAIC

- MoneyGeek — Fetch Pet Insurance Review (price-methodology scores 2.70 dogs / 2.95 cats; ranks near the bottom for affordability) — MoneyGeek

- AXIS Insurance Enters Pet Insurance Market With Petplan (AXIS added as underwriter, Nov 9, 2021) — AXIS Capital