Two questions bring most people to a USAA pet insurance review: is it any good? and who's actually behind it? Here are the short answers before the detail.

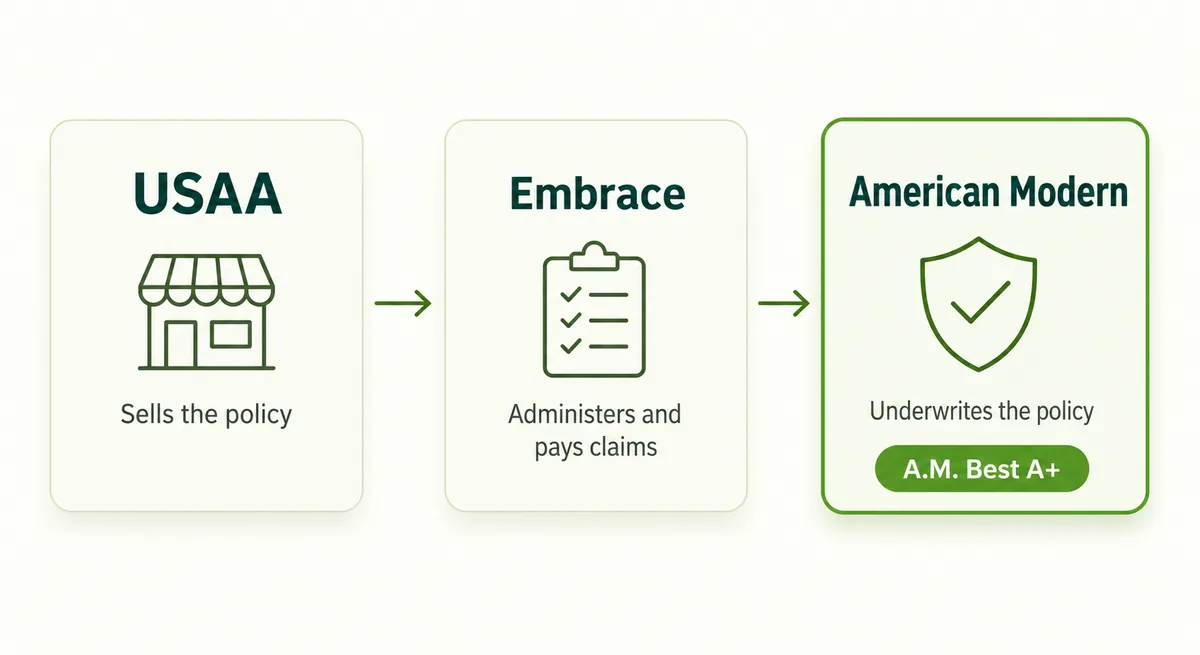

USAA doesn't insure your pet. "USAA pet insurance" is a branded storefront: USAA is the agency that sells it, Embrace administers the policy and handles your claims, and the underwriter that actually carries the risk is American Modern Home Insurance Company — a Munich Re company rated A+ (Superior) by AM Best. That matters more than it sounds: the carrier's state-filed policy — not USAA's marketing page — is what decides your waiting periods, sub-limits, and payouts.

So is it worth buying through USAA? The honest answer is conditional. The policy itself is a broad Embrace plan with buyer-friendly payout math, and the USAA member discount is the one thing you can't get by going to Embrace directly. But that discount is the only USAA-specific edge, it varies by state, and it isn't guaranteed to survive your renewal — and, as with most pet insurance, your premium tends to climb as your pet ages. This review names the real carrier, reconciles the discount against what Embrace actually publishes, works through the claim math, and maps the renewal risk, so you can decide with your eyes open.

Table of Contents

- The Verdict: Is USAA Pet Insurance Worth It (and Who's It For)?

- Who Actually Underwrites USAA Pet Insurance?

- What the USAA Discount Really Buys (and When It Shrinks)

- What It Covers (Plans, Limits & the Dental Catch)

- How a Claim Pays Out (Deductible First — in Your Favor)

- Waiting Periods, Pre-Existing & the Fine Print

- What It Costs — Now and at Renewal

- Does Your State Change the Rules?

- Ratings & What Owners Actually Say

- USAA vs. Buying Embrace Direct — and the Alternatives

- Frequently Asked Questions

- Sources

The Verdict: Is USAA Pet Insurance Worth It (and Who's It For)?

Our take: buying pet insurance through USAA is worth it for some members and beside the point for others — and the deciding factor is almost entirely the member discount. The policy underneath is a solid, broad Embrace plan whose claim math genuinely favors you (more on that below). USAA doesn't change that policy; it changes the price. So the real question isn't "is Embrace any good?" — it's "does going through USAA save me enough, durably enough, to matter?"

It's probably worth it if you:

- are a USAA member and your state currently approves a meaningful USAA discount;

- want one broad policy — any vet, no network — and value a payout that subtracts your deductible before applying the reimbursement percentage;

- are insuring a young, healthy pet, where premiums start lowest and the discount does the most work.

Look harder — or buy elsewhere — if you:

- live in a state where the USAA discount is small, or isn't guaranteed to hold at renewal;

- are price-sensitive about renewals, since your premium climbs as your pet ages regardless of the badge;

- could buy the identical Embrace policy directly and wouldn't clear a real discount by going through USAA.

Notice what's not on either list: a star rating. We don't score USAA out of five, because the thing you're actually buying — the coverage, the claims experience, the renewal curve — belongs to Embrace and its underwriter, not to the USAA logo on the quote page. The rest of this review walks each of those in turn, so your "worth it" answer fits your pet and your state, not an industry average.

Who Actually Underwrites USAA Pet Insurance?

Short answer: not USAA. When you buy "USAA pet insurance," three different companies each play a distinct role, and only one of them actually carries the risk on your pet.

Here is the chain, front to back:

- USAA — the seller. USAA is the agency that markets and sells the policy to members. It has partnered with Embrace on pet coverage since 2014, and it "receives compensation on the sale or renewal" of the product. It does not set the terms or decide your claim.

- Embrace — the administrator. Embrace Pet Insurance Agency, LLC quotes the policy, services it, and adjudicates and pays your claims on the underwriter's behalf. This is the brand you will actually deal with day to day.

- American Modern — the underwriter. The company that legally carries the risk is American Modern Home Insurance Company (NAIC #23469) in every state except Florida, where American Southern Home Insurance Company (NAIC #41998) underwrites; in California it operates as American Modern Insurance Company. All are part of American Modern Insurance Group, a Munich Re company.

Is that carrier solid? Yes. American Modern Home Insurance Company holds an AM Best rating of A+ (Superior), affirmed in July 2025 as part of AM Best's action on the Munich Re group. (The Florida underwriter shares that group rating rather than a separately published one.)

Why does any of this matter to you? Because the document that decides your waiting periods, your dental sub-limit, and how a claim pays out is the policy form American Modern files with your state's insurance department — not USAA's marketing page. When a question comes down to what is actually covered, the answer lives in that state-filed contract. That is why the rest of this review leans on Embrace's and the carrier's own policy language rather than the USAA brochure.

What the USAA Discount Really Buys (and When It Shrinks)

The USAA discount is the one thing you can't get by buying Embrace directly, so it's worth understanding exactly what it is — and how fragile it can be.

USAA advertises up to 15% off for buying through its agency, plus an extra up to 10% for military members, service-dog handlers, or multi-pet households — a maximum of 25%, with the important caveat that not all discounts are approved in every state and that they can change.

But look at what Embrace itself publishes, and the numbers don't quite line up. Embrace's own discount page lists a 10% multi-pet discount and a 5% military discount, applied only to the accident-and-illness part of your premium. So the "extra 10% for military" you'll see repeated across reviews is really 5% — the 10% is the multi-pet discount. The base 15% is a USAA-channel discount that doesn't appear on Embrace's public page at all.

Add it up, and the honest read is this: 25% is a best-case ceiling, not a typical result. One 2026 analysis of a Texas quote for a 3-year-old mixed-breed dog found the effective discount landed around 8–15%, depending on state and eligibility.

And here's the part almost no review mentions: the discount isn't locked in at renewal. In early 2026, a California member shared an Embrace renewal notice stating that "the USAA discount in California has been reduced to 4%" — down from 15% — after a state actuarial review. That's one owner's report from a single state, not a nationwide rule. But it points to something real: because the discount is state-regulated, it can be trimmed mid-relationship, and any shrinkage lands straight on your premium.

What It Covers (Plans, Limits & the Dental Catch)

Underneath the USAA badge is a standard Embrace accident-and-illness policy — a broad plan you build yourself from a menu, with one coverage quirk worth knowing before you buy.

You customize the core policy across three dials, plus a one-time fee:

- Reimbursement rate: 70%, 80%, or 90% of the covered bill.

- Annual deductible: $200 to $1,000.

- Annual limit: $5,000, $8,000, $10,000, $15,000, or $30,000 — with unlimited coverage available in some states.

- Enrollment fee: a one-time $25.

You'll see lower numbers — a $100 deductible, a $2,000 limit — on some comparison sites; those belong to Embrace's separate accident-only plan, not the standard accident-and-illness menu. Confirm the exact options at quote, since limit availability varies by state.

The dental catch. Most reviews say dental is "covered" or "not covered" and stop there. Embrace actually splits dental three ways, and the difference can be hundreds of dollars:

| Type of dental claim | How it's covered |

|---|---|

| Dental illness (e.g. periodontal disease) | Capped at $1,000 per policy year, after your deductible and reimbursement rate |

| Dental accident or trauma (e.g. a broken tooth) | Covered up to your full annual limit |

| Routine cleanings | Not covered by the insurance — only through the optional wellness add-on |

That optional add-on, Wellness Rewards, is worth flagging: it isn't insurance. It's a separate membership that reimburses routine care — cleanings, vaccines, grooming — up to an annual allowance you choose ($300, $500, or $700), with no deductible. Note those figures are the reimbursement allowance, not the price; you pay a monthly fee on top. Useful for some households, but don't count it as part of your medical coverage.

How a Claim Pays Out (Deductible First — in Your Favor)

Here's a piece of good news most reviews skip: Embrace calculates your reimbursement in the order that pays you the most.

You pay your vet directly — there is no network, so any licensed vet, specialist, or ER counts — then submit the bill and get reimbursed by check or direct deposit. When Embrace does the math, it subtracts your annual deductible first, then applies your reimbursement percentage. Its own worked example: a $1,200 covered bill, minus a $200 deductible, leaves $1,000; at 80% reimbursement, you get $800 back.

Why does the order matter? Because some insurers flip it — they apply the percentage first, then subtract the deductible. On that same $1,200 bill, percentage-first math ($1,200 × 80%, then − $200) would pay just $760. Same inputs, $40 less. It's a small edge on one claim, but it compounds over a policy's life, and it's a genuine point in Embrace's favor.

One note on cash flow: your deductible is annual, not per-incident, so you clear it once per policy year rather than on every visit. And if you're facing a big bill, Embrace offers a limited pre-certification path that can pay a hospital directly when a bill is likely to top $1,000 and the hospital agrees — though it is never required and isn't a standing direct-pay network. For everyday visits, plan to pay up front and wait for reimbursement.

Waiting Periods, Pre-Existing & the Fine Print

This is where a policy either works when you need it or quietly doesn't. Three things decide it: how long you wait for coverage to start, one exam-timing rule that can gut your illness coverage, and how Embrace treats conditions your pet already has.

Waiting periods are the days between enrolling and coverage kicking in:

| Coverage | Waiting period |

|---|---|

| Accidents | None — though your policy's effective date is itself about 2 days after you enroll |

| Illnesses | 14 days |

| Orthopedic (dogs) | 6 months — reducible to as few as 14 days in some states by completing an orthopedic exam |

| Orthopedic (cats) | 14 days |

These are Embrace's standard waiting periods, but some states cap them shorter — California, for example, limits non-accident waits to 30 days, so your own state form is the final word.

The 14-day exam trap

Here's the rule that catches people. Embrace requires a vet exam within the 12 months before your start date or within 14 days after. Miss that window and your policy silently defaults to accident-only — no illness coverage — with the illness portion of your premium refunded. If you're enrolling a pet that hasn't seen a vet recently, book that exam; don't let the deadline decide your coverage for you.

Pre-existing conditions. Any injury, illness, or irregularity you or your vet noticed in the 12 months before coverage — and before your waiting periods end — counts as pre-existing. The key split is curable vs. incurable: a curable condition can regain coverage after your pet is symptom- and treatment-free for 12 straight months, while conditions Embrace treats as incurable — it names diabetes, arthritis, and allergies — stay excluded for good. Two more catches: the bilateral rule means if one knee or hip was pre-existing, the matching joint is excluded too; and pets enrolled at 15 or older can get accident-only coverage only.

What It Costs — Now and at Renewal

There is no single "USAA average," and any review that hands you one without the fine print is guessing. Premiums swing enormously with your pet's age and breed, your state, and the three dials you picked — so the only useful price is one attached to its configuration.

Here's what published reviews estimate, each shown with the setup behind the number:

| Source (configuration) | Dog / mo | Cat / mo |

|---|---|---|

| Forbes ($10,000 limit, $250 deductible, 80%) | ~$84 | ~$45 |

| MoneyGeek (6-yr Lab / 7-yr Ragdoll, $5,000, $500, 80%) | ~$73 | ~$46 |

| Yahoo ($5,000 limit) | ~$67 | — |

| Embrace sample (age 3, $5,000, $1,000 deductible, 70%, TX, May 2025) | $11.16–$35.85 | $11.47–$14.26 |

See the spread? Estimates for the same insurer run from about $11 to $84 a month for a dog — a gap driven by differences in age, breed, state, how the policy is built, and even which reviewer ran the numbers and when. For context, the industry-wide average accident-and-illness premium is roughly $62/mo for dogs and $32/mo for cats (2024 data) — so on comparable setups, USAA/Embrace tends to sit at or above the mean, not below it.

The renewal curve is the real cost. Whatever you pay in year one climbs as your pet ages, and owners describe the jumps candidly. One shared a renewal rising from $147.94 to $272.01 a month, about 84%, for two senior cats; others report premiums doubling over roughly three years even with the USAA discount, and a loyalty penalty where a renewal reached $88.54 while new customers were quoted $58.52 for the same coverage. These are individual owner reports, not guaranteed outcomes — but premiums rising as a pet ages is a well-documented industry reality, not something unique to USAA, and owners describe similar increases at other carriers. Budget for a premium that grows, not one that holds.

Does Your State Change the Rules?

Yes — and sometimes in ways that matter. The policy form your underwriter files with your state's insurance department controls the actual terms, and a wave of 2023–2026 state laws (many following the NAIC's Pet Insurance Model Act) has been rewriting them. Two things vary by state: your waiting-period ceilings, and whether the seller even has to tell you who really underwrites the policy.

| State | In effect | What it requires |

|---|---|---|

| Maine | 2023 | Must disclose when the underwriter differs from the brand name |

| Florida | 2026 | Same brand-vs-underwriter disclosure; bans accident waiting periods |

| Hawaii | 2026 | Same disclosure; bans accident waiting periods |

| California | 2025 | Bans accident waits and caps others at 30 days — but does not require the brand-vs-underwriter disclosure |

That last row is the catch worth noticing: a California buyer gets stronger waiting-period protections, yet California's pet-insurance disclosure law doesn't require anyone to surface the USAA-to-American Modern gap this review has unpacked. Remember, too, that the underwriter itself shifts by state — American Modern Home in most states, American Southern Home in Florida — so "USAA pet insurance" is never quite a national constant. The takeaway is simple: pull up your own policy's declarations page and state form before you buy, because that document, not a national summary, is what governs your claim.

Ratings & What Owners Actually Say

If you go looking for a USAA pet insurance score, you'll find wildly different numbers — which is exactly why a single star rating is the wrong thing to trust here.

| Source | Score |

|---|---|

| Yahoo Finance | 4.4 / 5 |

| MoneyGeek | 2.55 / 5 dogs, 2.3 / 5 cats |

| BBB (for Embrace) | ~1.18 / 5 |

The gap between a 4.4 and a 1.18 isn't a contradiction — it's the difference between editors scoring features and unhappy customers self-selecting to file complaints. Notice, too, that the BBB reviews are filed against Embrace, not USAA, which tells you where the real relationship lives.

Reading through what owners write, a few themes repeat — all sentiment, not hard data:

- "Wait, is this really USAA?" Genuine confusion about who's behind the policy — the exact gap this review exists to close.

- Renewal shock. The loudest substantive complaint, and the one most likely to end a policy.

- Records and pre-existing disputes, alongside reports of slow claims and hard-to-reach service.

It isn't all negative. Some long-term customers say the policy has paid out more than they've put in, with big claims — including cancer care — reimbursed within days, and MoneyGeek's tally of Reddit found about 29% of comments positive. The honest read: this is a capable policy with a real customer-service tail, and the owners happiest with it tend to be the ones who understood the renewal math going in.

USAA vs. Buying Embrace Direct — and the Alternatives

Here's the question that ties the whole review together: if USAA is just the storefront, why not walk in through Embrace's front door instead? It's a fair question, and the answer is refreshingly simple.

The underlying policy is identical either way — same coverage, same deductible-first math, same waiting periods, same underwriter. The one thing that differs is the price: the USAA member discount you can't get buying Embrace directly, which is also the piece most likely to move at renewal. So the decision comes down to one question: is your discount real and durable enough to matter?

- Go through USAA if you're an eligible member and your state currently approves a meaningful discount — that's a real saving on an identical product.

- Buy Embrace directly if you're not a USAA member (membership is tied to military affiliation, not open to everyone) or if your state's discount is small or has been trimmed. You lose nothing but the discount.

- Shop the alternatives if the renewal math worries you or you want a different coverage structure. Other carriers price accident-and-illness cover differently, and a young, healthy pet is the easiest to move — so it's worth comparing before you commit.

One honest caveat: because the discount is state-regulated, it can shrink at renewal even if it's generous today, as one California member reported. That doesn't make USAA a bad choice — it just means the discount is a nice-to-have, not the whole reason to buy. Pick the underlying policy on its merits first, and treat the USAA savings as the bonus it is.

Frequently Asked Questions

Who underwrites USAA pet insurance?

USAA doesn't underwrite it. The policy is administered by Embrace and underwritten by American Modern Home Insurance Company (American Southern Home Insurance Company in Florida), a Munich Re company rated A+ (Superior) by AM Best. USAA is the agency that sells the policy and earns a commission; Embrace services it and pays your claims. That matters because the underwriter's state-filed policy form, not USAA's website, controls your actual coverage terms.

Is USAA pet insurance good?

It's a solid policy for the right buyer, with one important caveat. The underlying Embrace plan is broad — any vet, customizable limits, and a deductible-first payout that works in your favor — and it's backed by an A+-rated carrier. The catch is cost over time: premiums rise as your pet ages, and the USAA member discount (its main advantage over buying Embrace directly) varies by state and isn't guaranteed at renewal. It's a good choice if you value the coverage and clear a real discount, and less compelling if you don't.

How much does USAA pet insurance cost?

There's no single answer — it depends on your pet's age and breed, your state, and the limit, deductible, and reimbursement rate you choose. On common configurations, published reviews put a dog around $67–$84 a month and a cat around $45, which sits at or above the industry average of roughly $62/mo for dogs and $32 for cats. Always get a quote with your exact settings; any 'average' quoted without its configuration is close to meaningless.

Do I have to be a USAA member to buy it?

You do to buy it through USAA and get the member discount, since USAA membership is tied to military service, veterans, and their families. If you're not eligible, you can buy the exact same Embrace policy directly from Embrace — you'll just miss the USAA-specific discount. The coverage, underwriter, and claims process are identical either way, so a non-member loses nothing but the potential savings.

What is the USAA military discount on pet insurance?

Embrace's published military discount is 5%, applied to the accident-and-illness portion of your premium. USAA advertises up to 15% for buying through its agency, plus up to another 10% for military, service-dog, or multi-pet members, for a maximum of 25% — but that ceiling is state-dependent and rarely the number you actually get. Reviews describing a flat 'extra 10% for military' are conflating it with the multi-pet discount.

Does USAA pet insurance cover dental?

Partly, and the details matter. Dental illness such as periodontal disease is capped at $1,000 per policy year; a dental accident like a broken tooth is covered up to your full annual limit; and routine cleanings aren't covered by the insurance at all — only through the optional, non-insurance Wellness Rewards add-on. Most reviews flatten this into 'dental covered/not covered,' which is exactly why owners get surprised at claim time.

Does it cover pre-existing conditions?

No — like every pet insurer, Embrace excludes conditions your pet had before coverage began. There's one important exception: a curable condition can regain coverage after your pet has been symptom- and treatment-free for 12 straight months, while conditions treated as incurable (Embrace names diabetes, arthritis, and allergies) stay excluded. Remember that being able to buy a policy isn't the same as having a specific condition covered — and always get your pet the care it needs, regardless of insurance.

Why does USAA pet insurance have bad reviews or a low BBB rating?

The very low scores you'll see — around 1.18/5 on the BBB — are customer-review ratings filed against Embrace, the administrator, and they skew negative because unhappy customers are the ones most likely to post. Editorial reviewers scoring features rather than venting land much higher (Yahoo gives it 4.4/5). The honest read is a capable policy with a real customer-service and renewal-pricing tail; weigh the specific complaints, like renewal increases and slow claims, rather than any single star number.

Sources

- Underwriting — who underwrites Embrace pet insurance — Embrace Pet Insurance

- AM Best Affirms Credit Ratings of Munich Reinsurance Company and Its Subsidiaries — AM Best

- Pet Insurance for Dogs and Cats — USAA

- Pet Insurance Discounts — Embrace Pet Insurance

- USAA Pet Insurance Review 2026 — RatesChaser

- Anyone with Embrace through USAA based in California? — Reddit — r/petinsurancereviews

- Coverage FAQ (plan menu, deductibles, limits, enrollment fee) — Embrace Pet Insurance

- What does Embrace offer in terms of dental illness coverage? — Embrace Pet Insurance

- What is Embrace's Wellness Rewards? — Embrace Pet Insurance

- How pet insurance companies calculate your refund — Embrace Pet Insurance

- State Terms (v6) — any-vet reimbursement model; exam-timing default; bilateral rule — Embrace Pet Insurance

- Pre-certification — Embrace Pet Insurance

- Pet insurance waiting periods (no accident wait; 14-day illness) — Embrace Pet Insurance

- What is the waiting period for orthopedic conditions? — Embrace Pet Insurance

- What are pre-existing conditions and does Embrace cover them? — Embrace Pet Insurance

- USAA Pet Insurance Review (cost estimates by config) — Forbes Advisor

- USAA Pet Insurance Review (species-split scores and prices) — MoneyGeek

- USAA Pet Insurance Review — Yahoo Finance

- Pet insurance cost research (config-locked sample premiums) — Embrace Pet Insurance

- 2025 State of the Industry Report (average A&I premiums) — NAPHIA

- My Embrace pet insurance renewal is increasing by 84% — Reddit — r/petinsurancereviews

- Does anyone have experience with USAA pet insurance? — Reddit — r/petinsurancereviews

- NAIC passes Pet Insurance Model Act (#633) — NAIC via PR Newswire

- Maine Title 24-A §3155 (brand-vs-underwriter disclosure) — Maine Legislature

- Florida §627.71545 (brand-vs-underwriter disclosure; accident-wait ban) — Florida Legislature

- Hawaii Act 79 / HB544 CD1 (brand-vs-underwriter disclosure; accident-wait ban) — Hawaii State Legislature

- California Insurance Code §12880.2 (disclosures; no brand-vs-underwriter requirement) — California Insurance Code (FindLaw)

- Embrace Pet Insurance — BBB complaints & customer reviews (~1.18/5) — Better Business Bureau