If you're weighing Prudent Pet insurance in 2026, you're probably asking two things at once: is it actually any good? and who really stands behind it? That second question matters more than most reviews let on — because "Prudent Pet" is a brand and an agency, not the company that actually pays your claim. We read Prudent's own policy pages, its underwriters' financial-strength ratings, and what real owners report at claim time, so you don't have to.

The short answers first. Yes, it's a legitimate, widely-sold insurer with broad, build-it-yourself coverage — accident and illness care, dental, behavioral therapy, even an unlimited annual-limit option — that reimburses a percentage of your eligible vet bills (after your deductible, and minus anything the plan excludes). And no, Prudent doesn't underwrite the policy itself: your coverage is issued by one of two Markel insurance companies and administered by Prudent Pet Insurance Agency.

So this is a "should you — and read the fine print first" decision, not a star score. The catch is that Prudent's own pages don't always agree with each other on the rules that decide a claim. Below, we settle it for the three readers who usually land here: someone comparison-shopping Prudent, an owner burned by a renewal hike somewhere else, and a young- or newly-adopted-pet owner insuring before problems start.

Table of Contents

- The Verdict: Is Prudent Worth It (and Who's It For)?

- Who Actually Underwrites Prudent (Markel)?

- What Prudent Covers (Plans, Limits & the Exam-Fee Catch)

- How a Prudent Claim Pays Out (the Math That Pays Less)

- Waiting Periods, Pre-Existing & the Fine Print

- What Prudent Costs — Now and at Renewal

- Does Your State Change the Rules? (Florida & Hawaii, 2026)

- Ratings Split & What Owners Say

- Prudent vs. the Alternatives

- Frequently Asked Questions

- Sources

The Verdict: Is Prudent Worth It (and Who's It For)?

Here's the short version most Prudent reviews bury under a star score: it's a legitimate, genuinely broad policy backed by a financially strong carrier — the real decision is whether its build-your-own coverage is worth two catches, a claim formula that pays out a little less than rivals and a reimburse-you-later model. Prudent's pitch is flexibility: three plan tiers (including an unlimited annual limit), a customizable deductible and 70/80/90% reimbursement, and coverage for the things buyers actually want — sick-visit and dental care, behavioral therapy, and vet-administered alternative treatments. Owners widely report fast claim payouts, and the policy is underwritten by Markel, an A-rated insurer. The trade-offs are the payout order (Prudent subtracts your deductible from the reimbursement, not the bill), the reimbursement-first cash flow, exam fees that cost extra, and the fact that Prudent is a small, newer company.

Prudent is a reasonable pick if you:

- want broad, customizable coverage — dental, behavioral, an unlimited-limit option, and optional exam-fee and wellness add-ons — and will actually use it;

- can comfortably pay a large vet bill up front and wait to be reimbursed;

- value fast claim turnaround, or you're insuring a young or senior pet.

Look elsewhere if you:

- want the biggest possible payout per claim — Prudent's deductible-after-reimbursement math pays less than deductible-first insurers;

- need the insurer to pay your vet directly — Prudent reimburses you, not the clinic;

- want the reassurance of a large, long-established brand — Prudent is small and privately held, and some owners worry aloud about a future buyout.

The rest of this review settles what should actually decide it: who underwrites your policy, exactly how a claim pays out, what the fine print really says — including where Prudent's own pages disagree — and what it costs as your pet ages.

Who Actually Underwrites Prudent (Markel)?

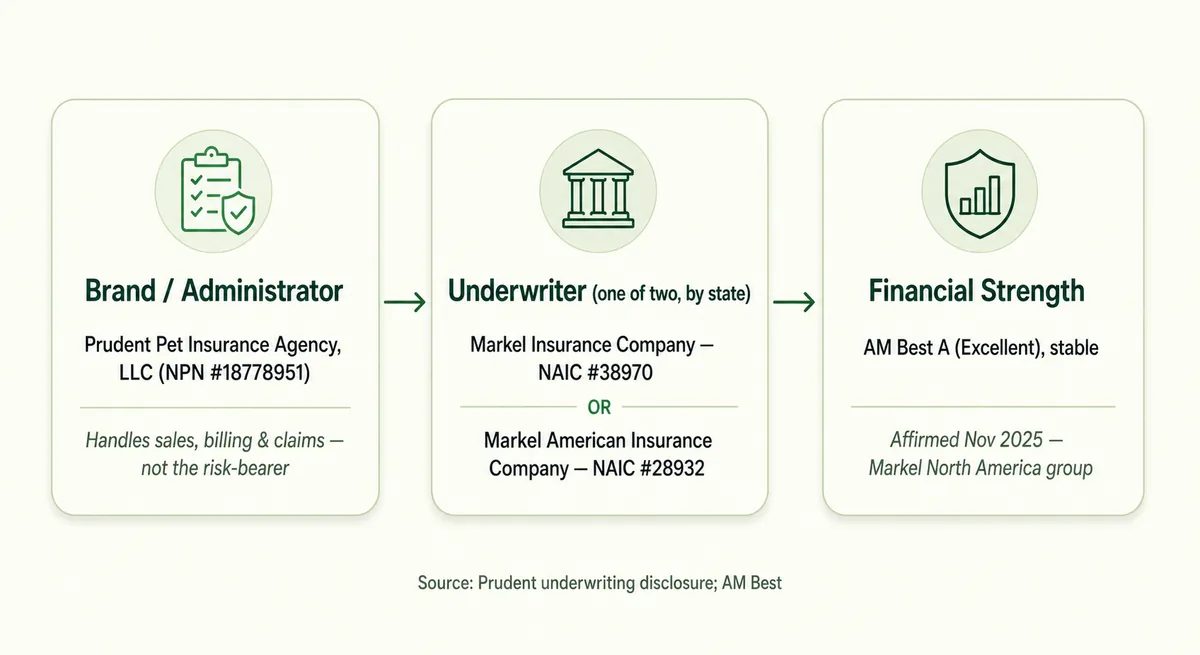

Nearly every Prudent review skips the thing that matters most: Prudent isn't the company that pays your claim. "Prudent Pet" is a brand and an agency — the policies are administered by Prudent Pet Insurance Agency, LLC, which handles quotes, billing, claims, and service — but the carrier that actually holds the risk is a Markel company named in your policy.

Per Prudent's own underwriting disclosure, your coverage is underwritten by either Markel Insurance Company (NAIC #38970) or Markel American Insurance Company (NAIC #28932), depending on your state. Both belong to the Markel North America group, and AM Best rates it A (Excellent), affirmed in November 2025 — a large, financially strong insurer that has backed pet coverage for years. The takeaway isn't the trivia; it's that the company standing behind your policy is Markel, not Prudent.

Why does this matter? Because your actual contract — the waiting periods, the exclusions, the exact caps — is the state-approved form filed by whichever Markel entity underwrites you, not the national marketing copy on Prudent's website. And Prudent doesn't publish a map of which carrier writes which state, so the only reliable way to know who backs your coverage — and to read the terms that truly apply — is your own declarations page.

One more thing, because owners ask: Prudent is small and privately held, and some worry aloud that it's "ripe for a buyout." It hasn't been sold. Some owners have described a 2023 episode in which a portion of Prudent's customers were moved to another insurer, Spot — but treat that as unverified owner discussion, not a confirmed corporate event. What is documented is that Prudent still operates and, per its underwriting disclosure, your policy is backed by Markel. Still, it's a newer, smaller company backed by a very established carrier, so weigh that stability question honestly against the breadth of the coverage.

What Prudent Covers (Plans, Limits & the Exam-Fee Catch)

Prudent sells three plans. Accident-Only covers injuries up to a $10,000 annual limit; Essential adds illness on the same $10,000 cap (a lower $2,500 tier is also reported, though Prudent's own table headlines only the larger numbers); and Ultimate — the plan Prudent flags "most popular" — is the only one of the three with an unlimited annual payout. Within whichever plan you pick, you set two dials: a reimbursement rate of 70%, 80%, or 90%, and an annual deductible of $100, $250, $500, or $1,000. Prudent's public page describes these only as "customizable," so treat the exact menu values as numbers to confirm in the live quote rather than gospel.

The coverage itself is genuinely broad for an accident-and-illness policy. Prudent reimburses a share of the bill for injuries, illnesses, hereditary and congenital conditions, cancer, dental disease, hospitalization and surgery, diagnostics, prescription medications, behavioral therapy, and even vet-administered alternative treatments such as acupuncture and physical therapy. (Prescription food is the notable narrow exception — covered only for a few specific conditions like bladder stones, not as an everyday diet.) The Ultimate tier layers on extras most owners never touch — lost-pet advertising, boarding fees, a mortality benefit — plus a $1,000-a-year behavioral sub-limit; an older "Ultimate Plus" form shows $2,000, so check the figure on your own form.

Then there's the catch that surprises owners at claim time: exam fees aren't included by default. Prudent's own pages list them as excluded "unless you have chosen to include them" — a paid add-on you can attach only at purchase or renewal. On a $1,300 emergency-room visit, that one rider is the difference between a claim that reimburses the exam and one that doesn't. Routine and preventive care is the same story: it's covered only if you buy the separate optional Wellness add-on, which pays fixed amounts per service rather than a percentage of the bill.

How a Prudent Claim Pays Out (the Math That Pays Less)

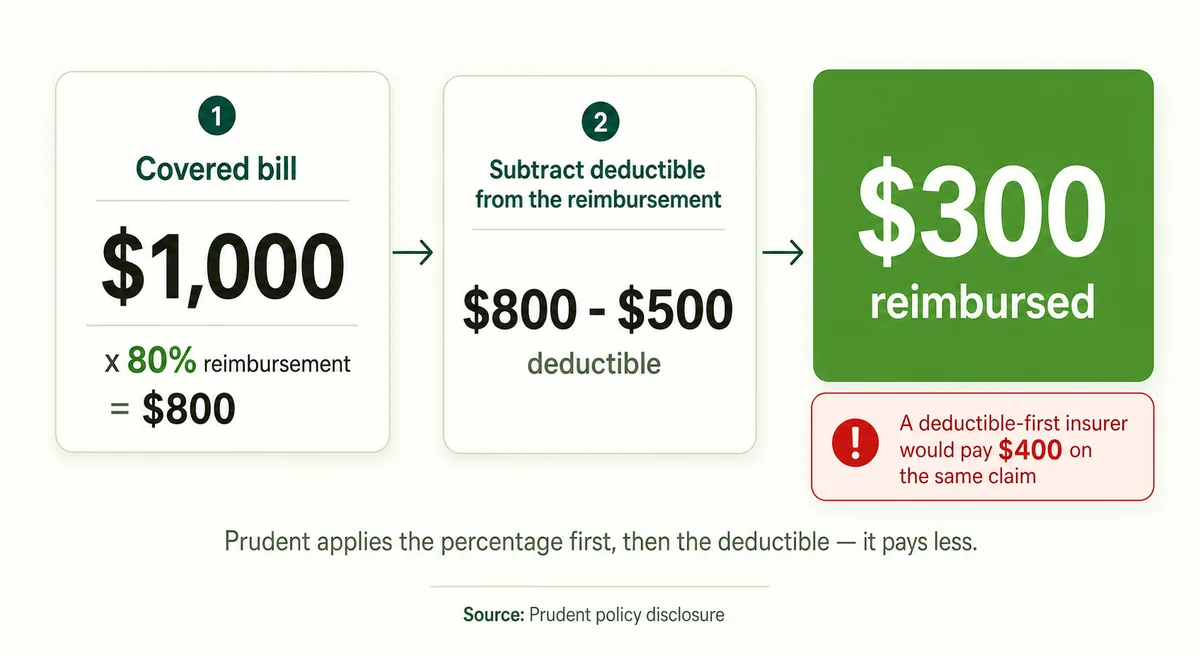

Prudent is a reimbursement policy with an unusual order of operations — and the order quietly costs you money. Most insurers subtract your deductible from the bill and then reimburse a percentage of what's left. Prudent does it the other way around: it applies your reimbursement percentage first, then subtracts the deductible from that reimbursed amount. In its own words, "the deductible is subtracted from the reimbursement amount."

Consider what that does to a real claim. Say you have a $1,000 covered vet bill, 80% reimbursement, and a $500 annual deductible. Prudent pays 80% of $1,000 = $800, then subtracts the $500 deductible, leaving $300. A deductible-first insurer on the identical plan subtracts the $500 from the bill first (leaving $500), then pays 80% = $400. Same inputs on paper, $100 less in your pocket. The gap equals your deductible times the share you don't get back, so it narrows at 90% reimbursement and widens at 70% — a real, checkable difference, not a knock on the brand. (NerdWallet, reviewing Prudent nationally, publishes this same $300-vs-$400 example, so this is how Prudent calculates generally — not a quirk of one state's form.)

Then there's cash flow, which is a separate question from whether a claim is covered. Prudent reimburses you by check or direct deposit after you pay the vet — there is no option to have Prudent pay the clinic directly, and you'll need to file within whatever window your policy specifies. So you front 100% of the bill and wait to be paid back a portion of it. That matters more than the star scores admit: about two-thirds of U.S. owners can absorb no more than $1,000 for lifesaving care. So ask two separate questions before you buy — will this policy pay, and can I float the bill until it does?

Waiting Periods, Pre-Existing & the Fine Print

Prudent's national waiting periods are standard: 5 days for accidents, 14 days for illnesses, and 6 months (180 days) for knee and ligament conditions (Prudent's FAQ). The orthopedic wait is the one you can shorten: have a vet examine your pet and document healthy knees within the first 30 days of the policy, file the knee & ligament waiver, and the six-month cruciate/patella exclusion lifts (Prudent's exclusions page). It only helps a pet with no prior knee trouble, but owners who complete it confirm the exclusion comes off.

Now the fine print where Prudent's own website disagrees with itself, on two rules that decide real claims. First, the curable-condition lookback: a cured condition can become coverable again after a symptom- and treatment-free stretch — but Prudent's pages don't agree on how long that stretch is. One page says 180 days; three others — the pre-existing primer, the FAQ, and a support article — say 365 days. Since the weight of Prudent's current pages points to a full year, assume the stricter 365-day window — don't drop or switch coverage believing a condition treated seven months ago is clean. And note the hard carve-out: knees and ligaments never get this relief. A prior cruciate or patella issue stays pre-existing for good, waiver or not.

Second, what the knee waiver actually buys you. The sample policy says the wait is "waived to 30 days," while the live exclusions text reads those 30 days as your deadline to file — do the exam in the first month and, on that reading, the knee exclusion doesn't apply at all. A third Prudent page once said "14 days"; it now returns a 404, so treat 14 as retired, not current. Either way, your declarations page and the state-filed policy form control — not a marketing page. If your pet has any orthopedic history, get the exact post-waiver rule in writing before you enroll — and confirm in your own policy how an ongoing, already-covered condition is treated at renewal, rather than relying on a forum or a marketing page.

What Prudent Costs — Now and at Renewal

Prudent doesn't publish an "average" premium, because the price is entirely config-driven — your pet's species, breed, age, and ZIP, plus the deductible, reimbursement rate, and annual limit you choose. To ground it: MoneyGeek's tested setup — a 6-year-old Labrador and a 7-year-old Ragdoll at $500 deductible / $5,000 limit / 80%, that $5,000 being MoneyGeek's standardized comparison limit rather than one of Prudent's own tiers ($2,500, $10,000, or unlimited) — came to about $88/month for the dog and $39/month for the cat. Younger pets run much cheaper: NerdWallet's sample mixed-breed dog was $22/month at age 2, rising to $41 by age 8. For context, the industry-average accident-and-illness premium is roughly $62/month for dogs and $32 for cats (NAPHIA, 2024 data) — so Prudent's fuller configs sit above the benchmark and its lean, young-pet ones below it. You can pull a quote down by raising the deductible or lowering the reimbursement percentage — but remember from the claim math above that a lower percentage also shrinks what you get back. Always read the quoted config, never a bare "average."

The renewal story is where Prudent breaks from the script. Pet premiums almost always climb — driven by your pet aging into higher brackets and by veterinary costs, which rose about 5% year over year in early 2026 — and Prudent is no exception to age-based "birthday pricing." But unusually, several Prudent owners report renewals going down: one described consecutive cuts of 18% and 13%, another a state-wide rate decrease. Treat those as owner-reported experiences, not a promise — renewal pricing varies by state, filing, and pet — but they're a real and genuinely uncommon counter to the "insurance only ever gets pricier" assumption. Budget as if your premium will rise with age, and treat any decrease as a bonus.

Does Your State Change the Rules? (Florida & Hawaii, 2026)

One thing no national review flags: in two states, Prudent's own waiting periods are illegal as written. Both Florida (Fla. Stat. §627.71545) and Hawaii (Act 79) enacted pet-insurance laws effective January 1, 2026 that:

- ban waiting periods for accidents — so Prudent's national 5-day accident wait doesn't apply to you;

- cap illness and orthopedic waits at 30 days — collapsing that 6-month knee wait to a month at most;

- put the burden of proving a pre-existing condition on the insurer, not on you; and

- require the company to disclose when the brand differs from the underwriter — the exact Prudent-vs-Markel split we opened with.

These two states modeled their laws on the NAIC's Pet Insurance Model Act (adopted August 2022), and other states are adopting their own versions — but the specifics vary, so don't assume your state carries the same protections. The rule that actually governs is always the one in your state-filed policy form and declarations page. If you live in Florida or Hawaii, these laws override Prudent's national waiting periods for policies issued or renewed under them — so confirm how they apply to your specific policy term rather than assuming an in-force policy changed overnight; everywhere else, check your own state's form to see which waits truly apply to your pet.

Ratings Split & What Owners Say

Prudent's aggregate scores look glowing — Trustpilot near 4.8 and an A+ from the BBB — but treat those as a reputation signal, not proof of how claims actually go. Many of those reviews are solicited right at enrollment, so they skew toward how easy the sign-up felt, not how a $3,000 claim got paid a year later. (Ignore the top-ranking UK Trustpilot page entirely — it's a different market with different policies.) The fuller picture comes from separating the praise from the complaints.

What owners praise most is claim speed. Real posters describe reimbursements landing in under a week — one reported a claim processed the same morning it was filed — against horror stories of six-to-eight-week waits at other insurers. That's Prudent's standout, and it shows up consistently enough to believe.

The complaints cluster in three spots. First, the exam-fee surprise — owners who skipped the rider find those charges carved out of a payout. Second, pre-existing disputes, the most substantive gripe: claims denied on a pre-existing basis, sometimes with the stated reason shifting between the first denial and the appeal. Third, billing friction at sign-up — double charges through comparison-site funnels and hard-to-reach support. You'll also see a recurring "will a small company like this get bought out?" worry — fair to raise, though remember the risk is carried by Markel, not Prudent's own balance sheet. None of this makes Prudent a scam; it makes it a fast-paying insurer whose fine print and onboarding trip some owners up. Add the exam-fee rider if you want it, and document your pet's health at enrollment.

Prudent vs. the Alternatives

Prudent's edge is a broad, build-your-own policy that owners say pays claims fast; its soft spots are the deductible-after-reimbursement math, the pay-first-get-reimbursed model, and the fact that it's a small, newer agency — though the carrier that actually bears the risk, Markel, is large and financially strong. Which of those matters most depends on what you're optimizing for — so shop by priority, not by star score.

If cash flow is the problem — you can't comfortably float a five-figure vet bill — Trupanion's direct-to-vet payment is the structural fix Prudent doesn't offer — at clinics that use its software, it can pay your vet directly so you never front the full bill (worth confirming your vet participates). If you want the simplest experience, Lemonade's app-first claims are quick and its base premiums often run low, though its dental and some breed-specific coverage are thinner — read the fine print if you have a toy breed. If dental is your priority, Pumpkin includes stronger dental coverage as standard, though it tends to cost more for older pets.

None of these is a clean "winner." Prudent competes best for the owner who wants wide, customizable coverage and fast reimbursement and can carry the bill for a week or two. If you landed here because another insurer priced you out or denied a claim, know the catch before you jump: pet insurance generally isn't portable. Switching to Prudent — or any new insurer — is a fresh start, so a condition your pet already has will usually be treated as pre-existing and excluded, no matter how continuously you were insured elsewhere. Get written confirmation of how your pet's history will be handled before you cancel your current policy.

Frequently Asked Questions

Is Prudent Pet Insurance legit, and who underwrites it?

Yes — Prudent is a legitimate, widely sold insurer. "Prudent Pet" is a brand and agency (Prudent Pet Insurance Agency) that handles sales, billing, and claims, but your policy is underwritten by one of two Markel companies — Markel Insurance Company (NAIC #38970) or Markel American Insurance Company (NAIC #28932), depending on your state. Both are rated AM Best A (Excellent), so the company standing behind your policy is financially strong.

What vets can I use with Prudent Pet Insurance?

Any licensed veterinarian in the U.S. — Prudent has no network and no in-network/out-of-network distinction. You pay whichever vet, ER, or specialist you choose, then file for reimbursement. That freedom is standard for reimbursement-model pet insurance and is one of Prudent's genuine strengths.

Does Prudent Pet Insurance cover exam fees?

Not by default. Prudent lists exam fees as excluded "unless you have chosen to include them" — they're an optional paid add-on you attach at purchase or renewal. Without that rider, the exam portion of a vet bill isn't reimbursed, which surprises some owners at claim time.

Does Prudent pay my vet directly, or reimburse me?

Prudent reimburses you, not the clinic. You pay the vet in full, submit the claim, and Prudent pays you back by check or direct deposit — there's no direct-to-vet payment option. Plan to front the entire bill and wait to be reimbursed a percentage of it.

Why does Prudent seem to pay less than other insurers?

Because of the order of operations. Prudent applies your reimbursement percentage first, then subtracts the deductible from that reimbursed amount. On a $1,000 covered bill at 80% reimbursement with a $500 deductible, that works out to $300 — versus $400 from an insurer that subtracts the deductible from the bill first. The gap equals your deductible times the share you don't get back, so it shrinks at 90% reimbursement and grows at 70%.

What are Prudent Pet's waiting periods?

Nationally, 5 days for accidents, 14 days for illnesses, and 6 months for knee and ligament conditions — the knee wait is waivable if a vet documents healthy knees within the first 30 days. Note that Florida and Hawaii laws effective January 1, 2026 ban accident waiting periods and cap the others at 30 days, so your state may override these.

What counts as a pre-existing condition with Prudent?

Any condition that showed signs before your coverage started or during a waiting period. Some cured conditions can become coverable again after a symptom- and treatment-free stretch — Prudent's own pages state both 180 and 365 days, so assume the stricter 365-day window. Knee and ligament conditions are the hard exception: a prior issue there stays pre-existing permanently.

Can I switch to Prudent without losing coverage?

Not for a condition your pet already has. Pet insurance generally isn't portable between companies, so a condition that is already pre-existing when you enroll — including one first treated at a prior insurer — usually stays excluded. If Prudent is already covering a condition, keeping the policy in force without a gap is how you avoid it being re-evaluated, though every future claim still depends on the policy's limits and terms. The safest move is to document your pet's health at enrollment and get written confirmation of how any existing condition will be handled before you cancel other coverage.

How much does Prudent Pet Insurance cost?

It's entirely config-driven — species, breed, age, and ZIP, plus the deductible, reimbursement rate, and annual limit you choose. One reviewer's mid-range setup came to about $88/month for a dog and $39 for a cat, while younger pets cost noticeably less. Always price your own configuration in a live quote rather than trusting a bare "average."

Sources

- Prudent Pet Insurance underwriting disclosure (agency + Markel underwriters, NAIC #38970/#28932) — Prudent Pet

- AM Best affirms Markel North America Insurance Group — A (Excellent), affirmed 2025-11-21 — AM Best

- Prudent Pet plans (three tiers; annual limits; exam fees an optional add-on; Ultimate sub-limits) — Prudent Pet

- Prudent Pet exclusions (exam fees "unless you have chosen to include them"; full exclusion list) — Prudent Pet

- Prudent Pet — Notice to California Residents (payout order: deductible subtracted from the reimbursement amount) — Prudent Pet

- Prudent Pet FAQ (reimbursement-first: pay the vet, then reimbursed by check or direct deposit) — Prudent Pet

- Prudent Pet Insurance review (publishes the $300-vs-$400 payout-order example) — NerdWallet

- Pet owners have skipped or declined veterinary care (66% can afford <=$1,000 for lifesaving care) — PetSmart Charities-Gallup

- Prudent Pet — what is covered (states the 180-day curable window — the outlier page) — Prudent Pet

- Prudent Pet — pre-existing conditions 101 (states the 365-day curable window; updated 2025-08-11) — Prudent Pet

- Prudent Pet sample policy (knee wait "waived to 30 days"; controlling form language) — Prudent Pet

- Prudent Pet review (~$88/mo dog, ~$39/mo cat on a 6-yo Lab / 7-yo Ragdoll at $500/$5,000/80%) — MoneyGeek

- US pet-insurance industry surpasses $4B in 2024 (avg A&I premium ~$62/mo dog, ~$32/mo cat) — AVMA (NAPHIA 2025 SOI)

- Veterinary-care prices up ~5% YoY, early 2026 (BLS CPI, via Fortune) — Fortune

- r/petinsurancereviews — Prudent Pet review thread (owner-reported renewal decreases of 18% and 13%) — Reddit

- Florida Pet Insurance Act — Fla. Stat. 627.71545 (accident-wait ban; 30-day cap; insurer burden; brand-vs-underwriter disclosure; eff. 2026-01-01) — Florida Legislature

- Hawaii Act 79 / HB544 CD1 (accident-wait ban; 30-day cap; no renewal waits; insurer burden; eff. 2026-01-01) — Hawaii State Legislature

- NAIC Pet Insurance Model Act #633 record (adopted August 2022; template for state pet-insurance laws) — NAIC

- Prudent Pet (US reviews; aggregate ~4.8 rating; sentiment, partly enrollment-solicited) — Trustpilot

- Prudent Pet Insurance Agency, Downers Grove IL (A+; complaints incl. pre-existing/billing) — Better Business Bureau

- Prudent Pet Insurance (owner sentiment; pre-existing denial and billing complaints) — ConsumerAffairs