Is Odie pet insurance legit, and will it actually pay your claims? The short version: Odie is a real, licensed operation with genuinely low premiums — but the thing most reviews get wrong is that "Odie" isn't one insurance company, or even one policy. Odie is a licensed producer and administrator (think of it as the storefront and the paperwork desk), while the financial risk sits with separate underwriters: Trisura on its current plans and Accredited on its legacy and ManyPets-renewal books, depending on your state and when you signed up (Odie's own licensing disclosures).

That distinction is the whole ballgame, because the carrier and the state-filed contract behind your policy — not Odie's marketing page — decide how a claim is actually paid.

If you were moved to Odie when ManyPets stopped writing U.S. policies, this review is especially for you: we'll walk through what changed, whether your already-covered conditions carry over, and whether it's worth staying put.

Here's our honest take, up front. For a young, healthy pet with a clean medical record and a tight budget, Odie's low price can genuinely make sense. For a ManyPets switcher in the middle of a claim — or anyone who values fast, frictionless reimbursements — the documentation demands and the 2025–2026 service complaints are real risks worth weighing. Over the next few sections we'll show you who actually underwrites your policy, how the reimbursement math works, the records you'll be asked to produce, what Odie's claims-service track record looks like, and exactly what to do if a claim stalls — so you can decide for your situation, not ours.

Table of Contents

- Who Actually Underwrites Odie? (It's Not One Product)

- Odie and ManyPets: What Changed When You Were Moved

- How Odie Pays Claims: The Reimbursement Math

- The Documentation Catch: 18 Months of Records

- Odie's Claims-Service Record: The ManyPets Migration and BBB

- What Odie Costs vs. the U.S. Average

- Coverage, Waiting Periods, and Pre-Existing Conditions

- If Your Claim Stalls: How to Escalate

- Should You Stay, Switch, or Skip Odie?

- Frequently Asked Questions

- Sources

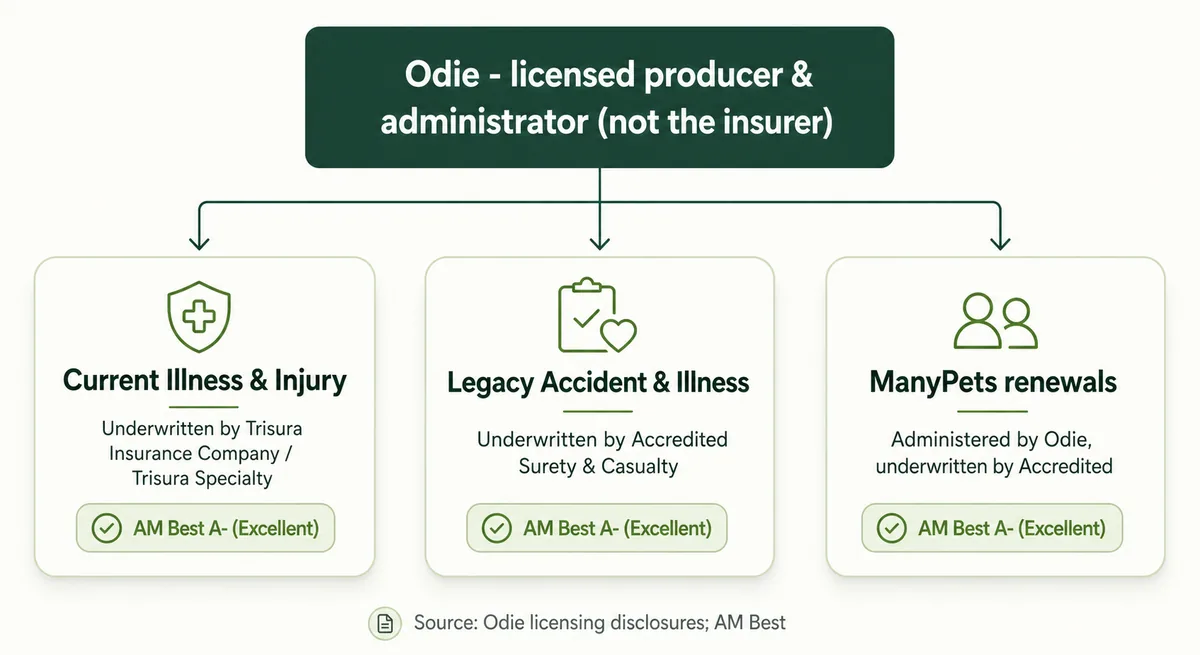

Who Actually Underwrites Odie? (It's Not One Product)

Here's the fact that reframes every Odie review: Odie doesn't carry the insurance risk, and "Odie" isn't a single policy. Odie Pet Insurance Marketing, Inc. is a licensed insurance producer and administrator — it sells the plans, services your account, and handles your paperwork — while the actual coverage is written by separate, financially rated carriers (Odie's licensing disclosures). Which carrier backs your policy depends on your state and which of Odie's books you're on.

That matters more than any star rating, because the underwriter's state-filed contract — not Odie's website — is what a claims adjuster reads when deciding whether to pay you. Here's how the book breaks down:

| Your Odie policy | Who actually underwrites it | Financial strength (AM Best) |

|---|---|---|

| Current Illness & Injury plans | Trisura Insurance Company (Trisura Specialty in Maine, and as a surplus-lines writer in CA, MA, MN & NY) | A- (Excellent), affirmed July 2025 |

| Legacy Accident & Illness, Accident-Only, and ManyPets renewals | Accredited Surety & Casualty Company | A- (Excellent), affirmed Aug 2024 |

| Wellness / routine-care add-on | Odie itself — and it is not insurance | — |

Two practical takeaways. First, both risk-carriers hold an A- ("Excellent") rating from AM Best — a strong mark of financial stability, though a rating is an opinion, not a guarantee. In plain terms, Odie's well-documented problems are about service, not the carrier's ability to pay claims. Second, if you live in California, Massachusetts, Minnesota, or New York, your current plan is written by Trisura Specialty on a surplus-lines (non-admitted) basis, which means your state's guaranty fund would not step in to pay claims if the insurer ever failed (Odie's state-residents disclosure). Given the A- rating that's a small risk, but it's the kind of fine print worth knowing before you buy.

One correction, because several popular Odie reviews still get this wrong: the underwriters are Trisura and Accredited today — not the "Clear Blue" or "PrimeOne" names you'll see on some older pages. If a review still lists those carriers, it predates Odie's current structure, and its plan details are probably out of date too.

Odie and ManyPets: What Changed When You Were Moved

If ManyPets moved you to Odie, here's the short version: Odie didn't buy your policy — it took over administering it. Odie became the program manager for ManyPets' U.S. policies on January 1, 2025, and renewed policies stay underwritten by Accredited, the same carrier ManyPets already used. Your renewal is automatic but voluntary: Odie sends notices roughly 55, 30, and 3 days out, and you get a 7-business-day window to opt out (Odie's ManyPets transition page).

On paper, the promises are reassuring. Odie says it honors your existing covered conditions "as defined by your ManyPets policy," charges the same rates ManyPets' own filings would have produced (adjusted for your pet's age), and applies no new waiting periods at rollover. Conditions that predate your original ManyPets policy stay excluded, exactly as before.

In practice, this is the book generating Odie's loudest complaints. On Reddit, transferred owners describe three recurring shocks — these are owner reports, not measured rates: premiums jumping at renewal; a previously unlimited annual limit dropping to $20,000; and, most painful, conditions that developed during the ManyPets policy being questioned or denied as "pre-existing" despite the continuity promise.

Our honest read: the continuity promise is real — it's Odie's stated policy, and when it's applied correctly it protects you. But the gap between that written promise and some owners' actual claim experience is exactly why this review spends so much time on the documentation and claims sections that follow. If you're weighing whether to stay, read those before you make a move — switching carriers now can turn today's covered conditions into tomorrow's pre-existing exclusions.

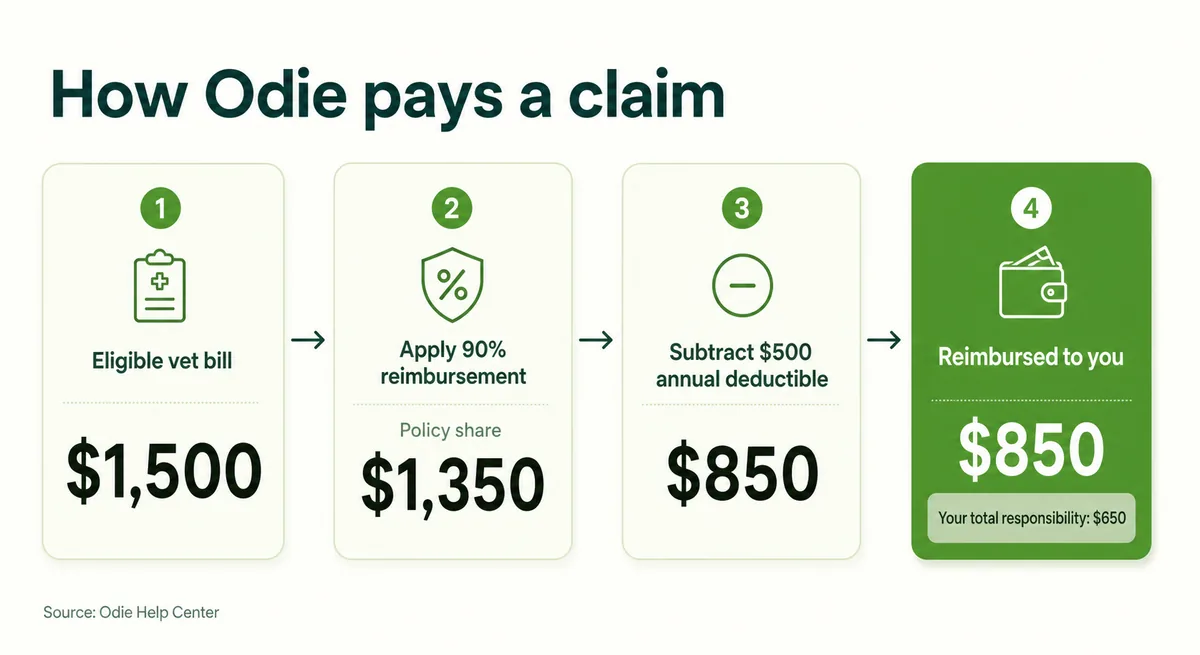

How Odie Pays Claims: The Reimbursement Math

Odie reimburses you after the vet visit, and the order it runs the math in trips up a lot of buyers: Odie applies your reimbursement percentage first, then subtracts your annual deductible from what's left (Odie's own claim-calculation examples). That's the opposite of what many people picture.

Here's Odie's own worked example. Say your pet has a $1,500 eligible vet bill, a 90% reimbursement rate, and a $500 annual deductible:

- Apply 90% reimbursement → the policy's share is $1,350 (you cover the other 10%, or $150, as coinsurance).

- Subtract the $500 annual deductible from that share → $850 is reimbursed to you.

- Your total out of pocket: $650 ($150 coinsurance + $500 deductible).

Why the order matters: a "deductible-first" carrier would subtract the $500 before applying the percentage — ($1,500 − $500) × 90% = $900 — paying you $50 more on the very same bill. Because the deductible is annual, that's a one-time difference of about $50 in this example, not something that repeats on every visit — but it's the single detail Odie reviews most often get backwards.

One thing that works in your favor: the deductible is annual, not per-claim. Once you've met it, later claims in the same policy year are reimbursed at your full percentage with nothing more subtracted, as Odie shows in its multi-claim example. And for a planned, high-cost procedure, it's worth asking Odie in advance what it expects to cover — treat that as an estimate, not a binding guarantee of payment. Still, confirm your own reimbursement percentage, deductible, and annual limit on your declarations page — those three numbers, applied in this order, decide every payout you'll ever get.

The Documentation Catch: 18 Months of Records

The most common real complaint about Odie isn't the price or the payout percentage — it's the paperwork. To approve a claim, Odie reviews your pet's medical records from the 18 months before your policy started, using them to set a health "baseline" and flag anything pre-existing (Odie Help Center). And it wants the complete file.

"Complete" is stricter than most owners expect. Odie asks for full SOAP notes — vital signs, history, clinical assessments, treatment plans, and medications — and says discharge summaries, invoices, or health certificates alone don't count. The policy language goes further: in Odie's sample policy, if you can't or won't provide a complete medical history when asked, Odie "may deny your claim," and if it requests more information and doesn't receive it within 30 days, the claim can be closed. (Exact terms vary by your state and underwriter, so check your own policy.) Chasing records from a former vet is on you, too — Odie's contract excludes records-retrieval and claim-processing fees, so any charge to pull that file comes out of your pocket.

The practical fallout: your first claim is usually the slowest, because that's when the records review happens. Adopted a pet with no paper trail? Odie accepts a nose-to-tail vet health report in place of the missing history.

Here's the honest line between a fair denial and a fixable one. If your pet's records genuinely show a condition that began before coverage, that's a legitimate pre-existing exclusion, and an appeal usually won't change it — though it's still worth appealing when the condition's onset, its classification, or the records themselves are truly in dispute. But if a routine "annual wellness" visit gets coded as an illness, or records you already sent are treated as "missing," that's an error worth appealing with your vet's written support (one owner describes exactly this, and we cover how to push back in the escalation section below). Either way, never skip or delay veterinary care to keep a record clean — the coverage is never worth your pet's health. Get the care first, then fight the paperwork.

Odie's Claims-Service Record: The ManyPets Migration and BBB

This is the part of the review that should give a prospective buyer pause — but it needs the right frame. Two kinds of evidence sit here: documented complaint records and owner sentiment. They point the same direction, but only the first is actually measured.

On the documented side, the Better Business Bureau gives Odie an "F" rating and, in November 2025, opened a formal investigation into its business practices after consumers alleged delayed claims, missing status updates, and non-responsiveness. BBB says it sent a formal inquiry on November 26, 2025, and that as of December 10, 2025, the company had not responded (BBB's Odie profile). That same profile shows 155 complaints, and its customer-review average is 1.03 out of 5 across 67 reviews.

On the sentiment side — self-selected reviewers, not a failure rate — Odie holds roughly 1.9 out of 5 on Trustpilot, where reviewers describe claims "taking months" (Trustpilot). On Reddit, transferred ManyPets owners repeatedly describe a gap between Odie's stated processing target and a lived reality closer to 60–90 days, a phone line no one answers, and enough shared frustration that some began organizing a class-action effort.

Now the counterweight, because it's real: plenty of owners do get paid. On those same threads, one poster reported more than $55,000 reimbursed across two dogs with cancer, including end-of-life costs, and others describe solid four- and five-figure payouts with only slow timing to complain about. A share of the angriest reviews also come from people who bought insurance after a problem appeared and then met a legitimate pre-existing exclusion — that's a coverage rule, not a scam.

Our read: Odie's money is sound (remember, both underwriters are A-rated), and it does pay claims — but its service and speed through 2025–2026 are a genuine, documented weak point, concentrated in the ManyPets-transition book. If fast, frictionless reimbursement is high on your list, weigh that heavily before you buy or stay.

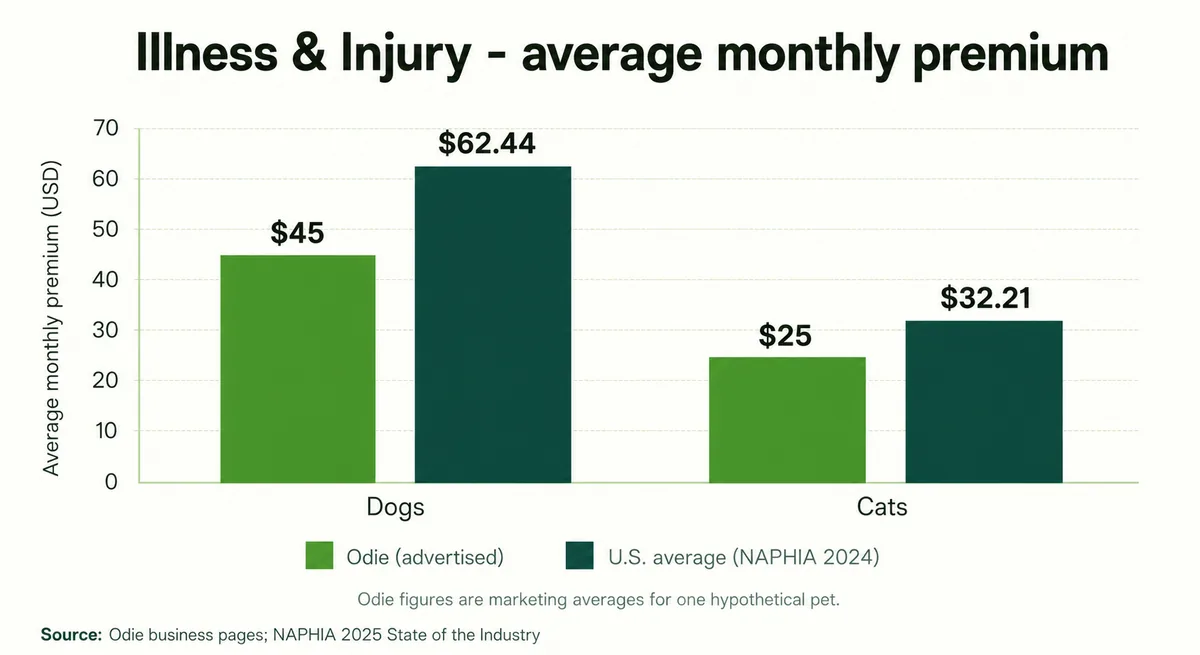

What Odie Costs vs. the U.S. Average

Odie's headline appeal is price, and on paper it's real: Odie advertises average illness-and-injury premiums well below the national number. But that figure needs an asterisk, because Odie's "average" isn't a rate you can hold it to — it's a marketing estimate for one hypothetical pet, quoted with no reimbursement percentage, deductible, or annual limit attached.

Here's the comparison, with sources so you can see the gap for yourself:

| Illness & Injury, average monthly | Dogs | Cats |

|---|---|---|

| Odie (advertised) | ~$38–$45 | ~$25–$28 |

| U.S. average (NAPHIA, 2024) | $62.44 | $32.21 |

About that Odie range: the company quotes roughly $45 (dogs) and $25 (cats) on its business pages but $38 and $28 on its consumer illness-and-injury page for a 3-year-old mixed-breed pet. We show both instead of splitting the difference — the real number depends on the cost-sharing config Odie doesn't publish. NAPHIA's $62.44 dog / $32.21 cat figures, by contrast, are weighted across millions of real in-force U.S. policies — so Odie's advertised premiums land well under market — roughly 28–39% below for dogs and 13–22% below for cats — genuinely cheap if the coverage behind them holds up.

Odie's Accident-Only plan is the clearest bargain: about $9/month for dogs and $6/month for cats at a fixed 90% reimbursement, $250 deductible, and $10,000 annual limit (Odie) — under NAPHIA's accident-only averages of about $16 and $9. It's inexpensive for a reason, though: it covers only accidents, not illness.

The honest way to read all of this: a low premium is only a deal if it pays when you claim. Run the math for your own pet — premium times 12 against a realistic vet bill at your actual reimbursement percentage and deductible — and weigh Odie's price against the service record above, not on its own.

Coverage, Waiting Periods, and Pre-Existing Conditions

What Odie covers is standard accident-and-illness territory — diagnostics, surgery, hospitalization, and treatment for new conditions. The fine print that actually decides claims lives in three places: waiting periods, pre-existing rules, and age limits — and because two different carriers underwrite Odie, these vary by segment and by state. Don't trust a single "the Odie waiting period is X" line; check your own declarations page.

Waiting periods, per Odie's state-residents disclosure: current Trisura plans use a 14-day illness wait; Accredited-backed policies use 15 days for illnesses (and, in Odie's wording, "most injuries"); there's a 30-day wait for orthopedic conditions not caused by an accident; and there's no waiting period for an accident or an injury from a sudden, unexpected event. Those limits track the NAIC Pet Insurance Model Act, which caps illness and orthopedic waits at 30 days, bans accident waiting periods, and — importantly — puts the burden on the insurer to prove a condition is pre-existing. A dozen-plus states have adopted it, so your exact protections depend on where you live.

Pre-existing conditions are excluded, as at every carrier — but keep the distinction that trips people up: you can almost always buy a policy, yet a condition already sitting in your pet's records won't be covered. Odie does let some curable conditions (a one-off UTI or ear infection, say) become eligible again if they resolve completely and later recur; incurable, chronic ones like diabetes stay excluded for good.

On age: Odie's current Trisura plans advertise no upper age limit, but Accredited-underwritten coverage is available only for pets between 8 weeks and 14 years old (Odie Help Center) — so "Odie has no age limit," repeated by many reviews, simply isn't true across the board. And one last line to keep straight: Odie's wellness/routine-care add-on is not insurance. It's a separate fixed-allowance product, so don't count it toward your accident-and-illness coverage or its limits.

If Your Claim Stalls: How to Escalate

If your Odie claim is stuck in "review" with no reply, you have more leverage than the silent inbox suggests. None of these steps is a guaranteed fix, but owners who've broken a logjam tend to use the same playbook — roughly in this order:

- Email the underwriter directly, not just Odie. Remember, Odie only administers the policy; the carrier (Trisura or Accredited) bears the risk. Owners repeatedly report that reaching the underwriter got claims reviewed and approved within hours after weeks of silence from Odie.

- File a complaint with your state's Department of Insurance (and, if needed, the attorney general). This is the real lever — a regulator's inquiry compels a response in a way the BBB can't. (The BBB is a pay-to-play directory that Odie isn't even accredited with, though it does sometimes respond there.)

- Put it in writing, formally. A certified letter citing Odie's own stated claim timeline and your state's claim-handling rules builds a paper trail regulators respect. Those deadlines vary by state and by claim stage, so pull the specifics from your Department of Insurance rather than relying on a single national number.

- Work the appeal. Send appeals to Odie's claims team with a completed appeal form and a letter from your vet explaining why the denied item isn't pre-existing; if it's denied again, Odie's process routes to a binding third-party veterinary review (Odie Help Center).

Two habits head off stalls in the first place: for a planned, expensive procedure, ask Odie in advance what it's likely to cover (treat the answer as an estimate, not a guarantee of payment); and keep your own copy of every record you submit, so "we never received it" can't quietly close your claim. If you want to understand how we weigh carriers like this, our methodology page lays it out — but the fastest relief with Odie is almost always the underwriter and the regulator, not one more email to support.

Should You Stay, Switch, or Skip Odie?

There's no single verdict on Odie — the right call depends entirely on your pet's situation. Here's how we'd think it through for the three readers who tend to land on this page.

The budget-first buyer with a young, healthy pet. If your dog or cat has a clean medical record and price is your main constraint, Odie can genuinely work. You'll get below-average premiums from an A-rated carrier, and the documentation burden is lightest when there's little history to review. Just go in clear-eyed about a slow first claim, and price the plan on its real config — reimbursement percentage, deductible, and limit — not the headline.

The ManyPets switcher deciding whether to stay. This is the hardest call, so start with the risk: leaving Odie usually turns your pet's current conditions into pre-existing ones at the next insurer, and restarts waiting periods — which can cost far more than any premium you'd save. If your pet is healthy and you just want better service, shopping around is reasonable. But if you're mid-treatment or your pet developed conditions while covered, staying (and leaning on the escalation playbook above) is usually the safer financial move. Don't chase a lower price and accidentally strand a chronic condition.

The buyer who prizes fast, frictionless claims. If quick, no-drama reimbursement matters more to you than a few dollars a month, Odie's 2025–2026 service record is a real strike against it. Frustrated Odie owners commonly move to Spot (often cited for flexible, customizable plans), while others weigh AKC, which can cover some pre-existing conditions after a waiting period. We line carriers up side by side in our reviews hub rather than crown one winner here.

The bottom line: Odie is a legitimately cheap, financially sound option whose weak spot is service speed. Match that trade-off to your pet's health and your own tolerance for paperwork, and you'll know whether it's a smart buy or a pass.

Frequently Asked Questions

Is Odie a good pet insurance company?

Odie is a legitimate, financially sound option that's genuinely inexpensive, but its weak spot is claims service. Its policies are underwritten by A-rated carriers (Trisura and Accredited), so the money behind them is solid. However, the Better Business Bureau gives Odie an "F" rating and opened a November 2025 investigation into claim delays and non-responsiveness. Whether it's "good" depends on your pet: strong value for a young, healthy pet on a budget, riskier if you need fast, frictionless reimbursement.

Who underwrites Odie pet insurance?

Odie itself doesn't underwrite anything — it's a licensed producer and administrator. Your policy is written by Trisura Insurance Company or Trisura Specialty Insurance Company (current illness-and-injury plans) or Accredited Surety & Casualty (legacy plans and ManyPets renewals), depending on your state and enrollment date (Odie's disclosures) — check the insurer named on your declarations page. Both carriers hold an A- ("Excellent") rating from AM Best. Older reviews that name "Clear Blue" or "PrimeOne" are out of date.

Is Odie the same as ManyPets?

No. ManyPets stopped writing U.S. pet insurance, and Odie became the program manager for those policies on January 1, 2025 (Odie). If you were a ManyPets customer, your renewed policy stays underwritten by Accredited at ManyPets' filed rates, and Odie says conditions covered after your original ManyPets policy began remain covered. In practice, this transition book has generated Odie's heaviest complaint volume.

How long does Odie pet insurance take to pay a claim?

Odie's Help Center says a routine claim is processed in as little as five business days once it has everything it needs, with reimbursement by direct deposit shortly after. In practice, many owners — especially ManyPets transfers — report far longer, often 30 to 90 days end to end, with first claims the slowest because that's when Odie reviews your pet's full medical history. If yours stalls, contacting the underwriter directly and filing a complaint with your state insurance department are the fastest ways to get it moving.

Does Odie pet insurance cover pre-existing conditions?

No — like nearly all pet insurers, Odie excludes pre-existing conditions, meaning anything diagnosed or showing signs before your policy started or during a waiting period. It does allow some curable conditions, such as a one-off ear infection or UTI, to become eligible again if they fully resolve and later recur; chronic conditions like diabetes stay excluded. Keep the distinction in mind: you can almost always buy a policy, but an existing condition won't be covered.

Why does Odie need 18 months of my pet's records?

Odie reviews your pet's medical records from the 18 months before your policy start to set a health baseline and identify pre-existing conditions (Odie Help Center). It asks for complete SOAP notes — not just invoices or summaries — and can deny or close a claim if the history isn't provided, which is why first claims are slow. Never delay veterinary care to keep a record clean: get the care, then handle the paperwork.

Is Odie's wellness plan insurance?

No. Odie's wellness and routine-care add-on is explicitly not insurance — it's a separate product with fixed annual allowances for things like exams and vaccines, not percentage reimbursement. It won't count toward your accident-and-illness coverage or limits, and in states that have adopted the NAIC model rules, wellness programs must be sold and disclosed separately from insurance. Treat it as a budgeting tool for predictable costs, not protection against a large, unexpected vet bill.

What is the best rated pet insurance company?

There's no single "best" — it depends on your pet's age and health and on what you value most. Odie stands out on price but not on claims service, so owners who prize fast, reliable reimbursement often prefer carriers with stronger service records. We line them up side by side in our reviews hub. The right pick balances premium, reimbursement terms, and how dependably a company actually pays when you file.

Sources

- Licensing Disclosures — Odie Pet Insurance

- Which States Is Odie Available In? — Odie Pet Insurance

- AM Best Affirms Ratings of Trisura Insurance Company — AM Best

- AM Best Affirms A- (Excellent) Ratings of Accredited Insurance Holdings Members — Accredited / AM Best

- Important Information About Your ManyPets Transition — Odie Pet Insurance

- ManyPets, Powered by Odie — Odie Pet Insurance

- Stick with Odie or find another company (former ManyPets customer) — Reddit r/petinsurancereviews

- How Claims Are Calculated — Odie Pet Insurance

- Help Center — Odie Pet Insurance

- Wyoming Trisura Sample Policy (PDF) — Odie Pet Insurance / Trisura

- Owner account: wellness-exam claim denied as pre-existing — Quora

- Odie Pet Insurance Marketing Inc — BBB Profile — Better Business Bureau

- Odie Pet Insurance Reviews — Trustpilot

- Anyone interested in a class action lawsuit against Odie Pet Insurance? — Reddit r/petinsurancereviews

- Odie deleted their Google Business page (thread with a $55k payout account) — Reddit r/petinsurancereviews

- Illness & Injury Plan — Odie Pet Insurance

- Accident-Only Plan — Odie Pet Insurance

- State of the Industry Report 2025 — Highlights — NAPHIA

- Pet Insurance Model Act (#633) — NAIC / NCOIL

- Can I Get Pet Insurance That Covers Pre-Existing Conditions? — Odie Pet Insurance

- Odie finally responded because I contacted the underwriter — Reddit r/petinsurancereviews

- Odie Pet Insurance — BBB Customer Reviews — Better Business Bureau