If you're reading Hartville pet insurance reviews in 2026, you probably arrived with two nervous questions: can I even still buy this? and is Hartville the same company as ASPCA or 24PetWatch? We read Hartville's actual policy, its underwriters' financial-strength ratings, and what real owners report — including the many who were moved onto Hartville without asking — so you don't have to.

The short answers first. Yes, Hartville is still selling new policies as of 2026 — its own quote engine returns real prices and doesn't hand you off to another brand. And no, "Hartville" isn't a single insurer: it's a brand marketed by an agency (PTZ Insurance Agency) and underwritten by one of two carriers — Independence American or United States Fire — depending on your policy form. Its main plan reimburses the actual vet bill at 90%, 80%, or 70%.

So this is a "should you," not a "can you," decision — and the answer splits by who you are. Below, we give a conditional verdict for two readers at once: someone shopping Hartville new, and someone involuntarily switched to it from 24PetWatch who needs to know what their policy actually is and what to do next.

Table of Contents

- The Verdict: Is Hartville Worth It (and Can You Still Buy It)?

- Who Actually Underwrites Hartville (and Are They Solid)?

- Is Hartville the Same as ASPCA or 24PetWatch?

- What Hartville Covers (and the Exclusions That Bite)

- Waiting Period, Pre-Existing & the Knee/Ligament Trap

- Legacy vs. Newer Hartville Policies: Why Two Owners Disagree

- What Hartville Costs — Now and as Your Pet Ages

- The 24PetWatch to Hartville Migration: What Transferred Owners Are Living

- Claims, Complaints & the Review-Freshness Problem

- Hartville vs. the Alternatives (ASPCA, Spot, Lemonade)

- Frequently Asked Questions

- Sources

The Verdict: Is Hartville Worth It (and Can You Still Buy It)?

Start with the question buried in most Hartville pet insurance reviews: yes, you can still buy it. As of 2026, Hartville's own site quotes and sells new accident-and-illness policies — so the real decision is whether you should, and that depends on who you are.

Hartville's pitch is breadth: one plan that reimburses your actual vet bill, builds in exam fees and dental-illness treatment, and lets you choose your reimbursement rate. The trade-offs are price and paperwork — premiums start mid-market and climb steeply as your pet ages, and what you're actually covered for depends on which policy form you happen to hold.

Hartville is a reasonable fit if you:

- want broad coverage and will actually read your policy — exam fees, dental-illness treatment, and hereditary conditions are built into the base plan;

- are insuring a younger pet and care more about what's covered than about the rock-bottom premium;

- would value having the insurer pay your vet directly — an option, if you request it on the claim form.

Look elsewhere if you:

- are shopping purely on price — several rivals quote lower for the same pet;

- have a pet with a knee or ligament problem, or any condition that already looks pre-existing — Hartville's rules will bite (see the knee trap below);

- were involuntarily moved to Hartville from 24PetWatch and are staring at a denial or a big premium jump — you may be better off appealing or switching, which we walk through near the end.

The rest of this review settles what should actually decide it: who stands behind your policy, what the fine print really does, what it costs over time, and exactly what that 24PetWatch migration means for you.

Who Actually Underwrites Hartville (and Are They Solid)?

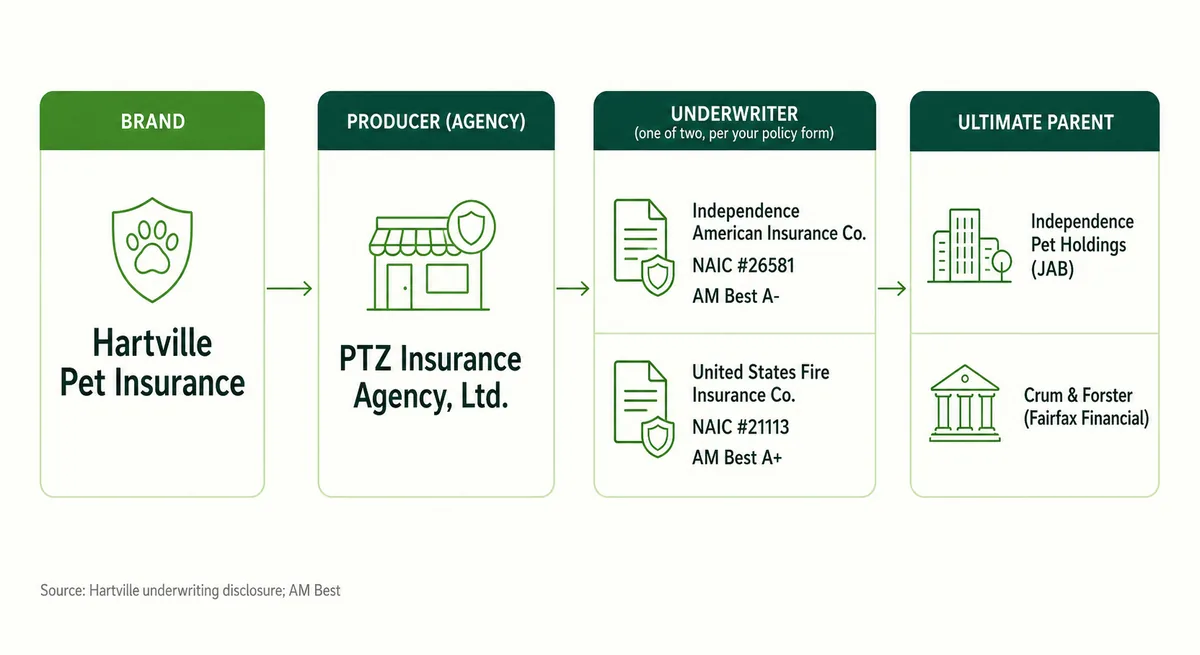

Here's the part most Hartville reviews get wrong: Hartville isn't an insurance company. "Hartville" is a brand, sold by a licensed agency — PTZ Insurance Agency — that markets and services the policy but doesn't pay your claims. The carrier that actually holds the risk is named on your policy documents, and it's one of two.

Per Hartville's own disclosure, policies are underwritten by "either Independence American Insurance Company or United States Fire Insurance Company," depending on your state and policy form — and the two carriers aren't equally strong. United States Fire (NAIC #21113), a Crum & Forster company, was upgraded to an AM Best "A+ (Superior)" rating in 2025. Independence American (NAIC #26581) sits two notches lower at "A- (Excellent)" — and spent part of 2025 under review over a pet-reinsurance accounting problem, resolved only after its parent added $125 million in capital. Both are financially sound; just read the rating against the carrier on your policy, not the "Hartville" brand.

That corporate family tree also answers a question owners often ask — is Hartville the same company as ASPCA? Effectively, yes: the producer and both underwriters are shared across Hartville, ASPCA Pet Health Insurance, and 24PetProtect — sibling brands on the Independence Pet Holdings platform (the JAB-owned pet-insurance group). The two carriers, though, sit under different parents: Independence American rolls up to Independence Pet Holdings and JAB, while United States Fire rolls up to Crum & Forster and Fairfax Financial — so, depending on your form, a Hartville policy can be backed by an entirely different corporate parent than the brand suggests.

One catch: Hartville won't publish a state-by-state map of which carrier you'll get. Its disclosure just says to "refer to your policy forms." So the only reliable way to know who stands behind your coverage is to read your own declarations page.

Is Hartville the Same as ASPCA or 24PetWatch?

Essentially, yes — and it trips up a lot of owners. Hartville, ASPCA Pet Health Insurance, and 24PetProtect are separate brand names sitting on the same machinery: the same producer (PTZ Insurance Agency), the same two underwriters (Independence American or United States Fire), and the same parent, Independence Pet Holdings. Their policy disclosures are, word for word, identical — the clearest proof that "different brand" doesn't mean "different company."

The 24PetWatch link is the one that matters most in practice. When Independence Pet Holdings wound down the 24PetWatch / 24PetProtect insurance program for new business, many of those customers report being moved onto Hartville-branded policies — which is why a share of today's Hartville owners never chose Hartville at all. If that's you, skip ahead to the migration section below: what changed on the switch is the single most important thing to understand about your coverage.

So when you weigh "Hartville vs. ASPCA," you're mostly comparing plan-design and price differences between related products — not rival companies.

What Hartville Covers (and the Exclusions That Bite)

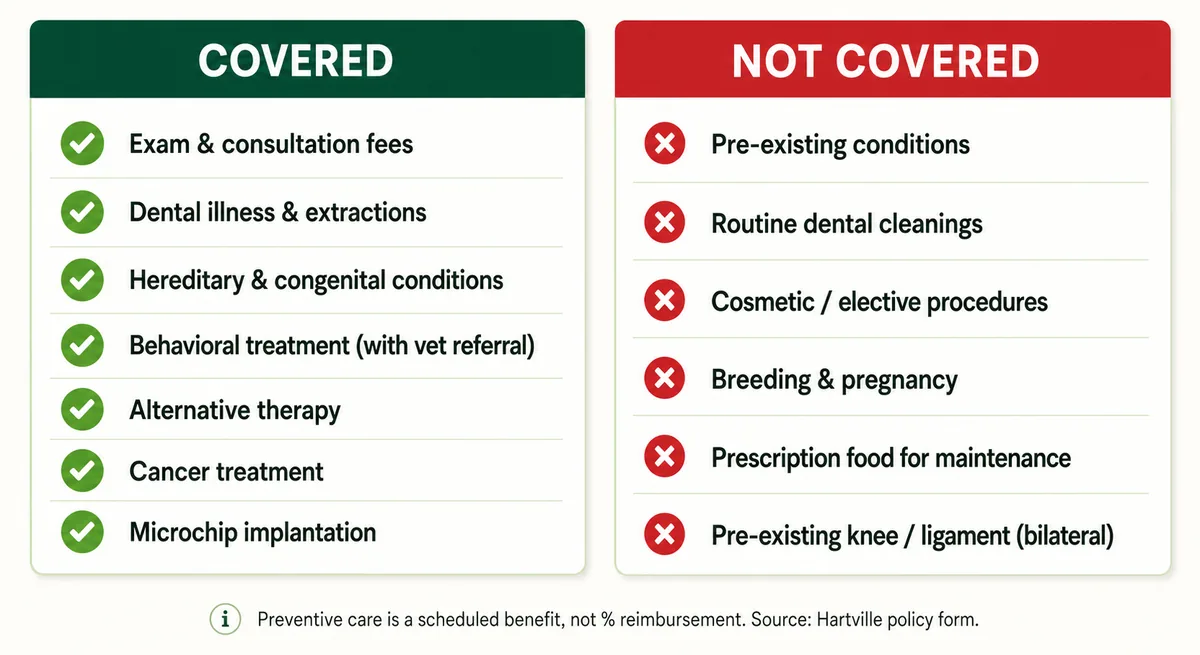

Hartville's current plan, Complete Coverage, is a genuinely broad accident-and-illness policy that reimburses a percentage of your actual vet bill — not a capped benefit table. You set the dials: 90%, 80%, or 70% reimbursement, an annual deductible of $100, $250, or $500, and an annual limit. Per Hartville's policy terms, the base plan includes:

- Exam and consultation fees for a covered accident or illness — the office-visit charge some carriers make you buy as a rider;

- Dental illness such as periodontal disease, plus tooth extractions;

- Hereditary and congenital conditions, behavioral treatment (with a vet's referral), alternative therapies, and microchip implantation.

That's a generous base plan — but "broad" isn't "everything," and a few limits catch owners off guard:

- Routine dental cleanings aren't covered — only dental illness is.

- Prescription food and supplements are covered only to treat a covered condition, never for maintenance.

- Standard exclusions apply too: pre-existing conditions, cosmetic and elective procedures, and breeding and pregnancy.

One expectation to reset: Hartville's optional Preventive Care add-on isn't percentage reimbursement — it pays a fixed dollar amount per service from a schedule of benefits, and isn't subject to your deductible or reimbursement rate. So if you're expecting "80% back" on a wellness visit, you'll be disappointed; it pays exactly what the schedule lists for each item, no more. Treat it as budgeting for routine care, not real protection against a big bill.

Waiting Period, Pre-Existing & the Knee/Ligament Trap

Hartville's waiting period is short — but the fine print around knees and ligaments is where the most painful denials come from, especially for owners who were moved over from 24PetWatch.

A flat 14-day wait

On the current Complete Coverage form (PET-P-20000-0918), coverage begins 14 days after your effective date, and that same 14-day wait covers accidents, illnesses, and orthopedic problems like knees and ligaments — as the insurer's state policy disclosures spell out. Many competitors impose a separate six- or twelve-month wait on cruciate issues; the current Hartville form doesn't. (Older "Level" (BAS) policies carried a 30-day illness and 12-month knee wait — one more reason to check which form you hold, since your declarations page and any state endorsement ultimately control.)

The knee trap: bilateral and non-curable

Here's the catch. The current form's language — published in Hartville's Notice to California Residents — treats knee and ligament conditions as bilateral: an issue on one leg is deemed to affect both, "regardless of cause." So if your pet showed any sign of a knee or ligament problem before coverage (or during the 14-day wait), both knees are treated as pre-existing. And Hartville's otherwise-generous "curable" rule — where a cured condition that's been symptom- and treatment-free for 180 days can become eligible again — explicitly does not apply to knee and ligament conditions. Once a knee or ligament condition is treated as pre-existing this way, it stays excluded for life on both sides — but a knee problem that first arises after your waiting period is covered like any other orthopedic condition.

What "pre-existing" means here

Hartville's definition is symptom-based: a condition counts as pre-existing if it first shows symptoms before coverage starts — a formal diagnosis isn't required. This is exactly the clause that catches migrated owners, whose previously-covered knee and ligament claims can be re-labeled pre-existing after the switch. It's the single biggest reason to read the migration section below before you file anything.

Legacy vs. Newer Hartville Policies: Why Two Owners Disagree

If Hartville reviews seem to contradict each other, there's a good reason: Hartville has sold pet policies on two structurally different form families, and which one you hold changes how your claims are actually paid.

Older "Level" (BAS-form) policies reimburse against "usual and customary" costs — Hartville pays a percentage not of your actual vet bill, but of a regional benchmark it calculates from ZIP-code fee data, subject to per-incident and lifetime limits. These are the plans that carry the longer 30-day illness and 12-month knee/ligament waits. An owner on one of these can pay a big bill and still be reimbursed against a smaller "customary" number.

Newer Complete Coverage (PET-P forms) reimburse a percentage of your actual invoice, up to a single annual limit, with the flat 14-day waits described above. It's the materially better structure of the two.

How do you tell which you have? Check your declarations page for two things: the policy-form number — a "BAS…" prefix means the legacy usual-and-customary design, a "PET-P-20000…" prefix means the newer invoice-based one — and the named underwriter. Two people can both say "I have Hartville" and be describing genuinely different insurance, which is exactly why a single star rating for "Hartville" tells you so little.

What Hartville Costs — Now and as Your Pet Ages

There's no single "Hartville price." What you pay depends on the deductible, reimbursement rate, and annual limit you choose, plus your pet's species, breed, age, and ZIP code. In one live 2026 quote — a young Labrador at a $5,000 annual limit, 80% reimbursement, and a $250 deductible — Complete Coverage ran about $60 a month and accident-only about $26; treat that as a single illustrative example, not a market price. The review sites that gather many quotes put Hartville's average around $55 a month for dogs and $23 for cats, while a separate NerdWallet sample came in lower, near $39 and $19. For context on what pet insurance costs across the market, NAPHIA's latest accident-and-illness average is roughly $62 a month for dogs and $32 for cats.

One quirk worth knowing before you quote: online, Hartville's annual-limit choices top out at $10,000 — its site markets an "unlimited" option, but that isn't selectable on the website, so you'd have to call for it. Multi-pet households get a 10% discount.

The part that stings: renewals

Hartville's most consistent complaint isn't denials — it's renewal increases. Premiums climb with your pet's age, breed, and local vet costs, and veterinary prices themselves are rising fast: the government's vet-services index was up about 5% over the past year. The insurer's own policy disclosure says it won't cut coverage or raise your premium because of your claims history — increases track your pet's age and local vet costs instead — but the long-term trend still points up. And if you were migrated from 24PetWatch, that increase can arrive as a one-time step-change rather than a gentle climb — more on that next. Go in budgeting for the cost to rise; that, not the intro price, is the real "is it worth it" math.

The 24PetWatch → Hartville Migration: What Transferred Owners Are Living

This is the part of any honest Hartville review that matters most in 2026. Independence Pet Holdings has wound down 24PetWatch / 24PetProtect for new business — its own site now sends new buyers to ASPCA — and transferred owners report being moved onto Hartville-branded policies with little notice and no real say. If you're one of them, read this before you file a claim or pay a renewal.

Two problems dominate the transferred-owner reviews. The first is price. Owners on Reddit and Trustpilot describe premiums jumping steeply on the switch — one reported a cat's annual premium going from about $567 to a $1,728 "replacement" quote (roughly triple), another a dog's monthly cost rising from ~$98 to $160 with no claims filed. These are owner-reported figures, not Hartville's published rates, but the pattern is consistent enough to plan around.

The second, and more damaging, is coverage that narrows on the switch — especially the knee/ligament trap from earlier. Owners describe a cruciate-ligament condition their old policy had already covered being re-classified as pre-existing "on rollover", so the follow-up surgery (a TPLO, often several thousand dollars) was denied even though coverage never lapsed. Because the current Hartville form treats knee and ligament conditions as bilateral, one affected leg can bar both.

What to do if you were migrated

- Get the paperwork. Ask Hartville for the coverage-change notice or waiver you were sent, and read your new declarations page — the policy-form number and named underwriter tell you what you actually have now.

- Appeal in writing if a previously-covered condition is denied as pre-existing; owners report that formal, documented appeals sometimes get escalated.

- Escalate to your state's Department of Insurance. Several owners have filed DOI complaints arguing that the insurer, not the customer, forced the plan change — a fair question for a regulator to weigh.

- Or switch, carefully. If your pet is now healthy and young enough, shopping a new policy may beat fighting the increase. If it already has conditions, remember that any new insurer applies its own pre-existing-condition definition and may exclude prior signs or symptoms — so compare the written terms and keep your current coverage in force until a replacement is issued and you understand its waiting periods.

Claims, Complaints & the Review-Freshness Problem

Filing a Hartville claim is straightforward — through the member portal or the "My Pet Insurance" app, with up to 270 days from treatment to submit — and the money is reimbursed to you (or to your vet, if you flag it on the form). The experience owners describe is genuinely mixed: several report claims paid smoothly "within a week," while the loudest negatives cluster around the migration, pre-existing denials, and renewal increases covered above.

The ratings are where most Hartville reviews mislead you, because they quote frozen numbers. Here's the current picture: Hartville's live Trustpilot score is 2.9 out of 5 across about 345 reviews (as of July 2026) — noticeably lower than the 3.1 or 4.2 you'll still see cited on older pages. And the "A+ BBB rating" other reviews love to mention belongs to the parent agency, PTZ Insurance Agency — which, behind that A+, shows roughly 72 complaints closed in three years and a customer-review average near 1 out of 5.

One last caveat: any NAIC or state "complaint index" you see quoted is a whole-company figure for the underwriter, which insures many brands — so there's no clean "Hartville" complaint rate to cite. Read the pattern of sentiment, dated, rather than a single score.

Hartville vs. the Alternatives (ASPCA, Spot, Lemonade)

If Hartville isn't the right fit — or you're a migrated owner weighing a move — here's how it stacks up against the carriers people cross-shop most.

- vs ASPCA: Barely a contest, because they're the same platform. ASPCA Pet Health Insurance uses the same producer and underwriters as Hartville, so the coverage is nearly identical — you're comparing quotes and wellness options, not companies.

- vs Spot: Another Independence Pet Holdings sibling on the same two carriers, so the core policy is very similar. With the underlying coverage this close, price and plan limits for your specific pet usually decide it — so if you like Hartville's design but not its number, pull a Spot quote at identical settings and compare like for like.

- vs Lemonade: A genuinely different company — app-first, often cheaper for a young pet, with fast AI claims — but it caps enrollment age and gates exam fees and dental behind add-ons. For a senior pet or someone who wants breadth built in, Hartville wins; for a young pet on a budget, Lemonade often does.

The short version: if you want breadth and don't mind the paperwork, Hartville is defensible; if you're chasing price or escaping the migration, Spot or Lemonade deserve a quote first.

Frequently Asked Questions

Is Hartville pet insurance still available in 2026?

Yes. As of 2026, Hartville still quotes and sells new accident-and-illness policies on its own website — it isn't a closed or renewal-only book. It's also the brand tied to the discontinued 24PetWatch / 24PetProtect program, and many current Hartville policyholders report being moved over rather than choosing it directly.

Is Hartville pet insurance worth it?

It depends on your priorities. Hartville's Complete Coverage plan is genuinely broad — it reimburses your actual vet bill and builds in exam fees, dental-illness treatment, and hereditary conditions. But it isn't the cheapest, premiums climb steeply with age, and its knee/ligament and pre-existing rules bite. It's a defensible pick for a healthy pet whose owner values breadth over the lowest price.

Who underwrites Hartville pet insurance?

"Hartville" is a brand. Policies are produced by PTZ Insurance Agency and underwritten by either Independence American Insurance Company (NAIC #26581, AM Best A-) or United States Fire Insurance Company (NAIC #21113, AM Best A+), depending on your state and policy form. Hartville doesn't publish a state-by-state map, so the only way to know your carrier is to read your declarations page.

Is Hartville the same company as ASPCA or 24PetWatch?

Effectively, yes — they're brands on one platform. Hartville, ASPCA Pet Health Insurance, and 24PetProtect share the same producer, the same two underwriters, and the same parent, Independence Pet Holdings. 24PetWatch's insurance program was wound down and its customers moved into Hartville policies, which is why the two names come up together so often.

What does Hartville pet insurance cover?

Hartville's Complete Coverage plan covers accidents and illnesses, including exam and consultation fees, dental illness, hereditary and congenital conditions, behavioral treatment (with a vet referral), alternative therapies, and microchipping. It does not cover pre-existing conditions, routine dental cleanings, cosmetic or elective procedures, or breeding. Its optional Preventive Care add-on pays routine care from a fixed benefit schedule, not a percentage.

What is Hartville's reimbursement rate?

On the current Complete Coverage plan you choose a reimbursement rate of 90%, 80%, or 70%. Hartville pays that percentage of your actual covered vet bill after you meet your annual deductible ($100, $250, or $500), up to your annual limit. Older "Level" policies instead reimbursed against a regional "usual and customary" benchmark, which can pay out less.

Why did my Hartville premium jump or my claim get denied after switching from 24PetWatch?

When 24PetWatch's program ended, customers were re-papered onto Hartville forms — and owners report premiums rising steeply (sometimes 2–3×) and terms narrowing on the switch. Most damaging: a knee or ligament condition your old policy covered can be re-classified as pre-existing "on rollover." If that happens, request your coverage-change notice, appeal in writing, and consider a complaint to your state's Department of Insurance.

Does Hartville cover pre-existing conditions or knee surgery?

Hartville doesn't cover pre-existing conditions, which it defines by symptoms rather than a formal diagnosis. A curable condition that's been symptom- and treatment-free for 180 days can become eligible again — but that grace does not apply to knee and ligament conditions, which Hartville treats as bilateral. So a single sign of a knee or cruciate problem before coverage can bar both legs for life.

Sources

- Hartville Pet Insurance — Underwriting Disclosure (dual underwriters, PTZ producer) — Hartville / PTZ Insurance Agency

- Hartville Pet Insurance — Using Your Coverage FAQs (270-day filing; pay owner or vet) — Hartville / PTZ Insurance Agency

- Crum & Forster upgraded to A+ (Superior) by AM Best (US Fire) — PR Newswire / Crum & Forster

- AM Best affirms Independence American A- after $125M parent contribution — Insurance Journal

- Hartville Pet Insurance — Our Plans (Complete Coverage: 90/80/70%, deductibles, invoice-based) — Hartville / PTZ Insurance Agency

- Hartville Pet Insurance — Notice to California Residents (bilateral knee/ligament; 180-day curable carve-out; legacy vs new forms) — Hartville / PTZ Insurance Agency

- Hartville Pet Insurance Review (averages, deductibles, limits) — MoneyGeek

- Hartville Pet Insurance Review (sample quotes) — NerdWallet

- State of the Industry Report 2025 (US A&I average premiums) — NAPHIA

- CPI — veterinary services (12-month change, June 2026) — U.S. Bureau of Labor Statistics

- Premium tripling with change from 24PetWatch to Hartville (owner reports; migration notice) — Reddit — r/petinsurancereviews

- Hartville denying TPLO claim after 24PetHealth→Hartville switch (knee/ligament re-classified pre-existing on rollover) — Reddit — r/Insurance

- Hartville Pet Insurance — Trustpilot (live 2.9/5, ~345 reviews, July 2026) — Trustpilot

- PTZ Insurance Agency, Ltd. — BBB profile (A+/accredited; ~72 complaints/3yr; ~1/5 customer reviews) — Better Business Bureau

- Delaware Insurer Disclosure of Important Policy Provisions (PET-DE-Notice-0124-APHI): 14-day waiting period; symptom-based pre-existing; no premium increase for claims history — Independence American Insurance Company / Hartville (APHI)

- 24PetProtect — new buyers directed to ASPCA (insurance program wound down for new business) — 24PetProtect / PTZ Insurance Agency