If you're weighing Pumpkin Pet Insurance, you're probably asking the only question that really matters: is it worth it? The honest answer is that it depends on your pet and your budget — Pumpkin buys unusually broad coverage, but you pay for that breadth, and the price climbs as your pet gets older. We read Pumpkin's actual policy, its underwriters' financial-strength ratings, and the reviews real owners leave, so you don't have to.

Here's the short version. Pumpkin sells a single accident-and-illness plan — not a menu of "Plus" and "Elite" tiers — that reimburses 80% or 90% of covered vet bills, builds in exam fees and dental-illness treatment that many rivals charge extra for, offers an unlimited annual-payout option, and sets no upper age limit to enroll. Pumpkin's own FAQ confirms each of those points.

That breadth is real — and so is the fine print. Two of the three things "Pumpkin" actually sells aren't insurance at all, your policy is backed by one of two different carriers depending on your state, and Pumpkin's short waiting period doesn't protect the one orthopedic claim owners worry about most. This review decodes all of it in plain English, then gives you a conditional verdict: who Pumpkin genuinely fits, and who should look elsewhere.

Table of Contents

- The Verdict: Who Pumpkin Fits, and Who Should Skip It

- Who Actually Underwrites Pumpkin (and Are They Solid)?

- What 'Pumpkin' Actually Sells: Insurance vs. Two Non-Insurance Products

- What Pumpkin Covers That Rivals Charge Extra For

- Waiting Period and the Knee/Ligament Trap

- What Pumpkin Costs — Now and as Your Pet Ages

- PumpkinNow: Fast Pay, With Real Limits

- Claims, Complaints, and Customer Experience

- Pumpkin vs. Lemonade, Trupanion, and Spot

- Frequently Asked Questions

- Sources

The Verdict: Who Pumpkin Fits, and Who Should Skip It

Pumpkin's reputation among owners is consistent: it tends to cover more and deny less than most rivals, and it charges accordingly. Across the Pumpkin threads we read on r/petinsurancereviews, the recurring line is "you get what you pay for" — broad, claim-friendly coverage at a price that climbs as the pet ages. So the question isn't whether Pumpkin is good; it's whether that trade fits your situation.

Pumpkin is a strong fit if you:

- are insuring an older or newly adopted pet — there is no upper age limit to enroll, so seniors aren't turned away;

- want breadth without buying up — exam fees, dental-illness treatment, behavioral care, and alternative therapies are built into the base plan rather than sold as paid add-ons;

- worry about affording a big emergency bill up front, and would value PumpkinNow's fast, point-of-care payments (we dig into how that really works below).

Look elsewhere if you:

- are shopping mainly on price — Pumpkin's sample premiums sit toward the higher end of the market, and the gap widens as your pet ages;

- have a pet with an existing knee or ligament problem, or another chronic condition — Pumpkin's pre-existing and bilateral rules will bite no matter how good the plan looks;

- mostly want routine-care reimbursement — that lives in Pumpkin's separate wellness products, which are not insurance.

If you're somewhere in between — a healthy young pet and a flexible budget — Pumpkin is a defensible, if pricey, choice. The rest of this review settles the two things that should decide it: who actually stands behind your policy, and how Pumpkin's fine print treats the claims you're most likely to file.

Who Actually Underwrites Pumpkin (and Are They Solid)?

Here's the part most reviews skip: Pumpkin isn't an insurance company. "Pumpkin" is a licensed agency — Pumpkin Insurance Services Inc. (National Producer Number 19084749) — that sells and services the policy but doesn't carry the risk. Your claims are paid by one of two separate carriers named on your policy documents.

Pumpkin's own disclosure states that policies are underwritten by "either Independence American Insurance Company or United States Fire Insurance Company," depending on your state. That matters, because the two carriers aren't equally strong. United States Fire (NAIC #21113), a Crum & Forster company, was upgraded to an AM Best "A+ (Superior)" rating in September 2025. Independence American (NAIC #26581) sits two notches lower at "A- (Excellent)" — and spent part of 2025 under review over a pet-reinsurance accounting issue, resolved only after its parent added $125 million in capital. Both are financially sound; just know which one is on your policy, and read the rating against that carrier, not the "Pumpkin" brand.

The corporate family tree also answers a question owners often ask — is Pumpkin the same company as Spot or ASPCA? Effectively, yes — they're corporate siblings. Pumpkin (originally launched with backing from animal-health giant Zoetis) now sits inside Independence Pet Holdings, the JAB-owned platform that also runs Spot, ASPCA, Figo, AKC, Pets Best, and Embrace. (United States Fire, by contrast, rolls up to Fairfax Financial — so a Pumpkin policy can be backed by a different corporate parent than the brand itself.) If you're cross-shopping Pumpkin against Spot or ASPCA, you're largely comparing siblings on shared infrastructure.

What 'Pumpkin' Actually Sells: Insurance vs. Two Non-Insurance Products

When people say "Pumpkin," they usually mean three different products — and only one of them is insurance. Keeping them straight is the difference between buying real protection and buying a routine-care budgeting tool.

1. The accident-and-illness plan is the actual insurance: the regulated policy, underwritten by the carriers above, that reimburses 80% or 90% of covered vet bills. When we talk about a "Pumpkin review," this is what we mean.

2. Preventive Essentials is an optional add-on that refunds routine care — the annual wellness exam, vaccines, and a parasite test. Pumpkin states plainly that it is "NOT INSURANCE, nor a regulated product," that you can only add it to an existing Pumpkin insurance policy, and that it isn't sold in California, Maine, Missouri, Montana, Rhode Island, Vermont, or Washington.

3. The Pumpkin Wellness Club is a separate, standalone membership — also not insurance — run by a Pumpkin subsidiary, Sprout Wellness Services LLC, starting around $15.95 a month for cats and $20.95 for dogs. Unlike Preventive Essentials, you can buy it without any insurance at all.

So is the wellness coverage "worth it"? Treat it as budgeting, not risk transfer: you're pre-paying for predictable routine costs and getting a set dollar amount back, not protecting against a $7,000 surprise. If you'd rather not front and track those small bills, it can be convenient — but it shouldn't sway how you judge the insurance itself.

What Pumpkin Covers That Rivals Charge Extra For

Pumpkin's real selling point is breadth: several things other insurers gate behind paid add-ons are built into its single base plan. Per Pumpkin's coverage terms, the accident-and-illness plan includes:

- Vet exam fees for a covered accident or illness — the office-visit charge many carriers make you buy as a separate rider;

- Dental illness such as periodontal (gum) disease, including the exam, X-rays, and treatment;

- Behavioral treatment (with a vet's referral), hereditary and congenital conditions, alternative therapies like acupuncture and hydrotherapy when a vet performs them, and microchip implantation.

That's a genuinely generous base plan. But "broad" isn't "everything," and a few limits catch owners off guard:

- Routine dental cleanings aren't covered — only dental illness is. If a cleaning turns up disease, treating the disease can be covered; the cleaning itself is not.

- Prescription food and supplements are covered only to treat a covered condition, never for general maintenance or weight loss.

- Standard exclusions apply too: pre-existing conditions, spay/neuter and other elective procedures, breeding and pregnancy, and routine parasite prevention (that last one lives in the wellness add-on, not the insurance).

The takeaway: if exam fees, dental-illness care, and alternative therapies matter to you, Pumpkin hands you more in the base plan than most rivals do — just don't mistake the wellness-style extras like cleanings and parasite prevention for insurance coverage.

Waiting Period and the Knee/Ligament Trap

Pumpkin's waiting period is genuinely one of its strongest features — with a catch buried in the knee fine print that trips up a lot of owners.

A single 14-day wait, even for knees and hips

Coverage begins 14 days after your policy's effective date, and that same 14 days applies to accidents, illnesses, and — unusually — orthopedic conditions like knee, ligament, and hip problems. Many competitors impose a separate six-month wait on cruciate-ligament (ACL/CCL) issues; Pumpkin doesn't. And to clear up a common myth: Pumpkin does not "exclude knee conditions entirely." A cruciate tear that first shows up after day 14, with no earlier signs, can be a covered claim.

The knee trap: bilateral and non-curable

Here's where the short wait gives with one hand and takes with the other. Pumpkin's policy treats knee and hind-leg ligament conditions as bilateral — an issue on one leg is deemed to affect both, "regardless of cause." So if your dog showed any sign of a knee or hind-leg ligament problem before coverage (or during the 14-day wait), both knees are treated as pre-existing.

And Pumpkin's otherwise-generous "curable" rule — where a cured condition that has been symptom- and treatment-free for 180 days can become eligible again — explicitly does not apply to knee and hind-leg ligament conditions. Once a knee is flagged pre-existing, it stays that way for life.

What "pre-existing" means here

Pumpkin's definition is symptom-based: a condition counts as a pre-existing condition if it "first occurs or shows symptoms" before coverage starts — a formal diagnosis isn't required. None of this means you should delay a vet visit to protect a future policy; get your pet the care they need, and buy coverage as early as you can, ideally before any symptoms appear.

What Pumpkin Costs — Now and as Your Pet Ages

There's no single "Pumpkin price." What you pay depends heavily on the deductible, reimbursement rate, and annual limit you choose, plus your pet's species, breed, age, and ZIP code — so treat any headline average with caution.

Sample prices, and why they vary so much

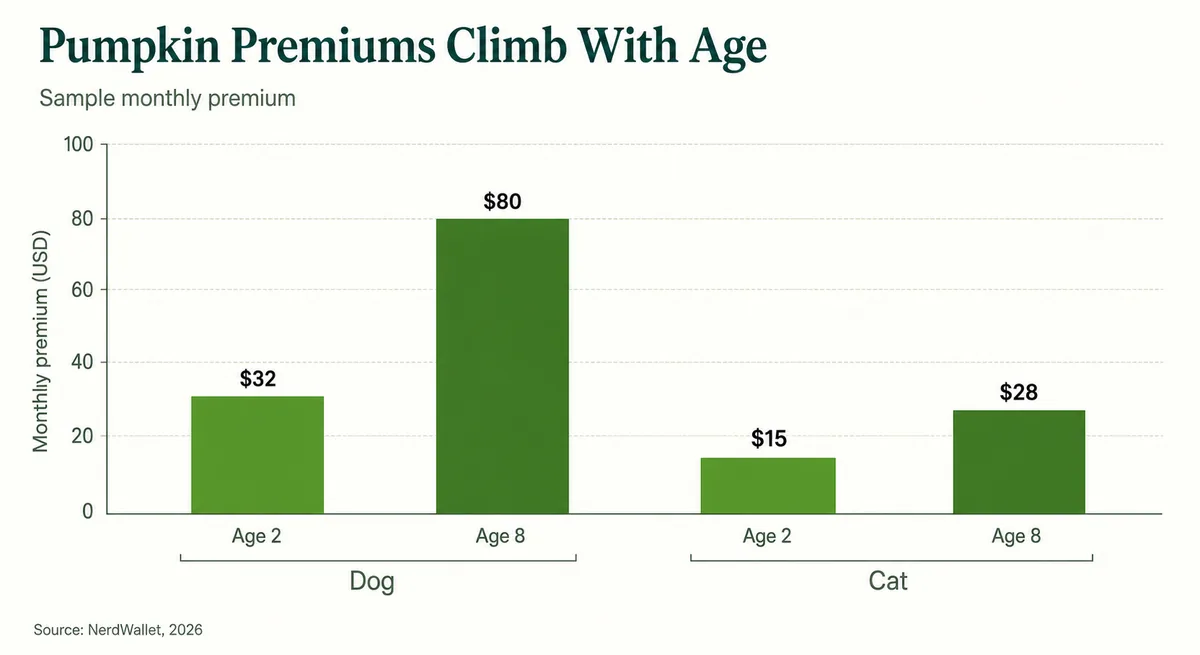

In one 2026 sample — a Texas quote at a $250 deductible, 80% reimbursement, and a $5,000 annual limit — NerdWallet found a medium mixed-breed dog running about $32 a month at age 2 and $80 at age 8, and a domestic shorthair cat about $15 rising to $28; a French Bulldog on the same terms hit $64 and $158. For context, NAPHIA's latest industry average for accident-and-illness coverage is roughly $70 a month for dogs and $36 for cats. Pumpkin can land under that for a young pet or well above it for a senior or a high-limit plan.

The part that stings: renewals

Pumpkin's most consistent complaint isn't denials — it's renewal increases. Owners on r/petinsurancereviews describe premiums climbing steeply as pets age: one insured a Golden Retriever at $53 a month and watched it reach $96 by year three, and senior-pet quotes above $300 a month come up repeatedly. Pumpkin is a property-and-casualty product, so your rate rises with age, breed, and local vet costs — not, currently, with your claims. The trap is that once your pet develops conditions, those become pre-existing everywhere else, so you can't easily switch to escape the increase. Go in expecting the long-term cost to climb; that, not the intro price, is the real "is it worth it" math.

Which annual limit should you actually buy?

Pumpkin's own claims data helps here: among customers who filed at least one claim, only 1.69% of dogs had annual claims over $10,000, and only 2.92% of cats over $7,000. A standard limit covers most owners just fine — but if you have a breed prone to cancer, orthopedic surgery, or foreign-body emergencies, the higher or unlimited tier is the more rational bet.

PumpkinNow: Fast Pay, With Real Limits

PumpkinNow is Pumpkin's answer to the biggest frustration with reimbursement insurance: you normally pay the whole vet bill up front and wait to be paid back. It's a genuine differentiator — with fine print worth understanding before you count on it.

Per Pumpkin's own terms, for an eligible accident or illness claim of $500 or more, PumpkinNow can send up to 90% of the covered amount to your bank account in as little as 15 minutes — ideally before you check out at the vet. Pumpkin reports it paid more than $4.6 million to over 3,200 pets in its first few months after launching in April 2025, with some claims cleared in about two minutes (those are Pumpkin's own figures).

Two catches keep it from being magic. First, it pays you, not the vet — so you still need a way to cover the bill at the counter, and the near-instant funding only works if your bank supports real-time payments. Second, the eligibility floor started at $1,000 and is now $500, so smaller bills don't qualify. If you genuinely couldn't front a large emergency bill, a carrier like Trupanion that pays the vet directly may fit you better. Used within its limits, though, PumpkinNow is one of the more useful features in the category — and a real reason some owners accept Pumpkin's higher price.

Claims, Complaints, and Customer Experience

Filing a Pumpkin claim is straightforward: submit through your online Member Center, by email, or have your vet send it, along with the itemized invoice, and you're reimbursed by check or direct deposit for the 80% or 90% of covered costs your plan pays. One gap worth noting: Pumpkin has no mobile app, so everything runs through the web.

Aggregate scores skew positive — Pumpkin holds around 4.8 out of 5 on Trustpilot across thousands of reviews — but the pattern in the negatives is worth knowing. On the Better Business Bureau profile for Pumpkin Insurance Services and in Reddit threads, the recurring gripes are consistent: claims denied as pre-existing (especially for repeat GI, ear, or eye issues), renewal price increases, and occasional cancellation or double-billing friction. These are owner reports, not verified rates — but they cluster where most pet-insurance complaints do.

One caveat on the "official" numbers: you may see a NAIC complaint index quoted for Pumpkin's underwriters. Read it skeptically. Those indexes measure an entire insurance company across every product it writes — and Independence American and United States Fire each back several brands beyond Pumpkin — so no published index isolates the Pumpkin pet experience. Treat any single "Pumpkin complaint rate" you come across as a whole-company artifact, not a clean signal.

Pumpkin vs. Lemonade, Trupanion, and Spot

Pumpkin's broad-but-pricey profile shows up clearly against the carriers owners cross-shop most. Here's how the plans differ on the things that actually change the decision:

| Feature | Pumpkin | Lemonade | Trupanion | Spot |

|---|---|---|---|---|

| Reimbursement | 80% / 90% | 70–90% | 90% (fixed) | 70–90% |

| Deductible type | Annual | Annual | Per-condition (lifetime) | Annual |

| Exam fees in base plan | Yes | Add-on | No | Yes |

| Unlimited annual limit | Yes | No | Unlimited only | Yes |

| Separate orthopedic wait | None (14 days) | 30 days | Varies by state | None (14 days) |

| Upper age limit to enroll | None | ~Age 14 | ~Age 14 | None |

| Pays the vet directly | No (PumpkinNow pays you) | No | Yes | No |

Rival plan terms above reflect each carrier's current published plans and can vary by state and plan tier, so confirm the specifics on each carrier's own site before you buy.

What that means in practice:

- vs Lemonade: Lemonade usually starts cheaper and has a slick app, but it caps enrollment age and charges extra for exam fees and dental illness. For a senior pet or someone who wants breadth built in, Pumpkin wins; for a young pet on a tight budget, Lemonade often does.

- vs Trupanion: Trupanion pays your vet directly and doesn't cover exam fees — nearly the mirror image of Pumpkin. If fronting a big bill is your worry and your vet supports it, lean Trupanion; if you want exam fees and lower entry pricing, lean Pumpkin.

- vs Spot: These are corporate siblings on the same two carriers, so the core coverage is very similar — though the dials differ. Spot adds a cheaper 70% reimbursement tier and a lower limit floor, so it can undercut Pumpkin on price — worth a quote if you like Pumpkin's design but not its cost.

The short version: your pet's age, your budget, and whether you need direct-to-vet payment are what actually decide it.

Frequently Asked Questions

Is Pumpkin a good pet insurance company?

Pumpkin is a strong choice if you value broad coverage over the lowest price. Its single accident-and-illness plan builds in exam fees, dental-illness treatment, and alternative therapies that many rivals charge extra for, and it sets no upper age limit to enroll. The trade-offs are a premium that starts higher and climbs steeply as your pet ages, plus a knee/ligament rule that can trip up orthopedic claims. For a healthy pet whose owner wants breadth and claim-friendliness, it's a defensible pick.

Does Pumpkin Pet Insurance pay the vet directly?

Not by default — Pumpkin is a reimbursement plan, so you normally pay the vet and get paid back. Its PumpkinNow feature can send up to 90% of an eligible claim of $500 or more to your bank account within minutes, but that money goes to you, not the clinic, and only funds instantly if your bank supports real-time payments. If direct-to-vet payment is essential, a carrier like Trupanion is built around it.

Which is better, Trupanion or Pumpkin?

It depends on how you want to pay. Trupanion pays your vet directly, uses a per-condition lifetime deductible, and fixes reimbursement at 90% — but it doesn't cover exam fees. Pumpkin includes exam fees, lets you choose your deductible and reimbursement rate, and tends to start cheaper, but it pays you back rather than the vet. Choose Trupanion if fronting a large bill worries you; choose Pumpkin if you want exam-fee coverage and lower entry pricing.

How much does Pumpkin pet insurance cost?

There's no single price — it depends on your deductible, reimbursement rate, and annual limit, plus your pet's species, breed, age, and location. In one 2026 sample, a young mixed-breed dog ran about $32 a month and a domestic shorthair cat about $15 — both climbing steeply by age eight (to roughly $80 and $28), and high-limit or senior plans cost considerably more. Expect the premium to rise as your pet ages.

Does Pumpkin cover pre-existing conditions?

No — like every pet insurer, Pumpkin excludes pre-existing conditions, which it defines by symptoms rather than a formal diagnosis. It is more generous than some on curable conditions: one that has been symptom- and treatment-free for 180 days can become eligible again. But that grace does not apply to knee and hind-leg ligament conditions, which stay excluded once flagged. Enroll before any symptoms appear to keep the most coverage.

Is Pumpkin's Preventive Essentials worth it?

Only if you'd actually use it. Preventive Essentials isn't insurance — it's an optional add-on that refunds a set list of routine care, such as the wellness exam, vaccines, and a parasite test. Treat it as budgeting: you pre-pay for predictable costs and get a fixed amount back, not protection against a big surprise. It can be convenient if you'd rather not track small bills, but it shouldn't factor into whether the insurance itself is worth buying.

Does filing a claim raise my Pumpkin premium?

Not directly — Pumpkin says claims themselves don't change your rate. But it's a property-and-casualty product, so your premium still rises with your pet's age, breed, and local vet costs, which is why owners report steep increases over time. A company can also change how it rates in the future. So while a single claim won't spike your bill, plan on the overall cost climbing as your pet gets older.

Is Pumpkin the same company as ASPCA or Spot?

They're corporate siblings. Pumpkin, Spot, ASPCA, Figo, and several other brands sit under Independence Pet Holdings, the JAB-owned platform, and Pumpkin's policies are underwritten by the same carriers that back some of those brands. That's why the coverage often looks alike. If you're comparing Pumpkin with Spot or ASPCA, you're mostly weighing plan-design and price differences between related products, not rival companies.

Sources

- Pumpkin Pet Insurance FAQ — Pumpkin

- r/petinsurancereviews — Pumpkin owner discussions — Reddit

- Pumpkin underwriting disclosure — Pumpkin

- Crum & Forster upgraded to A+ (Superior) by AM Best — PR Newswire / Crum & Forster

- AM Best affirms Independence American, $125M parent contribution — Insurance Journal

- JAB's pet-insurance platform acquires Pumpkin — BusinessWire

- Pumpkin Preventive Essentials (dog) — Pumpkin

- Pumpkin Wellness Club — Pumpkin / Sprout Wellness Services

- Pumpkin sample policy / sample plan — Pumpkin

- Pumpkin Pet Insurance Review (sample premiums) — NerdWallet

- How much is pet insurance? (NAPHIA averages) — NerdWallet

- Pumpkin References (claims-adequacy data) — Pumpkin

- PumpkinNow urgent-pay — Pumpkin

- A claim paid in 2 minutes with PumpkinNow (3,200+ pets, $4.6M) — PR Newswire / Pumpkin

- Pumpkin Pet Insurance reviews — Trustpilot

- Pumpkin Insurance Services Inc. — BBB complaints — Better Business Bureau